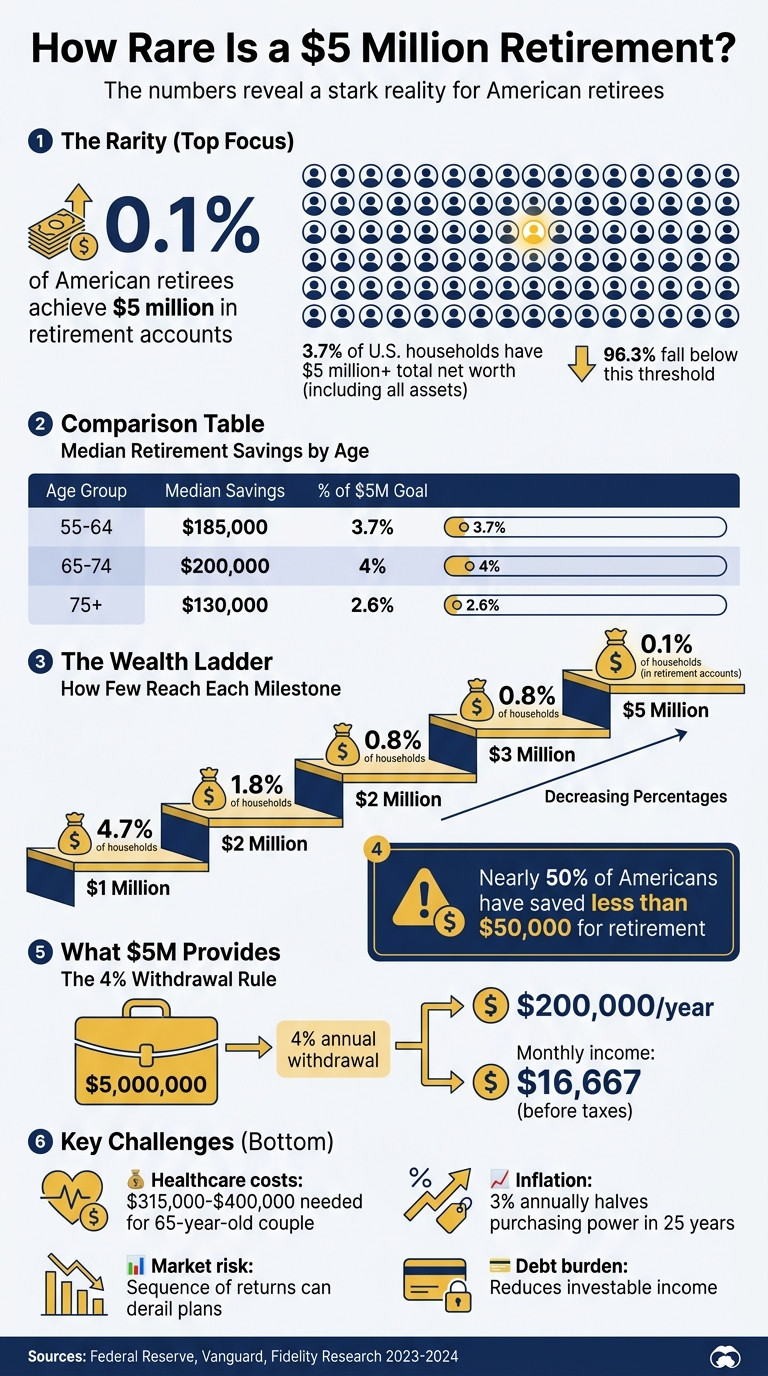

Retiring with $5 million is rare. Only about 0.1% of American retirees achieve this through retirement accounts, while 3.7% of U.S. households report a total net worth of $5 million or more, including assets like real estate and investments. For those in this bracket, implementing wealth management tax strategies is essential for asset preservation. For comparison, the median retirement savings for those aged 65–74 is just $200,000, far below this target. Achieving $5 million typically requires high income, disciplined saving, early investing, and careful financial management over decades.

Key Points:

- $5 Million Breakdown: Using the 4% withdrawal rule, $5 million may provide about $200,000 annually before taxes.

- Challenges: Inflation, taxes, healthcare costs, and market risks make this goal difficult for most.

- Reality Check: Nearly half of Americans have saved less than $50,000 for retirement.

- Strategies: Tools like Mezzi aim to simplify saving, retirement tax strategies, and portfolio management to help individuals work toward ambitious goals.

While $5 million is uncommon, having a clear plan and leveraging the right resources may improve your chances of building a secure retirement.

How Rare Is a $5 Million Retirement: Statistics and Comparisons

The Reality: How Few People Retire With $5 Million

The Numbers on High-Net-Worth Retirees

Reaching $5 million in retirement savings is an achievement that very few Americans accomplish. For context, within retirement accounts like 401(k)s and IRAs, only a tiny fraction of retirees ever hit this milestone. Even reaching $1 million - a far more modest goal - is relatively rare, with just 4.7% of households achieving it.

"Fewer than 0.1% of retirees hit that level, making it something closer to a statistical outlier than a standard goal." - Jeannine Mancini

When considering all assets - including real estate, brokerage accounts, business equity, and other investments - about 3.7% of U.S. households (around 4.8 million) reported a total net worth of $5 million or more in 2023. This leaves 96.3% of American households below this threshold. These numbers provide a stark contrast to the typical retirement savings landscape.

How $5 Million Compares to Typical Retirement Savings

While some households manage to accumulate significant wealth, the majority of retirees fall far short of the $5 million benchmark. For those aged 65–74, the median retirement account balance is $200,000, which is just 4% of the $5 million target. Even the average balance for this age group, at $609,230, represents only about one-eighth of that amount.

| Age Group | Average Retirement Savings | Median Retirement Savings |

|---|---|---|

| 55 to 64 | $537,560 | $185,000 |

| 65 to 74 | $609,230 | $200,000 |

| 75+ | $462,410 | $130,000 |

The gap becomes even more pronounced as the savings thresholds increase. Only 1.8% of households have $2 million or more in retirement accounts, and just 0.8% reach $3 million. Climbing higher on this ladder is exponentially harder - reaching $5 million is 47 times rarer than hitting $1 million. These figures highlight the steep challenges involved in building substantial wealth, emphasizing the importance of careful financial strategies for those aiming at such ambitious goals.

What $5 Million Actually Provides in Retirement

Annual Income Using the 4% Withdrawal Rule

With $5 million saved, applying the 4% withdrawal rule may provide about $200,000 annually, or roughly $16,667 per month before taxes. This rule involves withdrawing 4% of your portfolio each year, with adjustments for inflation. Historically, this approach has helped retirees maintain income for about 30 years without fully depleting their savings.

However, retiring earlier - say at 55 - extends the retirement period to over 40 years, which may increase the risk of running out of funds due to sequence-of-returns risk.

"The 4% rule is a starting point, not gospel. Bengen - who invented it in 1994 - updated his ceiling to 4.7% in 2025." – Andrew Izyumov, Founder, 8FIGURES

More recent studies suggest that the "safe" withdrawal rate depends on individual circumstances. For example, Morningstar recommends a 3.9% withdrawal rate for those who prefer a conservative approach. Meanwhile, William Bengen has suggested rates between 4.7% and 5.5%, depending on factors like market performance and asset allocation. To help mitigate risks during market downturns, some retirees keep 6–12 months’ worth of expenses in liquid assets such as Treasury bills or money market funds.

Next, let’s take a closer look at how inflation and taxes impact this income.

How Inflation and Taxes Affect Your $5 Million

Inflation and taxes can significantly reduce the real value of a $200,000 annual income. For example, with a 3% annual inflation rate, your purchasing power may be halved over 25 years. The inflation spike in 2022, which exceeded 7%, highlighted how quickly rising costs can erode value. Additionally, withdrawals from traditional retirement accounts like 401(k)s and IRAs are taxed as ordinary income, meaning you won’t be able to spend the full $200,000.

One way to manage taxes is to withdraw from taxable accounts first, leveraging lower capital gains rates. After that, tax-deferred accounts can be tapped, and Roth accounts saved for last to benefit from their tax-free growth.

Healthcare is another significant cost to plan for. A 65-year-old couple retiring today may need between $315,000 and $400,000 for medical expenses throughout retirement, and this figure doesn’t include potential long-term care costs.

Finally, where you live plays a big role in how long your portfolio lasts. Geographic cost differences can dramatically affect your spending power over time.

Why Most People Don't Reach $5 Million

Low Savings Rates and Market Downturns

Reaching a $5 million retirement portfolio is a daunting goal for most Americans. For households approaching retirement, the median savings is less than $200,000, and nearly half of all families lack any retirement accounts at all. In fact, 22% of Americans have saved less than $50,000 for their golden years.

One major hurdle is lifestyle inflation. As incomes rise, many people increase their spending on items that lose value over time, such as luxury cars or designer clothing, instead of focusing on assets that may grow wealth, like stocks or real estate. Even individuals earning six figures can find themselves stuck in a paycheck-to-paycheck cycle. Market volatility adds another layer of difficulty. Early downturns in an investment timeline or during retirement can lead to sequence of returns risk, where investors may be forced to sell assets at a loss, derailing long-term growth.

On top of this, rising healthcare expenses further strain the ability to build wealth over time.

Rising Healthcare Costs and Delayed Retirement

Healthcare costs are a significant financial burden. A 65-year-old couple retiring today is projected to need approximately $315,000 to cover medical expenses throughout retirement, and that figure doesn’t include long-term care like nursing home costs. Since Medicare doesn’t cover everything, retirees often face additional out-of-pocket costs for premiums, co-pays, and other medical expenses, which can quickly erode savings.

These rising costs often push people to delay retirement, leaving less time for peak earning years and consistent saving. On top of that, unexpected events - such as job loss or medical emergencies - can disrupt even the most disciplined financial plans. High levels of debt, whether from mortgages, car loans, or credit cards, further complicate the picture, reducing the amount of money available to invest. These setbacks not only slow the rate of savings but also shorten the timeline for building wealth, making ambitious goals like $5 million even harder to achieve.

When you combine these challenges - low savings rates, market risks, healthcare costs, and debt - it becomes clear why accumulating $5 million requires not just a high income and smart investing but also decades of financial stability and favorable market conditions. Unfortunately, this combination remains elusive for the majority of Americans.

This Is What a $5M Retirement ACTUALLY Looks Like

How to Build Toward $5 Million Using Mezzi

Navigating the challenges of saving, taxes, and market risks can feel overwhelming. That’s where smart technology comes in. Building a $5 million retirement portfolio requires disciplined saving, effective tax strategies, keeping fees in check, and having a clear understanding of your financial landscape. Mezzi’s AI-driven platform aims to simplify this process by identifying opportunities that might otherwise come with high advisory fees, offering these insights at a fraction of the cost.

Gain a Complete View of Your Finances with Mezzi

Many investors manage assets across multiple accounts, which can make it hard to see the bigger picture. This fragmented approach often leads to missed opportunities, such as unnoticed overlaps in holdings or inefficient asset allocation. Mezzi solves this by securely connecting all your accounts through read-only access using Plaid and Finicity. The result? A comprehensive snapshot of your wealth in one place. Unlike traditional advisors, who are limited to the accounts they manage, Mezzi provides a view of everything.

"Mezzi's X-Ray feature allowed me to uncover exposure to stocks I didn't realize I had." - Shuping, founder of Summer AI

Armed with this holistic view, Mezzi goes a step further by helping you refine your tax strategy to maximize your wealth.

Minimize Your Tax Burden with Mezzi’s Insights

Taxes can quietly chip away at your long-term wealth. Mezzi works year-round to identify tax-loss harvesting opportunities, monitor wash sale risks across accounts, and recommend the best asset locations - whether it’s a Roth IRA, Traditional 401(k), or taxable brokerage account. These strategies may add 1% to 2% to your annual returns, which could mean an extra $10,000–$20,000 each year on a $1 million portfolio. For example, saving $10,221 on capital gains taxes and reinvesting those savings could grow that amount to $76,123 over 30 years.

Mezzi also provides personalized recommendations, including advanced tactics like the "mega backdoor" Roth, tailored to your tax situation. Beyond taxes, Mezzi ensures your retirement strategy stays aligned with your goals and adapts to market conditions.

Realistic Retirement Projections Based on Your Data

Most retirement calculators rely on generic assumptions, but Mezzi takes a different approach. By using data from your connected accounts - like current portfolio value, contributions, and fees - Mezzi generates projections that reflect your actual financial situation. These projections automatically update with market changes and personal adjustments, keeping your plan relevant and actionable.

You can even ask Mezzi’s AI questions such as, “How much more do I need to save each month to retire with $5 million by age 60?” and receive a tailored response in minutes.

"I loved chatting with the AI to make important changes to my portfolio. I haven't found another wealth app like Mezzi." - Tim, CEO of Somnee

This personalized guidance helps you stay on track toward your $5 million goal while avoiding the high fees that can eat into your wealth over time.

Conclusion

Retiring with $5 million is far from common. In fact, fewer than 0.1% of American retirees achieve this within their retirement accounts. When you factor in total net worth - like home equity, businesses, and other assets - only about 3.7% of U.S. households surpass the $5 million mark. Compare this to the median retirement savings of approximately $200,000 for individuals aged 65–74, and it becomes clear just how rare this level of wealth is.

These figures highlight the difficulty of reaching such a goal. However, its rarity doesn’t make it unimportant. What truly matters is having a well-thought-out, personalized plan instead of relying on one-size-fits-all assumptions. Achieving $5 million often calls for a combination of high earnings, disciplined saving, decades of market growth, and tax-efficient withdrawal strategies. For most people, the real challenge lies in crafting a strategy that can endure inflation, market swings, and rising healthcare expenses over a retirement that may span 30 to 40 years - issues that Mezzi’s platform is designed to help address.

"The $5 million goal isn't just about wealth - it's about freedom and peace of mind. Whether you reach that number or land somewhere lower, what matters is having a plan that works for your life." - Ivy Grace, Business Analyst

Mezzi equips you to take charge of your financial future by providing insights on par with those of a traditional advisor - without the typical 1% annual fee. With features like integrated account management, year-round tax-saving strategies, and tailored retirement projections based on your actual financial data, Mezzi helps you navigate market uncertainties and work toward building lasting wealth. Whether your target is $5 million or another figure, the platform offers the clarity and support needed to make confident financial decisions at every stage.

Financial independence ultimately comes down to understanding where you stand today, identifying what you’ll need tomorrow, and using the right tools to bridge that gap.

FAQs

Is $5 million enough to retire early in the U.S.?

Yes, having $5 million may allow you to retire early in the U.S., whether at 45, 55, or another age. However, whether it will be sufficient depends on several factors, including your lifestyle choices, annual expenses, and how you plan to withdraw and manage your funds. While many consider this amount to provide substantial financial security for an extended retirement, it’s essential to account for variables like inflation, taxes, and potential market fluctuations when making your plans.

How much would I need to save each month to reach $5 million?

The amount you may need to save each month to reach $5 million hinges on factors like your current age, the timeline for your goal, and your investment approach. A good starting point is using a retirement calculator. By entering details such as your current savings, anticipated rate of return, and financial objectives, you can get a clearer picture of what it might take. Regular saving and smart investing play a big role in reaching this target. For a more personalized strategy, consider working with a financial advisor who can help craft a plan suited to your unique circumstances.

What tax moves can help my money last longer in retirement?

Using strategies that aim to minimize taxes may help stretch your retirement savings further. Options to consider include maximizing contributions to tax-advantaged retirement accounts, utilizing tax-loss harvesting to offset gains, and evaluating whether Roth IRA conversions align with your financial goals. These methods are designed to potentially lower your tax burden and retain more of your wealth over the long term.

Disclosures:

- This content is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.

- Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.

- Savings and performance examples are hypothetical and for illustrative purposes only. Actual results will vary based on individual circumstances, portfolio composition, market conditions, and fees.

- Registration does not imply a certain level of skill or that the SEC has approved the company or its services.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.