Mutual funds and ETFs make diversification simple, but their tax treatment can significantly impact your returns. ETFs generally offer better tax efficiency thanks to their in-kind redemption process, which minimizes capital gains distributions. Mutual funds, especially actively managed ones, often trigger higher tax liabilities due to frequent trading and cash redemptions.

Key points to know:

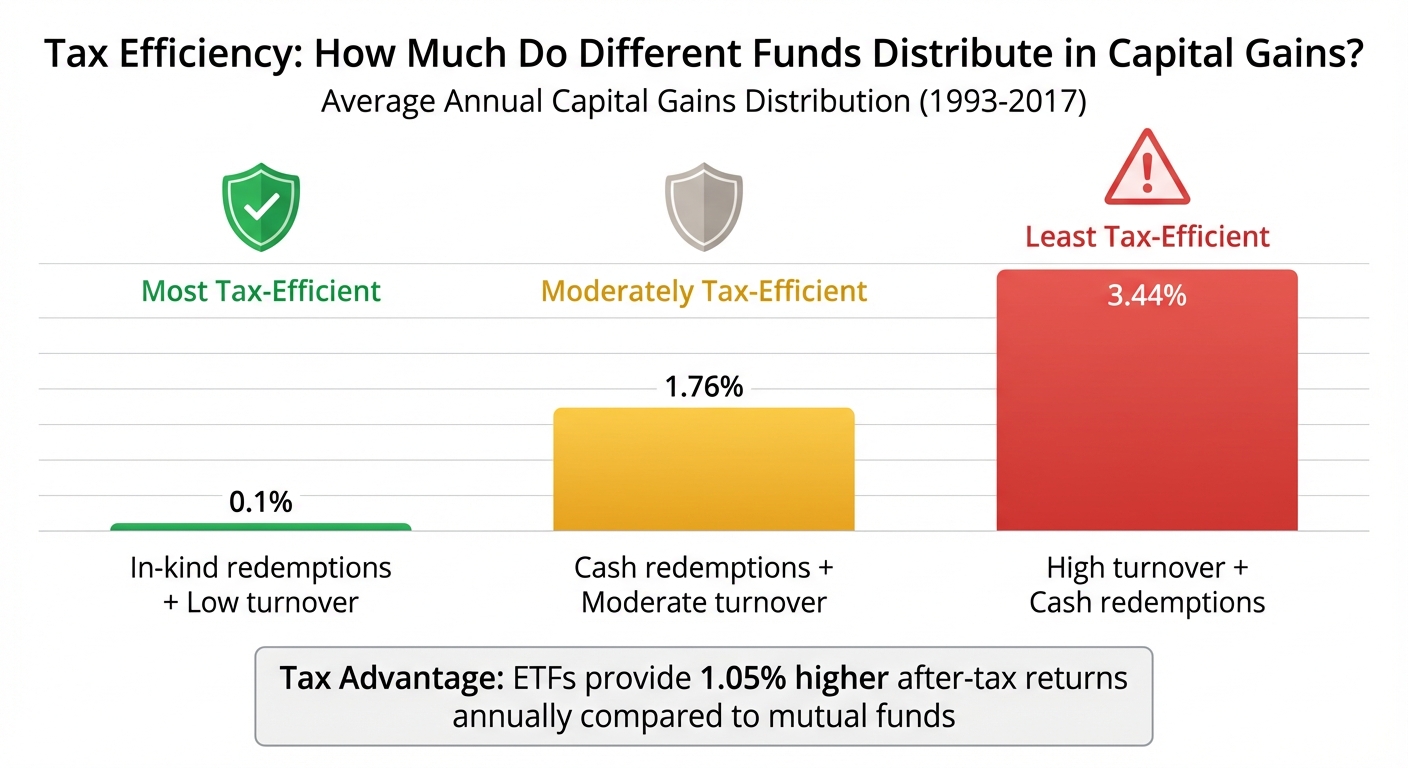

- ETFs distribute fewer capital gains (0.10% annually vs. 3.44% for active mutual funds).

- Reinvested dividends increase your cost basis but are still taxable.

- Asset location matters: Place tax-efficient ETFs in taxable accounts and tax-heavy funds like bonds in IRAs or 401(k)s.

- Tax-loss harvesting and capital gains deferral offset gains and reduces your tax bill.

Small tax advantages can add up over time, boosting your long-term savings. Advanced tools like Mezzi can streamline tax management, helping you track gains, avoid wash sales, and optimize your portfolio for taxes.

How Mutual Funds and ETFs Are Taxed

Taxation on Distributions and Gains

If you hold mutual funds or ETFs in a taxable brokerage account, you'll receive Form 1099-DIV every year. This form details your dividends, interest, and capital gains distributions. If you sell any shares, you'll also get Form 1099-B to report those transactions. Here's how the taxes break down:

- Ordinary dividends and interest: These are taxed at your regular income tax rate, which can go as high as 37%.

- Qualified dividends: These benefit from lower tax rates of 0%, 15%, or 20%, provided you meet the holding period requirements.

For capital gains distributions, the tax treatment depends on how long the fund held the securities. Gains from securities held for over a year are treated as long-term gains, while those held for a year or less are considered short-term and taxed at your ordinary income rate. This is true regardless of how long you've personally held the fund. Understanding these basics is key to managing the tax implications of your investments, especially when reinvesting dividends.

Reinvested Dividends and Cost Basis

Reinvesting dividends doesn't save you from paying taxes. The IRS treats reinvested dividends as though you received the cash and immediately used it to buy more shares. This increases your cost basis, which helps avoid double taxation down the line. For example, if you own 500 shares worth $10,000 and earn a $300 reinvested dividend, your cost basis rises to $10,300.

Tools like Mezzi can simplify this process by tracking detailed, lot-level cost basis records across your accounts, helping you avoid costly mistakes. While reinvested dividends adjust your cost basis without triggering immediate taxes, actively managing your portfolio for diversification could still lead to unexpected tax bills.

Tax Impact of Diversifying Through Funds

Diversifying through mutual funds or ETFs can sometimes lead to surprise tax obligations. For example, when a mutual fund manager sells securities - whether to rebalance the portfolio, meet investor redemptions, or adjust to an index change - the resulting gains are passed on to shareholders as taxable distributions, usually at the end of the year. You might owe taxes on these gains even if you haven't sold any shares yourself.

Actively managed mutual funds tend to have higher portfolio turnover, which often generates more short-term gains subject to higher tax rates. On the other hand, index funds and many ETFs generally have lower turnover, which can mean fewer taxable events.

ETFs, in particular, are designed to be more tax-efficient. Thanks to their in-kind creation and redemption process, ETFs can exchange baskets of securities without triggering taxable events. Mutual funds, however, may need to sell securities to meet redemptions, which can result in taxable gains for the shareholders who remain invested. This structural difference gives ETFs a tax advantage in many cases.

Mutual Funds vs. ETFs: What Are the Tax Implications in a Taxable Account?

Tax Efficiency: Mutual Funds vs ETFs

Tax Efficiency Comparison: ETFs vs Mutual Funds Annual Capital Gains Distribution

Why ETFs Are Often More Tax Efficient

The tax edge that ETFs hold lies in the way their shares are created and redeemed. With mutual funds, when investors want to cash out, the fund usually pays them in cash. If there’s a wave of redemptions, the fund manager might have to sell some of the underlying securities to generate that cash. This can lead to capital gains, which are then distributed to all remaining shareholders - even those who didn’t sell their shares .

ETFs operate differently. They rely on Authorized Participants - large financial institutions that handle ETF shares in what’s called "creation units." Instead of cash transactions, these participants exchange baskets of securities directly with the ETF. When redeeming shares, ETFs can transfer their most appreciated holdings (those with the lowest cost basis) in-kind. This means no taxable sale occurs within the fund .

This unique structure provides a clear tax advantage. Over time, this efficiency can significantly boost returns for ETF investors compared to those holding mutual funds .

Tax Efficiency of Index Funds vs Active Funds

Another factor that impacts tax efficiency is portfolio turnover and asset placement. Index mutual funds and index ETFs generally have very low turnover because they only trade when there’s a change in the underlying index. This results in fewer transactions and, consequently, fewer realized capital gains . In contrast, active mutual funds often trade more frequently as managers aim to outperform the market, which can lead to higher and more frequent capital gains distributions .

Active ETFs, while subject to some turnover due to active management, still benefit from the ETF structure and its in-kind redemption process. This means even with increased trading, active ETFs tend to distribute fewer capital gains than their mutual fund counterparts. For investors in taxable accounts, this translates to less tax drag on returns. Studies suggest that this tax efficiency has led to an average boost in long-term after-tax returns of about 1.05% annually for ETFs compared to mutual funds.

| Fund Type | Typical Annual Capital Gains Distribution (1993-2017) | Primary Tax Driver |

|---|---|---|

| Index ETFs | 0.1% | In-kind redemptions, low turnover |

| Index Mutual Funds | 1.76% | Cash redemptions, moderate turnover |

| Active Mutual Funds | 3.44% | High turnover with cash redemptions |

Beyond management style, the type of assets a fund holds also plays a big role in its tax profile.

Tax Considerations for Bond vs Stock Funds

The assets within a fund can have a major impact on its tax efficiency. Bond funds, for instance, generate interest income, which is taxed at ordinary income tax rates - potentially as high as 37% at the federal level. While bond funds might also distribute capital gains when bonds are sold at a profit, the majority of their distributions are taxed as ordinary income.

Stock funds, on the other hand, typically generate qualified dividends and capital gains. If investors meet the required holding periods, these distributions are taxed at lower rates - 0%, 15%, or 20% - making stock funds a better fit for taxable accounts .

For high-income investors, municipal bond funds can offer additional perks since their interest is usually exempt from federal income tax. In some cases, they’re also exempt from state taxes if the bonds are issued in-state. While municipal bond funds might show lower nominal yields, their tax-equivalent yield can be higher for investors in higher tax brackets. As a result, many financial advisors recommend holding taxable bond funds in tax-advantaged accounts like IRAs, while favoring tax-efficient equity index ETFs in taxable accounts to reduce the overall tax burden.

Tax Implications of Rebalancing and Diversification Trades

Capital Gains from Rebalancing

Rebalancing a taxable portfolio can lead to realized capital gains, which are subject to taxes. The tax rate depends on how long you've held the asset. Gains from assets held for over a year qualify as long-term capital gains, which are taxed at a lower rate compared to short-term gains.

For example, imagine you purchased a stock ETF for $10,000, and its value grows to $15,000 after 18 months. If you sell it to rebalance, the $5,000 gain would be taxed at the long-term capital gains rate of 15%, resulting in a $750 tax bill.

However, rebalancing within tax-advantaged accounts - like 401(k)s, traditional IRAs, Roth IRAs, or HSAs - doesn't trigger immediate capital gains taxes. In taxable accounts, timing plays a crucial role. Directing new contributions or dividends to underweight funds or waiting until assets qualify for long-term capital gains treatment can help lower the tax burden of maintaining diversification.

If rebalancing does lead to gains, Tax-loss harvesting software is a useful tool to automate this strategy and offset the impact.

Tax-Loss Harvesting and Offsetting Gains

Tax-loss harvesting can help reduce the tax burden of rebalancing by offsetting gains with realized losses. The process is straightforward: sell underperforming mutual funds or ETFs at a loss to generate capital losses. These losses can offset capital gains dollar for dollar. If your losses exceed your gains, you can deduct up to $3,000 of the excess against ordinary income, with any remaining losses carried forward indefinitely.

Here’s an example: Suppose you sell a domestic stock fund with a $10,000 gain as part of rebalancing, while holding an international ETF with an $8,000 loss. By realizing the loss, you offset most of the gain, leaving only $2,000 taxable. At a 15% long-term capital gains rate, this strategy saves you $1,200 in taxes. Over time, reinvesting these tax savings can significantly boost your portfolio’s growth - what saves $10,221 in taxes today could grow into $76,123 over 30 years.

That said, it’s important to watch out for the wash sale rule. If you sell a fund at a loss and repurchase the same or a "substantially identical" fund within 30 days before or after the sale, the IRS disallows the loss. Instead, the disallowed loss is added to the cost basis of the new shares. Tools like Mezzi can help investors manage these complexities by providing real-time alerts and ensuring compliance with the wash sale rule across multiple accounts.

Avoiding redundancy in fund selection is another way to minimize unnecessary tax liabilities.

Avoiding Redundant Diversification

Owning too many overlapping funds can create unintended tax issues. When multiple funds in your portfolio track similar markets - like two large-cap growth ETFs with 80% overlap - you may face multiple capital gains distributions from each fund’s internal rebalancing. This can inflate your tax bill without adding any meaningful diversification.

For example, splitting a $50,000 allocation equally between two ETFs with 80% overlap might result in $5,000 in annual capital gains, compared to $2,500 from a single fund. If the overlap (correlation >0.95) is high, you’re essentially doubling the taxes on the same exposure. Simplifying your portfolio by using a smaller selection of broad, low-cost index funds - covering U.S. stocks, international stocks, and bonds - can reduce unnecessary taxes while maintaining effective diversification.

Advanced tools can help identify and eliminate these overlaps. Mezzi’s X-Ray feature, for instance, analyzes your portfolio to pinpoint exposure to specific stocks held across multiple funds. This makes it easier to streamline your investments and avoid redundant capital gains distributions. By consolidating overlapping positions and focusing on a core set of complementary funds, you can let more of your returns stay in your portfolio instead of going to taxes.

Account Location Strategies for Tax Optimization

Taxable vs. Tax-Advantaged Accounts

Minimizing the tax bite on your investments starts with understanding asset location. The type of account where you hold your mutual funds and ETFs plays a big role in your after-tax returns. Asset location - placing specific investments in the most tax-efficient accounts - can help you keep more of your earnings without changing your overall risk profile.

The concept is simple: place tax-efficient assets in taxable accounts and tax-inefficient ones in tax-advantaged accounts. For example, U.S. stock index ETFs and low-turnover equity index funds are ideal for taxable brokerage accounts. These investments produce minimal capital gains distributions and benefit from lower long-term capital gains rates and qualified dividend treatment.

In contrast, tax-inefficient investments, like taxable bond funds, high-yield bond funds, REIT funds, and actively managed stock funds with high turnover, are better suited for retirement accounts. Why? These funds generate income taxed at ordinary rates (up to 37% federally). When held in a traditional 401(k) or IRA, those distributions grow tax-deferred until you withdraw them. In a Roth IRA or Roth 401(k), they can grow entirely tax-free, provided you follow the rules.

Roth accounts, in particular, are a great place for your highest-return, most tax-inefficient investments. Since Roth withdrawals are tax-free, you can maximize growth potential while avoiding future taxes. Meanwhile, traditional tax-deferred accounts are better for bonds and other income-generating funds, delaying taxes until retirement. Beyond these basics, international holdings bring additional tax layers to consider.

Foreign Tax Withholding on International Funds

Investing in international stock funds comes with a unique tax wrinkle: foreign withholding taxes. Many foreign governments take a cut of dividends at the source before they even reach your U.S. mutual fund or ETF. This reduces the dividends you ultimately receive.

If you hold these funds in a taxable account, there’s good news - you might be able to recover part or all of those taxes. Your fund will report the foreign tax paid on Form 1099-DIV, and you may qualify for a foreign tax credit or deduction on your U.S. tax return, subject to IRS rules. This can make taxable accounts a smart choice for international equity exposure.

However, in tax-advantaged accounts like IRAs or 401(k)s, you lose that opportunity. Since the account itself is treated as the taxpayer, you can’t claim the foreign tax credit. This means the withheld tax becomes a permanent loss, making taxable accounts more appealing for international funds when balancing overall portfolio goals.

Transitioning Between Mutual Funds and ETFs

Switching from a mutual fund to an ETF in a taxable account can trigger a taxable event. The difference between your cost basis and the sale price - any unrealized gain - becomes a recognized capital gain, subject to tax . If you’ve held the mutual fund for years and it has gained significantly, the tax bill could be substantial.

Before making the switch, evaluate factors like the size of the unrealized gains, how long you’ve held the fund, your current and future tax brackets, and whether you can offset gains with losses through tax-loss harvesting. Using specific lot identification can help you sell shares with smaller gains or losses first, reducing the tax hit. Additionally, spreading sales across multiple calendar years can help you stay in lower capital gains tax brackets and avoid the 3.8% net investment income tax.

Some fund companies offer tax-free conversions, allowing mutual funds to convert into ETF share classes or merge into ETFs through reorganizations. These conversions don’t trigger capital gains, letting you improve tax efficiency without an immediate tax bill. If this option isn’t available, you might hold onto highly appreciated mutual funds while directing new contributions into tax-efficient ETFs. Over time, this gradual approach can refine your portfolio’s tax profile .

Using Advanced Tools for Tax Optimization

Expanding on strategies like rebalancing and asset location to minimize tax impacts, advanced tools can take your tax planning to the next level.

Unified Financial Insights

Managing taxes can get tricky when your investments are scattered across multiple accounts - brokerage accounts, IRAs, 401(k)s, HSAs - you name it. Mezzi simplifies this by consolidating all your accounts into one clear view. This unified snapshot doesn’t just show what you own; it breaks down how each position affects your tax situation. You can see realized versus unrealized gains, distinguish between short-term and long-term gains, review recent distributions, and pinpoint tax-inefficient assets sitting in the wrong account types.

For example, if you’re holding a high-yield bond fund in a taxable account and an equity ETF in an IRA, Mezzi will flag this mismatch. It might suggest moving the bond fund into a tax-advantaged account while keeping the equity ETF in the taxable account to maximize tax efficiency. This kind of repositioning can make a big difference in reducing your tax liability.

Avoiding Wash Sales

Automated tax-loss harvesting is a popular strategy, but it loses its edge if you accidentally trigger a wash sale. A wash sale happens when you sell a security at a loss and then repurchase the same - or a substantially identical - security within 30 days. The IRS disallows the loss, wiping out the tax advantage you were aiming for. This risk multiplies when you’re juggling multiple accounts or trading between mutual funds and ETFs that track the same index.

Mezzi’s AI keeps an eye on all your linked accounts to prevent this by helping you avoid wash sales with AI insights. It monitors overlapping tickers, funds tied to similar benchmarks, and even dividend reinvestment settings. If it spots a potential wash sale risk - like a related security in another account - it’ll alert you. The platform might also recommend temporarily pausing dividend reinvestments during the 30-day window or suggest alternative replacement funds that provide similar exposure without breaking the IRS rules. This kind of proactive monitoring ensures your tax-loss harvesting efforts remain intact.

Real-Time Tax Optimization Recommendations

Static, one-time reviews often miss opportunities that arise from shifting market conditions or changes in your tax bracket. Real-time recommendations, however, can help you act when it matters most.

Mezzi’s AI provides timely, actionable insights as the market evolves. For instance, if it spots a taxable, actively managed mutual fund with frequent capital gain distributions, it might recommend switching to a tax-efficient ETF offering similar exposure. During market downturns, it can identify funds with large unrealized losses and suggest tax-loss harvesting while offering replacement options to maintain your portfolio’s diversification. The tool also tracks unrealized gains, advising on the best timing for sales - whether it’s waiting for long-term capital gain treatment or spreading significant sales over multiple years to manage taxable income.

Conclusion

Investing in mutual funds and ETFs can be a reliable way to grow wealth over time, but taxes can quietly chip away at your returns. Thanks to their lower capital gains distributions and in-kind redemption process, ETFs often deliver better after-tax returns. Even small tax savings can snowball into significant gains over the years - saving $10,221 on capital gains taxes today could grow into $76,123 in 30 years. Similarly, cutting investment costs by just 1% might add an impressive $186,877 to your retirement portfolio. These numbers highlight the real financial benefits of tax-efficient investing.

To truly maximize your portfolio's potential, incorporating tax-efficient strategies is key. For example, placing tax-inefficient bond funds in IRAs, holding ETFs in taxable accounts, and using ETF tax-loss harvesting to offset gains can all reduce your tax burden. However, juggling these strategies across various accounts - like brokerage accounts, 401(k)s, and IRAs - can quickly become overwhelming. That’s where advanced tools come into play.

Mezzi simplifies the process by consolidating all your accounts into a single view, alerting you to potential wash sale risks, and providing real-time AI-driven recommendations to optimize your tax approach. Whether it’s suggesting a strategic ETF swap to minimize distributions or pinpointing the best time to harvest losses, Mezzi ensures you can act on tax-saving opportunities when they matter most. For self-directed investors managing diverse portfolios, these features could translate into over $1 million saved in fees and taxes over 30 years.

FAQs

Why are ETFs generally more tax-efficient than mutual funds?

ETFs tend to be more tax-friendly compared to mutual funds, thanks to a mechanism known as in-kind redemption. This process enables ETFs to transfer actual securities to authorized participants when shares are sold, sidestepping the need to sell assets within the fund itself. By avoiding these sales, ETFs help investors steer clear of triggering taxable capital gains.

Mutual funds, on the other hand, often sell securities within the fund to handle redemptions. This can lead to capital gains distributions that affect all investors, even those who haven’t sold their shares. This fundamental difference in structure allows ETFs to reduce taxable events, making them an appealing option for those looking to manage their tax exposure.

How can I reduce taxes when investing in mutual funds and ETFs?

To reduce taxes while diversifying with mutual funds and ETFs, here are some practical strategies:

- Tax-loss harvesting: Sell investments that have decreased in value to offset any taxable gains. This can help lower your overall tax liability.

- Opt for tax-efficient funds: Consider funds like index funds or ETFs that are structured to limit taxable distributions.

- Hold investments for the long term: By holding onto your investments, you can qualify for long-term capital gains rates, which are typically lower than short-term rates.

- Steer clear of wash sales: Be mindful of IRS rules that disallow claiming a loss if you repurchase a "substantially identical" investment within 30 days of the sale.

Implementing these strategies can help you manage your tax obligations and retain more of your investment earnings.

How can Mezzi help manage taxes across multiple investment accounts?

Mezzi makes tax management easier by using advanced AI to deliver real-time insights specifically designed for your investments. It helps you steer clear of costly errors, such as wash sales, and fine-tune tax strategies to lower capital gains. Plus, it simplifies your financial planning by bringing all your accounts together into one clear, unified view.

With Mezzi, you can manage your taxes more effectively, make informed financial choices, and save both time and money while cutting down on avoidable tax obligations.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.