A wash sale may happen even if the buy and sell are at different firms. The rule may look across a 61-day window - 30 days before the sale, the sale date, and 30 days after - and it may also reach IRAs, 401(k)s, and a spouse’s account on a joint return.

Here’s the short version:

- I may sell at a loss in one taxable account and still trigger a wash sale if the same or a very similar holding gets bought in another account.

- Brokers may only flag wash sales they see inside one account, so cross-account issues may not appear on one statement.

- A buy in an IRA, Roth IRA, or 401(k) may be the harsh version of this problem, because the disallowed loss may not get added back to basis later.

- Small automated buys - like DRIP, recurring investments, robo rebalancing, or payroll contributions - may create the issue even when I did not place a manual trade.

- Some investors try to lower risk by pausing auto-buys, checking all household accounts before a loss sale, and using a replacement fund tied to a different index, not a near-clone.

A simple way to think about it: one household, one rule, one log. If I’m selling for a loss, I may need to review every account my household controls before and after that sale.

| Risk area | Why it may trigger a wash sale | What some investors look at |

|---|---|---|

| Second taxable brokerage | Same ticker bought in the window | DRIP, auto-invest, spouse trades |

| IRA or Roth IRA | Loss may be disallowed with no later basis add-back | Contributions, rebalancing, recurring buys |

| 401(k) | Payroll purchases of the same fund may conflict | Fund elections and contribution timing |

| Near-clone ETF | Same-index swap may be treated as too similar | Index provider and fund method |

| Options | Deep in-the-money calls may count as replacement exposure | Open option positions across accounts |

That’s the core idea of the article: wash sales may be a household tracking problem as much as a trading problem. The rest of the piece walks through the common mistakes, the account types people often miss, and the simple tracking setup some investors use during tax-loss harvesting season.

Wash Sale Rule Explained: Tax Loss Harvesting for Stocks and Crypto by Katie St Ores CFP

Wash sale rules you need to know when using multiple brokerages

Under IRC § 1091, a loss may be disallowed if you sell a security and then buy the same or a substantially identical security within 30 days before or after that sale. When you use more than one account, the hard part usually isn't the rule itself. It's figuring out what counts as the same holding and which accounts need to be reviewed together.

Before placing another trade, it may make sense to look at two things: what counts as the same security, and where the replacement purchase happened.

Same security, substantially identical security, and replacement purchases

The most obvious wash sale involves buying back the exact same stock or fund you just sold. But the rule may also reach options and funds that closely follow the same index. For example, selling SPY and buying IVV may trigger a wash sale because both track the S&P 500.

The IRS does not provide a fixed definition of substantially identical. So, the cautious move for some investors may be to avoid swapping a sold position for a similar-looking fund right away. If the goal is to keep roughly the same market exposure during the 31-day window, a fund tied to a different index may be a better fit.

There's also a small gotcha that trips people up: automatic dividend reinvestment and scheduled purchases may create a wash sale even if you never entered the trade yourself.

That matters because your broker may not have a full view of every account you own.

Which accounts count and why broker reporting falls short

The rule may apply across:

- Taxable brokerage accounts

- Traditional IRAs

- Roth IRAs

- Joint accounts

- 401(k)s

- A spouse's accounts when filing a joint return

In taxable accounts, the disallowed loss may be added to the basis of the replacement shares. In an IRA, Roth IRA, or 401(k), that loss may be permanently disallowed.

Brokers usually report wash sales only when the sale and repurchase happen in the same account. Once trades are spread across more than one account, manual review may be needed.

That's the problem in plain English: by tax time, the damage may already be done. Prevention usually has to happen before the next trade goes through.

Common multi-account mistakes that trigger wash sales

Wash Sale Risk by Account Type: What Every Multi-Brokerage Investor Must Know

Most cross-account wash-sale issues may start with automatic buys that were easy to miss.

A lot of the time, the problem isn't the sale itself. It's the small purchase sitting in another account that keeps running in the background.

Dividend reinvestment, auto-invest, and model portfolio conflicts

If you sell 500 shares of an ETF for a $2,000 loss and a DRIP buys the same ETF in another account during the window, part of that loss may be disallowed. Only the loss tied to the replacement shares may be disallowed, and the rule may apply even when the buy comes from a small DRIP, robo-advisor, or model portfolio.

The same issue may get worse when the replacement buy happens inside a retirement account.

Selling at a loss in a taxable account while buying the same fund in an IRA, Roth IRA, or 401(k)

This may be the more damaging version of the same mistake. When the replacement purchase happens inside a tax-advantaged account, the disallowed loss isn't deferred - it's gone permanently. That loss is permanently disallowed; there is no later basis adjustment in an IRA or 401(k).

Here's a plain example: you sell 300 shares of an ETF in your taxable account at a $3,000 loss on June 1. Your Roth IRA has an automatic contribution that buys 30 shares of the same ETF on May 20 and again on June 5. Both purchases fall within the 61-day window. The loss tied to those 30 replacement shares - $300 - is permanently disallowed.

Spouse accounts, near-clone ETFs, and options exposure

For joint filers, one spouse's buy may trigger the other spouse's wash sale. It may make sense to treat all accounts you and your spouse control as one trading system. A robo-advisor rebalancing Spouse B's IRA into an ETF that Spouse A just sold at a loss may be enough to create the problem.

Options add another layer of risk. Buying deep in-the-money call options on a stock you just sold at a loss in another account may be treated as acquiring a substantially identical position, which may trigger the wash-sale rule. The same concern may come up when someone swaps into a near-clone ETF during the window.

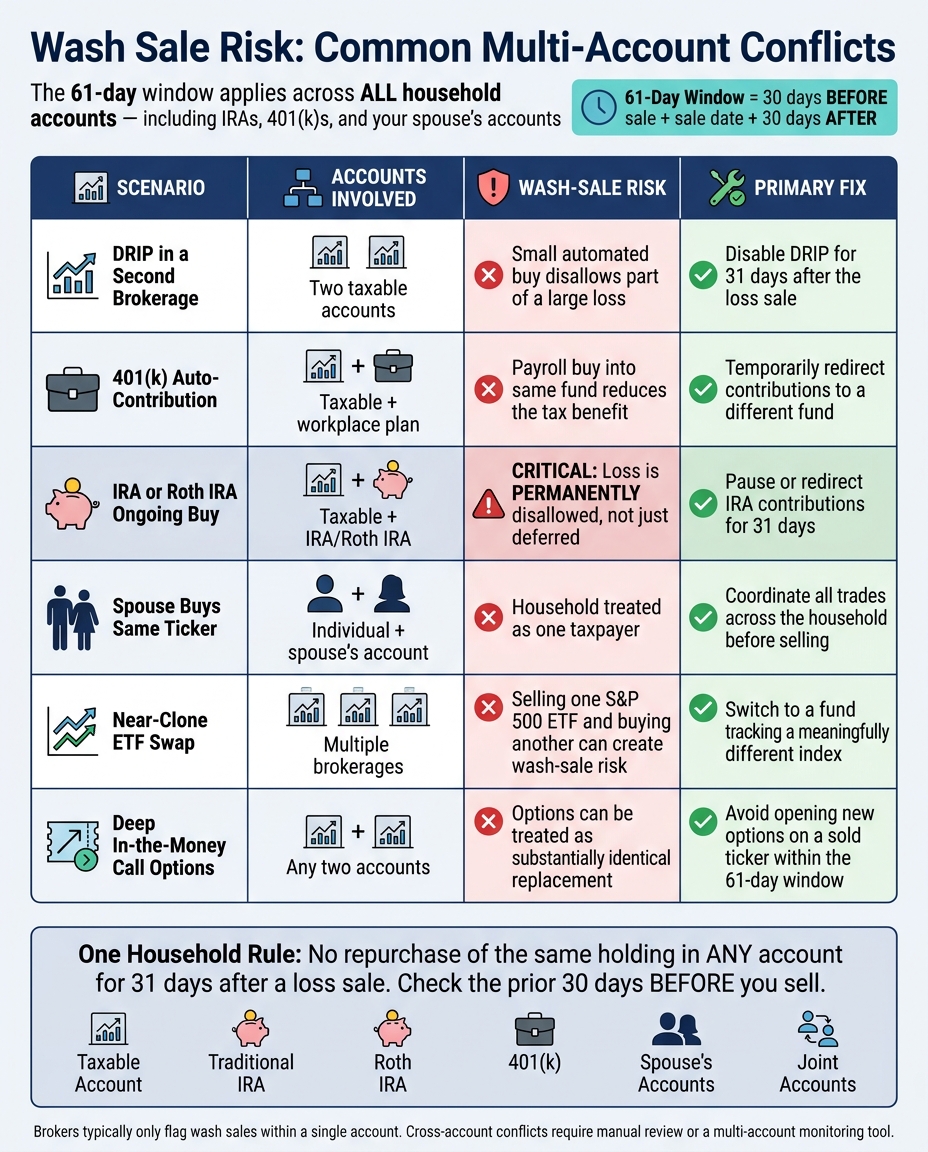

Use the table below to spot common household conflicts before you place the trade.

| Scenario | Accounts involved | Wash-sale risk | Primary fix |

|---|---|---|---|

| DRIP in a second brokerage | Two taxable accounts | Small automated buy disallows part of a large loss | Disable DRIP for 31 days after the loss sale |

| 401(k) auto-contribution | Taxable + workplace plan | Payroll buy into same fund reduces the tax benefit you meant to capture | Temporarily redirect contributions to a different fund |

| IRA or Roth IRA ongoing buy | Taxable + IRA/Roth IRA | Loss is permanently disallowed, not just deferred | Pause or redirect IRA contributions for 31 days |

| Spouse buys same ticker | Individual + spouse's account | Household treated as one taxpayer | Coordinate all trades across the household before selling |

| Near-clone ETF swap | Multiple brokerages | Selling one S&P 500 ETF and buying another can create wash-sale risk | Switch to a fund tracking a meaningfully different index |

| Deep in-the-money call options | Any two accounts | Options can be treated as substantially identical replacement | Avoid opening new options on a sold ticker within the 61-day window |

How to avoid wash sales before you place the trade

It may make sense to try to prevent a wash sale before you sell. A simple way to think about it: check every household account for recent or scheduled buys of the same holding before selling at a loss.

Apply a 31-day no-rebuy rule across the full 61-day window

One household rule may keep this easier to manage: no buy of the same holding in any account for 31 days after a loss sale, and check the prior 30 days before you sell.

Before selling, it may help to pause automatic activity that may still buy the security, such as:

- DRIPs

- Recurring buys

- Robo rebalances

- Workplace-plan contributions

Switch to similar exposure without using a same-index fund

If you want to stay invested, some investors rotate into a fund with similar market exposure but a different index or methodology. The main point: the replacement may be less likely to create wash-sale issues if it doesn't track the same narrow index as the fund you sold.

| Original holding | Potential replacement | Why it's less likely to be substantially identical |

|---|---|---|

| S&P 500 ETF (e.g., VOO) | Total Stock Market ETF (e.g., VTI) | Tracks a different index with a broader range of small- and mid-cap stocks. |

| Individual tech stock (e.g., Apple) | Technology Sector ETF (e.g., XLK) | Replaces a single company with a diversified basket of stocks in the same sector. |

| MSCI Emerging Markets ETF | FTSE Emerging Markets ETF | Uses different index providers and methodologies. |

| Growth Index Fund | Value Index Fund | Uses a different investment methodology and holds different underlying securities. |

Swapping one S&P 500 ETF for another S&P 500 ETF from a different fund family may still carry wash-sale risk. Since both funds track the same index, the IRS may view them as substantially identical.

Set one trading rule across taxable, IRA, and spouse accounts

If you're selling at a loss in a taxable account, check every household account for recent or scheduled purchases of the same security.

Some households use the same rule every time they trade: no repurchases of the same holding anywhere across all accounts during the 61-day window. If one spouse sells a fund at a loss, the other spouse's accounts - including any robo-managed IRA - may also need to be checked for that same period.

Build a simple cross-account monitoring process

Once you set the household trading rule, use one cross-account log to keep an eye on it. Avoiding wash sales across multiple brokerages may be less about investing skill and more about tracking. The simple approach: track the 61-day window, pause automatic buys, and keep every account in one log.

Keep one transaction log across every account

Build one spreadsheet that covers every account you and your spouse control. Export CSVs from each brokerage, add the account name and account type, then sort by trade date and ticker.

After that, cross-account conflicts may become much easier to spot. A sale of VTI in your taxable account and an auto-buy of VTI in your IRA two weeks later may sit right next to each other in the sheet - something a single brokerage statement may miss.

It may help to add a wash-sale watch tab. Any time you sell a security at a loss, log the ticker, the sale date, and the full 61-day window. Then flag any buy, automatic reinvestment, or spouse-account purchase of that same ticker - or a substantially identical security - that falls inside that range.

If manual tracking starts to feel slow, a dashboard may surface the same conflicts faster.

Use Mezzi to monitor wash sale risk across all your accounts in one place

If you want the same monitoring in one dashboard, Mezzi may centralize it. You connect your taxable accounts, IRAs, 401(k)s, HSAs, and spouse accounts through read-only access - no transfers, no trade execution, and no credentials are shared. The connection runs through Plaid and Finicity (Mastercard), so Mezzi may see your holdings and activity without touching your money.

From there, Mezzi's tax-optimization insights may flag potential wash-sale conflicts before you trade, not after. The X-Ray overlap tool surfaces holdings across accounts that may be substantially identical. And if you want to ask a specific question - for example, whether any account bought VTI in the last 30 days - the AI chat can check connected accounts for the ticker and date you ask about.

Mezzi monitors potential wash-sale conflicts; it does not place trades or move money.

FAQs

How do I know if two funds are substantially identical?

Two funds may be considered substantially identical if their holdings and investment strategies closely align. That may include funds that track the same index or focus on the same sector.

Because the IRS does not provide a strict definition, they need to be compared carefully.

Can a partial wash sale happen if only a few replacement shares were bought?

Yes. A partial wash sale may happen when only some replacement shares were bought.

The wash sale rule applies on a proportional basis to the shares involved. That means the disallowed loss and the basis adjustment are matched to those shares on a pro-rata basis.

What should I do if I discover a wash sale after the trade?

Adjust your tax reporting. A disallowed loss may be added to the cost basis of the replacement securities, so the tax benefit may be deferred until those shares are sold.

- Report it on Form 8949 using code W

- Recalculate the replacement shares’ cost basis

- Keep detailed trade records

If the wash sale happened in an IRA or Roth IRA, the loss may be permanently disallowed.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.