If you need to access retirement funds before age 59½ without paying the 10% IRS penalty, there are legal ways to do so. The most common options include:

- Rule of 55: Withdraw from your current employer’s 401(k) or 403(b) penalty-free if you leave your job in or after the year you turn 55 (50 for public safety employees). Regular income tax still applies.

- Substantially Equal Periodic Payments (SEPP): Take consistent withdrawals from an IRA or 401(k) under IRS Rule 72(t). Payments must follow strict rules for at least five years or until you turn 59½.

- Roth IRA Contributions: Withdraw contributions (not earnings) anytime, tax- and penalty-free.

- Penalty Exceptions: Situations like unreimbursed medical expenses, first-time home purchases (up to $10,000), or qualified births/adoptions (up to $5,000) allow penalty-free withdrawals.

Each method has specific rules and risks, such as triggering retroactive penalties for SEPP errors. Proper planning is essential to avoid costly mistakes and minimize taxes. Tools like Mezzi can help automate calculations and identify applicable exceptions to make the process easier.

How to Withdraw from Your IRA Before 59½ Without a Penalty

The 10% Early Withdrawal Penalty Explained

Most retirement accounts come with an extra 10% tax on withdrawals made before you turn 59½. This penalty is in addition to your regular income tax.

"Generally, the amounts an individual withdraws from an IRA or retirement plan before reaching age 59½ are called 'early' or 'premature' distributions. Individuals must pay an additional 10% early withdrawal tax unless an exception applies."

– Internal Revenue Service

The combination of taxes and penalties can significantly reduce the amount you actually receive. For instance, if you're in the 22% tax bracket and withdraw $40,000 early, you could lose over $12,800 to taxes and penalties. Beyond the immediate cost, early withdrawals also hurt your long-term savings potential, as explained below.

Purpose of the Penalty

The IRS imposes this penalty to discourage people from tapping into their retirement savings prematurely. Early withdrawals not only shrink your current balance but also rob you of future growth. For example, withdrawing $5,000 today could cost you over $28,000 in lost savings after 30 years, assuming a 6% annual return.

"This is designed to discourage people from dipping into retirement funds before their time is due, ensuring the account serves its intended purpose."

– Jacob Dayan, CEO, Community Tax, LLC

It's important to note that the penalty applies only to the taxable portion of your withdrawal. To report the penalty, you'll need to file IRS Form 5329. Unfortunately, this penalty isn't deductible on your tax return.

Which Accounts Are Subject to the Penalty

Most tax-advantaged retirement accounts are subject to the 10% early withdrawal penalty, but the rules can vary depending on the type of account. Here's a quick breakdown:

| Account Type | Early Penalty Rate | Special Notes |

|---|---|---|

| Traditional IRA | 10% | Includes SEP-IRAs |

| 401(k) / 403(b) | 10% | Applies to both traditional and Roth versions |

| SIMPLE IRA | 25% | Higher penalty during the first 2 years of participation; drops to 10% afterward |

| Roth IRA | 10% | Penalty applies only to earnings; contributions are always accessible without penalty |

| Governmental 457(b) | 0% | Generally exempt unless funds are rolled in from another plan type |

One key exception is the SIMPLE IRA, which carries a steeper 25% penalty if you withdraw funds within the first two years of participation. On the other hand, governmental 457(b) plans usually avoid the early withdrawal penalty altogether, unless you've rolled in funds from another retirement plan.

Roth IRAs are treated a bit differently. The IRS assumes that withdrawals come from your contributions first, which means you can access that portion of your account anytime, tax- and penalty-free. The 10% penalty only kicks in if you withdraw earnings before age 59½ and before the account has been open for at least five years.

3 Ways to Access Retirement Funds Without Penalty

If you need to tap into your retirement funds before turning 59½, there are a few IRS-approved ways to do so without facing the usual 10% penalty. Here’s a closer look at three strategies.

Rule of 55 for 401(k) Withdrawals

The Rule of 55 lets you withdraw from your current employer’s 401(k) or 403(b) without penalties if you leave your job in or after the year you turn 55. While you’ll avoid the penalty, regular income tax still applies. This rule only applies to your current employer’s plan - not IRAs or accounts from past employers. If you have funds from a previous employer, you’ll need to roll them into your current plan before leaving your job to take advantage of this option. Keep in mind, not all employer-sponsored plans offer Rule of 55 withdrawals, so it’s essential to check with your plan administrator.

For public safety employees, including police officers, firefighters, EMTs, air traffic controllers, and FBI agents, this rule kicks in earlier - starting at age 50.

"The rule of 55 is an IRS provision that allows workers who leave their job to withdraw funds from an employer-sponsored retirement account without incurring a penalty, though they must still pay income tax on withdrawals."

– Vision Retirement

Substantially Equal Periodic Payments (SEPP)

If your retirement plan doesn’t qualify for the Rule of 55, the SEPP method, based on IRS Rule 72(t), might be an option. This approach allows penalty-free withdrawals from an IRA or 401(k) as long as you’re no longer employed by the plan’s sponsor. SEPP requires you to take consistent, equal payments for at least five years or until you turn 59½ - whichever is longer. You can choose from three IRS-approved calculation methods: Required Minimum Distribution (RMD), Fixed Amortization, or Fixed Annuitization.

However, SEPP comes with strict rules. Once you start, you can’t make additional contributions, roll funds over, or take extra withdrawals. Changing or stopping the payment schedule early triggers a retroactive 10% penalty (called a recapture tax), which can be costly.

"SEPP plans require consistent withdrawals for at least five years or until age 59½, whichever is longer, using one of three approved calculation methods."

– Investopedia

It’s a good idea to consult with a Certified Financial Planner, tax expert, or use AI tools for retirement withdrawal planning before committing to a SEPP plan to avoid costly mistakes.

Withdrawing Roth IRA Contributions

Roth IRAs provide some flexibility for early withdrawals. You can take out your original contributions at any time without taxes or penalties. This is because Roth IRA withdrawals are processed in a specific order: contributions first, followed by conversions, and finally earnings. However, if you withdraw earnings before age 59½ and before the account has been open for five years, those earnings will be taxed and penalized.

It’s important to note that once you withdraw contributions, you typically can’t put that money back, unless it’s done within the same tax year and within the annual contribution limits.

"You can withdraw your Roth IRA contributions at any time, tax- and penalty-free, regardless of how long the account has been open."

– Hartford Funds

IRS Penalty Exceptions for Specific Situations

The IRS recognizes that life can throw curveballs, which is why they provide penalty waivers for certain hardship situations. While withdrawals from traditional retirement accounts are still subject to ordinary income tax, the 10% early withdrawal penalty can be avoided if you meet specific criteria.

Medical and Health-Related Exceptions

If your unreimbursed medical expenses exceed 7.5% of your adjusted gross income (AGI), you may qualify for a penalty waiver. For example, with an AGI of $80,000, you’d need to cover the first 7.5% (or $6,000) yourself. Any unreimbursed expenses above that threshold - like doctor visits, hospital stays, prescription drugs, or long-term care insurance premiums - can qualify for the waiver.

Additionally, if you are deemed totally and permanently disabled or have a terminal illness, as confirmed by a physician, the 10% penalty does not apply to your withdrawals.

Another health-related exception applies if you’ve received unemployment compensation for 12 consecutive weeks. In this case, you can make penalty-free withdrawals from your IRA to pay for health insurance premiums.

But the exceptions don’t stop at health-related hardships. There are also provisions for home purchases and family needs.

Home Purchase and Family Exceptions

If you’re buying your first home, you can withdraw up to $10,000 from an IRA without triggering the penalty (note: this exception doesn’t apply to 401(k) plans). You’re considered a first-time homebuyer if you haven’t owned a primary residence in the two years leading up to the purchase.

"The definition of 'first-time homebuyer' in this case is broader than you might think. You qualify as a first-time homebuyer so long as you had no ownership interest in a main home any time within two years before the date you acquire your new home."

– Stephen Fishman, J.D., Nolo

Other family-related exceptions include:

- Penalty-free withdrawals of up to $5,000 per parent for each birth or adoption.

- Distributions of up to $1,000 for personal or family emergencies.

- Withdrawals up to $22,000 for disaster recovery expenses.

Additionally, victims of domestic abuse can access the lesser of $10,000 or 50% of their account balance penalty-free.

To ensure you qualify for these waivers, make sure to file IRS Form 5329 and include all necessary documentation to support your claim.

How Mezzi Helps You Access Funds Without Penalties

Navigating the complex IRS rules for penalty-free withdrawals can feel like a daunting task, especially when dealing with SEPP (Substantially Equal Periodic Payments) calculations or figuring out which exceptions apply to you. Mezzi simplifies this process by securely connecting to your retirement accounts through read-only access using trusted platforms like Plaid and Finicity. With AI-powered analysis, Mezzi identifies opportunities you might otherwise overlook. Here's how it streamlines SEPP calculations, highlights penalty exceptions, and refines your tax strategy.

SEPP Calculation and IRS Compliance

Mezzi employs AI-driven tools to handle the three IRS-approved SEPP methods: Required Minimum Distribution (RMD), Fixed Amortization, and Fixed Annuitization. These tools automatically integrate current IRS life expectancy tables and interest rates to create compliant payment schedules.

For example, let’s say you’re 50 years old with a $500,000 IRA balance and opt for the RMD method using a 4.2% interest rate. Mezzi calculates annual payments of approximately $22,000. The platform ensures these payments align with IRS Section 72(t) rules, simulating the schedule for the required period - either five years or until you turn 59.5, whichever is longer. This helps you avoid modification penalties.

Once your SEPP plan is configured, Mezzi generates IRS Form 5329-ready documentation, so you’re prepared for tax filing. It also flags potential risks, like switching methods mid-plan, which could result in retroactive penalties on all prior distributions. Beyond SEPP, Mezzi’s analysis extends to identifying penalty exceptions tailored to your financial situation.

Identifying Penalty Exceptions

Mezzi’s system digs into your financial data to pinpoint IRS penalty exceptions that apply to you. By cross-referencing tax returns, medical expenses, mortgage records, and other documents, it evaluates your eligibility under IRS Section 72(t).

For instance, if your unreimbursed medical expenses exceed 7.5% of your adjusted gross income (AGI), Mezzi identifies this as a qualifying exception. With an AGI of $100,000 and $12,000 in medical bills, the platform determines you can access $12,000 from your retirement accounts without penalties.

It doesn’t stop there. Mezzi also highlights lesser-known exceptions, like penalty-free withdrawals for qualified birth or adoption expenses or distributions for reservists. For example, a new parent with a $200,000 IRA might use Mezzi to withdraw funds penalty-free and receive detailed instructions for filing IRS Form 5329.

Tax-Efficient Withdrawal Planning

Beyond helping you avoid penalties, Mezzi optimizes your withdrawal strategy to minimize taxes. The platform models different scenarios, sequencing withdrawals from Roth IRAs, 401(k)s under the Rule of 55, and SEPP distributions to lower your overall tax burden.

For example, someone with $100,000 in Roth IRA contributions, a $300,000 401(k), and medical expense exceptions might see Mezzi recommend withdrawing $50,000 from the Roth IRA first, followed by $40,000 under the medical exception. This sequence could reduce taxable income by 25% compared to withdrawing in reverse order.

Mezzi also aligns withdrawals with tax calendars. It might propose quarterly SEPP payments to match estimated tax deadlines or advise year-end Roth conversions to take advantage of lower tax brackets. For instance, a Q4 withdrawal could offset capital losses, potentially saving you 15% on taxes.

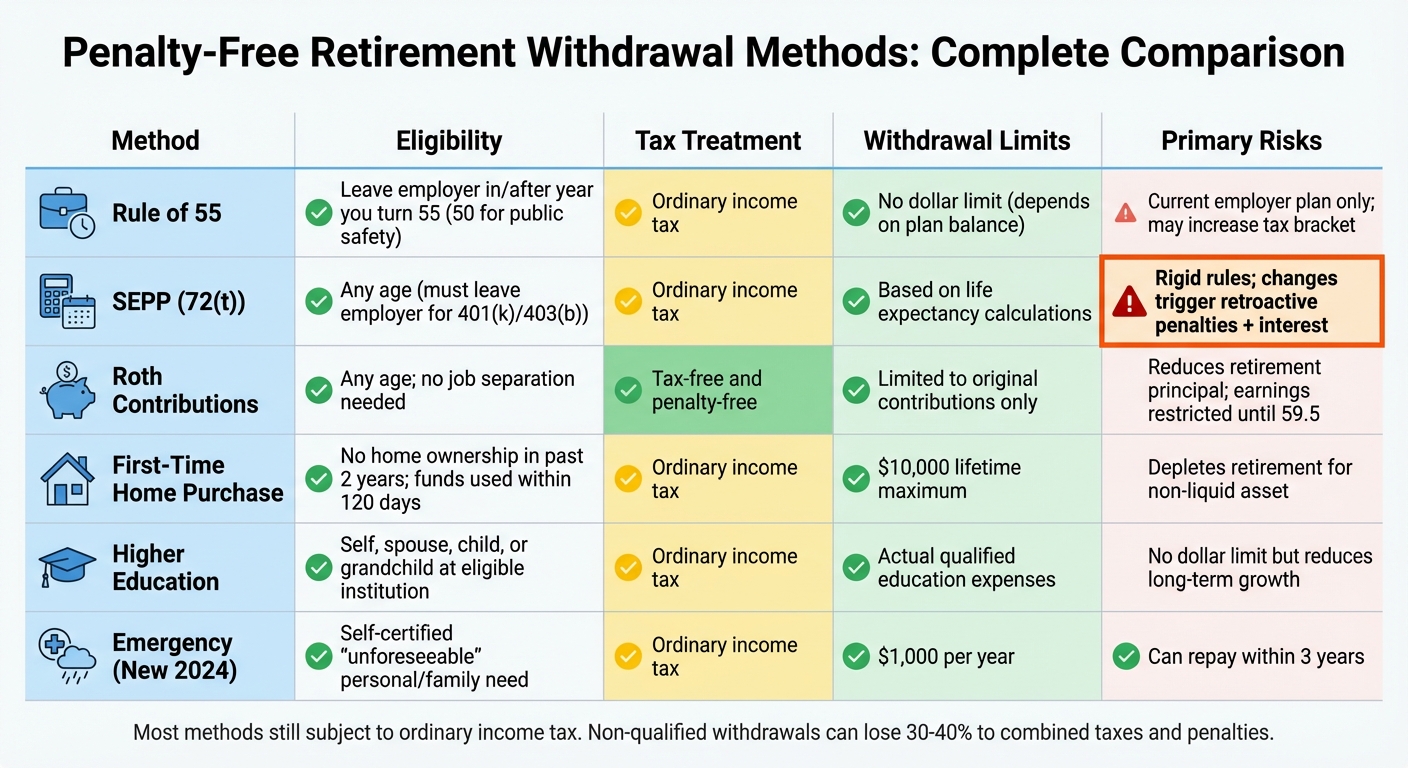

Comparison of Penalty-Free Withdrawal Methods

Penalty-Free Retirement Withdrawal Methods Comparison Chart

Every penalty-free withdrawal method comes with specific rules, tax implications, and limitations. Knowing these details can help you make informed choices and steer clear of costly errors. Mezzi’s AI-driven platform simplifies this process by comparing these options and helping you select the best strategy for your financial situation.

Here’s a breakdown of the most common methods, highlighting their eligibility, tax treatment, withdrawal limits, and potential risks:

| Method | Eligibility Requirements | Tax Treatment | Withdrawal Limits | Primary Risks |

|---|---|---|---|---|

| Rule of 55 | Must leave your employer in or after the year you turn 55 (50 for public safety workers) | Taxed as ordinary income | No specific dollar limit; depends on plan balance | Limited to the current employer’s plan; could push you into a higher tax bracket |

| SEPP (72(t)) | Available at any age (requires leaving employer for 401(k)/403(b)) | Taxed as ordinary income | Based on life expectancy calculations | Highly rigid; changes trigger retroactive penalties and interest |

| Roth Contributions | Any age; no job separation needed | Tax-free and penalty-free | Limited to the total amount of original contributions | Reduces retirement principal; earnings remain restricted until age 59.5 |

| First-Time Home | Must not have owned a home in the past 2 years; funds used within 120 days | Taxed as ordinary income | $10,000 lifetime maximum | Draws down retirement savings for a non-liquid asset |

| Higher Education | For self, spouse, child, or grandchild attending an eligible institution | Taxed as ordinary income | Limited to actual qualified education expenses | No set dollar limit, but diminishes long-term compounding growth |

| Emergency (New 2024) | Requires self-certification of an "unforeseeable" personal or family need | Taxed as ordinary income | $1,000 per year | Option to repay within 3 years |

While these methods avoid the 10% early withdrawal penalty, most are still subject to ordinary income taxes - except for Roth IRA contributions. Without proper planning, non-qualified early withdrawals can lose 30% to 40% of their value due to combined taxes and penalties.

The SEPP strategy stands out for its rigidity. If your financial situation changes and you alter the withdrawal schedule, you’ll face retroactive penalties on all prior distributions, plus interest. Likewise, withdrawals from SIMPLE IRAs within the first two years of opening the account come with a steep 25% penalty instead of the usual 10%.

Balancing these trade-offs is critical, and Mezzi’s platform can guide you in optimizing your withdrawals for both tax efficiency and compliance.

Conclusion

Tapping into your retirement funds before age 59.5 without facing the 10% IRS penalty is possible, but it demands careful planning and strict adherence to IRS guidelines. Options like Roth IRA withdrawal rules, the Rule of 55, SEPP (72(t)) distributions, and specific penalty exceptions each come with their own rules, tax consequences, and potential risks.

The financial stakes are significant. For instance, withdrawing $40,000 early could result in over $12,800 in combined penalties and taxes if you're in the 22% tax bracket. SEPP distributions, in particular, require precision - any misstep can trigger retroactive penalties on all previous withdrawals, plus interest. As Kathleen Coxwell from Boldin cautions:

"If you get it [SEPP] wrong at any point, all payments retroactively incur the penalty".

Beyond the immediate financial hit, early withdrawals also mean forfeiting the long-term benefits of compound growth. Thoughtful planning is crucial - not just to avoid penalties, but to ensure your financial stability and growth over time.

FAQs

Can I use the Rule of 55 if I have multiple 401(k)s?

Yes, you can! The Rule of 55 allows you to make penalty-free withdrawals from your 401(k) if you leave your job in or after the year you turn 55. This applies no matter how many 401(k) accounts you have. However, there’s an important catch: this rule only applies to the 401(k) plan tied to your most recent employer.

So, if you’ve changed jobs and have multiple 401(k) accounts, only the plan from your last employer qualifies for this penalty-free withdrawal option.

What SEPP mistakes trigger retroactive penalties?

Missteps with SEPP (Substantially Equal Periodic Payments) can be costly. Common errors include:

- Failing to stick to the strict payment schedule.

- Withdrawing funds too early or before the required timeframe.

- Changing the payment plan after it has started.

These mistakes can trigger the IRS to apply a 10% penalty retroactively to all previous withdrawals. To steer clear of this, it's crucial to follow SEPP rules carefully and stay consistent with the plan.

How do I prove I qualify for an IRS penalty exception?

To show you qualify for an IRS penalty exception, make sure your circumstances align with the specific criteria set by the IRS. You'll need to fill out Form 5329 to report the distribution and specify the exception you're claiming.

It's crucial to keep supporting documents on hand, such as medical bills, proof of a first-time home purchase, or documentation of financial hardship. These records are vital in case of an audit, so ensure you maintain detailed and accurate paperwork to back up your claim.

Disclosures:

- This content is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.

- Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.

- Savings and performance examples are hypothetical and for illustrative purposes only. Actual results will vary based on individual circumstances, portfolio composition, market conditions, and fees.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.