The order you tap retirement accounts may change your tax bill by more than many retirees expect. A common rule of thumb - taxable first, pre-tax next, Roth last - may work in some cases. But it may also leave money in pre-tax accounts too long, which may later lead to bigger RMDs, more Social Security being taxed, and higher Medicare premiums.

Here’s the short version:

- Taxable brokerage first may keep ordinary income lower, since only gains may be taxed.

- Pre-tax IRA/401(k) withdrawals add to income dollar-for-dollar, so some retirees may use them early to fill lower tax brackets.

- Roth withdrawals may be useful in high-income years because they usually do not add to AGI or MAGI.

- HSA withdrawals for qualified medical costs may come out tax-free.

- Cash may work as a short-term spending buffer, though interest may still add to taxable income.

A fixed order may miss key tax windows. Some retirees may lower lifetime taxes by using a mix each year instead of following one rule every year. That may matter most in:

- Low-income years before Social Security and RMDs

- Years near IRMAA thresholds

- Years with large pre-tax balances

- Years when Roth assets may be better held back or used as a tax-pressure valve

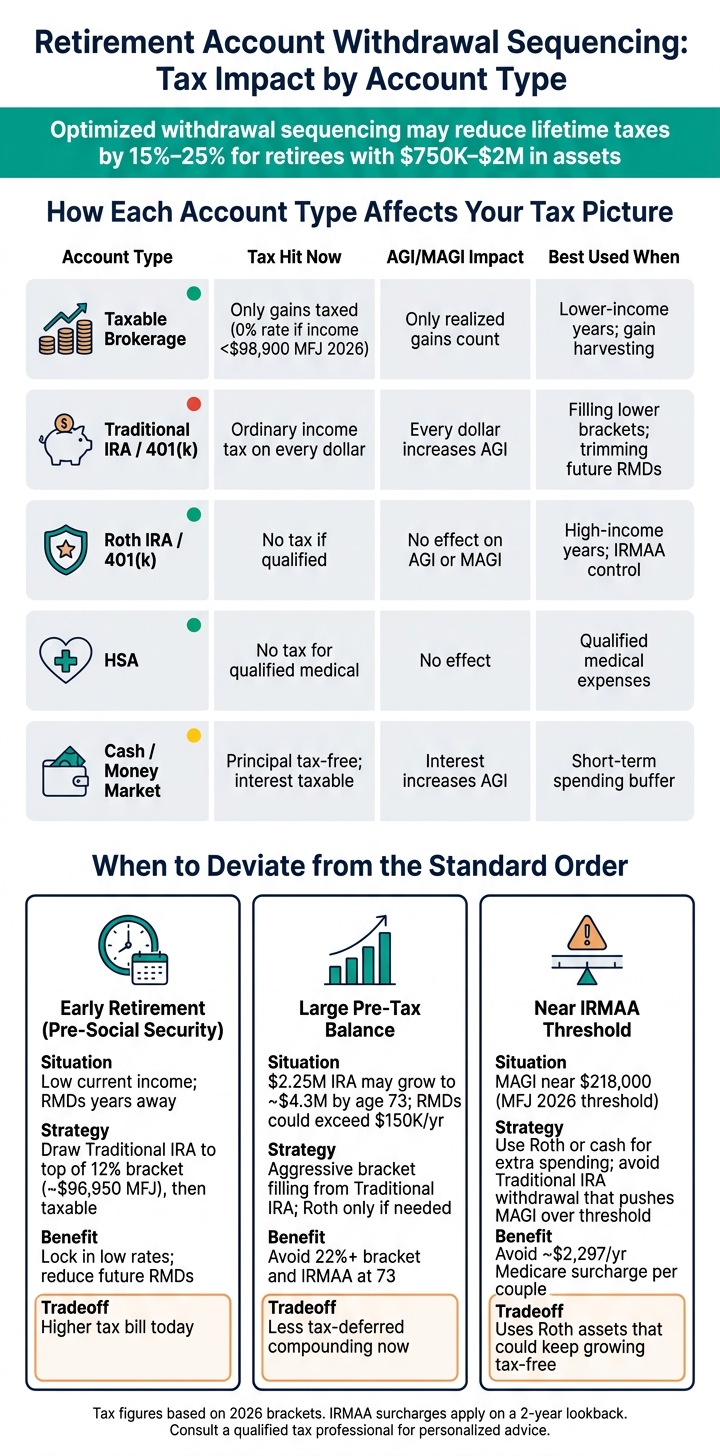

Research cited in the article suggests that a more tailored sequence may cut lifetime taxes by 15% to 25% for some households with $750,000 to $2,000,000 in assets. The tradeoff, though, may be paying more tax now to try to reduce taxes later.

Quick comparison

| Account type | Tax hit now | Effect on AGI/MAGI | Main use case |

|---|---|---|---|

| Taxable brokerage | Tax on realized gains | Only the gain portion counts | Lower-income years, gain harvesting |

| Pre-tax IRA/401(k) | Ordinary income tax | Every dollar counts | Filling lower brackets, trimming future RMDs |

| Roth IRA/401(k) | Usually none if qualified | No direct effect | High-income years, IRMAA control |

| HSA | Usually none for qualified medical | No direct effect | Medical spending |

| Cash/money market | Principal not taxed again; interest may be taxed | Interest may count | Short-term spending buffer |

Bottom line: the “best” withdrawal order may depend on bracket room, capital gains room, future RMD pressure, Social Security timing, and Medicare thresholds. For many retirees, the better question may not be which account comes first, but which mix may fit this year.

Retirement Account Withdrawal Sequencing: Tax Impact by Account Type

The Most Tax-Efficient Retirement Withdrawal Strategy

How each account type affects your withdrawal decision

Each account type may change current taxes, future RMDs, and Medicare income in a different way.

| Account Type | Current tax cost | AGI/MAGI impact | Future Tax/RMD Impact | Primary use first |

|---|---|---|---|---|

| Taxable Brokerage | Capital gains on realized appreciation | Only realized gains count | No RMDs; step-up in basis at death | Early retirement; gain harvesting |

| Traditional IRA/401(k) | Ordinary income tax | Every dollar counts | Subject to RMDs at age 73/75 | Filling lower brackets |

| Roth IRA/401(k) | No tax if qualified | None | No RMDs for original owner | High-spending years; IRMAA control |

| HSA | No tax for qualified medical | None | No RMDs | Qualified medical expenses |

| Cash/Money Market | Principal tax-free; interest taxable | Interest increases AGI | None | Short-term spending buffer |

Taxable brokerage: gains, basis, and flexibility

A taxable brokerage account may give you more room to manage income from year to year. When you sell, only the gain - the gap between what you paid and what you sold for - gets added to AGI and MAGI. Your original cost basis comes back tax-free.

For 2026, married couples filing jointly may realize long-term capital gains at a 0% federal rate if taxable income stays below $98,900. That may make taxable accounts useful in lower-income years. Some people also sell higher-basis lots first, since that may keep the taxable gain smaller.

Taxable assets may also receive a step-up in basis at death.

Traditional IRA and 401(k): filling brackets and managing RMD exposure

Traditional IRA and 401(k) withdrawals work in a much more direct way. Every dollar pulled out counts as ordinary income and increases AGI and MAGI dollar-for-dollar.

That may matter more when pre-tax balances are large. Bigger balances may lead to forced taxable distributions later through RMDs, and smaller withdrawals taken earlier may reduce some of that future pressure.

Roth, cash, and HSA: when to protect flexibility

Qualified Roth withdrawals are tax-free and do not count toward AGI or MAGI. That may make Roth assets useful in years when keeping reported income lower becomes a bigger goal, such as during high-spending years or when someone is trying to limit IRMAA effects.

Cash and money market accounts are simpler on the surface, but they still have a tax angle. The principal has already been taxed, so spending it does not affect AGI. Any interest earned, though, is taxed as ordinary income.

HSAs tend to work best when used for qualified medical expenses. Those withdrawals are tax-free and do not increase AGI.

These are the baseline rules. Once bracket control, IRMAA, or Roth preservation becomes the main focus, the order may change.

When to move away from the standard withdrawal order

Use taxable-first as the default. But in some years, a blended withdrawal mix may make more sense, especially when tax brackets, RMDs, or Medicare costs start to matter. Those tradeoffs often show up in three types of years: low-income years, high-income years, and years when Roth preservation may matter more.

Low-income years: realize gains, fill lower brackets, and consider Roth conversions

In lower-income years, some retirees may pull from a traditional IRA or 401(k) to fill the 10% and 12% brackets, even if they do not need that cash for spending. The same window may also be a good time to realize long-term gains in taxable brokerage accounts if taxable income stays below $98,900 for married couples filing jointly. That may reset cost basis without creating a federal capital gains bill.

Roth conversions may also fit into this window. Moving money during these years may permanently reduce the pre-tax balance that may later be subject to RMDs. Delaying Social Security until age 70 may stretch that lower-income period and may create more years for conversions at lower tax rates.

Mid- and high-income years: avoid bracket jumps and IRMAA surcharges

Once Social Security and RMDs begin, withdrawal sequencing may turn into a bracket-management issue. A large traditional IRA withdrawal on top of those income sources may push taxable income into a higher bracket or trigger a Medicare IRMAA surcharge. Crossing an IRMAA tier may add thousands in annual premiums.

That’s where Roth withdrawals may stand out. They do not increase MAGI, so they may cover spending needs without pushing income into a higher Medicare tier.

The Social Security tax torpedo adds one more wrinkle. When combined income exceeds $44,000 for a married couple, up to 85% of Social Security benefits may become taxable. In that setup, a traditional IRA withdrawal may do more than move you into a higher bracket. It may also cause more Social Security income to be taxed.

When Roth should come before near-term tax savings

If legacy matters, some people spend traditional IRA assets first and preserve Roth assets. Taxable accounts may also receive a step-up in basis at death.

Roth may also make sense in years when a traditional IRA withdrawal would push income over an IRMAA threshold or into a higher bracket. In those cases, Roth may work more like a pressure valve than a default spending source.

Withdrawal sequencing examples by tax situation

These examples show how withdrawal order may change with income, account balances, and timing.

The order that may make sense in one year may look very different in another. In some cases, the goal may be lower tax right now. In others, the focus may be smaller future RMDs or avoiding a jump in Medicare premiums.

Example 1: early retirement before Social Security begins

When current income is low and RMDs are still years away, the sequencing window may be large. Consider a married couple, both age 62, who retired in early 2026. They have $600,000 in a taxable brokerage account, $900,000 split between traditional IRAs, and $200,000 in Roth IRAs. Their annual spending need is $80,000. Social Security may not start until age 70, and RMDs may not begin until age 73.

A taxable-only approach may leave future RMD pressure unchanged. One alternate sequence may be to withdraw enough from the traditional IRA to fill the 12% bracket - up to roughly $96,950 in taxable income for married couples filing jointly in 2026 - and then cover the rest from the taxable account. Any excess may be converted to Roth, which may reduce future RMDs.

They may also harvest gains in taxable at a 0% federal rate if income stays low enough.

Example 2: large traditional IRA balances and future RMD pressure

When a large pre-tax balance is left alone for years, future RMDs may push income into higher brackets. At 6% growth, a $2.25 million IRA may reach roughly $4.3 million by age 73 and may produce $150,000+ in annual RMDs.

One approach some investors use is drawing from the traditional IRA now - using traditional IRA withdrawals first, then Roth only if needed - to fill the 12% bracket each year. Any amount not needed for spending may be converted to Roth, which may reduce the pre-tax balance before RMDs begin. The tradeoff may be a higher tax bill now.

Put simply: paying more tax today may reduce the chance of much larger tax bills later.

Example 3: a spending need near a Medicare IRMAA threshold

Near an IRMAA threshold, the account used for spending may matter more than the spending itself. A married couple, both age 68, has a 2026 MAGI of $205,000 - just below the $218,000 IRMAA threshold for married couples filing jointly. They need an extra $30,000.

If they take that $30,000 from a traditional IRA, their MAGI may rise to $235,000. That may push them into the first IRMAA tier and add roughly $2,297 in Medicare surcharges, with the surcharge appearing two years later. If they instead use a Roth IRA distribution or cash savings, MAGI may stay at $205,000, and no surcharge may be triggered. The Roth distribution does not show up in the IRMAA calculation.

Use the summary below to compare the tax pressure in each case.

| Scenario | Tax Characteristics | Withdrawal Order | Main Benefit | Main Tradeoff |

|---|---|---|---|---|

| Early retirement (pre-SS) | Low current AGI; high future RMD risk | Traditional IRA (to top of 12% bracket), then taxable | May lock in low rates; may reduce future RMDs | Higher tax bill today vs. taxable-first |

| Large pre-tax balance | Growing IRA; facing RMD wall at 73 | Traditional IRA (aggressive bracket filling), Roth only if needed | May reduce the chance of moving into the 22%+ bracket and IRMAA at 73 | Less tax-deferred compounding now |

| Near IRMAA threshold | MAGI close to $218,000 (MFJ) | Roth or cash for extra spending; traditional IRA only up to threshold | May avoid Medicare premium surcharges | Uses Roth assets that might otherwise keep growing tax-free |

The next step is checking all accounts together before deciding which one to tap.

Build a smarter withdrawal plan with full account visibility

The examples above show the tradeoffs. This checklist turns those tradeoffs into a year-by-year decision.

Withdrawal sequencing may sound simple at first. But once your money sits across different account types, the picture may get messy fast. A single view of taxable, pre-tax, Roth, cash, and HSA balances may make it easier to see how one move this year may affect the next one.

The key point: there may not be one fixed best withdrawal order. The mix that may make sense in one year may look different the next year based on income, tax bracket room, unrealized gains, RMD pressure, IRMAA exposure, and HSA-eligible expenses.

Mezzi's read-only consolidated view puts taxable, pre-tax, Roth, cash, and HSA accounts in one place. That may help you spot tax interactions, Roth conversion windows, and bracket issues before taking withdrawals.

For more complex cases, like large Roth conversions, highly appreciated assets, or income near a major threshold, some households may want to confirm the plan with a qualified tax professional.

What to check before each withdrawal year

Before each withdrawal year, it may help to run through a short set of checks:

- Projected AGI and bracket room: How much room may remain before the 22% bracket? For 2026, married couples filing jointly may stay in the 12% bracket up to about $99,200 in taxable income.

- Capital gains room: May you realize long-term gains at 0%? For 2026, married couples filing jointly may qualify up to about $98,900 in taxable income.

- Future RMD exposure: Project your IRA or 401(k) balance at 73. A rough estimate may be current balance × 6% growth ÷ 26.5. If that points to a large RMD, some people draw down earlier.

- IRMAA proximity: Compare MAGI with the 2026 thresholds - $109,000 single, $218,000 married filing jointly. Crossing by $1 may add about $2,297 a year for a couple, with premiums based on a two-year lookback.

- Cash and HSA balances: Keep enough liquid reserves so you may be less likely to sell stocks during a downturn. Some people use the HSA first for qualified medical reimbursements.

That’s why a fixed withdrawal order rarely stays the best fit for long.

Key takeaways: choose the mix each year, not a fixed order

Taxable-first may be a solid default. But blended withdrawals may lower lifetime taxes more than sticking with one fixed order. Research suggests optimized sequencing may cut lifetime taxes by 15% to 25% for many retirees with $750,000 to $2,000,000 in assets.

That judgment often starts with seeing every account in one place.

FAQs

Should I always withdraw from taxable accounts first?

No. A common rule of thumb says people may want to spend taxable accounts first. But that approach may create tax issues later in retirement.

A different approach may be to coordinate withdrawals across account types each year. The goal, for some retirees, may be to smooth out tax brackets, manage MAGI, and reduce future RMD pressure. That approach may also be associated with lower Medicare premiums and less tax on Social Security benefits in some cases.

When does it make sense to use pre-tax accounts before Roth?

Using pre-tax accounts before Roth may make sense in some cases, especially when the goal is to avoid larger tax issues later.

If someone relies only on taxable accounts first, they may leave a large balance in pre-tax accounts. Over time, that may lead to higher future RMDs, higher Medicare IRMAA surcharges, and more Social Security benefits being taxed.

A few common situations come up:

- Filling lower tax brackets in early retirement

- Doing Roth conversions

- Reducing future RMDs

- Using years with sizable deductions to offset the ordinary income from pre-tax withdrawals

The basic idea is pretty simple: taking some pre-tax money earlier may create more room to manage taxes over time, instead of letting those balances build up and potentially create a bigger tax bill later.

How do withdrawals affect RMDs, Social Security taxes, and IRMAA?

Withdrawals from traditional IRAs and 401(k)s are generally taxed as ordinary income, which may increase your adjusted gross income. And if you build up large tax-deferred balances, those accounts may also lead to required minimum distributions, or RMDs, starting at age 73 or 75. That may create a taxable income floor later in life and may push some people into a higher tax bracket.

Higher taxable income may have other ripple effects too. It may make up to 85% of Social Security benefits taxable, and it may trigger Medicare IRMAA surcharges. Planning ahead may help some households manage those thresholds and may reduce lifetime taxes.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.