Mezzi and Altruist serve different types of investors. Mezzi is designed for individuals who want control over their investments with AI-driven insights, while Altruist is a platform used by financial advisors to manage client portfolios. Here's a quick breakdown:

- Mezzi: For self-directed investors. It analyzes your accounts (like IRAs, 401(k)s, and brokerage accounts) to provide guidance on tax strategies, portfolio risks, and retirement planning. You stay in control of decisions and execution. Costs start at $299/year.

- Altruist: For those who prefer an advisor to manage their portfolio. Advisors use Altruist to handle trading, tax strategies, and reporting. Investors access updates via an advisor-provided portal. Fees are typically based on a percentage of assets under management.

Quick Comparison

| Feature | Mezzi | Altruist |

|---|---|---|

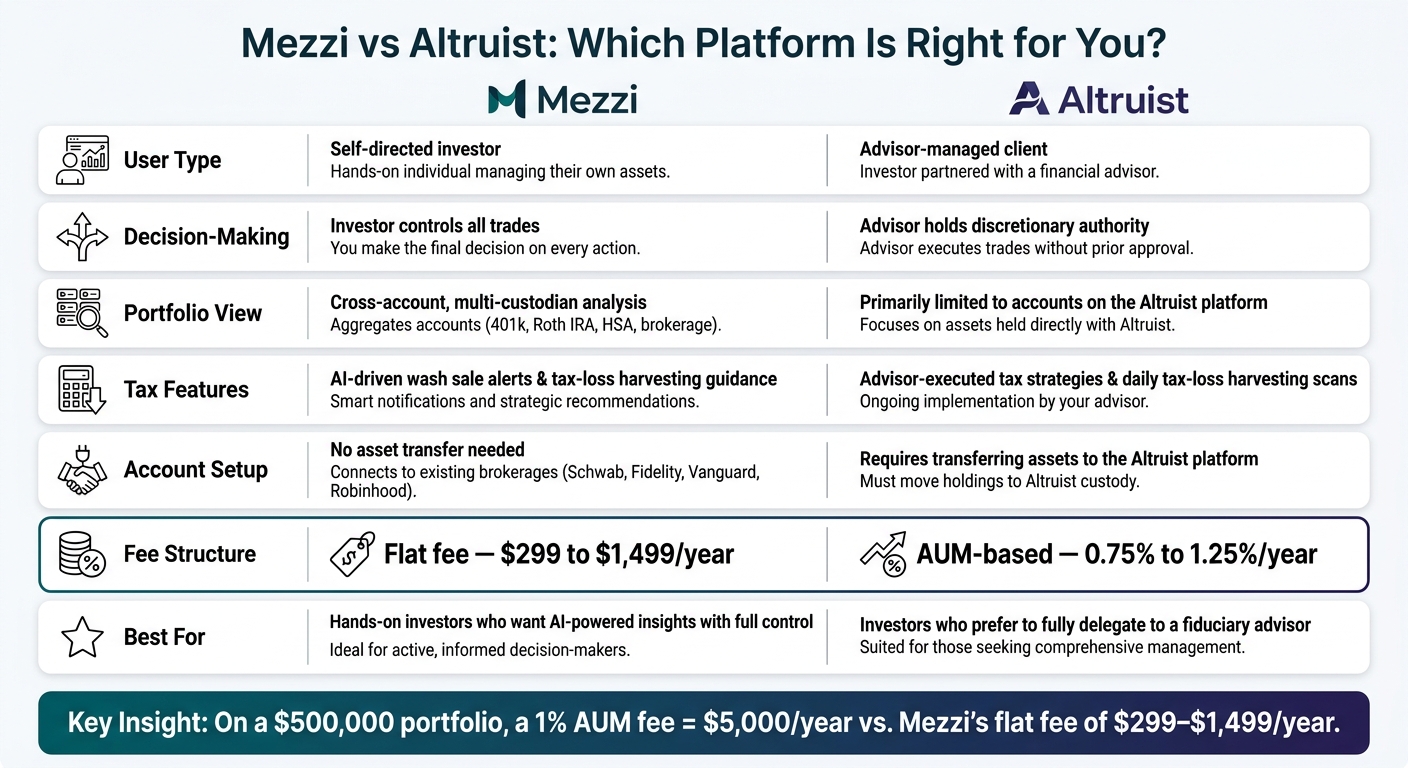

| User Type | Self-directed investors | Advisor-managed clients |

| Decision-Making | Investor makes decisions | Advisor makes decisions |

| Account Setup | Uses existing accounts | Requires transferring assets |

| Tax Guidance | AI-driven suggestions | Advisor-executed strategies |

| Fees | Flat fee ($299–$1,499/year) | AUM-based (0.75%–1.25%) |

Your choice depends on whether you want to manage your investments yourself or prefer a professional to handle it for you.

Mezzi vs Altruist: Self-Directed vs Advisor-Led Investing Compared

Mezzi for Self-Directed Investors

Key Features and Tools

Mezzi provides four essential tools designed to give you a full picture of your financial situation.

- Account aggregation: This feature brings together data from all your accounts - 401(k), Roth IRA, traditional IRA, taxable brokerage, and HSA - into one place. It helps you see your overall asset allocation and risk exposure across different custodians.

- Tax optimization guidance: Mezzi identifies opportunities throughout the year, such as potential tax-loss harvesting, alerts for wash sale risks, and suggestions for improving asset location.

- Portfolio X-Ray: This tool dives deep into your ETFs and mutual funds, breaking them down into individual holdings to highlight overlaps and concentration risks that might otherwise go unnoticed.

- Retirement planning: Using real data from your connected accounts, this tool models your projected retirement income, calculates success probabilities, and shows the financial impact of changes like retiring early or increasing your 401(k) contributions.

| Feature | What It Does |

|---|---|

| Account Aggregation | Combines all account types into a unified view using Plaid/Finicity. |

| Tax Optimization | Highlights tax-loss harvesting, wash sale risks, and asset location tweaks. |

| Portfolio X-Ray | Exposes overlapping holdings, sector concentration, and duplicate funds. |

| Retirement Planning | Uses real account data to model outcomes and test financial adjustments. |

These tools work together, turning insights into clear, actionable steps.

How Mezzi Works

Mezzi connects to your existing accounts securely through read-only integrations. Its AI engine analyzes your account balances, holdings, and types to generate personalized recommendations. Importantly, Mezzi doesn't access your brokerage login credentials and cannot move money or execute trades - its role is purely to provide analysis and guidance. Acting as a dashboard for your investments, Mezzi organizes everything in one place, allowing you to make informed decisions and execute them directly through your brokerage accounts.

Who Should Use Mezzi?

Mezzi is designed for investors who value having control over their decisions but also want expert insights to guide them. It’s particularly suited for professionals like physicians or tech workers who actively manage their finances. Mezzi is especially helpful for those with multiple accounts across different custodians, including a mix of taxable and tax-advantaged accounts. Each tool is built to support self-directed investing, offering portfolio analysis, tax efficiency strategies, and retirement planning - all while keeping you in the driver’s seat.

Altruist for Advisor-Led Management

Core Features for Advisors

Altruist provides an all-in-one custody and execution platform, combining custody, trading, rebalancing, reporting, and billing into a single system.

Its automated rebalancing feature uses a "review and release" process. This means the platform generates optimized trades for advisors to review, helping portfolios stay on track without the need for constant manual adjustments. Over a full market cycle, this disciplined approach may add approximately 20–40 basis points in annualized returns. Additionally, Altruist performs daily tax-loss harvesting scans for taxable accounts, identifying opportunities to reduce tax burdens. This process may result in an after-tax benefit of 0.5% to 1.3% annually. When combined with intelligent asset location strategies, these tools have the potential to deliver 130–200+ basis points of annualized after-tax value.

The platform also offers access to a Model Marketplace with over 500 professionally managed models. These include direct indexing options that feature values-based screens powered by Smartleaf and MSCI. Costs are kept low, with some models starting at 0 basis points and others costing up to three times less than the average TAMP.

Altruist's "Hazel" AI engine simplifies routine tasks by drafting client plans, answering advisor questions, and pulling data from CRM notes and emails. Advisors have praised its impact:

"Hazel has been a game changer for our firm. It actually improves how we communicate our value to prospects, trains us to be better after every meeting, and even drafts the first version of our client plans." - Dave Zoller, CFP, Streamline Financial Services

These features work together to streamline advisory processes while ensuring investors benefit from optimized, automated portfolio management.

How Altruist Serves Investors

Altruist extends its advisor-focused tools to deliver institutional-level strategies directly to clients. While clients do not interact with the platform themselves, they benefit from their advisor’s use of it. Advisors handle all trade execution, while clients enjoy access to a co-branded mobile app and desktop portal. These tools provide real-time updates on performance, holdings, and tax savings. Through this setup, strategies like direct indexing and tax-sensitive rebalancing - once only available to ultra-high-net-worth investors - are now accessible to a broader audience. This blend of technology and human oversight ensures efficient and precise wealth management.

Security is a top priority. Assets are held in segregated accounts with SIPC protection, which is further backed by excess coverage from Lloyd's of London. Additionally, cash accounts are insured up to $3 million for individual accounts and $6 million for joint accounts through partner banks.

Who Should Use Altruist?

Altruist is designed for investors who prefer a hands-off approach, relying on their advisor to handle strategy, tax efficiency, and daily management. It’s not a platform for direct client use but serves as infrastructure for advisors to deliver a seamless experience. Investors who value a fiduciary advisor and appreciate the combination of human expertise with automated tools may find Altruist especially appealing.

"The advantage of Altruist's technology is not that it replaces human judgment - it amplifies it." - Mark Stancato, CFP®, VIP Wealth Advisors

Currently, over 6,000 independent advisors use Altruist, and it was recognized as the #1 highest-rated custodian in the 2026 T3/Inside Information Software Survey.

Could an AI Co-pilot be Better Than Your Financial Advisor?

Mezzi vs. Altruist: Side-by-Side Comparison

Mezzi provides self-directed investors with actionable insights, setting itself apart from Altruist’s advisor-driven approach.

Investing Approach and Control

The key difference between Mezzi and Altruist lies in decision-making. Mezzi puts you in control, offering AI-driven insights like tax-loss harvesting opportunities, concentration risks, and rebalancing suggestions. You decide whether to act and execute trades through your existing brokerage. Altruist, on the other hand, operates under an advisor-led model. Advisors have discretionary authority to make portfolio adjustments, implement model changes, and apply tax strategies without requiring your approval for each move.

This distinction can be especially important during market volatility or major life changes. Mezzi users can quickly respond to market shifts by reviewing AI-flagged opportunities and acting directly through their brokerage accounts. Altruist clients, however, rely on their advisor’s expertise and timing to make portfolio changes.

Next, let’s look at how these platforms differ in portfolio oversight and tax management.

Portfolio and Tax Management Features

Mezzi offers a comprehensive cross-account view by linking multiple accounts such as 401(k)s, Roth IRAs, taxable brokerage accounts, and HSAs. This multi-custodian perspective helps identify risks like wash sales and duplicate exposures across accounts. Altruist’s platform focuses on optimizing tax strategies within accounts held directly on its platform. While advisors can manage tax strategies effectively within these accounts, they may lack the broader, cross-custodian visibility that Mezzi provides.

Account Structure and Custody

Mezzi integrates with your existing brokerage accounts, whether that’s Schwab, Vanguard, Fidelity, or Robinhood. There’s no need to move assets or sign new custodial agreements. Altruist, however, requires transferring assets to its platform, which involves opening new accounts and signing custodial and advisory agreements. While centralizing accounts on Altruist can streamline management, it also means leaving behind established relationships with your current brokerages.

These structural differences also influence the overall cost for investors.

Pricing and Value for Investors

Mezzi uses a flat annual fee structure, ranging from $299 per year for the Core plan to $1,499 per year for the White Glove plan, regardless of portfolio size. Altruist advisors typically charge fees based on assets under management (AUM), with rates commonly between 0.75% and 1.25% per year, billed quarterly.

The difference in pricing becomes more pronounced as portfolio sizes grow. For example, a 1% AUM fee can lead to much higher costs compared to Mezzi’s flat-fee model. For investors who are comfortable making decisions based on AI insights, Mezzi’s pricing may represent significant savings as portfolio values increase.

| Factor | Mezzi | Altruist |

|---|---|---|

| Primary User | Self-directed investor | Financial advisor (RIA) |

| Decision-Making | Investor controls all trades | Advisor holds discretionary authority |

| Portfolio View | Cross-account, multi-custodian analysis | Primarily limited to accounts on the platform |

| Tax Features | AI-driven wash sale alerts and tax-loss guidance | Advisor-executed tax strategies and rebalancing |

| Custody | Assets remain at current brokerages | Assets held on the Altruist platform |

| Fee Structure | Flat subscription ($299–$1,499/year) | AUM-based fees (0.75%–1.25% per year) or retainer |

| Best For | Investors seeking direct control with AI guidance | Investors who prefer to delegate decisions |

Choosing Between Mezzi and Altruist

Questions to Ask Before Deciding

When weighing your options, it helps to reflect on a few key considerations. How involved do you want to be in managing your investments? If you'd rather delegate everything, an advisor-led platform like Altruist might align with your needs. For those who value seeing all their accounts in one place without the hassle or cost of consolidating, Mezzi provides that comprehensive overview. Cost is another factor - traditional advisory fees often grow with your portfolio, whereas Mezzi charges a flat fee, offering consistency regardless of account size.

Answering these questions can help clarify which platform better suits your investment approach.

Matching Investor Profiles to Each Platform

Mezzi caters to individuals who prefer hands-on involvement in their financial decisions. If you're comfortable analyzing insights, making decisions independently, and want tools for tax optimization and asset allocation, Mezzi offers these features without requiring you to move or consolidate accounts. It’s ideal for those who want control and a clear, unified view of their finances.

Altruist, by contrast, is tailored for those who prefer to delegate entirely. It’s designed to support advisory firms rather than individual investors directly. For example, in February 2026, Gerber Kawasaki Wealth & Investment Management - managing over $4 billion in assets - chose Altruist as its custodial partner. CEO Ross Gerber stated:

"We're entering a rapid growth phase, and Altruist is the partner to help us scale... we're moving all new business to Altruist to streamline operations and accelerate our path to $10 billion."

This highlights Altruist's role as a modern platform for advisors, enabling clients to benefit from advanced infrastructure while maintaining an advisor-client relationship.

Final Takeaways

Deciding between Mezzi and Altruist ultimately comes down to how much control you want over your investments. Mezzi is geared toward those seeking autonomy, transparency, and fiduciary-grade insights without paying traditional AUM fees. Meanwhile, Altruist functions as a streamlined solution for advisors, ideal for investors who prefer to rely on professional guidance. Your choice should reflect your preferred level of involvement and control.

FAQs

Can Mezzi suggest actions without being able to trade?

Mezzi doesn't execute trades on your behalf. Instead, it provides AI-driven insights and recommendations to help inform your decisions. If you decide to act on these suggestions, you'll need to manually execute trades through your current brokerage account.

How does Mezzi spot wash sales across multiple brokerages?

Mezzi works to identify potential wash sales across multiple brokerages by securely linking to your investment accounts through providers such as Plaid and Finicity. It keeps an eye on your portfolios, monitoring for possible wash sale violations. When risks are detected, it sends timely alerts, helping you stay within the rules and adjust your investment approach as needed.

When does a flat Mezzi fee beat an AUM advisor fee?

When your portfolio falls within the range of approximately $50,000 to $100,000, Mezzi’s flat fee may be a more budget-friendly option compared to the typical 1% fee charged by advisors based on assets under management (AUM). To illustrate, a 1% fee on a $50,000 portfolio amounts to $500 annually, which is higher than Mezzi’s fixed subscription cost, ranging from $199 to $499 per year. For smaller to mid-sized portfolios, this predictable pricing structure may result in notable savings over percentage-based AUM fees.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.