A generation-skipping trust may make sense for families with large estates, long time horizons, and a goal of passing assets to grandchildren while limiting estate exposure in a child’s name.

Here’s the short version:

- I may use a generation-skipping trust to move assets to grandchildren or later heirs.

- My children may still receive trust income, but they may not own the principal.

- GST tax analysis usually centers on 3 transfer types: direct skip, taxable distribution, and taxable termination.

- If federal GST exemption is not allocated, transfers may face an extra 40% GST tax.

- For 2026, the federal GST exemption is listed here as $15 million per person and $30 million per married couple.

- The exemption may be allocated on Form 709 for lifetime gifts or Form 706 at death.

- These trusts may also offer asset protection, privacy, and more control over distributions.

- The tradeoff may include high legal complexity, trustee oversight, extra tax work, and less flexibility because the trust is usually irrevocable.

- A simpler plan may fit better if an estate is far below the exemption amount or if the goal is limited, such as helping with education costs.

- The article also notes the 2026 annual gift exclusion of $19,000 per recipient as a simpler option in some cases.

In plain English: this trust structure may be most relevant when a family wants multigenerational transfer planning, wants to keep future growth outside a child’s taxable estate, and is comfortable with added cost and strict rules.

A quick comparison may help:

| Topic | Direct inheritance | Generation-skipping trust |

|---|---|---|

| Estate exposure | Assets may later sit in a child’s estate | Assets may stay outside a child’s estate |

| Control | Child usually controls assets outright | Trustee follows trust terms |

| GST tax issue | Usually not the main feature | Central planning issue |

| Asset protection | Often lower | Often higher |

| Setup and upkeep | Simpler | More complex |

If I were screening this option fast, I’d focus on four questions: How large is the estate? Who should get income vs. principal? Are the assets likely to grow a lot? And is the family comfortable giving up flexibility for tighter control and tax planning?

How to Minimize Generation Skipping Transfer Tax

How a generation-skipping trust works

Once funded, the trust usually may not be easy to change. So the document needs to spell out who controls the assets and how they move over time. The grantor usually works with an estate planning attorney to draft the trust document, which lays out the trustee's powers, the beneficiaries, and the rules for distributions.

A trust may be funded with cash, stocks, real estate, or business interests. A generation-skipping trust may be set up during life or at death through a will or revocable living trust. Lifetime funding may move future growth outside the grantor's taxable estate. Assets passed at death use their date-of-death value. Those timing choices may matter because GST tax may depend on who receives the assets and when.

The roles of the grantor, trustee, and beneficiaries

Each party has a separate role.

The grantor creates and funds the trust and usually gives up direct control once assets are transferred. The trustee manages the assets and handles distributions under the trust terms. Trustees may be individuals or corporate entities, such as banks or trust companies, and they are expected to act in the beneficiaries' best interests.

Beneficiaries are often grandchildren or later descendants, who are referred to as skip persons. Some trusts also allow non-skip persons, usually the grantor's children, to receive income while the principal stays preserved for the skip-generation beneficiaries. That setup may affect whether assets remain protected for those later-generation beneficiaries. Distributions may also be tied to milestones or to a health, education, maintenance, and support standard.

The 3 transfer types that trigger GST tax analysis

Once the trust is funded, the next issue may be which transfers trigger GST tax. When reviewing an estate plan that involves a GST, it may help to know the three events that may trigger it:

- Direct skip: Assets pass straight to a skip person. The donor or estate pays the tax at the time of the transfer.

- Taxable distribution: The trust makes a distribution of income or principal to a skip person while non-skip beneficiaries still have an interest. The recipient pays when the distribution is made.

- Taxable termination: A non-skip beneficiary's interest ends and only skip persons remain. The trustee pays the tax at that point.

These three categories set the timing of the tax and identify who pays it.

How the tax rules apply

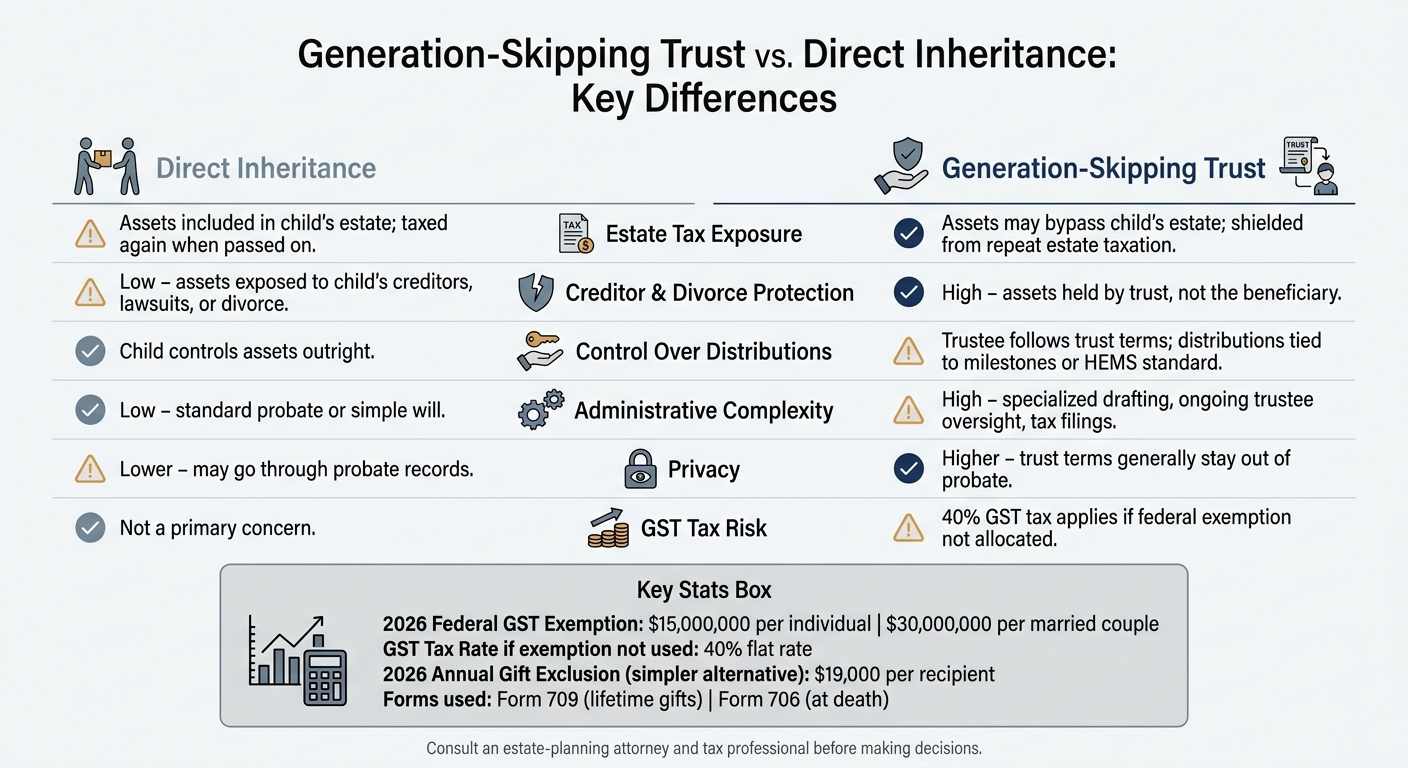

Generation-Skipping Trust vs. Direct Inheritance: Key Differences

These transfer types matter because the tax treatment follows the transfer itself, not just the trust document. A generation-skipping trust may still trigger GST tax unless the grantor allocates federal GST exemption. In plain English: what counts is whether the transfer uses federal GST exemption. Without that step, the trust may still face a flat 40% GST tax on top of any estate or gift tax.

How the GST exemption can reduce or eliminate extra transfer tax

The main way this extra tax may be reduced is by using the GST exemption the right way. Each person has a lifetime GST exemption set at $15 million per individual or $30 million for married couples for the 2026 tax year. If that exemption is allocated to a trust, the trust may receive a zero inclusion ratio. That may shield future trust distributions from GST tax, including future growth on the original assets.

GST exemption may be allocated on Form 709 for lifetime gifts or Form 706 at death. The exemption is not portable to a surviving spouse.

Direct inheritance vs. generation-skipping trust: a side-by-side comparison

The table below shows how the two approaches may differ.

| Feature | Direct Inheritance | Generation-Skipping Trust |

|---|---|---|

| Tax exposure | Assets may be included in the child's estate, then taxed again when passed on. | Assets may bypass the child's estate; GST tax may apply only if exemption is not fully allocated. |

| Creditor protection | Low; assets may be exposed to the child's creditors, lawsuits, or divorce. | High; assets are held by the trust, not the beneficiary. |

| Administrative complexity | Low; standard probate or a simple will. | High; requires specialized drafting and ongoing trustee oversight. |

That tax tradeoff often shapes which households may even want to look at this strategy. With the rules laid out, the next step is figuring out who this approach may fit.

Who should consider a generation-skipping trust

Once the tax rules make sense, the next step is figuring out whether this setup may fit your family.

Households most likely to benefit

This approach may fit families that are likely to use most or all of the federal GST exemption and want assets to skip a child's taxable estate. The aim may be multigenerational wealth transfer with tax efficiency: keeping assets out of the children's taxable estates so the same wealth may not be taxed again at the next generational step.

A few situations may make this structure worth a closer look:

- Financially independent adult children. If your children are already high earners, passing wealth to them directly may increase their future estate tax exposure. Moving that wealth into a GST trust may preserve the inheritance for grandchildren instead.

- Business owners with appreciating assets. Transferring a minority interest in a family business into a GST trust while the valuation is still lower may make more use of the GST exemption, since future growth may happen inside the trust instead of inside your taxable estate.

- Families that want trust-controlled distributions and long-term asset protection. Because beneficiaries do not own trust assets outright, those assets are generally shielded from lawsuits, creditors, and divorce settlements.

- Grandparents who want to fund education over time without giving up control of principal. A GST trust may support a grandchild's education across many years while keeping the principal intact for later generations.

If those traits don't apply, a simpler inheritance plan may work better.

When a simpler inheritance plan may be enough

If your estate is well below the exemption range, a GST trust may add more cost and complexity than value. For smaller goals, like helping a grandchild with college costs, the $19,000 annual gift exclusion per recipient in 2026 or direct payments to educational institutions may be much simpler tools. Those options do not touch your lifetime exemption at all.

Those tradeoffs may matter most for large, appreciating estates and families that want long-term control. The next section lays out what you may gain, what you may give up, and when that tradeoff may make sense.

Advantages, tradeoffs, and a decision checklist

What you gain and what you give up

If the trust appears to fit your goals, the next step may be a plain tradeoff check. You may gain more control, privacy, and tax planning options. At the same time, you may give up flexibility and take on added cost and upkeep.

| Advantage | Tradeoff |

|---|---|

| Estate tax efficiency: May help keep assets out of the child's taxable estate. | Irrevocability: Terms generally may not be changed once the trust is funded. |

| Asset protection: Trust assets are generally shielded from creditors, lawsuits, and divorce. | Complexity: Requires specialized legal and tax expertise to set up correctly. |

| Long-term control: Distributions may be tied to age or milestones. | Administrative costs: Ongoing trustee, legal, and accounting fees may add up. |

| Wealth preservation: Future growth may stay inside the trust. | Family tension: Children may resent losing control of the principal. |

| Privacy: Trust terms usually stay out of probate records. | Ongoing coordination: Requires periodic legal and tax review. |

Checklist: signs it is worth discussing with an estate-planning professional

If those tradeoffs line up with what you want, this checklist may help you decide whether it makes sense to bring up with an estate-planning professional.

- Your estate may be near the 2026 federal GST exemption.

- You may want children to benefit during life while principal passes to grandchildren.

- You may hold high-growth assets - such as a family business or real estate - that are expected to appreciate.

- You may want guardrails on how heirs use inherited funds, such as limiting distributions to education or healthcare.

- You may be concerned about protecting family wealth from a beneficiary's future divorce or creditor claims.

Conclusion: the core decision in plain terms

A good next step may be to review estate size, beneficiaries, and distribution goals with an estate-planning attorney and tax professional. A generation-skipping trust may be worth discussing when the tax savings, control, and asset-protection features appear to outweigh the loss of flexibility.

FAQs

Can a generation-skipping trust be changed later?

Usually not. Generation-skipping trusts are typically irrevocable. Once you create and fund the trust, you generally may not change its terms or take the assets back.

That’s why careful planning may matter. Your circumstances may change over time, and tax laws may change too. Either one may affect how the trust works.

There are a few rare exceptions. In some cases, a court may dissolve the trust, such as when there was fraud or a lack of sound mind at the time it was created.

What assets work best in a generation-skipping trust?

Assets that may have more room to grow over time - like stocks and other investments with high appreciation potential - are often used for this kind of transfer. If those assets are moved when their value is still relatively low, and the lifetime GST tax exemption is applied, that approach may shield both the starting value and later appreciation from transfer taxes.

Other assets people often use include cash, bonds, and real estate. 529 plans are also common, since they may help fund grandchildren’s education while making use of gift tax exclusions.

How do I know if my estate is large enough for this trust?

A generation-skipping trust may make the most sense for high-net-worth estates. It may be worth a closer look if your total assets approach or exceed the federal estate tax exemption threshold.

For smaller estates, the math may look different. Setup costs, ongoing administrative fees, and tax complexity may outweigh the upside for some families. In those cases, this type of trust may add more work and expense than value.

An estate-planning professional may help assess whether your estate size appears to justify this strategy.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.