Switching from a robo-advisor requires careful planning to avoid unnecessary fees, tax implications, or disruptions to your portfolio. Robo-advisors are convenient for beginners but may not address complex financial needs like managing multiple account types, optimizing taxes, or handling stock compensation. This guide outlines a step-by-step process to assess your current setup, prepare for the transition, and rebuild your portfolio with greater control.

Key Steps:

- Evaluate Fees and Services: Combine advisory fees and fund expenses to determine your total costs. Identify gaps in services like tax strategies or account integration.

- Organize Documents: Download agreements, fee schedules, statements, and tax forms. Understand transfer terms, potential fees, and tax consequences.

- Choose Your New Strategy: Decide whether to keep your current custodian or switch. Use tools like Mezzi to connect accounts and refine your portfolio.

- Prepare for Transfer: Disable automated features like rebalancing or dividend reinvestment. Review tax implications and consult a CPA for complex cases.

- Transfer and Rebuild: Opt for in-kind transfers where possible to avoid triggering taxes. Use tools to consolidate holdings, optimize asset placement, and automate contributions.

By following these steps, you can transition smoothly and take greater control of your financial planning.

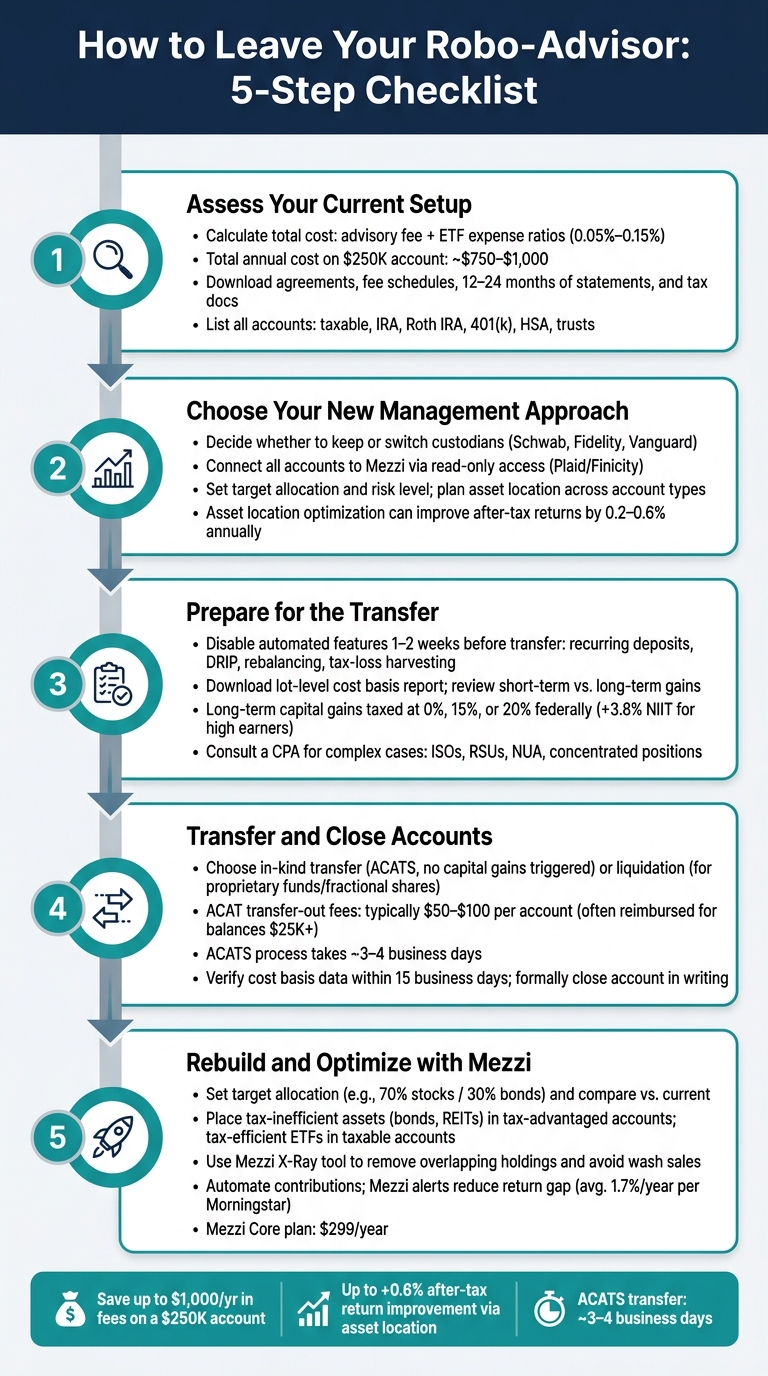

How to Leave Your Robo-Advisor: 5-Step Checklist

Step 1: Assess Your Current Robo-Advisor Setup

Take a close look at your current robo-advisor setup by examining fees, services, and any areas where it might fall short.

Review Fees and Service Gaps

Start by figuring out your total cost - this goes beyond just the advisory fee your robo-advisor advertises. Combine the management fee with the average expense ratios of the ETFs in your portfolio. With typical ETF expense ratios falling between 0.05% and 0.15%, the total annual cost for a $250,000 account could range from $750 to $1,000.

Basic robo-advisor plans typically include automated rebalancing and tax-loss harvesting for taxable accounts. However, access to a CFP® professional usually requires upgrading to premium tiers, which often come with higher account minimums. Advanced tax strategies - like Roth conversions, managing RSUs, or planning for multi-year capital gains - are rarely part of the package at any level. Additionally, if your robo-advisor doesn’t account for your 401(k), HSA, or stock compensation accounts, it’s only addressing a portion of your overall financial picture.

Be sure to document these fee details before moving on to gather your account paperwork.

Download Your Account Documents

For each account, download and save these key documents:

| Document | Why It Matters |

|---|---|

| Client/advisory agreement | Details termination terms, transfer restrictions, and any prorated fees you might face |

| Fee schedule | Outlines ACAT transfer-out fees (usually $50–$100 per account), wire fees, and closure charges |

| Recent account statements (12–24 months) | Verifies holdings, cost basis, and cash balances - critical for ensuring a smooth transfer |

| Tax documents (Form 1099, gain/loss reports) | Essential for your CPA and for tracking potential tax consequences from liquidating positions |

The client agreement deserves extra attention. Search for terms like "termination", "in-kind transfer," and "ACAT" to determine whether your robo-advisor allows you to transfer investments directly or requires you to sell everything first. This information will be crucial as you prepare your account inventory in the next step.

List All Accounts and Holdings

Create a detailed spreadsheet to track every account, including taxable brokerage accounts, Traditional IRAs, Roth IRAs, rollover IRAs, joint accounts, and trusts. For each account, note the following:

- Account type and custodian

- Current market value in U.S. dollars

- Cash balance

- A detailed holdings list with ticker symbols, share quantities, and cost basis

Also, document any automated features like recurring deposits, rebalancing, dividend reinvestment plans (DRIP), and tax-loss harvesting. These features need to be turned off systematically before initiating a transfer to avoid unexpected transactions during the process. This thorough inventory will serve as a roadmap for making informed decisions in the next steps.

Step 2: Choose Your New Management Approach

Once you've organized your account inventory, it's time to decide how you'll manage your investments moving forward.

Separate Your Custodian from Your Advice Source

You don't need to move your assets to use Mezzi. Your custodian - the institution holding your assets - and your advice source - the entity guiding your decisions - can remain independent.

If your current custodian offers low fees, diverse investment options, and reliable tax reporting, there's no pressing need to switch. You can keep your accounts at Schwab, Fidelity, Vanguard, or wherever you prefer, and simply layer Mezzi on top for planning and analysis. This approach avoids the hassle of ACAT fees, extra paperwork, or concerns about market timing.

That said, if your current custodian charges higher fees, has limited investment choices, or provides subpar tax-lot reporting, switching might be worth considering. These factors could make it harder to implement Mezzi's recommendations effectively.

Once you've settled on your custodian setup, the next step is to securely connect your accounts to Mezzi for a complete analysis.

Connect Your Accounts to Mezzi

Mezzi uses read-only access through Plaid and Finicity (Mastercard) to link to your accounts. This connection allows Mezzi to view balances, positions, and transaction histories - but never your login credentials or funds.

The process is simple: through Mezzi's interface, you select your financial institution, authenticate using a secure portal, and choose which accounts to link. You remain in control of what information is shared and can revoke access whenever you choose.

For the best results, connect all your investment accounts, including taxable accounts, IRAs, 401(k)s, HSAs, and 529 plans. This comprehensive view enables Mezzi to provide guidance tailored to your entire household portfolio. Research on asset location suggests that strategically placing investments across account types could improve after-tax returns by around 0.2–0.6 percentage points annually. However, this level of optimization requires a full picture of your holdings.

Set Your Target Allocation and Risk Level

Once your accounts are connected, it's time to refine your strategy. Mezzi consolidates your holdings across all custodians, account types, and asset classes, giving you a complete view of your portfolio.

From there, you can set a target allocation and define your preferred risk level. This involves reviewing your stock-to-bond ratio based on factors like your time horizon, income stability, and comfort with market fluctuations. Applying this target across all your accounts ensures consistency and helps you stay on track during market downturns.

Mezzi also assists with asset location - deciding which assets belong in which account types. For example, tax-inefficient investments like bond funds or REITs are often better suited for tax-advantaged accounts like a Traditional IRA or 401(k), while tax-efficient index funds might be a better fit for taxable accounts. Planning this out in advance minimizes mistakes and sets the stage for a tax-conscious portfolio from the start.

Step 3: Get Ready for the Move

Now that you've set up your new management approach, it's time to ensure your current robo-advisor accounts are fully inactive before initiating any transfers. Skipping this step is a common reason for delays or incomplete transfers. Once you've prepared, take steps to disable any automated features to keep the process seamless.

Turn Off Automated Features

Robo-advisors often run several background automations, such as recurring deposits, automatic rebalancing, dividend reinvestment, and tax-loss harvesting. If any of these processes activate during your transfer, they could create complications like new tax lots, delays in the Automated Customer Account Transfer Service (ACATS), or trades that are difficult to reverse.

To avoid these issues, disable all automated features 1–2 weeks before starting the transfer:

- Recurring deposits and auto-invest: Stop new cash inflows by disabling these features.

- Dividend reinvestment (DRIP): Set dividends to "pay to cash" to prevent fractional shares from being created during the transfer.

- Automatic rebalancing: Turn this off to avoid last-minute trades that could impact your holdings.

- Tax-loss harvesting: Disabling this feature prevents wash-sale rules from complicating future reallocation decisions.

Take screenshots of these changes with timestamps as a record for your audit trail.

Review Tax Implications Before You Transfer

This step is especially important for taxable brokerage accounts, as selling investments in these accounts typically triggers capital gains taxes. However, this doesn’t apply to accounts like IRAs, Roth IRAs, or 401(k)s, where selling is generally tax-free. For taxable accounts, the financial impact of selling depends on factors like how long you’ve held your investments and your tax bracket.

To make an informed decision between an in-kind transfer or liquidation, download a lot-level cost basis report from your robo-advisor. This report provides details like purchase dates, cost basis, and unrealized gains or losses for each position. Tools like Mezzi’s tax insights can help analyze this data, highlighting short-term versus long-term gains and identifying positions where selling might be costly or where realizing a loss could work in your favor. Remember, long-term capital gains are taxed federally at 0%, 15%, or 20%, depending on your income, with an additional 3.8% Net Investment Income Tax for higher earners.

Additionally, some robo-advisors use proprietary ETFs or mutual funds that cannot be transferred in-kind. These positions must be liquidated, so identifying them early allows you to plan for the potential tax impact.

Bring in a Tax Professional for Complex Situations

In certain scenarios, consulting a CPA or enrolled agent before transferring your portfolio can be invaluable. Complex cases might include:

- Large, concentrated positions in a single stock

- Recently exercised incentive stock options (ISOs) or vested RSUs

- Employer stock with net unrealized appreciation (NUA) inside a 401(k)

- A recent significant income event, such as a business sale or inheritance, that temporarily places you in a higher tax bracket

These situations often involve intricate interactions between your portfolio changes and your overall tax strategy. Mistakes in these cases can be costly, so professional advice may save you more than the consultation fee.

When meeting with a CPA, bring relevant documents such as downloaded statements, 1099s, cost-basis reports, and a summary of your new plan. Providing as much context as possible enables your tax professional to model the potential tax outcomes of different transfer strategies. They may even suggest spreading sales across multiple tax years if it aligns better with your financial goals.

Step 4: Transfer and Close Your Robo-Advisor Accounts

Now that you've prepared your accounts and tax documents in Step 3, it's time to move forward with the actual transfer. This step ensures your assets are migrated properly while keeping your tax records in order.

Choose Between In-Kind Transfer or Liquidation

When transferring your investments, you have two main options: an in-kind transfer or liquidation. The choice depends on your holdings and your goals.

An in-kind transfer lets you move your shares directly to your new custodian using the Automated Customer Account Transfer Service (ACATS). This approach avoids selling your investments, which means no capital gains are triggered, and you stay invested throughout the process. As Jeffrey Barnett, Founder of Fintegrity LLC, explains:

"The most important thing to understand about ACATS is this: your investments transfer in-kind. That means the shares of stock, bonds, and ETFs you own at your current firm move directly to your new firm. Nothing is sold. No capital gains are triggered."

However, liquidation may be necessary in certain situations. For example, if your robo-advisor holds proprietary funds or fractional shares, these must often be sold because ACATS doesn’t support them. The cash from these sales will then be transferred along with any whole shares.

Here’s a quick comparison of the two options:

| In-Kind Transfer | Liquidation | |

|---|---|---|

| Tax Impact | None | May trigger capital gains or losses in taxable accounts |

| Market Exposure | Fully invested | Out of the market while cash is in transit |

| Best For | Stocks, bonds, ETFs | Proprietary funds or fractional shares |

Before deciding, confirm with your new custodian which of your current holdings they’ll accept. This step can help you avoid unexpected forced sales.

Start the Transfer Through Your New Custodian

Once you’ve chosen your transfer method, initiate the process through your new custodian’s platform. Transfers use a "pull" system, meaning your new custodian will electronically request your assets from your previous firm.

Before starting, gather your latest account statement to verify details like account numbers and types. If your account type doesn’t match (e.g., trying to move a Roth IRA to a standard brokerage account), the transfer won’t go through. Also, if your name has changed due to marriage or divorce, you may need to provide additional documents.

You can opt for a full transfer (moving the entire account) or a partial transfer (specific holdings only). Once your request is submitted, your robo-advisor typically has 1–3 business days to respond, and the full ACATS process usually takes about 3–4 business days as of 2026.

Be aware of potential fees. Most robo-advisors charge $50–$100 to transfer an account, but many receiving custodians may reimburse this fee if your account balance meets certain thresholds. For example, balances starting at $25,000 may qualify for a reimbursement, with some custodians waiving fees entirely for accounts over $250,000. Check with your new custodian for details before initiating the transfer.

Once the transfer process begins, keep an eye on its progress to ensure everything moves smoothly.

Track the Transfer and Confirm Account Closure

Most custodians offer a transfer status tracker, which allows you to monitor the process in real-time. Transfers often happen in stages, with whole shares moving first, followed by cash from any fractional share liquidations or pending dividends.

After your assets have arrived, verify the cost basis data. By law, the delivering firm must provide cost basis details for covered securities within 15 business days. Cross-check this information with your final robo-advisor statement to ensure accuracy.

"At Fintegrity®, we verify every tax lot after a transfer is complete. If something does not look right, we research it and correct it before making any portfolio decisions that depend on cost basis accuracy." - Jeffrey Barnett, Fintegrity LLC

Finally, formally close your robo-advisor account. Send a written notice via email and certified mail requesting a stop to all trading activity. Ask for a final statement of holdings and a fee summary. Before your portal access is removed, download your last account statements. These records will be essential if any discrepancies arise during tax season.

Step 5: Rebuild and Optimize Your Portfolio with Mezzi

Now that your accounts are all in one place, it’s time to focus on reshaping your portfolio. Mezzi offers tools and insights to help you take a more deliberate approach to allocation and management.

Rebuild Your Portfolio Allocation

Start by setting a clear target allocation for your entire portfolio - something like 70% stocks and 30% bonds, for example. Mezzi can help you compare your current allocation against this target, making it easier to spot any gaps.

When restructuring, consider tax efficiency. Place tax-inefficient assets, such as taxable bonds, REITs, or high-turnover funds, in tax-advantaged accounts like a Traditional IRA or 401(k). On the other hand, tax-efficient assets like broad-market equity ETFs or index funds are often better suited for taxable accounts, where long-term capital gains and qualified dividends benefit from favorable U.S. tax treatment. Unlike a one-off allocation change, Mezzi provides ongoing insights to help you adjust your holdings dynamically. This approach allows you to shift assets across account types when needed, all while avoiding unnecessary taxable events. According to Vanguard research, disciplined strategies like these may add as much as 3 percentage points to net annual returns for U.S. investors.

Remove Overlapping Holdings with Mezzi's X-Ray Tool

Once you’ve set your target allocation, it’s time to refine your holdings. Robo-advisors often use simplified fund lineups, which can create unintentional redundancies. For example, you might end up with multiple large-cap ETFs that essentially track the same stocks, leading to duplicate fees.

Mezzi’s X-Ray tool dives into the details of your ETFs and mutual funds, uncovering overlapping securities. By identifying these overlaps, you can consolidate your positions. In taxable accounts, consider selling loss positions first to offset gains, followed by positions with smaller gains to minimize tax impact. Mezzi also helps you avoid wash sales by flagging risks if you sell a position at a loss and plan to buy a similar security within 30 days.

Set Up Automations That Match Your Plan

Reestablish recurring contributions and automate the flow of funds into underweighted asset classes. When it comes to dividend reinvestment, think about the account type: automatic reinvestment is often a good fit for retirement accounts, while in taxable accounts, some investors prefer receiving dividends as cash. This allows for more strategic reinvestment, avoiding adding to overweighted positions.

Mezzi’s alerts keep you informed about allocation drift, idle cash, and tax opportunities throughout the year - not just during tax season. According to Morningstar’s "Mind the Gap" study, U.S. investors have historically seen their dollar-weighted returns trail their funds’ time-weighted returns by about 1.7 percentage points annually over a decade. This gap often stems from poor timing and inconsistent rebalancing. By using Mezzi’s automated safeguards, you can help ensure your portfolio stays aligned with your strategy, even as market conditions shift.

Conclusion: Taking Control of Your Portfolio with Mezzi

Taking charge of your investments is a step-by-step journey, and leaving a robo-advisor requires careful planning. By following the five steps - assess, choose, prepare, transfer, and rebuild - you can create a portfolio you truly understand and feel confident managing.

The key distinction between robo-advisors and Mezzi lies in transparency and control. Robo-advisors often operate behind the scenes, while Mezzi provides a unified view of all your accounts. This means you can clearly see your risk exposure, overlapping holdings, and potential tax considerations across your entire portfolio.

One standout feature of Mezzi is its tax insights. It highlights potential tax implications - such as short- versus long-term capital gains, wash sale risks across accounts, and asset placement between taxable and tax-advantaged accounts - before you make decisions. While Mezzi isn’t a tax preparer, it equips you with the information your CPA may need, especially for more intricate scenarios like RSUs, concentrated positions, or Roth conversions.

Staying on track with your financial plan becomes more manageable with Mezzi. A simple quarterly review can help you monitor allocation drift, spot tax-loss harvesting opportunities, and ensure your strategy aligns with your goals. Mezzi also alerts you to areas that may need attention, such as idle cash, significant allocation shifts, or unrealized losses worth addressing - helping you focus on actionable insights rather than unnecessary distractions.

At $299 per year, Mezzi’s Core plan offers tax-aware guidance and comprehensive portfolio insights at a fraction of what traditional advisors might charge. It’s a cost-effective way to gain the clarity and control you need to manage your investments confidently.

FAQs

Will moving my account trigger taxes?

Whether transferring your account results in taxes often depends on how the transfer is handled. In-kind transfers usually don't trigger taxes because your investments move as-is, keeping their original cost basis and holding periods intact. On the other hand, cash transfers involve selling your investments, which may create a taxable event and lead to capital gains taxes.

For retirement accounts, a direct trustee-to-trustee transfer typically avoids taxes. However, if you withdraw funds instead, you could face income taxes and possibly early withdrawal penalties. It's also important to check if all your assets are eligible for an in-kind transfer before proceeding.

How long does an ACATS transfer take?

When transferring assets through ACATS, the process typically spans 3–6 business days once your new firm initiates the request. Here's how it generally unfolds:

- Day 1: Your previous firm reviews and validates the transfer request.

- Up to 3 days: Any discrepancies or issues are addressed and resolved.

- Final 3 days: The assets are transferred to your new account.

Keep in mind, cost basis details might not transfer immediately. These usually arrive separately, often within 15 business days following the initial asset transfer.

What should I do with fractional shares and proprietary funds?

Fractional shares and proprietary funds often cannot be moved in-kind using the Automated Customer Account Transfer Service (ACATS). This means you may need to sell these investments before transferring, which could result in a taxable event, such as capital gains taxes if there's a profit. Another option is to keep these assets with your current provider while transferring the rest of your portfolio.

Disclosures:

- This content is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.

- Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.

- Savings and performance examples are hypothetical and for illustrative purposes only. Actual results will vary based on individual circumstances, portfolio composition, market conditions, and fees.

- Mezzi is not a tax preparer. Users should consult a qualified tax professional for personalized tax advice.

- Registration does not imply a certain level of skill or that the SEC has approved the company or its services.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.