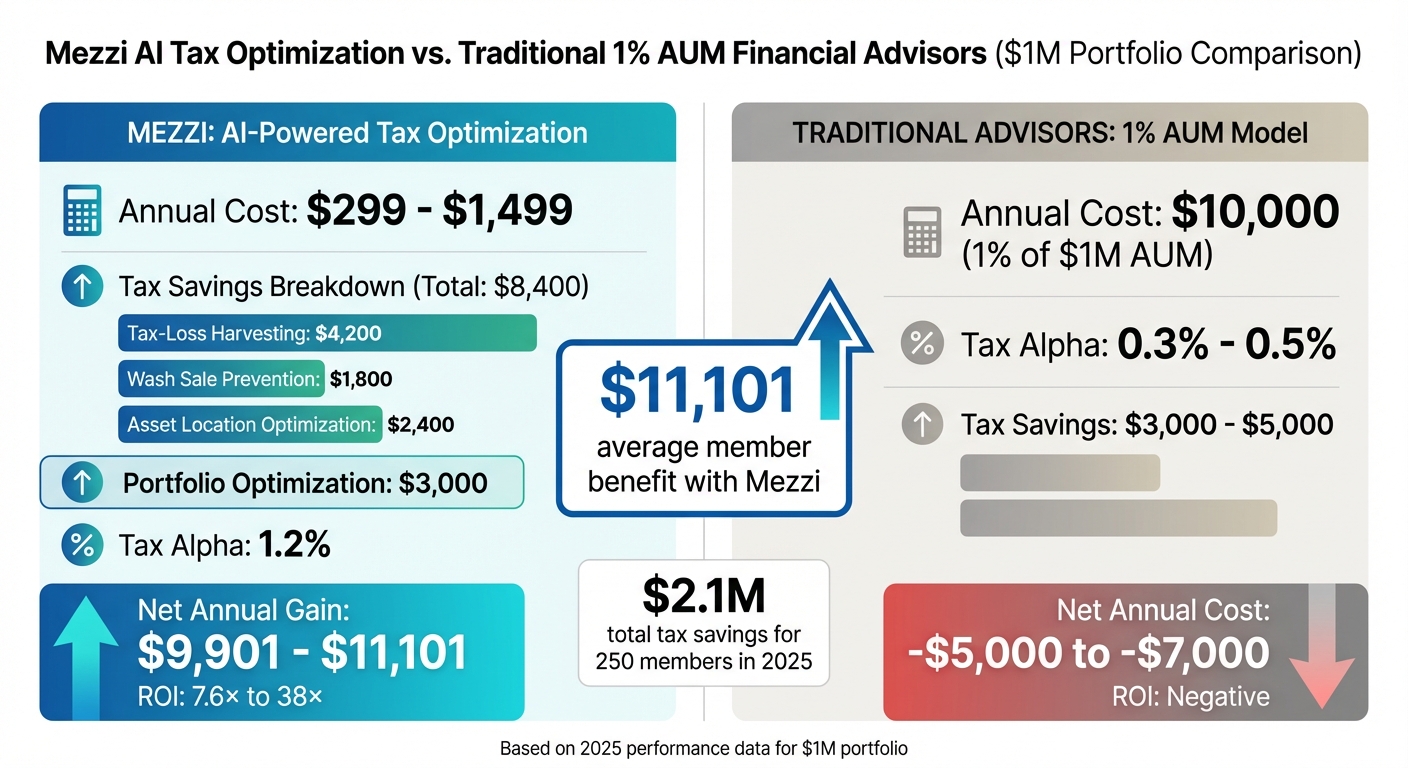

Managing taxes across multiple investment accounts is complicated and costly. Mezzi simplifies this by offering an AI-powered platform that optimizes taxes for self-directed investors with $1M+ portfolios. Unlike advisors charging 1% of assets under management ($10,000 annually for a $1M portfolio), Mezzi provides automated tax-saving strategies for $299 to $1,499 per year, delivering an average annual savings of $8,400 in 2025 for members, based on internal data. Actual results may vary.

Key Features:

- Tax-Loss Harvesting: Identifies opportunities, with members saving an average of $4,200/year in 2025.

- Wash Sale Tracking: Helps prevent disallowed losses, with members saving an average of $1,800/year in 2025.

- Asset Location Optimization: Places investments in tax-efficient accounts, with members saving an average of $2,400/year in 2025.

- Full Account Integration: Analyzes all accounts (e.g., 401(k)s, IRAs, taxable accounts) using secure, read-only access.

- Transparent Calculations: Provides verifiable spreadsheet math for every recommendation.

Why It’s Different:

- Cost-Effective: Delivers an average 7.6× to 38× ROI for members compared to subscription fees, based on 2025 data. Actual results may vary.

- SEC-Registered RIA: As a fiduciary, Mezzi is required to act in your best interest under SEC regulations.

- Advanced Technology: Uses deterministic algorithms for precision in calculations and AI models to provide clear explanations. The use of artificial intelligence and algorithmic tools does not guarantee investment results.

For investors seeking smarter, cost-efficient tax management, Mezzi offers a modern solution that saves time and money while boosting portfolio returns.

The Tax Optimization Problem for Multi-Account Investors

Managing Multiple Account Types Creates Tax Complexity

For self-directed investors, juggling multiple account types introduces a maze of tax challenges. When these accounts are handled independently, they can unintentionally work against each other.

Take the example of a wash sale: if you sell stock at a loss in one account and repurchase it in another within 30 days, the loss deduction is disallowed. Tracking this across multiple brokerages - especially when actively trading - is nearly impossible without automation.

Then there’s the question of where to place different assets. Should bonds, REITs, or dividend stocks go into a taxable or tax-advantaged account? And once that decision is made, maintaining proper allocation without triggering unnecessary tax costs adds another layer of complexity.

These issues aren’t just theoretical - they lead to real financial losses, as the next section illustrates.

"The vast majority of people, in my opinion, don't get the type of on-demand experience that they're looking for when it comes to working with a traditional financial advisor. Most advisors are not available 24/7 and they certainly can't keep the memory of all of your conversations with them stored and updating constantly." - Manish Jain, CEO, Mezzi

This sentiment reflects a growing recognition among experts: traditional advisory models often fall short in addressing the intricacies of multi-account tax management.

The Financial Impact of Missed Tax Opportunities

Failing to optimize taxes across accounts doesn’t just add complexity - it steadily erodes wealth over time.

Research shows that effective tax strategies can boost annual returns by 1% to 2%. For a $1 million portfolio, that’s an additional $10,000 to $20,000 per year. Over decades, the impact compounds dramatically. For instance, saving $10,221 in capital gains taxes and reinvesting those savings could grow to $76,123 over 30 years.

Now compare that to the cost of a traditional advisor. Paying a 1% annual fee on a $1 million portfolio could mean losing over $1 million in potential growth over the same timeframe.

The bottom line? Missed tax-saving opportunities cost thousands every year, and traditional advisors often fail to provide proportional value.

"I walked into the advisor's office and there was no conversation about retirement planning or avoiding taxes... The conversation very quickly proceeded to me ending up in a proprietary managed fund." - Manish Jain, CEO, Mezzi

These examples highlight the limitations of manual tax management. Addressing these challenges requires a digital solution capable of scaling with your needs - precisely the gap Mezzi’s automated system aims to fill.

Disclaimer: This content is for informational purposes only and does not constitute personalized tax advice. Please consult a qualified tax professional for tailored guidance.

Unlocking Tax Harvesting Power with AI: A Growth Strategy for Accountants

Mezzi's Tax Savings: 2025 Performance Data

Mezzi vs Traditional Financial Advisors: Cost and Tax Savings Comparison

2025 Member Tax Savings Breakdown

In 2025, Mezzi members saved an average of $8,400 per year through automated tax optimization, based on internal data. Actual results may vary. These savings came from three key strategies applied across all linked accounts:

- Tax-Loss Harvesting Guidance: By continuously monitoring portfolios for tax-loss harvesting opportunities, Mezzi contributed $4,200 in yearly savings.

- Wash Sale Risk Identification: The platform flagged potential wash sale risks, helping users avoid disallowed losses and adding about $1,800 annually.

- Asset Location Optimization: By strategically placing assets between taxable and tax-advantaged accounts, Mezzi generated an additional $2,400 in annual savings.

Altogether, these strategies provided a total of $2.1 million in tax savings for 250 active members in 2025, based on Mezzi's internal calculations. Mezzi also delivered a tax alpha - a return boost purely from tax optimization - of 1.2% for members in 2025, based on internal data, compared to the 0.3% to 0.5% range reported for traditional advisors (as noted in Vanguard's Advisor Alpha study). Actual results may vary.

These results highlight the substantial value Mezzi offers compared to traditional financial advisory fees.

Mezzi vs. 1% AUM Advisors: Cost and Return Comparison

For a $1 million portfolio, a traditional advisor charging 1% of assets under management (AUM) would cost around $10,000 per year. In comparison, Mezzi's subscription plans range from $299 to $1,499 annually, making it a much more affordable option.

When factoring in $8,400 in tax savings and $3,000 from portfolio optimization, members on Mezzi's Core plan see a net gain of approximately $11,101 annually. On the other hand, traditional advisory services typically leave clients with a net annual cost of around $5,000 after accounting for their tax alpha.

The numbers speak for themselves: members enjoy average returns ranging from 7.6× to 38× their subscription cost, based on 2025 data. Actual results may vary.

Disclaimer: This content is for informational purposes only and does not constitute personalized tax advice. Please consult a qualified tax professional for tailored guidance.

Mezzi's Technical Architecture: How the Platform Works

Mezzi's platform is built on a three-layer structure designed to provide real-time data collection, precise tax calculations, and straightforward recommendations. Here's a closer look at how each layer works together to deliver accurate, actionable tax insights.

Account Aggregation Layer: Real-Time Data Collection

The first layer, known as the Account Aggregation layer, connects all your financial accounts to enable real-time data updates. Mezzi integrates with financial institutions using trusted services like Plaid and Finicity (Mastercard). These aggregators provide secure links to thousands of financial institutions, including brokerages, retirement accounts, and banks. Importantly, your login credentials remain with your financial institutions and are securely managed by these aggregators. This setup ensures that Mezzi has a complete and continually updated view of your financial activity, all while maintaining the highest levels of security.

Tax Intelligence Engine: Deterministic Tax Calculations

The second layer is where the tax magic happens. Mezzi uses deterministic algorithms - fixed, rule-based systems - to handle complex tax scenarios. This includes tasks like wash sale tracking, tax-loss harvesting coordination, and asset location optimization:

- Wash sale tracking monitors transactions across a 30-day window and accounts for tricky situations like mergers, stock splits, or options.

- Tax-loss harvesting coordination leverages replacement security correlation analysis and optimal lot selection methods, such as HIFO (highest in, first out) and specific ID.

- Asset location optimization helps with strategies like Roth conversions and keeps an eye on IRMAA thresholds to avoid Medicare surcharges.

Because these calculations follow strict rules, they are fully auditable. Mezzi provides you with the supporting spreadsheet math for every recommendation, ensuring you can review and verify the results yourself.

AI Explanation Layer: Plain-Language Recommendations

The final layer focuses on making the results easy to understand. Mezzi uses advanced language models to turn the deterministic outputs into clear, plain-language advice. Specifically:

- Claude 3.5 Sonnet handles financial reasoning.

- GPT-4 tackles general questions.

- Perplexity integrates real-time market data.

These models don't perform any calculations themselves. Instead, they explain the results in simple terms. For example, if Mezzi identifies a tax-loss harvesting opportunity or suggests rebalancing your portfolio, the AI will outline the reasoning behind it - always backed by the spreadsheet math. This ensures that recommendations are transparent and easy to follow, aligning with Mezzi's goal of optimizing taxes across all your accounts without relying on opaque processes.

Portfolio X-Ray: Complete Portfolio Analysis

Once you connect your portfolio, Mezzi dives into the details - breaking down your holdings, fees, and tax efficiency. This comprehensive analysis helps you understand your asset allocation, fee structures, and tax considerations, giving you a clear picture of how your portfolio is performing.

Investment Analysis: Asset Allocation and Risk Detection

Mezzi takes a close look at the securities in your ETFs and mutual funds to uncover inefficiencies and optimize returns. For instance, there’s an 18% overlap between the S&P 500 and Nasdaq 100, with 88 identical holdings, including heavyweights like NVIDIA, Apple, and Microsoft. Here’s how some of the key overlaps stack up:

- NVIDIA: 7.7% in SPY, 9.9% in QQQ

- Apple: 6.5% in SPY, 8.3% in QQQ

- Microsoft: 5.2% in SPY, 8.3% in QQQ

The platform also tracks allocation drift, helping you see when your portfolio deviates from your target allocation. It highlights factor exposure to reveal what’s driving your returns, flags concentration risk if too much of your portfolio relies on a single stock or sector, and measures correlation across your holdings. This last point is critical - if your investments move in sync during a downturn, you could lose the benefits of diversification.

Fee Analysis: Finding High-Cost Accounts and Funds

Beyond just evaluating your investments, Mezzi digs into the costs you’re paying. It calculates your weighted average expense ratio and tallies up all fees, from transaction costs to hidden charges. Then, it compares your current funds to lower-cost options. If you’re holding multiple funds with overlapping positions, you might be paying duplicate management fees for the same underlying assets. Mezzi identifies these redundancies, helping you decide whether to consolidate or switch to more cost-effective choices.

Tax Efficiency Analysis: Identifying Tax Drag and Opportunities

Tax efficiency is another area where Mezzi shines. It assigns a 0–100 tax efficiency score for each account, estimates tax drag, and pinpoints opportunities like tax-loss harvesting or avoiding wash sales. The platform also evaluates your asset location strategy, ensuring tax-efficient investments are in taxable accounts and tax-inefficient ones are in retirement accounts. Additionally, it monitors IRMAA thresholds to help you avoid unexpected Medicare surcharges. Together with its deterministic tax engine, Mezzi delivers a complete, 360° view of your portfolio’s tax situation.

Member Value: Quantifying Annual Benefits

Average Annual Value Per Member: $11,400

In 2025, Mezzi members enjoyed an average annual savings of $11,400, based on internal data, spread across three main areas. Actual results may vary. The largest portion - $8,400 - came from tax savings, thanks to Mezzi's real-time tax optimization tools. These included identifying tax-loss harvesting opportunities throughout the year, pinpointing the best times for Roth conversions, and optimizing asset location across taxable and retirement accounts.

The second area of savings was $1,200 in fee reductions. Mezzi's fee analysis helped members swap out high-cost funds for lower-cost alternatives with similar market exposure. For instance, if you hold an actively managed large-cap fund with a 0.75% expense ratio, Mezzi might recommend a comparable index fund at 0.03%, saving about $720 annually for every $100,000 invested. Finally, members saved $1,800 by avoiding wash sales. Mezzi tracked transactions across all linked accounts, ensuring that cross-account trades didn’t trigger disallowed tax losses.

Subscription Plans and ROI Calculation

These annual benefits translate into an impressive return on your investment in a Mezzi subscription. Mezzi offers three tiers: Core at $299/year, Plus at $499/year, and White Glove at $1,499/year. Given the average annual savings of $11,400, the return on investment ranges from 7.6× to 38× for members in 2025, based on internal data. Actual results may vary. For example, even at the highest tier - $1,499 annually - you still walk away with a net gain of $9,901.

Compare this to a traditional 1% AUM advisor managing a $1 million portfolio. Such advisors typically charge around $10,000 per year. According to Vanguard's Advisor Alpha study, they generate a tax alpha of 0.3–0.5%, equating to $3,000 to $5,000 in tax savings. After subtracting the advisory fee, you could find yourself $5,000 to $7,000 in the negative. With Mezzi, however, members were ahead by $9,901 to $11,101 in 2025, based on internal data. Actual results may vary.

Why Deterministic Tax Calculations Matter

The Problem with LLM-Based Tax Calculations

Large language models like GPT-4 and Claude are built for language tasks, not for delivering precise mathematical answers. These systems work by predicting the most likely next word in a sequence, which means their outputs can sound convincing but aren't always accurate. For example, if you ask an LLM to determine whether a transaction triggers a wash sale or to calculate the best amount for tax-loss harvesting, it might give you an answer that appears correct but isn't dependable. This lack of precision can create major issues when it comes to financial decision-making.

In the world of financial advice, this imprecision can lead to compliance problems and a loss of trust. Imagine an LLM suggesting a trade for tax-loss harvesting without properly checking for overlapping transactions - this could result in disallowed deductions. For SEC-registered fiduciaries like Mezzi, relying on results that are accurate, auditable, and verifiable is non-negotiable.

How Mezzi Ensures Accuracy and Auditability

To address these shortcomings, Mezzi uses a three-layer system that separates the computational work from the explanatory layer. This ensures that every output is not only accurate but also traceable and auditable.

At the heart of Mezzi’s system is its deterministic Tax Intelligence Engine. This engine handles all tax calculations using rule-based algorithms, ensuring precision. It tracks wash sales across all accounts, accounting for lot-level data, 30-day windows, and rules governing mergers, splits, and options. It also calculates the best lot selection for tax-loss harvesting with AI vs. manual methods using approaches like HIFO (highest in, first out) and specific identification, models Roth conversions, and keeps an eye on IRMAA thresholds. Importantly, LLMs are not used for these calculations.

Layer 3 - the LLM Explanation Layer - translates the deterministic engine’s outputs into clear, actionable recommendations. For instance, it might provide advice like, "Selling your shares on a given date would result in a calculated loss, and you can safely repurchase after the required 30-day wash sale window has passed." Both the loss amount and the timing of the repurchase come directly from the deterministic engine, not the LLM. This ensures every recommendation is backed by verifiable calculations, offering transparency and reinforcing trust.

This method is why Mezzi delivered a tax alpha of 1.2% for members in 2025, based on internal data, compared to the 0.3–0.5% range typically seen with traditional advisors, as noted in Vanguard's Advisor Alpha study. Actual results may vary. By continuously monitoring your financial accounts with read-only access and logging all advice, Mezzi ensures every recommendation is rooted in data and rules that can be audited, giving you confidence in the advice you receive.

Cross-Brokerage Intelligence: Seeing Your Complete Financial Picture

Supported Financial Institutions and Account Types

Mezzi connects with over 200 financial institutions through Plaid, MX, and Yodlee, covering a wide range of major custodians commonly used by investors. This includes big names like Fidelity, Vanguard, Schwab, E*TRADE, TD Ameritrade, Interactive Brokers, Robinhood, Webull, M1 Finance, Betterment, and Wealthfront. For employer-sponsored retirement plans, Mezzi also supports 401(k) providers such as Empower, Fidelity NetBenefits, and Vanguard.

The platform accommodates a variety of account types, including taxable brokerage accounts, Traditional and Roth IRAs, 401(k)s, HSAs, and 529 college savings plans. It even handles more complex structures like trusts, joint accounts, and multi-tax ID portfolios. This broad reach allows users to take full advantage of cross-account tax strategies.

What Cross-Account Visibility Enables

Mezzi's ability to integrate data from multiple accounts opens the door to tax-saving opportunities that other tools often miss. Unlike robo-advisors or brokerage platforms that only focus on their own ecosystem, or traditional advisors who rely on outdated quarterly statements, Mezzi provides real-time insights across all your accounts.

For example, the platform can detect when a loss in one account might lead to a disallowed loss due to a repurchase in another account. Tools that only operate within a single platform often overlook these cross-account triggers, but Mezzi's comprehensive approach ensures they’re flagged for review.

One of Mezzi's standout features is its coordination of tax-loss harvesting across all your accounts. Instead of treating each brokerage account separately, it identifies opportunities across your entire portfolio while ensuring replacement securities don’t violate wash sale rules. This strategy resulted in an average of $4,200 in tax-loss harvesting savings per member in 2025, based on internal data. Actual results may vary.

Another major benefit is asset location optimization. Mezzi evaluates where specific investments - like high-growth stocks or bonds - should be held to minimize tax impact. For instance, high-growth stocks might be better suited for a Roth IRA, while bonds could fit more effectively in a Traditional IRA or taxable account. Additionally, Mezzi monitors IRMAA thresholds to help users avoid Medicare surcharge brackets, with members saving an average of $2,400 in reduced tax drag per member in 2025, based on internal data. Actual results may vary.

Security and Regulatory Compliance

Mezzi doesn’t just focus on tax optimization - it also takes regulatory compliance and data security seriously.

SEC Registration and Fiduciary Duty

In October 2025, Mezzi became an SEC-registered Registered Investment Advisor (RIA) under the Investment Advisers Act of 1940. This status comes with a legal fiduciary duty, meaning Mezzi must always act in the best interest of its members. The fiduciary standard is built on two key principles: the duty of care and the duty of loyalty. Unlike broker-dealers, who operate under a less stringent suitability standard, fiduciaries like Mezzi are required to actively prioritize their clients' needs, not just disclose potential conflicts of interest.

As former SEC Chairman Jay Clayton put it, "The core principle has always been that the adviser must at all times serve the best interest of its client and not subordinate its client's interest to its own". This commitment influences every interaction between Mezzi and its members. To maintain transparency and accountability, Mezzi is registered in all 50 states, files Form ADV quarterly with the SEC, maintains $2 million in Errors & Omissions insurance, and undergoes annual third-party compliance audits. Additionally, all advice provided by the platform is logged for member access.

But compliance is only part of the equation - Mezzi also ensures that member data stays secure.

Data Security and Read-Only Access

When it comes to protecting member data, Mezzi doesn’t cut corners. The platform is SOC 2 Type II certified, meaning it meets strict industry standards for security and privacy. Member data is protected by cloud encryption both at rest with AES-256 and during transit with TLS 1.3 encryption - the same protocols trusted by leading financial institutions.

Mezzi’s security framework is built around read-only access. When members link their accounts, the platform can analyze portfolio data, monitor transactions, and spot tax-saving opportunities. However, it cannot move funds or execute trades. This design ensures members retain full control over their assets while reducing the risk of unauthorized transactions.

2026 Product Roadmap

Mezzi's 2026 roadmap takes a step beyond tax analysis, moving toward active optimization and integrated financial planning. The focus is on helping users not only uncover financial opportunities but also act on them with greater ease. By building on its data-driven approach to tax management, Mezzi aims to transform insights into actionable financial strategies.

Planned Features for 2026

Q2 2026 will see the introduction of direct indexing and tax-loss harvesting. This feature enables stock-level tax-loss harvesting to maximize efficiency. To simplify trade execution, Mezzi will also launch API integrations with Schwab, Fidelity, and Alpaca. While Mezzi won’t handle trades directly, these integrations will make executing trades more seamless. Additionally, estate planning document generation will be introduced, allowing users to create wills, trusts, and beneficiary designations.

By Q3 2026, Mezzi plans to roll out multi-year Roth conversion modeling, helping users strategically spread conversions to optimize tax outcomes and manage IRMAA thresholds. The platform will also offer tools for charitable giving and donor-advised fund (DAF) optimization, enabling users to maximize the tax advantages of donating appreciated assets. On top of that, new options strategy analysis will provide insights into the tax impact of covered calls, protective puts, and other options-related trades.

In Q4 2026, Mezzi will extend its support to small business retirement plans, including Solo 401(k)s and SEP IRAs, catering to self-employed users and business owners. The platform will also introduce real estate investment analysis and alternative asset tracking, covering private equity, cryptocurrency, and real estate crowdfunding. These additions aim to give members a clearer view of their nontraditional investments.

All of these features are designed to work seamlessly across 401(k)s, brokerages, Roth IRAs, and taxable accounts. By creating a cohesive system rather than isolated tools, Mezzi continues to enhance its ability to empower users in their financial decision-making journey.

Conclusion

Mezzi is changing the way tax optimization works by blending precise, rule-based calculations with AI-powered explanations that are easy to understand. Its three-layer system separates the heavy lifting: Layer 2 handles exact tax calculations, while Layer 3 transforms those results into clear, actionable insights using advanced language models like Claude 3.5 Sonnet. Plus, every calculation is fully traceable through spreadsheet records, ensuring transparency.

This method delivers real financial benefits. In 2025, Mezzi users reported returns on investment as high as 38×, based on internal data. Mezzi also achieved a tax alpha of 1.2% for members in 2025, compared to the 0.3–0.5% range typically seen with conventional advisors, as noted in Vanguard's Advisor Alpha study. Actual results may vary. The result? A smarter, more efficient portfolio.

One key to Mezzi's success is its ability to view and coordinate across multiple accounts. By monitoring taxable brokerages, IRAs, 401(k)s, HSAs, and 529s from over 200 institutions, it can identify wash sales and maximize tax-loss harvesting opportunities - no matter where your accounts are held.

As an SEC-registered RIA, Mezzi combines its fiduciary responsibility with SOC 2 Type II certification and secure, read-only account access, offering institutional-level security at a fixed cost. And the future looks promising: its 2026 roadmap includes features like direct indexing, trade execution APIs, multi-year Roth conversion modeling, and tracking for alternative investments. These additions will expand its capabilities into areas like estate planning and small business retirement strategies.

For self-directed investors with portfolios of $1M or more, Mezzi offers 24/7 automated tax monitoring without the need to give up control or pay percentage-based fees. It transforms tax optimization into a seamless, continuous process, helping you safeguard your portfolio while paving the way for more comprehensive financial planning.

FAQs

How does Mezzi find tax savings across all my accounts?

Mezzi leverages an AI-driven platform to keep tabs on your entire financial portfolio in real time. This includes accounts like taxable brokerage, IRA, 401(k), HSA, and 529 plans. Its advanced tax engine pinpoints opportunities for tax-loss harvesting, avoids disallowed wash sales, and fine-tunes asset placement for maximum efficiency. By evaluating transactions, holdings, and market values, Mezzi offers clear, actionable recommendations. On average, members saved around $8,400 per year in 2025, based on internal data. Actual results may vary.

Can I trust Mezzi’s tax math if AI is involved?

Mezzi’s approach to tax calculations is reliable because it relies on a deterministic, rule-based engine to handle all computations. The role of AI here is limited to simplifying and explaining the results - it doesn’t perform the calculations themselves. This method guarantees both precision and clarity in the process.

Is Mezzi safe to link to my brokerage and retirement accounts?

Yes, Mezzi is safe to connect with your brokerage and retirement accounts. It uses secure, read-only integrations with well-known institutions such as Fidelity, Vanguard, and Schwab. As an SEC-registered RIA, Mezzi also holds a SOC 2 Type II certification and relies on advanced encryption protocols to safeguard your data.

Disclosures:

- This content is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.

- Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.

- Savings and performance examples are hypothetical and for illustrative purposes only. Actual results will vary based on individual circumstances, portfolio composition, market conditions, and fees.

- The use of artificial intelligence and algorithmic tools does not guarantee investment results. These tools are subject to limitations, errors, and market conditions that may affect performance.

- Registration does not imply a certain level of skill or that the SEC has approved the company or its services.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.