If I want carbon exposure, I may be choosing between three very different things. KRBN may give me ETF exposure to compliance carbon futures, GRN may give me ETN exposure with Barclays credit risk, and direct offsets may be more like buying project credits one by one than buying a market investment.

Here’s the short version:

- KRBN may fit investors who want exchange-traded, multi-region compliance carbon exposure

- GRN may fit investors who accept ETN structure risk and want more EU-linked exposure

- Direct offsets may fit people focused more on impact than resale value

A few facts stand out:

- KRBN’s expense ratio is 0.90%

- GRN’s expense ratio is 0.75%

- KRBN’s average daily volume is about 34,450 shares

- GRN’s average daily volume is about 95 shares

- The voluntary carbon market fell to about $535 million in 2024, down 29% from 2023

- One cited 2023 study found 87% of offsets used by major companies had a high risk of not delivering real additional cuts

That means the main question may not be “Should I invest in carbon?”

It may be: “Do I want liquid market exposure, issuer-backed note exposure, or project credits?”

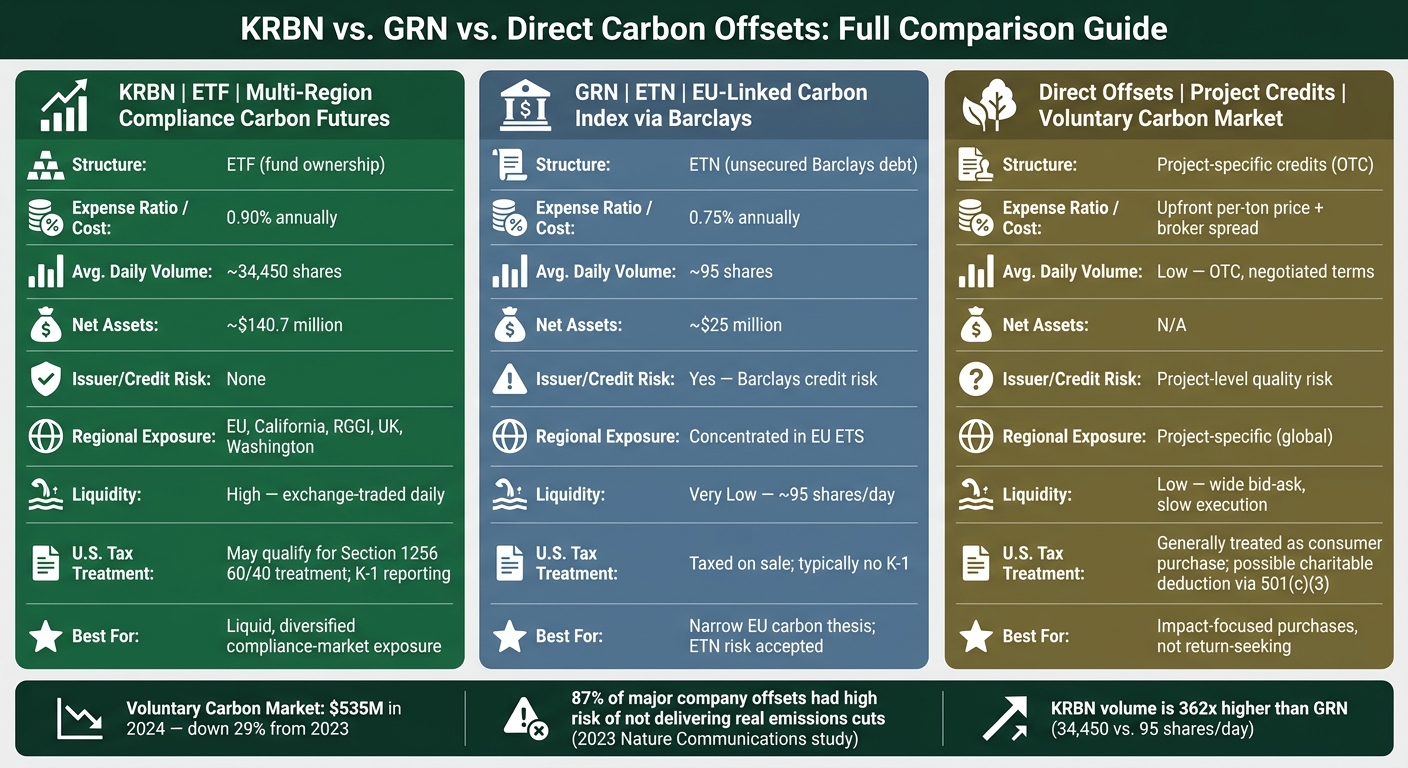

KRBN vs. GRN vs. Direct Carbon Offsets: Full Comparison Guide

The Investment Thesis On Carbon Credits with Luke Oliver Of KraneShares

Quick Comparison

| Option | What I may be buying | Main use case | Main tradeoff |

|---|---|---|---|

| KRBN | ETF exposure to compliance carbon futures | Broader carbon market exposure | Higher fee, futures/tax complexity |

| GRN | Barclays ETN tied to a carbon index | Narrower EU-linked thesis | Barclays credit risk, very thin trading |

| Direct Offsets | Project-based voluntary credits | Impact-focused purchases | Low liquidity, uneven quality, hard resale |

So before I buy anything in this space, I may want to separate market exposure from offset purchases. They may sound similar, but they may behave very differently.

KRBN vs. GRN: How the Two Exchange-Traded Options Differ

KRBN: ETF Structure, Futures Exposure, and Portfolio Role

KRBN is an ETF that tracks the S&P Global Carbon Credit Index through futures held in a Cayman subsidiary. When you buy KRBN, you own fund exposure rather than the futures contracts themselves.

The fund focuses on the most liquid contracts across the EU, California, RGGI, UK, and Washington carbon markets. It uses near-dated December contracts, screens for liquidity, and weights holdings by trading volume. In plain English, KRBN may offer a basket of carbon markets instead of a bet on just one region.

KRBN has an expense ratio of 0.90% per year, about $140.7 million in net assets, and average daily volume of roughly 34,450 shares. In taxable accounts, it may involve Section 1256 treatment and K-1 reporting, which may be one reason many U.S. investors lean toward tax-advantaged accounts.

GRN takes a different path to carbon exposure, and that structure may shape much of its risk.

GRN: ETN Structure, Issuer Risk, and How It Differs from KRBN

GRN is a Barclays-issued exchange-traded note tied to the Barclays Global Carbon II TR USD Index. Unlike KRBN, GRN does not give you fund ownership. You own an unsecured debt obligation of Barclays, so returns may depend not only on carbon prices but also on Barclays' ability to meet its obligations.

That issuer risk is the big dividing line. GRN also trades far less often and has narrower exposure than KRBN. If Barclays were to run into financial trouble, GRN holders would be unsecured creditors, no matter what happened to carbon prices.

GRN is also more concentrated, with heavier exposure to EU ETS-linked futures than KRBN's multi-region mix. Its stated expense ratio is 0.75%, which is lower than KRBN's 0.90%. But trading volume is much thinner, at about 95 shares per day on average. ETNs usually do not involve K-1s, though some investors may want to confirm current tax treatment before buying.

Those gaps may stand out most when structure, liquidity, and taxes are lined up next to each other.

KRBN vs. GRN: Side-by-Side Comparison

| Feature | KRBN | GRN |

|---|---|---|

| Structure | ETF | ETN |

| What you own | Fund exposure to futures and collateral | Barclays' unsecured note |

| Barclays credit risk | No | Yes - exposed to Barclays' credit risk |

| Index tracked | S&P Global Carbon Credit Index | Barclays Global Carbon II TR USD Index |

| Regional exposure | EU, California, RGGI, UK, and Washington carbon markets | More concentrated in EU ETS-linked futures |

| Net assets | About $140.7 million | About $25 million |

| Expense ratio | 0.90% | 0.75% |

| Avg. daily volume | About 34,450 shares | About 95 shares |

| Tax reporting | May involve Section 1256 treatment and K-1 reporting | Typically treated more like debt; usually no K-1 |

| Best fit | Broader exposure and easier trading | More targeted exposure for investors comfortable with ETN risk |

Direct offsets come with a different mix of tradeoffs: less standardization, lower liquidity, and more project-level risk.

Direct Offset Markets: What You Gain and What You Give Up

Direct offsets are project-specific credits. They are not the same as the regulated allowance exposure tied to KRBN or GRN. So if someone buys direct offsets, they may not get exchange-traded exposure. Instead, they may need to pick projects one by one and handle due diligence at the project level.

How Direct Offsets Work for Individual Investors

Buyers usually get access to credits through brokers or platforms linked to registries like Verra, Gold Standard, American Carbon Registry, and Climate Action Reserve. That setup may make access, pricing, and exit planning much less standardized than with carbon ETFs.

A buyer may hold credits and try to resell them later, or retire them for good. Once a credit is retired, the resale option is gone. At that point, the credit may function more like a consumption choice than an investment position.

Each credit represents one metric ton of CO₂e reduced, avoided, or removed. And each one is tied to a specific project, such as methane capture, reforestation, or renewable energy. Removal credits often trade at a premium to avoidance credits, but that higher price may not remove key risks. They may still involve permanence risk and reversal risk. For example, a wildfire or land-use change may eliminate stored carbon that has already been credited.

Quality, Liquidity, and Pricing Risks in Direct Credits

Paying more for a credit does not solve the main issue: quality varies a lot. In direct markets, most of the due-diligence work may fall on the buyer. Before buying, someone may need to look at:

- additionality

- permanence

- verification

- leakage risk

A 2023 study in Nature Communications found that 87% of offsets used by major companies carried a high risk of not providing real, additional emissions reductions. If credit quality is weak, offsets may not serve the goal of climate exposure or speculative return.

Liquidity is the other big tradeoff. Most voluntary carbon trades happen over the counter through brokers, with negotiated terms and no continuous market-making. Exchanges and platforms have improved transparency, but trading activity is still concentrated in a small group of popular credit types and larger corporate deals. For a small retail position in a niche project, an investor may run into:

- wide bid-ask spreads

- slower execution

- limited ability to exit fast

Pricing may also differ a lot across brokers, even for similar credits. Without central price discovery, fair value may be hard to judge.

After a 2021–2022 boom, the voluntary carbon market cooled sharply. Market value fell to about $535 million in 2024, down 29% from 2023, while volume fell 25%. That slowdown appears linked to quality concerns and more selective buying, which may make it harder to exit a speculative trade.

Which Option Fits Your Portfolio: Returns, Taxes, and Account Placement

Return Drivers, Fees, and Tax Friction

Once the structure is clear, the next step may be figuring out which vehicle lines up with your return goals, tax situation, and account mix. These options differ in what may drive returns, what they cost, and how taxes may apply. Direct offsets don't offer a steady market return. Any resale value may depend on project quality and buyer demand.

| Feature | KRBN (ETF) | GRN (ETN) | Direct Offsets |

|---|---|---|---|

| Return Source | Carbon futures and roll yield | European carbon futures; issuer-backed | No steady market return; resale only |

| Expense Ratio | 0.90% annually | 0.75% annually | Upfront per-ton price + broker spread |

| Liquidity | High - exchange-traded daily | Very low - ~95 shares/day avg. | Low - OTC, negotiated terms |

| U.S. Tax Treatment | KRBN may qualify for Section 1256 60/40 treatment | Taxed on sale as an ETN; typically no distributions | Generally not deductible from for-profit providers; possible charitable deduction through qualified 501(c)(3) |

Taxes may matter just as much as fees when you're looking at carbon exposure. KRBN may qualify for Section 1256 treatment, which may blend gains and losses at 60% long-term and 40% short-term rates regardless of holding period. GRN, as an ETN, is generally taxed on sale, and it typically makes no cash distributions. Direct offsets bought from for-profit providers are generally treated more like a consumer purchase than an investment. If offsets are funded through a qualified 501(c)(3), a tax professional may help determine whether a charitable deduction applies.

When KRBN, GRN, or Direct Offsets Make Sense

That shifts the choice from simple market access to portfolio use.

KRBN may be the most direct option for liquid compliance-market exposure. It trades daily, publishes holdings and methodology, and spans multiple regulated programs. Some investors may use it as a satellite allocation.

GRN may fit a much narrower case: someone with a specific thesis on European carbon markets who also accepts ETN structure risk. Because GRN is an unsecured obligation of Barclays Bank PLC, its market value may be affected by the issuer's credit quality independently of the underlying index. Investors who hold GRN may choose to keep total ETN exposure within a defined risk budget.

Direct offsets may make more sense as an impact expense than a return-seeking allocation. In that setup, selection may center more on project quality, verification standard, and permanence than on price appreciation. If purchases are made through a qualified 501(c)(3), it may be worth asking a tax advisor whether a charitable deduction applies. Across all three vehicles, some investors may prefer not to let total carbon exposure - KRBN, GRN, and offsets combined - become a core allocation.

Using Mezzi to Evaluate Carbon Exposure Across All Accounts

After you pick the vehicle, account location may change the after-tax result. That's where Mezzi's read-only account aggregation may come into play. By connecting all your accounts - brokerage, 401(k), Roth IRA, and others - Mezzi gives you a full portfolio view.

From that broader picture, Mezzi may surface account placement guidance. For example, it may show whether holding KRBN or GRN in a tax-advantaged account makes sense to help shield volatility and simplify tax reporting. Mezzi's X-Ray may also show whether a carbon position adds diversification or overlaps with exposure you already have.

Conclusion: How to Choose Between KRBN, GRN, and Direct Offset Markets

At this point, the choice may come down to exposure, liquidity, and intent. KRBN may be the more liquid ETF, while GRN adds Barclays credit risk on top of the carbon exposure itself.

Direct offsets sit in a different category. They may fit best when impact is the main goal, not return. The tradeoff may include limited resale options, no standard pricing, and the need to assess project quality, verification standards, and permanence on your own.

For many readers, the framework may look pretty simple:

- KRBN for liquid compliance-market exposure

- GRN for a narrower ETN position tied to tighter carbon policy, for investors who accept ETN and issuer risk

- Direct offsets for impact

One question may help frame the choice: is this for exposure or retirement?

FAQs

How risky is GRN compared with KRBN?

GRN and KRBN both track carbon credit pricing, but their risk may depend on the specific carbon markets they follow and on how each fund uses futures.

Because they’re futures-based, both may face tracking differences, contract roll costs, and market-driven price swings tied to global carbon supply and demand.

Can direct offsets be easily resold?

Usually not. Unlike carbon-credit ETFs, which trade on public exchanges, direct offsets are usually private, project-based instruments with limited liquidity.

Some Inflation Reduction Act energy tax credits may be transferred, but that applies to specific government-issued tax incentives, not standard voluntary carbon offsets.

Should I hold carbon exposure in a taxable account?

It may depend on the specific fund and your broader asset location plan. Some carbon-credit ETFs use futures, and those contracts may come with their own tax rules, including the 60/40 rule.

If tax efficiency matters to you, some investors use tax-advantaged accounts like IRAs or 401(k)s for assets that may create frequent taxable events. Taxable accounts may be a better fit for low-turnover investments that may be more tax-efficient.Disclosures:

- This content is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.

- Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.

- All links to external sources are provided for reference only.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.