Choosing between Mezzi and Retirable depends on your financial goals and stage of life. Mezzi is ideal for self-directed investors who want AI-powered tools to optimize their portfolios, reduce taxes, and maintain control over their investments. Retirable, on the other hand, caters to those nearing or in retirement, offering tailored strategies for Social Security, pension management, and creating sustainable income streams.

Key Takeaways:

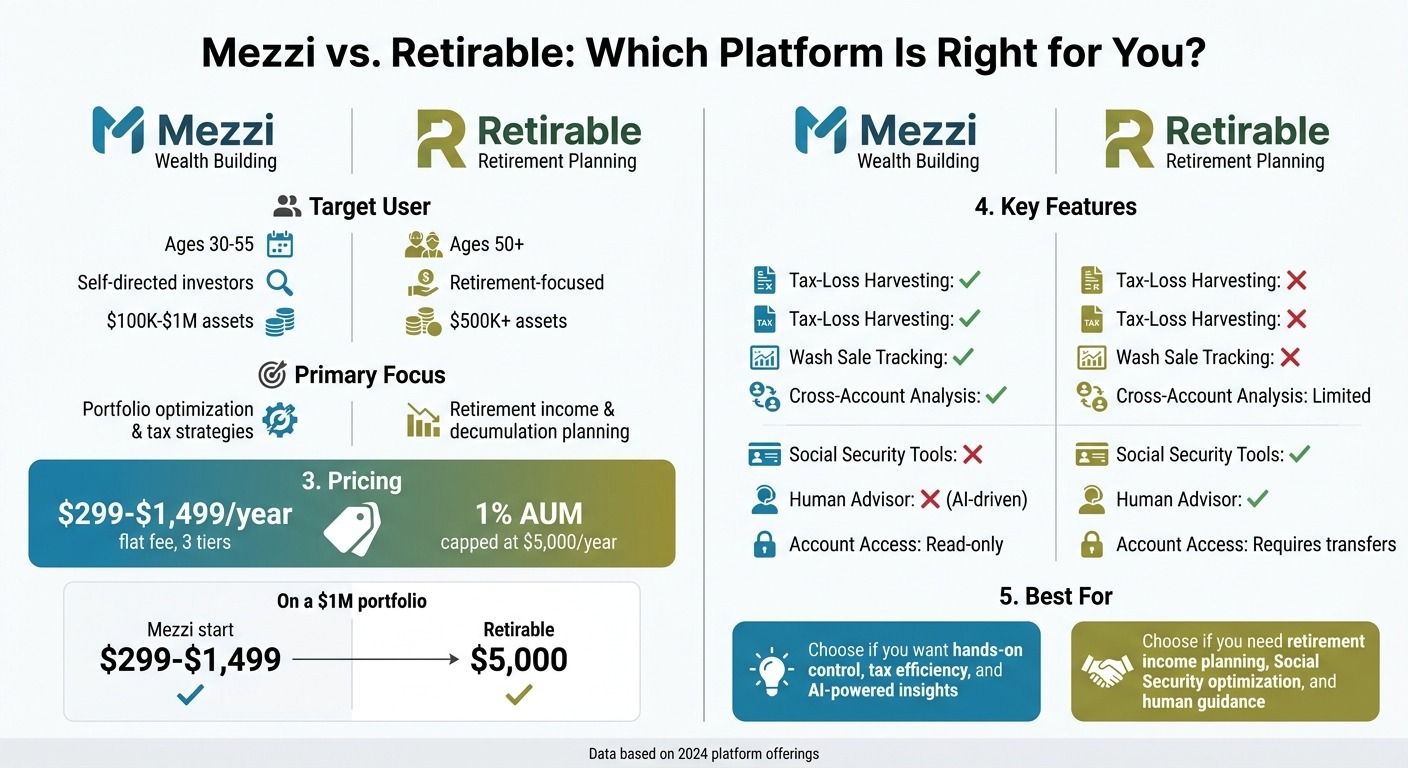

- Mezzi: Best for investors aged 30–55 focused on growing wealth and using AI for tax and portfolio strategies. Flat pricing starts at $299/year.

- Retirable: Designed for individuals 50+ managing retirement income. Includes human advisors and charges 1% of assets under management, capped at $5,000/year.

Quick Comparison

| Feature | Mezzi (Wealth Building) | Retirable (Retirement Planning) |

| Focus | Portfolio optimization and tax strategies | Retirement income and decumulation planning |

| Pricing | $299–$1,499/year (flat fee) | 1% AUM, capped at $5,000/year |

| Human Advisor | No, AI-driven advice | Yes, dedicated fiduciary advisor |

| Tax-Loss Harvesting | Yes | No |

| Social Security Tools | No | Yes |

| Account Access | Read-only | Requires account transfers |

If you want to grow your wealth with hands-on control, Mezzi is a better fit. If your priority is retirement income stability, go with Retirable.

Mezzi vs Retirable: Feature and Pricing Comparison Chart

Platform Overview: Mezzi vs. Retirable

Mezzi: AI-Driven Fiduciary Advice

Mezzi is an SEC-registered fiduciary platform designed to provide advisor-level guidance for self-directed investors - without charging the typical 1% assets under management (AUM) fee. It securely connects to all your accounts - like 401(k)s, brokerage accounts, Roth IRAs, and taxable accounts - using read-only access, ensuring your assets remain untouched.

What sets Mezzi apart is its ability to analyze all your accounts, not just managed ones. This approach helps detect wash sale risks, overlapping ETF holdings, and improves asset location across different account types. Its AI chat assistant uses real account data to deliver customized portfolio insights and trade suggestions. Additionally, Mezzi offers features like tax-loss harvesting insights and retirement planning guidance, making it a comprehensive tool for investors. Got a tricky financial question? Mezzi’s AI assistant is ready to provide actionable advice whenever you need it.

On the other hand, Retirable focuses on a different stage of financial planning: retirement.

Retirable: Retirement-Focused Planning

Retirable is tailored to help individuals transition from building wealth to managing it during retirement. It offers tools to project income, design withdrawal strategies, and create customized plans to ensure a steady flow of retirement income.

While Mezzi focuses on real-time portfolio optimization, Retirable zeroes in on structural retirement planning. It helps users determine sustainable withdrawal rates, decide on the best timing for Social Security benefits, and manage pension income effectively. This focus is significant because advised investors tend to experience less financial stress (14%) compared to self-directed investors (27%). Furthermore, 86% of advised clients report feeling more at ease with their financial situation.

Feature Comparison

Mezzi and Retirable tackle wealth management with distinct approaches, which is evident in their feature offerings. Mezzi emphasizes portfolio efficiency and tax strategies across all accounts, catering to both wealth-building and maintenance. Retirable, on the other hand, focuses on retirement income planning, ensuring users can turn their savings into a steady income stream.

Mezzi stands out for its cross-account analysis capabilities. It can pinpoint portfolio overlaps in ETFs and mutual funds, flag wash sale risks, and suggest tax-efficient rebalancing strategies. The platform’s AI chat assistant adds another layer of usability, offering real-time, personalized advice based on your connected account data. Whether it’s Roth conversions, asset location decisions, or tax-loss harvesting, Mezzi provides year-round tools tailored for self-directed investors.

Retirable takes a different path, excelling in decumulation planning, which focuses on transitioning from saving to spending during retirement. It offers tools to project retirement income, create withdrawal strategies, and optimize Social Security benefits. These features are designed for individuals nearing or entering retirement who need to manage pension income and develop sustainable spending plans.

This divergence in focus leads to differences in how the platforms operate. Mezzi uses read-only access to provide fiduciary-level advice without executing trades, empowering users to act independently. Retirable, meanwhile, concentrates on structural planning and projections, helping retirees design a sustainable financial future.

Feature Comparison Table

| Feature | Mezzi | Retirable |

| Tax-Loss Harvesting Guidance | Identifies candidates year-round | - |

| Wash Sale Tracking | Flags wash sale risks across accounts | - |

| Portfolio Overlap Detection | X-Ray tool reveals hidden exposure in ETFs/funds | - |

| Cross-Account Analysis | Analyzes all connected accounts (401(k), IRA, taxable, etc.) | Limited account integration |

| Asset Location Optimization | Advises on Roth, Traditional, and taxable placement | - |

| Retirement Income Projection | Basic retirement planning based on connected accounts | Comprehensive income modeling tools |

| Withdrawal Strategy Planning | General guidance via AI chat | Detailed decumulation plans |

| Social Security Optimization | - | Specialized claiming strategy tools |

| Pension Management | - | Integrated pension income planning |

| AI Chat Assistant | 24/7 access using real account data | - |

| Rebalancing Guidance | Tax-efficient suggestions | - |

Pricing: Mezzi vs. Retirable

Mezzi and Retirable take very different approaches to pricing. Mezzi offers a tiered subscription model with three options: Core at $299/year, Plus at $499/year, and White Glove at $1,499/year. Retirable, on the other hand, charges a percentage-based fee of 1% of assets under management (AUM), capped at $5,000 annually. For example, a client with $1 million in assets would pay $5,000 with Retirable, compared to the $10,000–$20,000 they might pay at a traditional firm charging 1–2%.

Mezzi's flat subscription fee keeps costs consistent regardless of portfolio size. Whether your portfolio is $500,000 or $5 million, you pay the same annual fee depending on your chosen tier. Retirable’s percentage-based fee, however, scales with your assets until it hits the $5,000 cap. For a $1 million portfolio, this results in an effective fee rate of 0.5%.

Mezzi markets itself as a way to eliminate advisor fees entirely by avoiding percentage-based pricing. Additionally, it highlights potential tax optimization benefits, stating these strategies could add 1–2% to annual returns. On a $1 million portfolio, this could mean $10,000–$20,000 more annually and over $1 million in extra wealth over 30 years. Retirable, in contrast, includes a dedicated human fiduciary advisor in its fee structure, while Mezzi relies on AI-driven fiduciary insights that users implement on their own.

Pricing Breakdown Table

| Feature | Mezzi | Retirable |

| Pricing Model | Tiered subscription (Core, Plus, White Glove) | 1% of AUM, capped at $5,000/year |

| Core/Entry Tier | $299/year | - |

| Mid Tier | $499/year (Plus) | - |

| Premium Tier | $1,499/year (White Glove) | - |

| Cost on $500K Portfolio | $299–$1,499/year (depending on tier) | $5,000/year |

| Cost on $1M Portfolio | $299–$1,499/year (depending on tier) | $5,000/year (0.5% effective rate) |

| Human Advisor Included | No (AI-driven advice only) | Yes (dedicated fiduciary advisor) |

| Fee Increases with Portfolio Growth | No | Yes, until the $5,000 cap is reached |

| Account Transfers Required | No (read-only access to existing accounts) | Typically yes (consolidation into Altruist IRA) |

Who Should Use Each Platform

Here's a breakdown of who benefits most from these platforms based on their unique features and target users:

Mezzi for Self-Directed Wealth Builders

Mezzi caters to self-directed investors aged 30–55 with assets ranging from $100,000 to $1 million. These users typically have a solid grasp of investment basics but want to leverage AI for smarter strategies. It's particularly appealing to individuals like tech employees, doctors, or financial professionals who value hands-on control while benefiting from tools like tax-loss harvesting and wash sale tracking.

If you're someone who prefers making your own investment decisions and prioritizes efficiency over personalized guidance, Mezzi's flat subscription pricing is a practical choice. For example, a 42-year-old software engineer with $250,000 in assets used Mezzi to optimize an early retirement plan. By incorporating AI-driven Roth conversions and ESG filters, they achieved a hypothetical 12% annualized return compared to 8% with manual methods. Plus, Mezzi's read-only access ensures your investments stay where they are, while still providing fiduciary-level advice at a fraction of traditional costs.

That said, if you're looking for a more structured approach to retirement income, another platform may be better suited.

Retirable for Retirement-Focused Planners

Retirable is tailored for individuals 50 and older who are nearing or already in retirement, typically with $500,000 or more in retirement savings. These users prioritize income stability and need help with Social Security strategies, Medicare planning, and longevity risk management rather than aggressive growth.

The platform shines with specialized tools like RMD calculators that comply with SECURE 2.0 Act regulations and annuity comparison features. For instance, a 62-year-old couple used Retirable to address a $40,000 income gap by delaying their Social Security claims. This approach resulted in an 8% increase in benefits and a 95% success rate in Monte Carlo simulations.

If your focus is on creating a steady and reliable retirement plan, Retirable’s features are designed to meet those specific needs.

Conclusion: Which Platform Is Right for You

Deciding between Mezzi and Retirable depends on your financial goals and how much involvement you want in managing your investments.

For self-directed investors with moderate portfolios, Mezzi offers AI-driven fiduciary guidance without charging a 1% AUM fee. It allows you to keep your accounts where they are, provides tax optimization insights, and lets you retain complete control over your investment choices. Mezzi strikes a balance between independent investing and professional advice, giving you the tools to manage your wealth while staying in charge.

Retirable, on the other hand, is tailored for those transitioning from building wealth to generating retirement income. If you need help with Social Security, RMDs, or Medicare planning, Retirable focuses on these areas. The platform is designed to create steady income streams and address longevity risks - key concerns as you approach or enter retirement.

In short, choose Mezzi if you value hands-on control, tax efficiency, and a clear view of your entire portfolio. Opt for Retirable if your priority is turning your savings into reliable retirement income with specialized guidance for this critical phase. Matching your financial needs to either Mezzi's AI-powered support or Retirable's retirement-focused tools can help you make smarter decisions for your future.

FAQs

Can Mezzi help me reduce taxes without moving my accounts?

Mezzi offers a way to lower your tax obligations without the hassle of relocating your accounts. By taking a comprehensive look at your portfolio, Mezzi employs AI-powered tax strategies like tax-loss harvesting and asset location recommendations. These methods work to reduce your taxes while ensuring your accounts remain exactly where they are.

How does Mezzi’s AI know what trades to suggest?

Mezzi’s AI takes a deep dive into your portfolio and keeps a close eye on market trends to deliver personalized trade suggestions. By leveraging advanced algorithms, it considers your financial goals, risk tolerance, and even tax strategies to provide investment insights that are specifically designed for you.

Which Mezzi plan should I choose for my portfolio size?

Selecting the best Mezzi plan depends on the size of your portfolio and your specific needs. The free plan is a great starting point, offering AI-driven, personalized advice - perfect for smaller or moderately sized portfolios.

If you manage a larger portfolio or want access to more advanced tools, the premium plan might be a better fit. At $299 per year, it includes features like tax optimization and in-depth insights to help you make more informed decisions.

A smart approach? Begin with the free plan. As your portfolio grows or your needs become more complex, you can always upgrade to the premium option.

Disclosures:

- This content is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.

- Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.

- The use of artificial intelligence and algorithmic tools does not guarantee investment results. These tools are subject to limitations, errors, and market conditions that may affect performance.

- Savings and performance examples are hypothetical and for illustrative purposes only. Actual results will vary based on individual circumstances, portfolio composition, market conditions, and fees.

- Registration does not imply a certain level of skill or that the SEC has approved the company or its services.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.