Looking to optimize your retirement income diversification? Here's the key difference: SCHD focuses on growing dividends over time, while VYM prioritizes higher payouts now. SCHD is ideal for retirees aiming to keep up with inflation through long-term growth. VYM suits those needing immediate, steady cash flow. Both ETFs provide tax-efficient dividends but cater to different goals, which you can further analyze by using AI to evaluate your dividend portfolio.

Quick Overview:

- SCHD: Long-term dividend growth, lower initial yield, better for inflation protection.

- VYM: Higher current yield, steady income for immediate needs, broader diversification.

Choose SCHD for future growth or VYM for current income - or combine both for balance.

VYM Is Winning 2025 - But SCHD Is Building Real Wealth

SCHD: Dividend Growth Strategy

SCHD focuses on companies with a strong history of increasing dividends, providing an income stream that can keep pace with rising costs.

Investment Approach and Index Details

SCHD tracks the Dow Jones U.S. Dividend 100 Index, which identifies high-quality dividend-paying companies using specific financial metrics. To maintain diversification, the fund caps individual holdings and periodically rebalances. This ensures that companies failing to meet its quality criteria are replaced with those showing a steady ability to grow dividends. This disciplined strategy contributes to SCHD's track record of reliable performance.

Performance Data: Growth and Returns

SCHD has shown consistent returns, supported by regular dividend increases and a low expense ratio. These features make it an attractive option for long-term investors looking to maximize gains over extended periods.

When SCHD Works Best

SCHD is a strong choice for retirees with a long-term outlook. Its initially modest yields grow over time, helping to counteract inflation, especially when dividends are reinvested in tax-advantaged accounts. It’s particularly effective in traditional or Roth IRAs, where reinvested dividends can compound without immediate tax implications. Unlike strategies focused solely on high yields, SCHD prioritizes growth, making it an appealing option for retirees aiming to preserve and grow wealth over the long run.

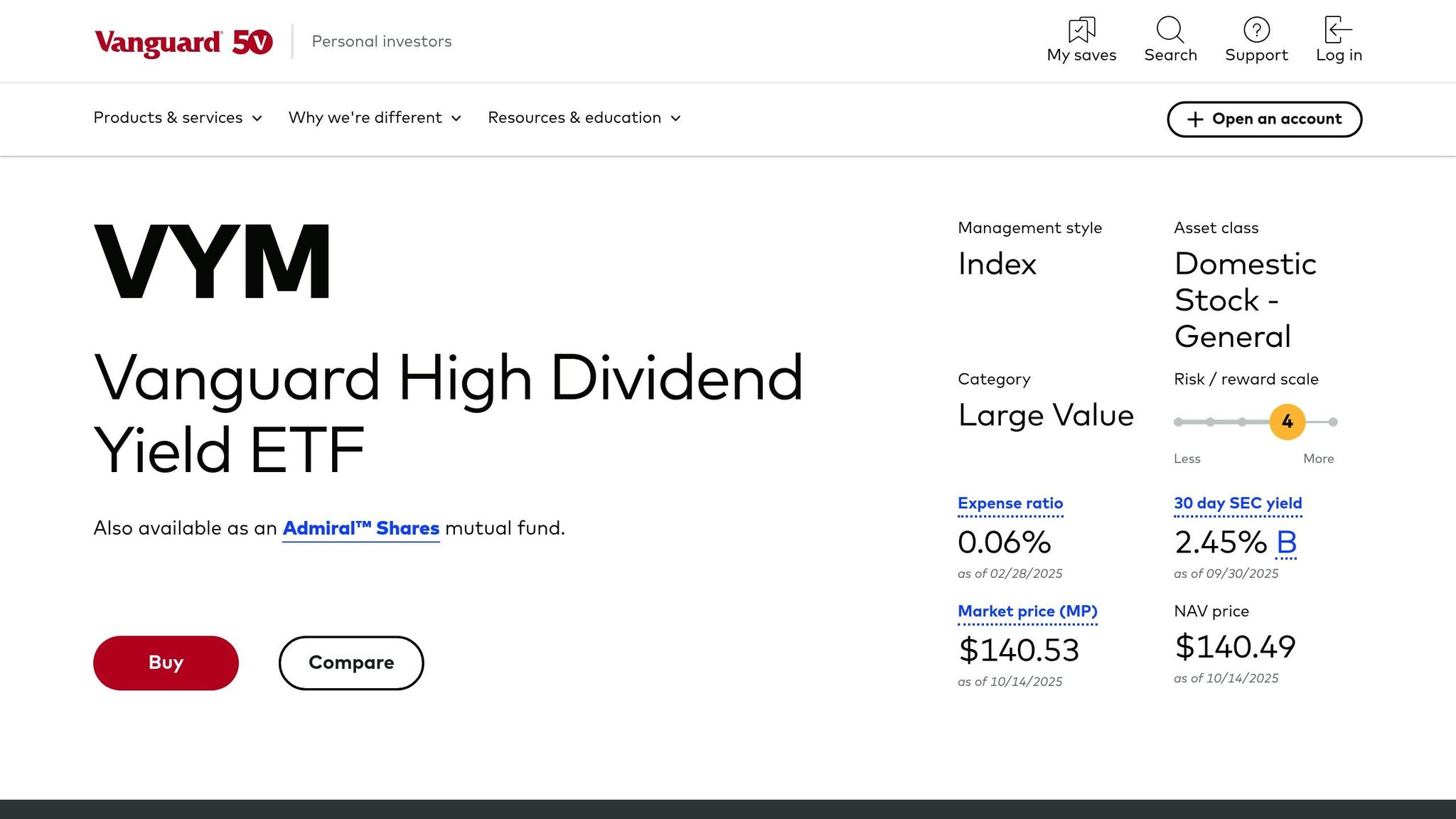

VYM: Current Yield Strategy

VYM is tailored for those seeking immediate income rather than long-term dividend growth, making it a strong option for retirees needing steady cash flow. Here's how VYM aligns with its income-focused strategy.

Investment Approach and Index Details

VYM follows the FTSE Custom High Dividend Yield Index, which selects companies based on their projected dividends over the next 12 months. The fund targets firms already paying substantial dividends and excludes REITs to concentrate on traditional dividend-paying corporations.

With a portfolio of roughly 580 companies, VYM has a notable concentration in its top 10 holdings, which account for about 26% of its total assets. The fund leans heavily toward large-cap, value-driven companies with a history of returning cash to shareholders. These are typically mature businesses operating in stable industries, known for generating consistent cash flows that support reliable dividend payments.

Performance Data: Yield and Consistency

VYM consistently offers higher current yields compared to strategies centered on dividend growth. This is achieved by prioritizing companies that distribute cash to shareholders instead of reinvesting earnings. Its sector allocation reflects this focus, with Financial Services, Technology, Healthcare, Consumer Defensive, Industrials, and Energy making up the bulk of the portfolio. These sectors are dominated by established companies with mature business models and steady cash flows, making them dependable sources of dividends.

When VYM Works Best

For retirees relying on investment income to cover living expenses, VYM's emphasis on delivering higher current yields can provide immediate financial support. Its consistent income stream helps with budgeting and financial planning, offering a practical solution for those prioritizing predictable cash flow over long-term growth.

SCHD vs VYM: Direct Comparison

After analyzing SCHD's focus on growth and VYM's emphasis on current income, it's time to directly compare their core metrics. SCHD and VYM stand apart in terms of tax efficiency and income strategy. While both funds deliver dividends in a tax-efficient manner, they cater to different retirement income needs. The table below highlights their key metrics, offering a snapshot of their differences.

Key Metrics Comparison

| Metric | SCHD | VYM |

|---|---|---|

| Tax Efficiency | 100% of dividends are qualified | Over 90% of dividends are qualified |

Tax efficiency is a significant factor for investors. SCHD has a slight advantage, with all of its dividends historically qualifying for lower tax rates - 0%, 15%, or 20%, depending on capital gains tax brackets. VYM also performs well, with over 90% of its dividends typically meeting the qualified dividend criteria. Moreover, neither fund has historically distributed capital gains, making them even more appealing for taxable accounts. However, for retirees choosing between taxable accounts or IRAs for tax efficiency, this distinction may hold less weight. Beyond tax considerations, the decision often comes down to balancing dividend growth versus immediate yield and your withdrawal strategy.

Growth vs Yield Trade-offs

SCHD focuses on dividend growth over time, making it ideal for those seeking increasing income as they move through retirement. On the other hand, VYM provides higher immediate payouts, appealing to retirees who prioritize cash flow right now. Choosing between these ETFs depends on your retirement goals: opt for SCHD if you're looking for dividends that grow steadily or VYM if you need higher income upfront. Both funds, however, offer tax-efficient benefits for those investing in taxable accounts.

Managing Retirement Income with Mezzi

Once you've decided between SCHD and VYM, the next step in managing your dividend portfolio is paying attention to tax efficiency, risk management, and income projections. Mezzi offers a suite of tools designed to fine-tune your dividend ETF approach. Let’s break down how each tool can help you shape your retirement income strategy.

Portfolio Analysis and Tax Savings

Tax efficiency plays a big role in keeping more of your dividend income, especially in taxable accounts. Mezzi’s tax optimization tools help you sidestep common mistakes, like wash sales across multiple accounts. By keeping a close eye on your portfolio, the platform flags potential tax issues, helping you avoid unnecessary expenses that could chip away at your retirement income.

Risk Analysis with X-Ray Tool

Dividend-focused portfolios can sometimes carry hidden risks, like over-concentration risks by issuer or sector. Mezzi’s X-Ray tool digs into the holdings of SCHD and VYM, pinpointing areas where your portfolio might be too concentrated. This feature ensures your investments align with your risk tolerance, giving you a clearer picture of whether your portfolio is truly balanced.

Retirement Planning with Financial Calculator

Planning for retirement means having a clear sense of what your income will look like down the road. Mezzi’s Financial Calculator takes into account factors like your portfolio size, annual contributions, expected returns, and fees. It offers projections tailored to different dividend strategies, making it easier to decide when and how to rebalance or withdraw funds.

Conclusion: Choosing the Right ETF for Retirement

Deciding between SCHD and VYM largely comes down to your retirement goals and income timeline. If you have many years ahead before fully relying on dividends, SCHD's focus on growing payouts over time could help protect your purchasing power against inflation. On the other hand, if you're already retired or need higher income now, VYM's larger immediate yield might better suit your needs. For instance, individuals in their early 60s planning for a 20-30 year retirement may benefit from SCHD's growth-oriented approach, while those actively drawing income could lean toward VYM.

Taxes are another key factor to consider. Both ETFs are designed with tax efficiency in mind, but their impact varies depending on whether you hold them in taxable accounts or tax-advantaged ones like IRAs or 401(k)s. SCHD's focus on companies with sustainable dividend growth often leads to more favorable tax treatment, while VYM's higher payouts could result in more taxable income if held outside retirement accounts. This makes a case for diversifying your portfolio to manage both income and tax implications effectively.

In fact, many retirees choose to include both SCHD and VYM in their portfolios. You might allocate a larger share to VYM for immediate income while keeping SCHD for its potential to grow dividends over time. This strategy helps balance short-term cash flow with long-term financial security.

To make the most informed decision, it's important to look beyond just the numbers. Mezzi's platform offers tools like the X-Ray tool, which identifies any overlapping holdings in your portfolio, and the Financial Calculator, which projects how different dividend strategies could impact your retirement income. These resources simplify the process, helping you align your portfolio with your overall retirement goals while balancing current income and future growth.

FAQs

What are the key differences in risk and sector exposure between SCHD and VYM, and how could these impact my retirement portfolio?

SCHD and VYM take distinctly different approaches when it comes to risk and sector focus, which can play a big role in shaping your retirement strategy.

SCHD zeroes in on roughly 100 companies that demonstrate solid fundamentals and a track record of consistent dividend growth. It leans heavily on sectors like financials, healthcare, and consumer staples. While this concentrated strategy might pave the way for stronger growth over time, it also comes with the downside of being more vulnerable to risks tied to specific sectors.

VYM, by contrast, casts a wider net with over 500 stocks, creating a more diversified portfolio. It places significant weight on financials and technology. This broad diversification helps spread out company-specific risks, but it might not deliver the same level of dividend growth you'd see with SCHD.

For retirees, the choice often comes down to priorities: SCHD may appeal to those who value dividend growth and high-quality holdings, while VYM could be a better fit for those looking for steady income with less exposure to concentrated risks.

What are the tax differences between holding SCHD or VYM in a taxable account versus a retirement account like an IRA?

The way SCHD and VYM are taxed depends on whether you hold them in a taxable account or a tax-advantaged account, such as an IRA. If they are in a taxable account, any dividends you receive will be subject to taxes. Qualified dividends benefit from lower capital gains tax rates, ranging from 0% to 20% based on your income level. On the other hand, nonqualified dividends are taxed at your regular income tax rate, which can go as high as 37%.

If these funds are held in a retirement account like an IRA or 401(k), the tax situation changes. Dividends earned within these accounts are not taxed immediately. Instead, taxes are deferred until you withdraw the funds, at which point the withdrawals are taxed as ordinary income. This makes tax-advantaged accounts a smart option for reducing immediate tax obligations on dividend income.

Can combining SCHD and VYM help retirees balance current income with long-term dividend growth, and how should they be allocated?

Combining SCHD and VYM can be a smart move for retirees aiming to balance immediate income with long-term dividend growth. Here's why: SCHD emphasizes dividend growth and tax efficiency, while VYM delivers higher current yields along with broad diversification and lower volatility.

How you split your allocation between the two largely depends on your financial priorities. If steady income is your main goal right now, you might lean more heavily toward VYM. On the other hand, if you're looking to grow your dividend income over time, SCHD could play a larger role in your portfolio. For many retirees, a blend of both ETFs creates a strategy that balances income needs with future growth potential.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.