Planning for retirement at 50 requires more than just saving - it’s about avoiding mistakes that can derail your financial future. Here’s what you need to know:

- Hidden risks: Many portfolios have overlaps, like owning the same stocks across multiple funds, which can increase risk and reduce returns.

- Tax inefficiencies: Without proper strategies, taxes can quietly erode your savings. Tools like tax-loss harvesting and asset location can save thousands each year.

- Healthcare costs: Most people underestimate future medical expenses, which can exceed $172,500 per person.

- Withdrawal pitfalls: The standard 4% rule may not work for everyone. AI tools can tailor withdrawal strategies to your specific situation.

- Portfolio adjustments: As you approach retirement, balancing growth and preservation is critical to protect your savings.

AI tools like Mezzi analyze your accounts to identify risks, optimize taxes, and refine your strategy in real-time. By connecting all your accounts, you get a clear view of your finances and actionable advice to improve your retirement readiness - without the high fees of traditional advisors.

Hidden Portfolio Overlaps and Concentration Risks

At 50, juggling multiple accounts can make it hard to see the full picture of your investments. A 401(k) with Fidelity, a Roth IRA at Vanguard, and a taxable account at Schwab each give you just a partial view. This lack of clarity can create hidden risks, especially as you approach retirement. Let’s break down how these overlaps can impact retirement income diversification and performance.

How Overlaps Affect Portfolio Performance

Portfolio overlaps happen when different funds hold the same stocks. For instance, owning VTI and SCHB might unexpectedly push your tech exposure from 20% to 35%. In 2022's market slump, portfolios with such overlaps dropped 28%, compared to 22% for benchmarks that were better diversified.

"I discovered individual stock exposure I didn't even know I had. Turns out my 'diversified' ETF portfolio had significant overlap, with some companies appearing across multiple funds." - Nishant Jayant, Meta engineer

Studies show that around 60–70% of investors over 50 have overlaps exceeding 20%, while their sector concentrations average about 18%, far above the ideal 10–12% range. These overlaps don’t just increase your portfolio’s risk - they also drag down performance. Annual volatility can rise, and returns may underperform benchmarks. On top of that, redundant fees can reduce returns over time. Understanding these risks is essential, and that’s where AI steps in to help.

How AI Identifies Overlaps

Mezzi’s X-Ray feature simplifies the process by consolidating all your accounts and analyzing the securities within each fund. It scans thousands of positions in seconds, uncovering hidden concentrations - like a 15% duplicate exposure to FAANG stocks you didn’t even realize you had. On average, users of Mezzi uncover three to five overlap areas they hadn’t noticed before.

For example, Apple might appear in VOO, VGT, and QQQ, inflating your exposure and disrupting diversification. Traditional methods, like manually comparing spreadsheets, are tedious and prone to error. Mezzi’s AI, on the other hand, uses natural language processing to analyze fund prospectuses and real-time data, quickly identifying overlaps. It can even flag cases where two "diversified" funds share as much as 40% of their holdings.

Tax Inefficiencies and Optimization Opportunities

Tax-Efficient Asset Location Guide for Retirement Accounts

Taxes can quietly chip away at your retirement savings, often without you noticing. By 50, you’re likely juggling a mix of accounts - 401(k)s, Roth IRAs, and taxable brokerage accounts - each with its own set of tax rules. Without a clear strategy, you might end up paying more than necessary. AI tools can uncover tax-saving opportunities that might slip past traditional advisors, especially since many advisors only review portfolios once or twice a year. Let’s dive into how Mezzi’s AI takes advantage of these strategies to keep more of your money working for you.

Tax-Loss Harvesting Year-Round

Tax-loss harvesting involves selling investments at a loss to offset gains and reduce your tax bill. For example, if a stock drops by $5,000, that loss can cancel out $5,000 in gains elsewhere, saving you hundreds in taxes at the 15–20% long-term capital gains rate. The catch? Many advisors only look for these opportunities during tax season, missing the daily fluctuations in the market that create losses throughout the year.

Mezzi’s AI changes the game by monitoring your portfolio 24/7, actively scanning for losses exceeding $1,000. When it spots an opportunity, it suggests selling the losing position and replacing it with a similar - but not identical - asset to maintain your investment strategy. This constant oversight may improve after-tax returns over time. With Mezzi’s AI, every tax-saving opportunity is captured, ensuring you get the most out of your investments.

Next, let’s look at how to sidestep costly wash sales across your accounts.

Avoiding Wash Sales Across Accounts

A wash sale happens when you sell a security at a loss and then repurchase the same - or a substantially identical - security within 30 days before or after the sale. The IRS won’t allow the tax deduction in this case, leaving you stuck with a higher tax bill. This risk multiplies when you’re managing multiple accounts. For instance, you might sell a tech ETF in your taxable account, only to realize you bought a similar one in your IRA 20 days earlier.

Mezzi’s AI helps by linking all your accounts - 401(k)s, IRAs, taxable brokerages - and flagging potential wash sale violations before they occur. If the AI detects a similar purchase within the 30-day window, it sends an alert to delay the repurchase or suggests an alternative, like a broad market ETF, to avoid the wash sale. This ensures you can still claim your $3,000 loss deduction and keeps your tax strategy on track. Traditional methods often overlook these cross-account risks, but Mezzi’s AI keeps you covered.

Now, let’s explore how smart asset placement can make a big difference in tax efficiency.

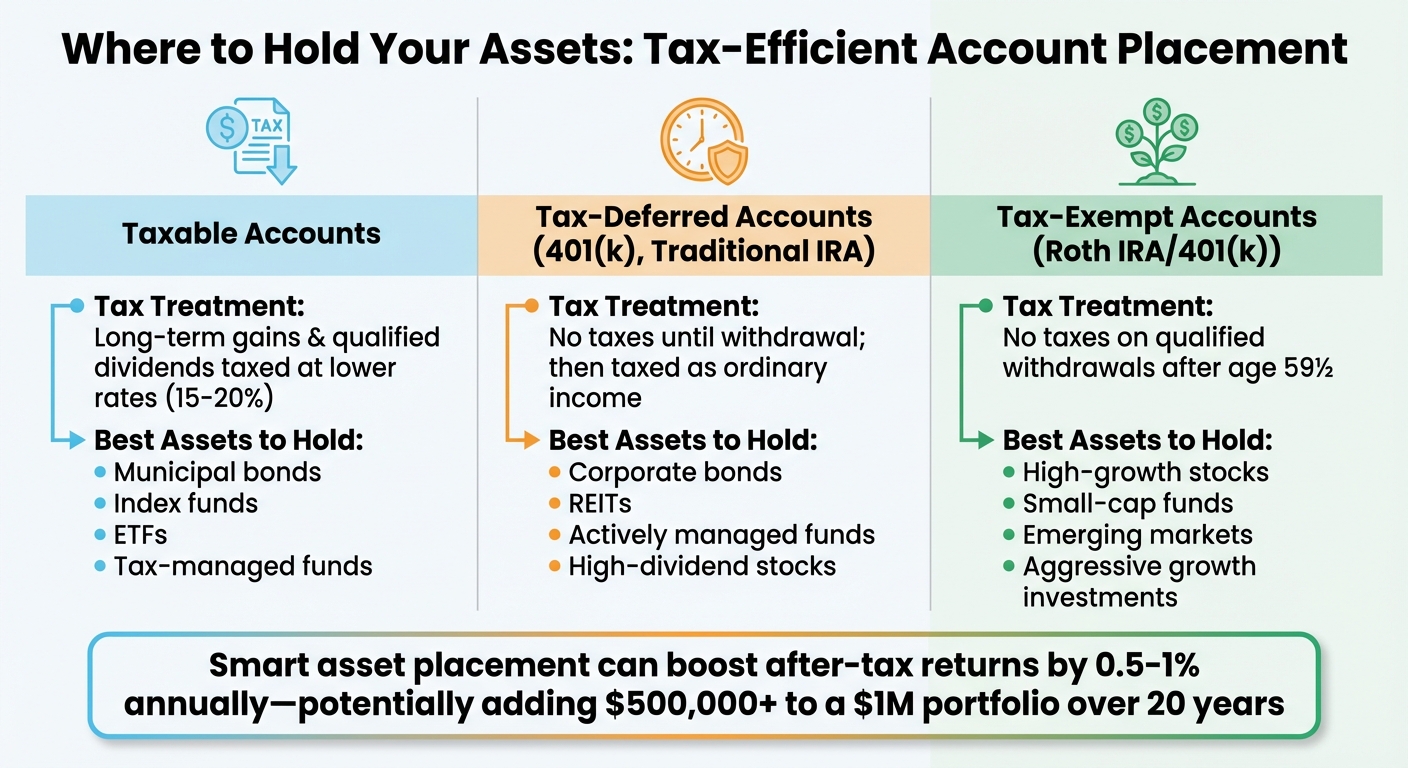

Optimizing Asset Location for Tax Efficiency

Not all accounts handle taxes the same way, which makes the placement of your investments critical. Tax-inefficient assets - like corporate bonds and REITs that generate ordinary income - are best suited for tax-deferred accounts, such as Traditional IRAs, where taxes are deferred until withdrawal. Tax-efficient assets - like index funds and ETFs with low turnover - fit better in taxable accounts, where long-term gains benefit from lower tax rates. Meanwhile, high-growth investments - like small-cap stocks or emerging markets - thrive in Roth accounts, where future gains are entirely tax-free.

Mezzi’s AI takes this a step further by simulating the tax impact of different asset placements over 20–30 years, factoring in projected returns and future withdrawals. For instance, placing high-dividend stocks in a Roth IRA instead of a taxable account could boost net returns by 20–30% over three decades. By reallocating assets, Mezzi can add 0.5–1% to your annual after-tax returns. Over time, this "tax alpha" could be the difference between a secure retirement and running short on funds.

| Account Type | Tax Treatment | Best Assets to Hold |

|---|---|---|

| Taxable Accounts | Long-term gains/qualified dividends taxed at lower rates | Municipal bonds, index funds, ETFs, tax-managed funds |

| Tax-Deferred (401(k), IRA) | No taxes until withdrawal; taxed as ordinary income | Corporate bonds, REITs, actively managed funds |

| Tax-Exempt (Roth IRA/401(k)) | No taxes on qualified withdrawals | High-growth stocks, small-cap funds, emerging markets |

Healthcare Costs and Withdrawal Rate Blind Spots

By the time most people hit 50, they tend to underestimate healthcare expenses while overestimating how much they can safely withdraw from their retirement savings. These blind spots can throw even the best-laid retirement plans off course. Why? Many calculators rely on broad assumptions that don’t account for an individual’s unique situation. That’s where AI-driven tools come in, offering a more detailed analysis by factoring in your specific investments, income sources, and tax profile to expose potential risks.

Healthcare Costs: A Growing Concern

Did you know the average 65-year-old will need about $172,500 to cover healthcare expenses in retirement? Despite this, nearly two-thirds of pre-retirees plan to budget $1,220 less than the estimated annual cost of $8,600. That’s a serious gap. To make matters worse, medical costs have skyrocketed by over 120% since 2000 and continue to climb at a rate of 5–7% annually - well above general inflation and Social Security cost-of-living adjustments.

Another commonly overlooked factor? Long-term care. More than 70% of people don’t expect to need it, even though it’s one of the biggest drains on retirement savings.

"Our research shows many households may be unprepared for the realities of the healthcare challenges and expenses they will face."

- Glen Franklin, Assistant Vice President of Research at Jackson National Life Distributors LLC

This is where Mezzi’s AI steps in. Unlike generic calculators, it analyzes your projected income streams - like retirement distributions, capital gains, and Social Security - and flags potential IRMAA surcharges (income-based Medicare premium increases). These surcharges can add hundreds to your monthly costs. For example:

- If your Modified Adjusted Gross Income (MAGI) as an individual exceeds $106,000, your Medicare Part B premium jumps from $185 to $259 per month.

- Cross $133,000, and it spikes to $370 per month.

Mezzi’s AI doesn’t just highlight these thresholds - it projects them over 20–30 years, accounting for your portfolio’s growth and withdrawal strategies. It even suggests ways to manage your MAGI to avoid unnecessary surcharges.

Understanding these escalating healthcare costs is crucial because they directly impact how you approach your withdrawal strategy.

Withdrawal Rates and Portfolio Longevity

Once you’ve accounted for healthcare expenses, the next step is fine-tuning your withdrawal strategy. The traditional 4% rule may not cut it. Why? It doesn’t consider your portfolio’s specific makeup, fees, or market conditions. For example, retiring during a market downturn and withdrawing 4% could lock in losses that might snowball over time.

Mezzi’s AI goes a step further by simulating countless market scenarios based on your actual holdings, fees, and tax situation. It calculates a sustainable withdrawal rate tailored to your portfolio, often recommending a more conservative approach, using tax-efficient withdrawals vs. traditional approaches to ensure your savings last 20–30 years.

"We are particularly concerned that too many people nearing or in retirement don't have a good grasp of their potential healthcare needs and out-of-pocket costs, which could narrow their options when it comes time to pay the bills."

- Andrew Eschtruth, Director of the Center for Retirement Research at Boston College

Asset Allocation for Decumulation

Once you've addressed healthcare costs and withdrawal rates, it's time to adjust your portfolio for decumulation. By the time you hit 50, your investment priorities shift from accumulating wealth to preserving it while generating income. This phase requires balancing three goals: achieving enough growth to keep up with inflation, protecting your capital to avoid running out of money, and ensuring a steady income to cover living expenses.

Shifting from Growth to Preservation

When you're 35, a 30% market drop might feel like just a bump in the road - you've got decades to recover. But at 50 or older, things look different. The "Retirement Red Zone" - the five years before and after retirement - is a critical period where portfolio performance carries extra weight. A significant market downturn during this time could seriously impact your financial security, thanks to something called sequence of returns risk.

To mitigate this risk, gradually reduce your exposure to equities. A more balanced portfolio can help by leaning into income-generating assets like dividend stocks, municipal bonds, or Treasury Inflation-Protected Securities (TIPS). The exact mix depends on your unique needs, but the goal is to reduce volatility while still aiming for modest growth.

Research from BlackRock, which oversees $498 billion in lifecycle solutions, supports this gradual transition. They use AI-enhanced glidepath adjustments to fine-tune the process. The next step? Leveraging AI to streamline rebalancing while keeping taxes in check.

AI-Optimized Rebalancing Strategies

Preservation becomes the name of the game in decumulation, and rebalancing takes on a new level of importance. But rebalancing comes with challenges - especially taxes. Selling appreciated stocks to buy bonds might align your portfolio, but it can also trigger capital gains taxes that eat into your returns. Traditional advisors often rebalance on a fixed schedule, without considering tax impacts or market conditions.

This is where Mezzi's AI shines. Instead of sticking to a rigid calendar, it uses threshold-based rebalancing. Mezzi continuously monitors your portfolio and suggests adjustments only when your asset allocation drifts beyond a set range. This approach reduces unnecessary trades and minimizes tax drag. On top of that, Mezzi identifies tax-efficient strategies, like focusing rebalancing efforts within tax-advantaged accounts (401(k)s, IRAs) and using tax-loss harvesting or deferring capital gains to offset your tax liability.

For example, let’s say you need to reduce your equity exposure from 70% to 55%. Mezzi will analyze your portfolio to find positions with potential losses to harvest first, recommend selling those, and suggest directing new contributions toward bonds. It will also advise on which accounts - taxable or tax-advantaged - should be adjusted to limit your overall tax liability. This careful, tax-aware strategy helps preserve more of your investment returns, allowing your money to grow more effectively over time.

Another benefit? Mezzi takes a holistic view of your portfolio. It considers all your accounts - 401(k)s, IRAs, taxable brokerage, and Roth accounts - when offering advice. This comprehensive perspective ensures that your assets are optimized across the board, unlike traditional advisors who may only focus on the accounts they directly manage.

How Mezzi Simplifies Retirement Planning with AI

Managing retirement accounts across multiple platforms often creates a fragmented picture of your finances. This disjointed approach can lead to costly mistakes, as it’s hard to spot risks and overlaps without a unified view. That’s where Mezzi steps in, offering a smarter way to plan for retirement by leveraging AI.

Mezzi provides a complete financial overview without requiring you to move your assets. By connecting your accounts through secure, read-only access, its AI analyzes your entire portfolio. It identifies risks, redundancies, and opportunities that traditional advisors might overlook because they only focus on the assets they manage. And unlike advisors who charge 1% of your assets under management, Mezzi offers its service starting at just $299 per year. This affordable, ongoing monitoring addresses the challenges of fragmented account management while delivering fiduciary-level guidance.

Full Visibility Across All Accounts

Having a clear view of all your accounts is key to avoiding hidden risks. Mezzi achieves this by aggregating financial data from platforms like Plaid and Finicity (Mastercard), linking your 401(k)s, IRAs, Roth accounts, HSAs, and taxable brokerage accounts into one seamless dashboard. Importantly, your assets remain right where they are - there’s no need to transfer funds, switch custodians, or deal with unnecessary complications. Mezzi simply accesses your account data securely, without handling logins, trades, or money transfers.

This consolidated view can uncover insights that might otherwise go unnoticed. For instance, if you own Microsoft stock in a taxable account and also hold an S&P 500 ETF in your 401(k) that’s heavily weighted toward Microsoft, Mezzi’s X-Ray tool will flag the overlap. Traditional advisors, limited to the accounts they directly manage, might miss such duplications. With Mezzi, you gain clarity across your entire portfolio.

Real-Time Guidance Without the Wait

Mezzi doesn’t just offer a static snapshot of your finances - it actively monitors your portfolio around the clock, delivering timely insights. Whether it’s identifying tax-loss harvesting opportunities throughout the year or alerting you when your asset allocation drifts off course, Mezzi provides actionable recommendations in real time.

Wondering if you can retire at 62? Mezzi answers that question based on your actual accounts, not generic models or assumptions. If a tax-loss harvesting opportunity arises and you act on it, Mezzi will even notify you when the 30-day wash sale window has passed, so you can repurchase safely.

This kind of proactive, real-time guidance eliminates the delays and high fees typical of traditional advisors. By combining advanced analysis with immediate notifications, Mezzi simplifies the retirement planning process, ensuring you stay on track without the usual hassle or expense.

Getting Started with AI Retirement Planning

You can set up Mezzi in just a few minutes without needing to move your assets. The platform securely links to your existing accounts using read-only access and instantly starts analyzing your portfolio. This helps you spot risks and opportunities you may have overlooked. Here’s how to get actionable AI insights for your retirement portfolio in four simple steps.

Step 1: Connect All Accounts

Start by creating your Mezzi account, and for added privacy, you can use your Apple login. Then, link all your accounts - 401(k)s, IRAs, Roths, taxable accounts, and HSAs. Mezzi uses trusted aggregators like Plaid and Finicity (a Mastercard company) to securely connect with thousands of financial institutions, including Schwab, Fidelity, Vanguard, and Chase. Rest assured, these connections are secure and read-only.

Step 2: Review Overlaps and Risks

Once your accounts are linked, use Mezzi’s X-Ray tool to scan your portfolio for hidden overlaps and risks. This tool identifies duplicate exposures, such as owning Apple stock directly in a taxable account while also holding an S&P 500 ETF in your 401(k) that’s heavily weighted toward Apple. Eliminating these overlaps can save you from paying unnecessary fees.

"Mezzi's X-Ray feature allowed me to uncover exposure to stocks I didn't realize I had."

– Shuping, Founder of Summer AI

The tool also flags potential vulnerabilities, like if more than 40% of your portfolio is concentrated in tech stocks. This insight is critical for reducing risk and refining your asset allocation.

Step 3: Act on Tax and Allocation Recommendations

Mezzi doesn’t just identify opportunities - it shows you how to act on them. For example, it might suggest harvesting bond losses to offset gains. It also offers tax-efficient asset location strategies.

If Mezzi recommends adjusting your stock allocation - for instance, shifting from 60% to 50% for better preservation - it provides a clear breakdown of which positions to adjust and in which accounts. This minimizes tax impacts, and you can execute changes directly through your brokerage.

Step 4: Monitor Progress and Adjust

Mezzi doesn’t stop at recommendations - it continuously monitors your portfolio. It tracks your retirement readiness score, factoring in account performance, safe withdrawal rate projections (typically 3.5–4%), and healthcare cost estimates. For example, Fidelity estimates lifetime healthcare costs of about $315,000 for a couple.

"Mezzi gives me answers and ideas when I need them, no matter what time of day or how big or small the question."

– Mike, Product Manager

If you sell assets for tax-loss harvesting, Mezzi will alert you when the 30-day wash sale window ends so you can safely repurchase. It also notifies you if market changes cause your stock allocation to drift (e.g., from 50% to 55%), providing actionable advice to rebalance efficiently. With continuous monitoring, you can make timely adjustments and keep your retirement strategy on track. These tools ensure you stay actively engaged in managing your retirement planning.

Conclusion

At 50, it’s time to uncover hidden risks and untapped opportunities in your portfolio with AI-powered insights. Mezzi helps address key challenges like unnoticed overlaps, tax inefficiencies, and decumulation risks, giving you the tools to refine your retirement strategy.

What sets Mezzi apart? It offers complete visibility and real-time guidance - without the high fees or long wait times. By linking all your accounts - 401(k)s, IRAs, taxable brokerage accounts, and HSAs - you gain access to fiduciary-level insights. Mezzi pinpoints areas of overexposure in your portfolio, highlights tax-loss harvesting opportunities, and provides tailored advice for efficient rebalancing across your accounts.

With AI taking care of overlap detection and scenario modeling, you can focus on making informed, actionable decisions. Even small adjustments based on Mezzi’s insights can help improve your portfolio management. These recommendations come straight from your connected accounts, ensuring they’re specific to your financial situation.

The process couldn’t be simpler: connect your accounts, review AI-identified risks, act on tax and allocation suggestions, and continuously monitor your progress. In just minutes, you’ll have access to insights without traditional assets-under-management fees. This streamlined approach ensures every decision you make is backed by data.

Take control of your retirement planning with Mezzi. Spot risks early, make smarter decisions, and secure a more confident future. Your portfolio has a story to tell - Mezzi helps you understand it.

FAQs

What should I fix first in my portfolio at age 50?

When it comes to managing your portfolio, it's crucial to address the risk of over-concentration. If too much of your investment is tied up in a single asset or sector, your financial stability could take a hit if that area underperforms. To avoid this, consider rebalancing your holdings. This means adjusting your investments to match your target asset allocation - essentially, the mix of stocks, bonds, and other assets that aligns with your financial goals and risk tolerance.

By regularly rebalancing, you can reduce exposure to risks you didn’t intend to take on. Plus, it helps create a more diversified portfolio, which can provide a steadier foundation for your finances, especially as you get closer to retirement. Diversification spreads your investments across various areas, so no single downturn has too much impact on your overall wealth.

How do I avoid wash sales across my accounts?

AI tools, such as Mezzi, offer a practical way to help you stay compliant with IRS rules on wash sales. By linking your accounts and monitoring trades in real time, these tools keep track of purchase and sale dates, ensuring you don’t accidentally buy the same or a substantially identical security within the 30-day window before or after selling at a loss. On top of that, they can recommend alternative investments and generate reports that meet IRS standards, making record-keeping much easier.

How can I lower Medicare IRMAA in retirement?

To reduce Medicare IRMAA costs in retirement, consider appealing the adjustment if you’ve experienced qualifying life events, such as marriage, divorce, or a significant income change. Providing proper documentation can help correct any inaccuracies in income calculations.

You can also take proactive steps to manage your taxable income. For example, Roth conversions or tax-efficient withdrawals from investment accounts can help lower your modified adjusted gross income (MAGI), keeping it below IRMAA thresholds. Staying mindful of your income levels is key to avoiding these additional surcharges.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.