When inflation rises, your investment returns can lose value in real terms. To protect against this, you have three main options: I Bonds, TIPS, and VTIP. Each works differently:

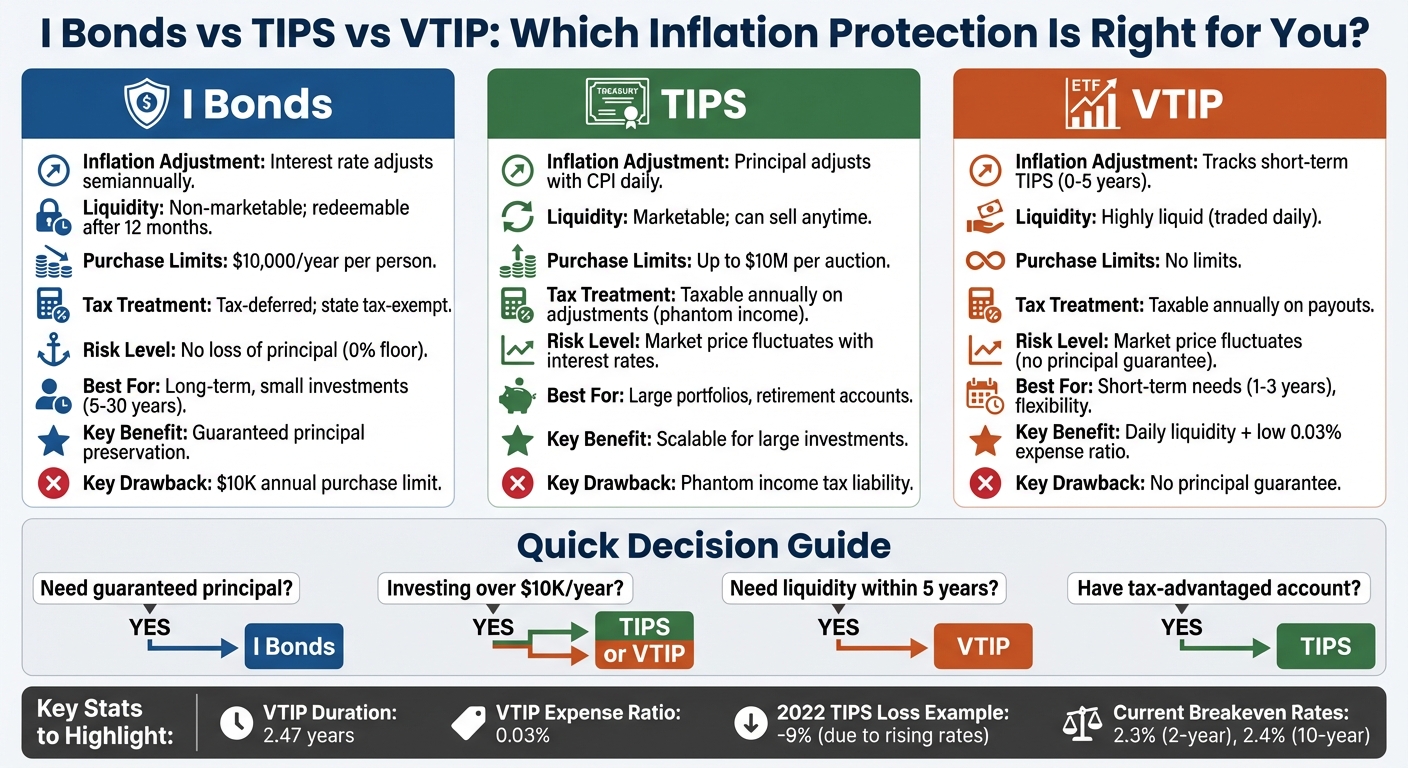

- I Bonds: U.S. savings bonds with rates tied to inflation. They guarantee your principal, grow tax-deferred, and are ideal for smaller investments. However, they have purchase limits and early redemption restrictions.

- TIPS (Treasury Inflation-Protected Securities): Bonds that adjust their principal with inflation. They’re good for larger portfolios and can be traded or held to maturity. Taxation on annual inflation adjustments can complicate things.

- VTIP (Vanguard Short-Term TIPS ETF): A fund holding short-term TIPS, offering liquidity and monthly payouts. It’s a flexible option but doesn’t guarantee your principal.

Quick Comparison

| Feature | I Bonds | TIPS | VTIP |

|---|---|---|---|

| Inflation Adjustment | Interest rate adjusts semiannually | Principal adjusts with CPI | Tracks short-term TIPS (0–5 years) |

| Liquidity | Non-marketable; redeemable after 12 months | Marketable; can sell anytime | Highly liquid (traded daily) |

| Purchase Limits | $10,000/year per person | Up to $10M per auction | No limits |

| Tax Treatment | Tax-deferred; state tax-exempt | Taxable annually on adjustments | Taxable annually on payouts |

| Risk | No loss of principal | Market price fluctuates | Market price fluctuates |

| Best For | Long-term, small investments | Large portfolios, retirement | Short-term needs, flexibility |

Each option serves a different purpose. I Bonds may be appropriate for smaller, low-risk investments. TIPS may fit large portfolios or tax-advantaged accounts. VTIP may offer liquidity for short-term goals. Consider your timeline, tax situation, and investment size. when evaluating these options.

I Bonds vs TIPS vs VTIP: Complete Comparison Chart for Inflation Protection

How Each Inflation-Protection Tool Works

How TIPS Work

TIPS (Treasury Inflation-Protected Securities) safeguard your investment by adjusting their principal in line with changes in the Consumer Price Index (CPI). When inflation rises, the principal increases; during deflation, it decreases. However, at maturity, you are guaranteed to get back at least your original principal. The interest rate for TIPS is set at auction (with a minimum of 0.125%), but because this rate is applied to the inflation-adjusted principal, your semiannual interest payments can vary. As TreasuryDirect explains:

"The principal of your TIPS goes up and down with inflation and deflation. While the interest rate is fixed, the amount of interest you get every six months may vary based on any change in the principal."

For instance, based on TreasuryDirect data from March 2026, if you invested $1,000 in a 5-year TIPS with a 0.125% interest rate and an Index Ratio of 1.01165, your adjusted principal would be $1,011.65. This adjustment would result in a semiannual interest payment of about $0.63. This structure ensures your investment maintains its purchasing power, regardless of inflation or deflation.

How I Bonds Work

I Bonds take a different approach to inflation protection by adjusting their interest rate instead of the principal. They offer a composite rate, which combines a fixed rate (unchanging for up to 30 years) with a semiannual inflation adjustment based on the CPI-U. This rate compounds every six months, ensuring your investment keeps pace with inflation. For example, bonds issued between November 1, 2025, and April 30, 2026, carry a composite rate of 4.03%, which includes a fixed rate of 0.90% and a 1.56% semiannual inflation rate. The formula for calculating the composite rate is:

Fixed rate + (2 × semiannual inflation rate) + (fixed rate × semiannual inflation rate).

Even in periods of deflation, the composite rate cannot fall below 0%. This ensures that your investment grows over time, maintaining its value and shielding your portfolio from inflationary pressures.

How VTIP Works

VTIP (Vanguard Short-Term Inflation-Protected Securities ETF) offers a market-based alternative for inflation protection, focusing on short-term TIPS with maturities of 0–5 years. It tracks the Bloomberg US Treasury Inflation-Protected Securities 0–5 Year Index, holding about 26 short-term TIPS that adjust their principal in response to CPI changes. Because of its short-term focus, VTIP has lower sensitivity to interest rate changes. For example, as of September 2023, its average effective duration was 2.47 years. Morningstar analyst Mo'ath Almahasneh explains:

"Targeting short-term TIPS strengthens the fund's sensitivity to inflation because short-term interest rates are more correlated with inflation than long-term rates and the inflation protection embedded in the fund's performance isn't overshadowed by interest-rate risk."

VTIP also offers practical advantages, such as an ultra-low expense ratio of 0.03% and high trading liquidity, with over 3.3 million shares traded monthly. Unlike I Bonds, VTIP doesn't have purchase limits or redemption penalties. As of February 25, 2026, VTIP traded at approximately $49.79 per share, offered an annual dividend yield of 3.78%, and managed around $16.3 billion in assets. This makes it a flexible option for investors seeking inflation protection.

Best Inflation Protection for 2025: VTIP TIPS or I Bonds

Pros and Cons of I Bonds, TIPS, and VTIP

Here’s a closer look at the strengths and weaknesses of TIPS, I Bonds, and VTIP, building on how each works.

TIPS: Pros and Cons

TIPS (Treasury Inflation-Protected Securities) adjust their principal daily based on the Consumer Price Index, making them a solid option for inflation protection. You can buy up to $10 million per auction, which caters well to large portfolios. Another perk is their liquidity - you can sell them anytime on the secondary market. As PIMCO points out:

TIPS offer the U.S. government's assurance that investors will never receive less than the original face value of the bond at maturity, even in the event of deflation.

However, TIPS come with some tax headaches. Every year, you’ll owe federal taxes on the inflation adjustments to the principal - even though you won’t see that money until the bond matures. This is often called "phantom income". Additionally, TIPS are sensitive to interest rate changes. When real interest rates climb, TIPS prices drop. For example, in 2022, TIPS funds saw an average loss of 9% due to rising rates.

I Bonds: Pros and Cons

I Bonds are known for preserving your capital - they won’t lose value even during deflation, thanks to a 0% floor on their composite rate. Christine Benz, Director of Personal Finance at Morningstar, highlights their appeal:

I bonds are considered a source of inflation-adjusted yields by some analysts..

They also offer tax advantages, letting you defer federal taxes until you cash them in, and the interest is exempt from state and local taxes.

On the flip side, I Bonds come with purchase limits - you’re capped at $10,000 per Social Security number each year, plus an extra $5,000 if using your tax refund. They’re non-marketable, meaning you can’t sell them to other investors. Liquidity is another limitation: you can’t cash them for the first 12 months, and redeeming them within five years will cost you the last three months of interest.

VTIP: Pros and Cons

VTIP (Vanguard Short-Term Inflation-Protected Securities ETF) provides daily liquidity, professional management, and a rock-bottom expense ratio of just 0.03%. Unlike individual TIPS, VTIP pays out both interest and inflation adjustments monthly, giving you cash flow to handle tax liabilities. Its short-term focus (average duration of about 2.5 years) makes it less sensitive to interest rate changes compared to long-term bonds.

That said, VTIP doesn’t guarantee your principal. Unlike holding individual TIPS to maturity, VTIP’s value fluctuates with market conditions. If you need to sell during a market downturn, you could lose money. As Real Money Moves explains:

TIPS ETFs can lose money short-term even when inflation rises, if rates rise faster. This isn't a flaw; it's bond mechanics.

You’ll also owe taxes on the distributions each year, similar to individual TIPS.

These factors highlight the trade-offs, helping you decide which option aligns with your financial goals.

Which Inflation-Protection Tool Is Right for You?

Choosing the right tool to guard against inflation depends on your financial goals, how accessible you need your funds to be, and how long you plan to invest. Here's a breakdown to help you decide.

When to Choose TIPS

TIPS (Treasury Inflation-Protected Securities) are a strong choice for investors with larger portfolios who need to exceed the annual purchase limit for I Bonds. If inflation outpaces current breakeven rates - around 2.3% for 2-year TIPS and 2.4% for 10-year TIPS as of November 2025 - TIPS can deliver solid inflation-adjusted returns. They’re best suited for long-term investors who can hold them until maturity, avoiding the ups and downs of market prices.

To sidestep phantom income taxes on TIPS, consider using tax-advantaged accounts like IRAs or 401(k)s. As Christine Benz from Morningstar points out:

the purchase limitations on I bonds are so restrictive that for larger investors, TIPS are the only way to build meaningful inflation protection.

When to Choose I Bonds

I Bonds may be appropriate if your main goal is preserving capital. Unlike TIPS, the value of I Bonds never drops below your initial investment, making them a safe choice during deflation or economic uncertainty. They also come with tax perks, such as deferring federal taxes until redemption and avoiding state and local taxes altogether.

However, keep in mind the restrictions: you must hold I Bonds for at least 12 months, and redeeming them within the first five years means forfeiting three months’ worth of interest. If you’re saving for a financial goal 5 to 30 years down the road and can work within the annual purchase limits, I Bonds offer a stable, inflation-adjusted return without any price volatility. Plus, if you meet the criteria for the education tax benefit, the interest earned can be tax-free when used for qualified higher education expenses.

When to Choose VTIP

For those who need daily liquidity and want to limit interest rate risk, VTIP (Vanguard Short-Term Inflation-Protected Securities ETF) could be the answer. With a duration of 2.4 years, a 1% increase in interest rates would typically reduce VTIP’s price by about 2.4%, which is less than the impact on broader TIPS funds. This may make VTIP suitable for protecting cash you might need in the next 2 to 5 years or during periods when interest rates are expected to rise.

VTIP’s ETF structure allows you to access your funds instantly during market hours, and its low 0.03% expense ratio is hard to beat. It also provides monthly distributions that include both interest and inflation adjustments, offering cash flow to help manage taxes. However, VTIP doesn’t guarantee your principal like individual TIPS do if held to maturity - selling during a market downturn could result in a loss.

Each of these tools serves a different purpose, so considering your specific financial needs is important for managing inflation risk.

Final Thoughts on Inflation Protection

Shielding your portfolio from inflation involves several tools, each with its own strengths. I Bonds, TIPS, and VTIP cater to different financial needs and timelines. I Bonds, with their guaranteed principal and zero risk, are a great fit for smaller investments, especially given the $10,000 annual purchase limit. For larger portfolios and retirement planning, TIPS can be a strong choice, particularly when held to maturity in tax-advantaged accounts. On the other hand, VTIP offers liquidity and lower volatility, making it ideal for short-term needs (generally 1 to 3 years). Your selection should align with your investment horizon and tax strategy.

To refine your approach, consider how each option fits your tax situation and timeline, including asset location strategies. For example:

- I Bonds: Use these in taxable accounts to defer taxes until redemption. They may also qualify for tax-free treatment if used for education expenses and you meet income requirements.

- TIPS and VTIP: Holding these in tax-advantaged accounts like IRAs or 401(k)s can help you avoid taxes on phantom income.

It’s important to remember that inflation-protection tools are designed to preserve purchasing power, not to generate significant growth. Unlike stocks, these securities aim to maintain value. For instance, in 2022, despite soaring inflation, many TIPS funds experienced losses because rising interest rates drove prices down. This highlights the importance of your holding period - while short-term fluctuations can be painful, the long-term benefits often outweigh the volatility.

For smaller portfolios, purchasing the annual maximum of I Bonds may be an option to consider. Larger investors, however, may need to focus on building a TIPS ladder or integrating VTIP to achieve meaningful inflation protection. While I Bonds offer inflation-adjusted yields, their purchase limits may make them less practical for substantial investments. If you’re looking for a more detailed evaluation of your strategy, tools like Mezzi may help analyze tax efficiency and identify ways to improve your inflation hedge while monitoring costs.

FAQs

Should I hold TIPS to maturity or use VTIP instead?

Choosing whether to hold TIPS until maturity or invest in VTIP really comes down to your financial goals and how much risk you're willing to take. If you hold TIPS to maturity, you get a steady, inflation-adjusted return, which is perfect if you're looking to avoid interest rate risk. On the other hand, VTIP, a short-term TIPS ETF, gives you liquidity, diversification, and the option to sell anytime. This makes it a good choice for short-term inflation protection, especially if you're okay with market ups and downs.

How do taxes differ for I Bonds vs TIPS vs VTIP?

Taxes work differently for I Bonds, TIPS, and VTIP, and understanding these differences is key.

- I Bonds: These allow you to defer federal taxes until you redeem them. Plus, they might qualify for tax exclusions if used for education expenses, making them an attractive option for certain savers.

- TIPS: With TIPS, you’ll face annual taxes on both the interest earned and any inflation adjustments, even if you haven’t cashed them out. This can result in a tax liability before you see the cash.

- VTIP: As a short-term TIPS ETF, VTIP shares the same tax treatment as TIPS. However, selling shares can also trigger capital gains taxes, adding another layer to consider.

Each option has its own tax implications, so it’s worth evaluating them based on your financial goals and tax strategy.

What’s the best inflation hedge for money I need in 1–5 years?

For those looking to hedge against inflation over a 1–5 year period, a short-term TIPS fund like VTIP may be an option to consider. VTIP focuses on Treasury Inflation-Protected Securities (TIPS) with maturities under five years. This approach may provide a balance of inflation protection and reduced interest rate risk.

With a short duration of about 2.5 years, VTIP provides greater stability compared to longer-term TIPS funds. It adjusts effectively for inflation without exposing investors to significant interest rate fluctuations.

While I Bonds are excellent for longer-term goals, their annual purchase limits and liquidity restrictions can make them less practical for shorter timeframes. For immediate inflation hedging needs, VTIP is often the more convenient and accessible choice.

Related Blog Posts

- How can I diversify my portfolio with ETFs before retiring in a few years?

- Are municipal bond funds preferable to U.S. Treasury funds for residents of specific states?

- SGOV vs BIL vs SHV vs TFLO - Best T-bill ETF for cash parking in a taxable account

- TIP vs SCHP vs VTIP - Best TIPS ETF for inflation protection in an IRA

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.