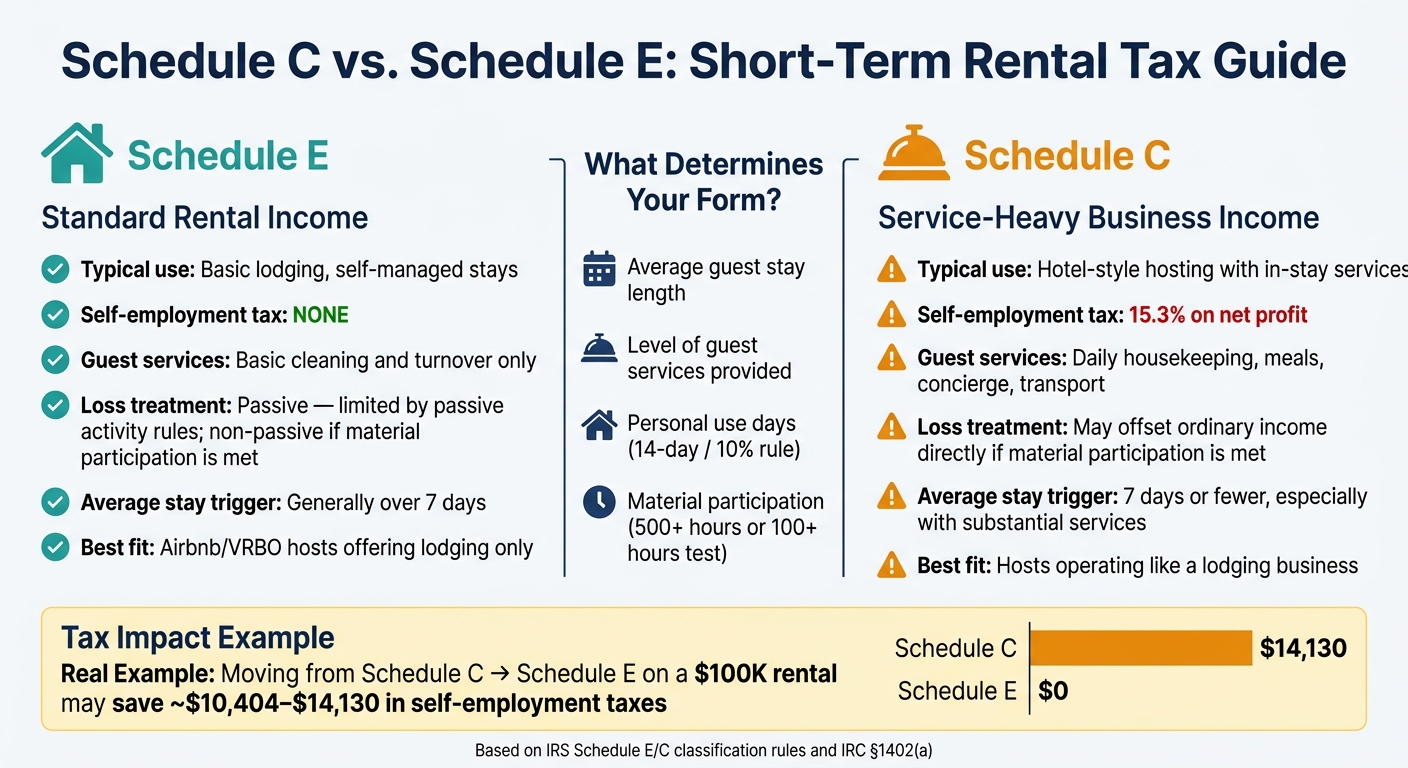

A short-term rental may go on Schedule E or Schedule C, and that choice may change self-employment tax by thousands of dollars. In many cases, the key inputs may be average guest stay, guest services, personal use, and material participation.

Here’s the short version:

- If a rental looks like basic lodging, it may lean toward Schedule E

- If it looks more like a service business, it may lean toward Schedule C

- Schedule C profit may face 15.3% self-employment tax

- Schedule E income generally may not face self-employment tax

- Stays of 7 days or less may affect passive-loss treatment

- Personal use over 14 days or 10% of rental days may limit or block losses

- Renting for 14 days or less in a year may make the income nonreportable in some cases

I’d frame it this way: the platform doesn’t decide the tax result. How the property runs day to day may matter more than whether it’s listed on Airbnb or Vrbo.

A simple example shows the gap. A host with no hotel-style services and an average stay of 11 days reportedly moved from Schedule C to Schedule E and may have avoided $10,404 in self-employment tax. Same rent. Different tax treatment.

Schedule C vs. Schedule E for Short-Term Rentals: Key Tax Differences

Airbnb Tax Secrets: How to Optimize Your Short Term Rental Taxes

Quick Comparison

| Topic | Schedule E | Schedule C |

|---|---|---|

| Usual setup | Rental activity | Service-heavy business activity |

| Guest services | Basic cleaning/turnover | In-stay services, meals, concierge, transport |

| Self-employment tax | Generally none | May apply at 15.3% |

| Loss treatment | May be passive unless an STR exception and material participation apply | May offset other income if material participation rules are met |

| Best fit in many cases | Self-managed stays with basic lodging | Hotel-like hosting |

Bottom line: I’d treat this as a facts-and-circumstances issue, not a branding issue. The article may be most useful if you want a plain-English way to sort the form choice, tax exposure, and loss rules before filing.

IRS filing rules: when short-term rental income goes on Schedule E vs. Schedule C

The IRS looks at how the activity runs in practice. The main tests are average stay length, services provided, and how the property is used. The day-to-day question is simpler: based on those facts, which form may fit the activity?

Most short-term rentals default to Schedule E as passive rental income, and that income is generally exempt from self-employment tax under IRC §1402(a).

| Feature | Schedule E | Schedule C |

|---|---|---|

| Form Purpose | Supplemental income from rental activity | Profit or loss from a business |

| Typical Trigger | Average stay over 7 days, or 7 days or fewer with only basic services | Guest services beyond basic upkeep |

| Self-Employment Tax | No, generally exempt | Yes |

How average guest stay length affects tax classification

An average stay of 7 days or fewer may move the activity out of default rental treatment. But that fact by itself may not force Schedule C. After that, the service test and the owner’s level of participation may shape the filing result.

What counts as substantial services to guests

If the stay test doesn’t settle it, the service test often does. Basic host services usually may not change the filing position.

Services that may push the activity toward Schedule C include:

- Daily housekeeping during a stay

- Prepared meals

- Concierge support

- Transportation

How personal use and the 14-day rule affect reporting

Personal use may change both the filing result and the amount that may be deductible.

If you rent a property for 14 days or fewer during the year, the income is generally tax-free and may not need to be reported. In that case, rental expenses generally may not be deducted against that exempt income. Mortgage interest and property taxes may follow the usual personal-use rules.

Once personal use goes over the greater of 14 days or 10% of rental days, the property is treated as mixed-use. When that happens, rental losses are generally limited to rental income.

If the activity still qualifies as a rental, Schedule E is usually the starting point.

Schedule E: the standard path for self-managed vacation rentals

For many Airbnb and VRBO hosts, Schedule E may fit when the property is mainly providing lodging, not hotel-style service. If you offer basic lodging and only minimal guest services, the activity generally belongs on Schedule E as passive rental income. That label may affect both the deductions you claim and whether self-employment tax applies.

What hosts can deduct on Schedule E

Schedule E deductions may cover a lot of common rental costs. Hosts may generally deduct Airbnb or Vrbo fees, guest turnover cleaning, mortgage interest, property taxes, insurance, utilities, repairs, supplies, and depreciation. Depreciation may end up being the biggest deduction for many owners.

Why Schedule E often means no self-employment tax

The main tax upside is that Schedule E income generally may not be subject to self-employment tax. That may be a meaningful difference from Schedule C, where self-employment tax may apply to net profit directly.

Once guest services go beyond basic lodging, the filing path may start to shift toward Schedule C.

Schedule C: when a rental starts operating like a hospitality business

Once guest service starts to look more like a hotel stay, the tax filing question may shift from rental income to business income. When a short-term rental operates more like a lodging business, Schedule C may apply. The clearest sign is substantial in-stay service, such as daily housekeeping, prepared meals, concierge assistance, or transportation. Those services go well beyond what a typical Airbnb or VRBO host may offer.

Most short-term rentals may still belong on Schedule E. Schedule C may come into play when the property is run more like a lodging business.

The IRS looks at the full set of facts, so two similar rentals may end up on different forms based on the level of service the host provides.

The self-employment tax tradeoff

Filing on Schedule C may come with a real financial cost for profitable properties. In 2026, self-employment tax is 15.3%, applied to 92.35% of net profit. On net profit of $100,000, that may add roughly $14,130 in self-employment taxes that Schedule E filers generally may not owe.

If you materially participate, Schedule C losses may offset ordinary income directly, without passive-loss limits.

"Schedule C business losses, for hosts who materially participate in the activity, are not subject to passive activity loss limitations. They reduce ordinary income directly, without the $25,000 annual cap." - Jed Collins, Legal & Policy Contributor, StaySTRA

Here’s how the two forms compare on the factors that matter most:

| Feature | Schedule C | Schedule E |

|---|---|---|

| Self-employment tax | 15.3% on net profit | Generally none |

| Loss deductibility | May offset ordinary income | Limited by passive activity rules |

| Typical use | Daily in-stay services provided | Basic lodging only |

The next issue is material participation, because that may affect whether Schedule C losses offset other income.

Example: owner-operated property with hotel-style services

A short average stay may matter most when it’s paired with in-stay services and hands-on management. Consider Marcus, a beach house host operating in 2026 with an average guest stay of 4 nights. He provides daily towel service and manages all bookings and guest communications. Because he provides services during each stay and actively manages the property, his rental is classified as a Schedule C business - meaning his net profit is subject to the 15.3% self-employment tax.

Marcus’s situation shows the core point: it’s not just the short average stay that may trigger Schedule C. It’s the mix of in-stay services and active involvement that may push the activity into business territory. How that active involvement is measured - and what it may mean for loss deductibility - is what the next section covers.

Material participation and common host scenarios

How material participation affects loss deductibility

Once the filing form is set, the next issue is whether the loss may offset ordinary income this year. Form choice alone doesn't control loss treatment. Passive-activity status may.

For short-term rentals with average stays of 7 days or less, the activity may fall outside the IRS rental-activity treatment under the passive-loss rules. REPS may not be required in that case. Material participation may be enough, such as:

- 500+ hours during the year

- 100+ hours, if that amount is more than anyone else involved

If a host meets that bar, losses tied to depreciation or operating costs may offset ordinary income, including W-2 wages. If not, those losses may be passive and are generally suspended unless passive income is available to absorb them.

Personal use above the 14-day threshold, or above 10% of rental days, may block losses entirely, no matter the participation level.

Four common setups and their likely reporting outcome

These four setups cover many of the host arrangements people run into.

| Scenario | Likely Form | SE Tax Risk | Loss Deductibility |

|---|---|---|---|

| Personally managed STR (avg stay ≤ 7 days, basic services) | Schedule E | None | Non-passive if MP met - may offset W-2 income |

| STR with property manager (avg stay ≤ 7 days) | Schedule E | None | Likely passive unless the owner meets material participation |

| Owner-run unit with hotel-style services | Schedule C | Subject to SE tax | Generally not subject to passive-loss limits |

| Mixed-use vacation home (personal use > 14 days or 10% of rental days) | Schedule E | None | Losses disallowed by vacation home rule |

A personally managed Airbnb and one turned over to a property manager may look almost the same on paper. The difference often comes down to the owner's hour count. That may be what separates a current deduction from a suspended loss.

A simple framework for choosing the right reporting approach

When sorting out which form may apply, it may help to move through a few questions in order.

First, does the activity look more like a lodging service or a standard rental? If substantial in-stay services are involved, Schedule C may be required. If not, Schedule E is usually the starting point.

Second, what is the average guest stay? Divide total rental days by the number of separate rental periods. If the result is seven days or less, the STR exception may apply, and the activity may fall outside the standard rental passive-loss rules.

Third, does personal use stay below the 14-day threshold? If that line is crossed, loss deductions may be eliminated entirely.

Last, does the owner meet a material participation test? If yes, losses may be treated as non-passive and may reduce ordinary income now instead of being deferred.

Track hours, guest-stay days, expenses, and personal use through the year. Those records may drive both form choice and loss treatment.

FAQs

How do I calculate average guest stay?

Divide the total number of nights a property was rented during the tax year by the total number of separate guest bookings. Do this for each property on its own.

Here’s the basic math: 200 rented nights across 50 bookings equals an average guest stay of 4 days.

To keep reporting accurate, track two things for each property:

- Total rented nights

- Total number of bookings

Then divide rented nights by bookings to get the average stay length.

What services count as substantial guest services?

Guest services may be treated as substantial when they’re offered mainly for the guest’s convenience and go beyond normal landlord tasks. That may include daily housekeeping during a stay, meal or breakfast service, concierge support, organized activities or tours, and transportation such as airport shuttles.

By contrast, basic rental tasks - like providing linens, cleaning between stays, maintenance, Wi‑Fi, and self-check-in - do not count as substantial services.

What records should I keep for Schedule E or C?

Keep organized records for rental income, platform fees, property taxes, insurance, mortgage interest, depreciation, and receipts for repairs, cleaning, and guest amenities.

If you're claiming a specific tax treatment, it may also make sense to keep time logs that show your participation in bookings, guest communication, and maintenance. Along with that, keep records of average guest stay length, total days rented, and separate rental periods.Disclosures:

- This content is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.

- Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.