Most rental losses may not offset W-2 income. For many landlords, those losses stay passive and may only offset passive income unless a narrow IRS exception applies.

Here’s the short version:

- Rental losses usually stay passive under IRC §469.

- The $25,000 rental loss allowance may apply only in limited cases and may phase out once MAGI gets too high.

- Real Estate Professional Status (REPS) may let rental losses offset W-2 wages, but only if the IRS tests are met every year.

-

There are 2 REPS tests:

- 750+ hours in real property trades or businesses

- More than 50% of all personal service work in those real estate activities

- Material participation still matters. REPS alone may not be enough.

- Spouses may not combine hours for REPS, but they may combine hours for material participation on a joint return.

- A grouping election may let multiple rentals count as one activity.

- Good time logs matter. Weak or rebuilt records may lead to IRS pushback.

- Even with REPS, basis, at-risk, and excess business loss rules may still limit deductions.

A simple way to think about it: REPS may remove the passive-loss roadblock, but not every tax limit that sits behind it.

The Tax Court Just Killed Real Estate Professional Status (3 Cases You Need To See)

Quick Comparison

| Topic | General Rule | What May Change It |

|---|---|---|

| Rental losses vs. W-2 income | Usually not allowed | REPS + material participation may allow it |

| $25,000 allowance | May help some landlords | May phase out by $150,000 MAGI |

| 750-hour test | Must be met yearly | Only qualifying real estate work may count |

| 50% test | Must be met yearly | Full-time W-2 work may make this harder |

| Married filing jointly | REPS tested per spouse | Material participation hours may be combined |

| Multiple rentals | Treated separately by default | Grouping election may combine them |

| Audit support | IRS may look for proof | Contemporaneous logs may carry more weight |

If I were putting this in one sentence, I’d say this: REPS may let some high-income landlords use rental losses now instead of later, but only if their hours, participation, elections, and records all line up.

The IRS Tests for Real Estate Professional Status

How to Qualify for Real Estate Professional Status (REPS) & Deduct Rental Losses Against W-2

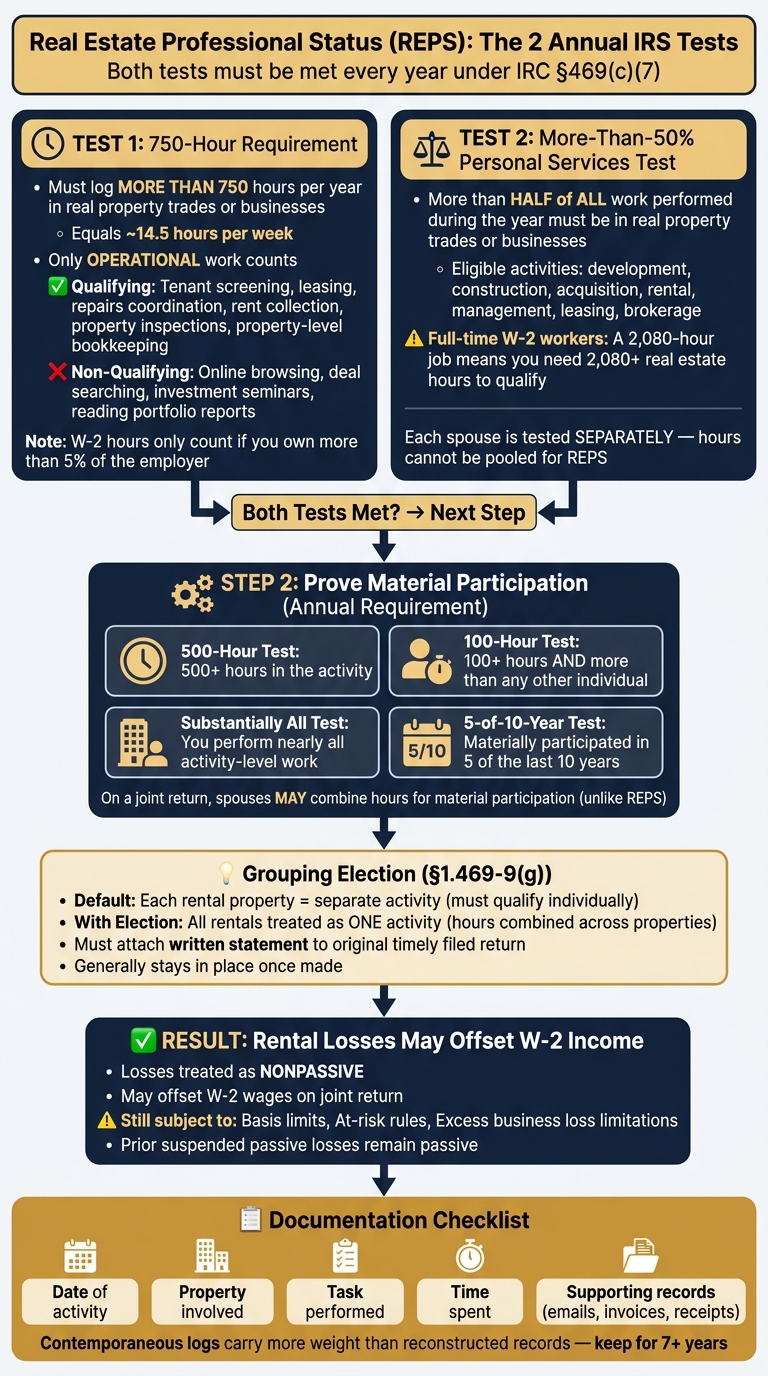

REPS under IRC §469(c)(7) has two annual tests: 750 hours and more than 50% of your personal services in real estate. Both apply every year. These tests may determine whether rental losses stay passive or may offset W-2 wages.

The More-Than-50% Personal Services Test

More than half of all the work you perform in any trade or business during the year must be in real property trades or businesses in which you materially participate. Those trades or businesses include development, redevelopment, construction, reconstruction, acquisition, conversion, rental, operation, management, leasing, and brokerage.

A full-time W-2 job may make this test hard to meet. High-income salaried taxpayers may log enough hours at work alone that real estate falls below the 50% mark, even if they spend a lot of time on landlord duties.

The 750-Hour Requirement

The second test requires more than 750 hours of services during the year in real property trades or businesses in which you materially participate. That works out to about 14.5 hours per week.

The IRS looks at operational work, not investor activity. Work like tenant screening, coordinating repairs, managing vendors, collecting rent, handling lease renewals, and property walk-throughs may count. By contrast, online browsing, deal searching, reading portfolio-level reports, and attending investment seminars generally do not.

| Qualifying (Operational) Activities | Non-Qualifying (Investor) Activities |

|---|---|

| Tenant screening, leasing, and renewals | Online browsing and deal searching |

| Coordinating repairs and managing vendors | Reading portfolio-level reports |

| Property-level bookkeeping and administration | Attending investment seminars or general education |

| Rent collection and managing property finances | Travel time, which the IRS often discounts unless documentation is strong |

| Property inspections, walk-throughs, and turnovers |

W-2 hours in a real estate business do not count unless you own more than 5% of that employer.

How Each Spouse Is Tested Separately on a Joint Return

On a married filing jointly return, each spouse must meet both REPS tests separately. Hours can't be pooled. That said, one spouse who qualifies may still open the door to the deduction for the joint return.

That may make REPS more workable in higher-income households where one spouse has a full-time job and the other has enough schedule flexibility to meet both tests. In that setup, rental losses may offset the higher-earning spouse's W-2 income.

Once both REPS tests are met, the next question is whether the rentals themselves meet the material participation rules.

Material Participation and Grouping: The Rules That Determine Whether Losses Are Usable

REPS may remove rental activity’s automatic passive status. But that alone may not make the losses usable. You also may need to show material participation.

From there, the next issue is scope: does your rental work count for one property at a time, or for a grouped set of properties?

The IRS lays out seven material participation tests under Temp. Reg. §1.469-5T. And this test happens every year. So if you fail in one tax year, that year’s losses may remain passive and suspended, even if you still qualify as a real estate professional.

The Material Participation Tests That Apply Most Often

| Test | What It Requires | Common mistakes |

|---|---|---|

| 500-Hour Test | More than 500 hours of participation in the activity during the year | Counting "investor" hours like reading financial statements, general market research, or education |

| 100-Hour / More-Than-Anyone-Else Test | More than 100 hours of participation, and more than any other individual | Failing to account for the hours worked by a third-party property management firm |

| Substantially All Test | You perform nearly all activity-level work, including work done by employees and contractors | Claiming this when a full-time property management company or contractors handle most of the work |

| 5-of-10-Year Test | You materially participated in the activity for 5 of the last 10 years | Assuming current REPS qualification automatically satisfies it |

One detail trips people up a lot: on a joint return, spouses may combine hours for material participation. But REPS qualification works differently. Each spouse still may need to meet the REPS tests on their own.

When to Group Multiple Rental Properties Into One Activity

If you own several rentals, the grouping election may change the whole setup.

By default, the IRS treats each rental property as a separate activity. That means you generally may need to meet a material participation test for each property on its own. The main exception is the grouping election under Treas. Reg. §1.469-9(g), which may let you treat all rental real estate interests as one activity.

That may matter quite a bit for households with more than one property. Grouping may allow one spouse’s hours to count toward material participation across a larger rental portfolio.

To make the election, attach a written statement to the original timely filed return. Once made, it generally stays in place unless the facts materially change.

In plain English: grouping may make qualification easier because hours across properties may be combined. But it also tends to stick, and it may make suspended-loss treatment harder on a partial sale.

With material participation in place, the next section looks at how those losses may offset W-2 income in practice.

How REPS Can Offset W-2 Income in Practice

If both REPS tests are met, and the rental activity also meets material participation, rental losses may be treated as nonpassive and may offset W-2 wages. That’s the basic idea.

The examples below show how this may play out on a joint return, and what may happen when a taxpayer does not qualify.

On a joint return, one spouse may qualify for REPS based on that spouse’s own hours alone. Those REPS hours are not combined between spouses. But spouses may combine hours for material participation.

Example: A Married Couple Where One Spouse Qualifies

Consider a married couple filing jointly. One spouse earns $480,000 in W-2 income. The other spends 1,100 hours managing four rental properties and 500 hours in consulting work.

In this case, the real estate spouse may clear both REPS tests on their own: the 750-hour test and the more-than-50% test. If the rental activity also meets material participation, the couple may use the rental losses against the W-2 income on the joint return.

Assumes sufficient basis, at-risk amount, and no excess business loss limitation.

Example: A Full-Time W-2 Worker Who Does Not Qualify

Now take a full-time W-2 employee who works 2,080 hours in a year and spends 400 hours on rental activity.

Those 400 hours may still count. But they do not meet the more-than-50% test. For someone with a 2,080-hour W-2 job, qualifying for that test may require more than 2,080 hours in eligible real estate work.

If that test is not met, the rental losses stay passive and suspended. In that case, they may not reduce current W-2 wages. Instead, they may generally be used only against passive income or when the property is sold.

Other Limits That Still Apply After REPS

REPS may change whether current-year rental losses are deductible against nonpassive income, but it does not remove other limits.

Basis limits, at-risk rules, and the excess business loss limit may still apply. Prior suspended passive losses remain passive. Put simply, REPS may change current deductibility, not the character of earlier passive losses.

Documentation, Filing Mistakes, and Key Takeaways

What Your Time Logs and Activity Records Must Show

Once you clear REPS qualification, the next issue may be proof. In an audit, the IRS may first ask for a contemporaneous time log. Without one, REPS may be much harder to defend.

Each entry should show:

- the date

- the property involved

- the task you performed

- the time spent

- the result

Vague notes like "worked on rentals" may not carry much weight. More specific entries, such as "screened three tenants for Property A" or "supervised HVAC installation at Property B", may be stronger. Your log may also be backed up with other records, including tenant emails and texts, contractor invoices, mileage logs, and time-stamped repair receipts.

It also may make sense to track non-real-estate work hours, such as W-2 timesheets, since the more-than-50% test requires real estate hours to exceed all other work hours combined. Hours by themselves may not be enough. The records may need to support both qualification and material participation. Keep those records for at least seven years.

The Most Common Reasons the IRS Denies REPS Deductions

Large rental losses offset against high W-2 income may draw IRS attention, especially for first-time REPS claims. A lot of denials appear tied to a handful of filing and recordkeeping mistakes.

Counting investor-type hours. Time spent reviewing financial statements, browsing Zillow, attending real estate seminars, or analyzing deals you never bought does not count toward the 750-hour threshold or material participation. The IRS looks for operating work instead, such as leasing, maintenance coordination, tenant management, and similar hands-on tasks.

Missing the grouping election. If you do not attach the §1.469-9(g) election in the first year, you may have to test each property on its own.

Reconstructing records after the fact. In Almquist v. Commissioner (T.C. Memo 2016-81), the taxpayer was denied REPS treatment after providing an incomplete logbook assembled only after the IRS audit began.

Assuming spouses can pool REPS hours. Each spouse must meet REPS on a separate basis. Pooled hours count only for material participation.

Key Takeaways and Where Mezzi Fits

Use this checklist before filing:

| Checkpoint | What to Confirm |

|---|---|

| 750-hour test | You logged 750+ hours in qualifying real property trades or businesses |

| More-than-50% test | Real estate hours exceed all other work hours combined |

| Material participation | You meet at least one of the IRS tests for the rental activity itself |

| Grouping election | A §1.469-9(g) statement is attached to your return if you want to treat multiple rentals as one activity |

| Contemporaneous logs | Records were maintained throughout the year, not reconstructed later |

| Remaining limits | Basis, at-risk, and excess business loss rules still need separate review |

If you want a clearer view of how this may fit into your overall plan, Mezzi may help. Mezzi may show how rental losses fit into your broader financial picture through read-only account access and guidance you control.

FAQs

Can one spouse qualify for REPS on a joint return?

Yes. On a joint return, if one spouse qualifies for REPS, the couple may deduct qualifying rental losses against their total active income.

There’s one catch: spouses may not combine hours to qualify for REPS itself. One spouse has to meet both tests on their own:

- The 750-hour test

- The more-than-50% personal services test

That said, a spouse’s hours may still be combined for the separate material participation tests for each rental activity.

What rental tasks count toward the 750 hours?

Time counts only if you provide personal services in a real property trade or business where you materially participate. That may include development, construction, acquisition, rental, operation, management, leasing, or brokerage.

In plain English, the IRS may look for hands-on work. Tasks that may count include:

- Screening tenants

- Negotiating leases

- Approving contractors

- Managing day-to-day operations

- Supervising employees or contractors

By contrast, passive investor activities - like reviewing financial statements - generally may not count.

Keep detailed, contemporaneous logs. If your time is ever questioned, those records may carry a lot of weight.

Can suspended passive losses be used after qualifying for REPS?

Yes. Qualifying for Real Estate Professional Status (REPS) may allow rental activities to be treated as non-passive. If that applies, rental losses - including previously suspended passive losses - may offset active income, such as W-2 wages.

There’s one more piece to it, though: you also need to meet material participation rules for the rental activities in the year you want to use those losses.Disclosures:

- This content is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.

- Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.