Estate planning may come down to one simple rule: every asset may need one clear transfer path. If that path is missing - or if a will, trust, title, and beneficiary form do not match - money and property may move in ways you did not intend.

Here’s the short version:

- A will may cover assets that pass through probate.

- A revocable living trust may reduce probate if it is funded.

- Beneficiary forms on IRAs, 401(k)s, and life insurance may override a will.

- Account titles like joint tenancy, POD, and TOD may move assets outside probate.

- Powers of attorney and advance directives may deal with incapacity during life.

-

Tax rules may change the better transfer route:

- the 2026 federal estate and gift tax exemption may be $15,000,000 per person

- the top federal estate tax rate may remain 40%

- the 2026 annual gift exclusion may be $19,000 per recipient

- assets held until death may receive a step-up in basis under current law

A few mistakes may cause many of the problems: unfunded trusts, old beneficiary forms, naming the wrong person on retirement accounts, and leaving out incapacity documents.

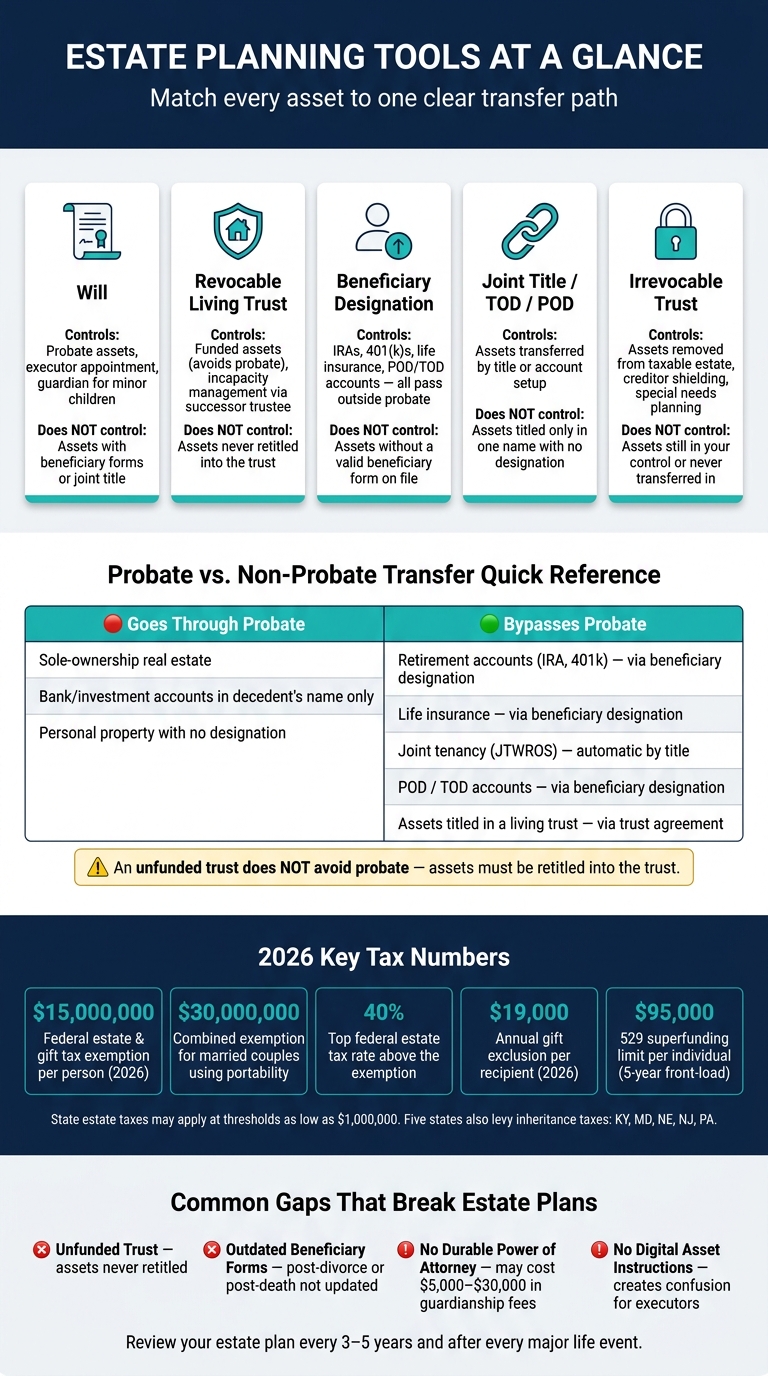

Estate Planning Tools: What Each One Does & When to Use It

Estate Planning Explained: Wills vs Trusts (What Actually Controls Your Assets)

Quick Comparison

| Tool | What it may do | What it may not control |

|---|---|---|

| Will | Direct probate assets, name an executor, name guardians for minor children | Assets with beneficiary forms or joint title |

| Revocable living trust | Hold assets during life, avoid probate for funded assets, allow a successor trustee to step in at incapacity | Assets never retitled into the trust |

| Beneficiary designation | Move IRAs, 401(k)s, life insurance, POD/TOD accounts outside probate | Assets without a valid beneficiary form |

| Joint title / TOD / POD | Transfer some assets by title or account setup | Assets titled only in one name with no designation |

| Irrevocable trust | Move assets out of the taxable estate in some cases, add control or creditor shielding in some cases | Assets you still control or never transfer in |

If I strip the topic down to its core, this article may be about matching each asset to the right transfer method, while keeping taxes, probate, and family friction in view.

Wills, Probate, and How Assets Actually Pass

What a Will Does and What It Cannot Override

A will directs the assets that go through probate, names an executor, and may appoint a guardian for minor children. Put simply, it serves as a backup transfer route, not a full estate plan.

But a will has limits. It only controls property titled solely in your name. Retirement accounts, life insurance, and payable-on-death accounts pass outside the will and usually follow the beneficiary form on file instead.

That split matters, because it shapes which assets may end up in probate and which ones may pass another way.

Probate vs. Non-Probate Transfers

Probate is the court-supervised process for validating a will, paying debts, and distributing what remains to beneficiaries. It may be public, slow, and costly.

A large share of many estates may bypass probate when assets are titled the right way and beneficiary forms are up to date.

| Asset Category | Probate Required? | Transfer Mechanism |

|---|---|---|

| Sole-ownership real estate | Yes | Will or intestacy |

| Accounts in decedent's name only | Yes | Will or intestacy |

| Retirement accounts (401(k), IRA) | No | Beneficiary designation |

| Life insurance | No | Beneficiary designation |

| Joint tenancy (JTWROS) | No | Automatic transfer by title |

| POD / TOD accounts | No | Beneficiary designation |

| Assets titled in a living trust | No | Trust agreement |

There’s one detail people often miss: a revocable living trust may avoid probate only for assets that were actually retitled into the trust. That’s the unfunded trust problem. The trust exists on paper, but if the accounts were never moved into it, those assets may still go through probate.

Once that path is clear, the next step may be making sure each asset lines up with the right title or beneficiary form.

Beneficiary Designations and Account Titling

Beneficiary forms and account titles need to match the plan. One common point: naming a minor child directly may create problems, so some families use a trust for the child’s benefit instead.

Account titling has its own trade-offs. Adding a child to a home deed to avoid probate may expose the property to the child’s creditors and may interfere with the intended tax result.

Keeping beneficiary designations and account titles aligned with the estate plan may reduce the odds of transfers going somewhere you did not mean for them to go.

How Common Trusts Work and When to Use Them

Once the will is clear, trusts may become the main tool for avoiding probate and shaping control.

Revocable Living Trusts: Probate Reduction and Incapacity Planning

A revocable living trust (RLT) is set up during your lifetime. You - the grantor - usually serve as your own trustee, which means you may keep control over day-to-day management and may usually amend or revoke the trust at any time. You also name a successor trustee to step in if you become incapacitated or die, and you name beneficiaries who may later receive the assets.

The main upsides are probate avoidance and incapacity planning. A funded RLT may help avoid multiple probate filings. And if you're unable to manage your finances, your successor trustee may step in without court involvement.

There’s one catch: only funded assets are controlled by the trust. Real estate, bank accounts, and non-retirement brokerage accounts need to be retitled into the trust’s name. Put simply, an unfunded trust is ineffective for probate avoidance.

Revocable trusts are usually tax-neutral during life. Assets held in the trust at death receive a step-up in basis under IRC §1014.

| Feature | Will-Only Plan | Will + Revocable Living Trust |

|---|---|---|

| Asset Transfer | Court-supervised probate | Avoids probate; stays private. |

| Public Record | Yes, filed with court | No, remains private |

| Incapacity Coverage | Requires separate power of attorney | Successor trustee can manage assets directly |

| Multi-State Property | A second probate proceeding in another state may be needed | Avoids a second probate proceeding in another state |

| Upfront Cost | Lower | Higher |

| Cost at Death | Higher probate-related costs | Lower probate-related costs |

An RLT is usually paired with a pour-over will. That short document may catch any assets you forgot to retitle and direct them into the trust through probate.

When control needs to be reduced for tax or protection reasons, irrevocable trusts may come next.

Irrevocable Trusts: Tax Planning, Asset Protection, and Special Cases

With an irrevocable trust, you give up the ability to change or take back the assets. The tradeoff is less control, but the assets moved out of your estate may reduce federal estate tax exposure, may be shielded from creditors, or may preserve eligibility for government benefit programs.

The federal estate tax rate is 40% on amounts above the exemption. The 2026 exemption is $15,000,000 per person under the One Big Beautiful Bill Act.

| Trust Type | Primary Purpose | Control Level | Key Tax Consideration |

|---|---|---|---|

| Irrevocable Life Insurance Trust (ILIT) | Keeps life insurance proceeds out of the taxable estate | None | Death benefit excluded from estate |

| Spousal Lifetime Access Trust (SLAT) | Transfers assets to a spouse's benefit while removing them from the estate | Limited | Reduces taxable estate; spouse retains indirect access |

| Special Needs Trust | Provides for a disabled beneficiary without disqualifying them from government benefits | None | Preserves government benefit eligibility |

| Charitable Remainder Trust (CRT) | Provides income to the grantor for a term; remainder goes to charity | Limited | Partial charitable deduction; estate reduction |

Sometimes the point isn’t tax removal at all. Sometimes it’s control over how heirs receive money. That’s where testamentary trusts may fit.

Testamentary Trusts, Marital Trusts, and Controlling How Heirs Inherit

A testamentary trust sits inside your will and comes into existence only after you die. Its main use is control over how and when heirs receive assets.

This setup may be especially useful for minor children. Instead of a child receiving a lump sum at age 18, a testamentary trust may stage distributions by age or milestone. A spendthrift clause - a clause that blocks creditors from reaching a beneficiary’s share - may also add a layer of protection against poor financial decisions or outside claims.

For married couples with larger estates, marital trusts - sometimes called "A/B" or bypass trust structures - may help each spouse make full use of their individual estate tax exemption. The structure may help use exemptions efficiently, but it may also change basis outcomes. Coordinating this with an estate attorney matters, and assets in a bypass trust generally do not receive a step-up at the surviving spouse’s death.

Tax-Efficient Transfers During Life and at Death

Tax efficiency matters because the transfer method may shape who receives the asset, when they receive it, and what tax may apply.

Federal and State Transfer Taxes: What the Thresholds Mean for You

After choosing the transfer path, the next question is whether taxes may change the better route. For 2026, the federal estate and gift tax exemption may be $15,000,000 per person, or $30,000,000 for married couples using portability. The top federal estate tax rate remains 40% on amounts above the exemption.

State estate or inheritance taxes may apply far earlier than the federal tax, sometimes around $1,000,000. Five states - Kentucky, Maryland, Nebraska, New Jersey, and Pennsylvania - levy an inheritance tax on heirs.

For married couples, filing Form 706 at the first death may preserve any unused exemption, also called DSUE.

For many families, basis planning may matter more than estate tax. That shifts the next decision to a very practical one: gift now or hold until death.

Step-Up in Basis vs. Carryover Basis: What to Hold and What to Gift

The biggest income-tax decision in estate planning may be whether to transfer an asset during life or hold it until death.

Assets held until death usually receive a step-up in basis to fair market value, which may erase lifetime gains for capital-gains purposes. By contrast, lifetime gifts carry over the donor's basis. So appreciated assets may be better held until death, while low-basis or loss assets may be handled earlier.

There is one common exception. Assets with built-in losses are often sold before death. If they are held until death, they receive a step-down to fair market value, and the ability to deduct the loss disappears permanently.

Annual Gifting, 529 Plans, and Charitable Transfers

Tax strategy only works when the asset may be moved cleanly and legally. That usually means beneficiary forms and account titles need to be in order before gifting begins.

In 2026, you may give $19,000 per recipient - or $38,000 for married couples using gift-splitting - without filing a gift tax return. Cash or low-appreciation assets are often a better fit here.

Direct payments for tuition or medical expenses, when paid to the institution or provider, are unlimited and do not count against the annual exclusion or lifetime limit. For a larger one-time transfer, 529 plan superfunding lets you front-load five years of annual exclusions - up to $95,000 per individual or $190,000 for married couples.

Charitable transfers add another option. They may reduce both estate and income tax. For charity, appreciated securities may avoid capital gains, and qualified charitable distributions may move IRA dollars to charity in a tax-aware way for donors age 70½ or older.

| Transfer Method | Estate Tax Effect | Income Tax Effect | Control |

|---|---|---|---|

| Lifetime Gift | May remove future appreciation from the estate | Carryover basis; recipient may owe capital gains later | Relinquished immediately |

| At-Death Bequest | Included in taxable estate | Step-up in basis for heirs | Retained until death |

| Charitable Transfer | May reduce taxable estate | May avoid capital gains on appreciated assets | Relinquished |

The final step is matching each asset to the right title, beneficiary, or trust.

Putting the Plan Into Practice Without Costly Gaps

Once the tax plan is set, the last step comes down to execution. Titles, beneficiary forms, and legal documents need to line up. If they don't, the plan on paper may not match what happens later.

Match Each Asset to the Way It Transfers

The last review is pretty simple: make sure each asset has one clear transfer path.

Use this checklist to match each asset to its transfer rule.

| Asset Type | Primary Transfer Method | Common Gap |

|---|---|---|

| IRA / 401(k) | Beneficiary designation | Naming the estate instead of a person |

| Life insurance | Beneficiary designation | Outdated beneficiary form |

| Bank accounts | Payable on Death (POD) | No POD designation |

| Brokerage accounts | Transfer on Death (TOD) or trust | Left in personal name instead of the trust |

| Real estate | Trust title or joint tenancy with right of survivorship | Out-of-state property left outside the trust, triggering a second probate |

| Business interests | Buy-sell agreement or trust | No buy-sell or succession agreement |

| Personal property | Will | No will; state law decides |

Mistakes That Cause Delays, Taxes, or Family Conflict

The biggest breakdowns usually come from mismatches, not from missing paperwork.

The gaps that show up most often are unfunded trusts, stale beneficiary forms, and missing incapacity documents.

Unfunded trusts may be the most common issue. If an asset stays in your personal name, the trust may not control it. That means each asset may need to be retitled into the trust, and new purchases may need a review too.

Outdated beneficiary forms may create problems just as often. After a marriage, divorce, or death, those forms may no longer match your plan. Some people also name a contingent beneficiary for each account so there is a backup path if the first person listed is no longer able to inherit.

Two other gaps often get missed: no durable power of attorney and no digital asset instructions. Without a durable financial power of attorney, incapacity may lead to a guardianship petition that may cost $5,000 to $30,000. For digital assets, written access instructions and authorization may make things far less messy for the people handling the estate.

Conclusion: The Few Decisions That Drive Most Outcomes

A short list tends to do most of the work in an estate plan: have a will as a backstop, fund any trust you create, keep beneficiary designations current, and know which assets may bypass probate through titling or designation.

Tax efficiency, including a step-up in basis and annual gifting, may improve what heirs receive. But that may only hold up when the ownership structure is clean. A tax-aware plan built on mismatched titles and stale beneficiary forms may fall apart when it's tested.

Estate plans may drift over time. Laws change. The federal estate tax exemption is $15,000,000 per person in 2026 under OBBBA. Life may change even faster. Many people review the plan every 3 to 5 years and after any major life event.

FAQs

Do I need both a will and a trust?

Everyone may need a will. It’s the core document in an estate plan, and it’s the only document that may name a guardian for minor children.

A revocable living trust may not be required, but many people have both. When that happens, a pour-over will directs any assets not placed in the trust into it at death, while the trust may help manage assets and may help avoid probate.

Which assets should stay outside my trust?

Assets with named beneficiaries - like retirement accounts, including 401(k)s and IRAs, and life insurance - generally stay outside your trust. Those assets usually pass straight to the people you named as beneficiaries, no matter what your will or trust says.

The same idea may apply to property held as joint tenants with right of survivorship. That property usually passes automatically to the surviving owner.

It may make sense to keep beneficiary designations up to date.

When is gifting better than waiting until death?

Gifting during your lifetime may make more sense if the goal is to reduce your taxable estate and move future asset growth outside of it. The annual gift tax exclusion - $19,000 per recipient in 2026 - may let some people transfer wealth without using their lifetime exemption.

Waiting until death may make more sense for highly appreciated assets, since those assets may receive a step-up in basis. That may reduce capital gains tax for heirs.

So the choice may come down to a tradeoff: estate tax savings on one side, and income tax treatment on the other.

Disclosures:

- This content is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.

- Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.