The short answer: tax-loss harvesting may work for alternative investments, but not all losses are equally usable.

If I boil it down, the article says this:

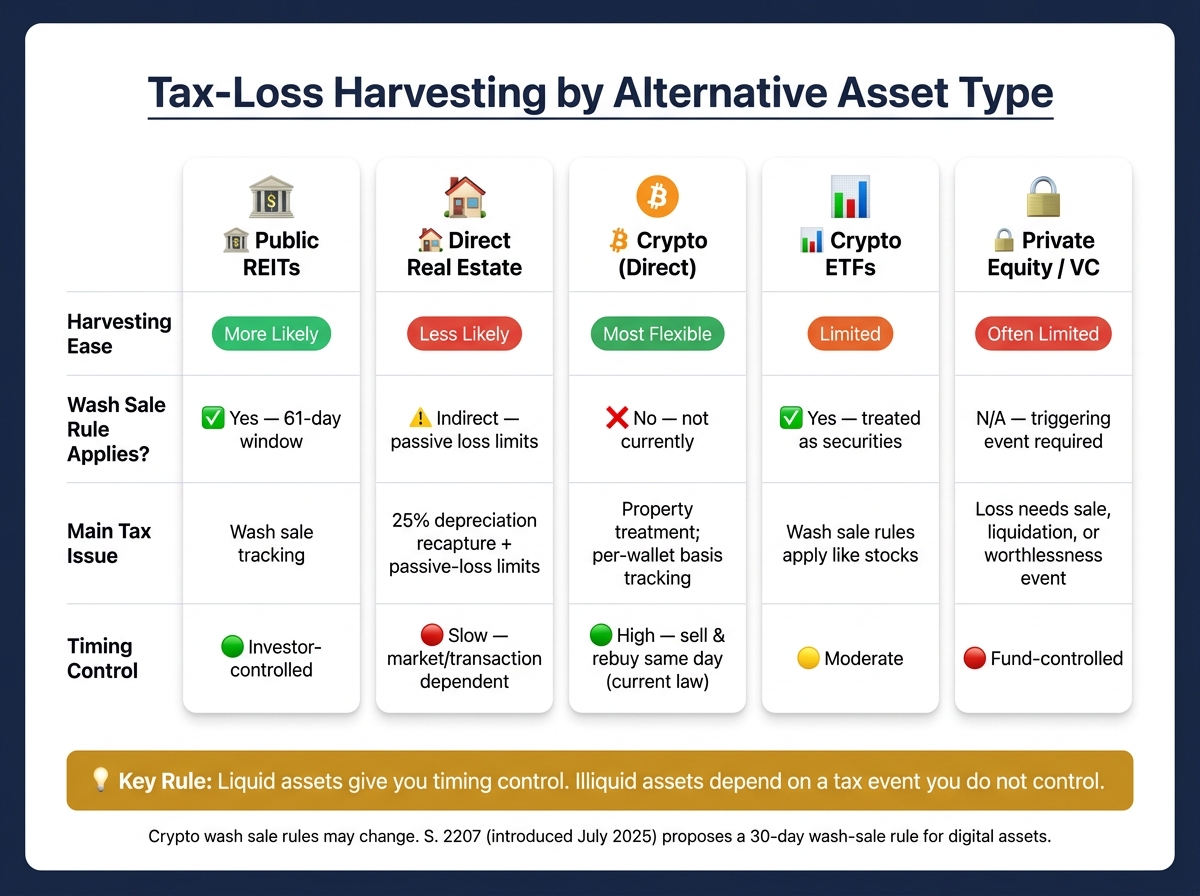

- REITs may be the simplest alt asset to harvest because they trade like securities, and wash sale rules may apply.

- Direct real estate may be harder to use because sales take time, costs may be high, and passive-loss limits or 25% depreciation recapture may change the tax result.

- Crypto may offer the most timing control right now because directly held crypto is treated as property, and the wash sale rule does not currently apply under current federal rules. But recordkeeping may be much harder.

- Private equity and private funds may be the hardest area because a paper loss usually does nothing until there’s a sale, liquidation, abandonment, or worthlessness event.

- Across all of these, lot-level basis, holding period, and account-by-account records may shape whether a loss is usable at all.

If I were summarizing the whole piece in one line, it would be this: liquid assets may give you timing control; illiquid assets may depend on a tax event you do not control.

Quick Comparison

| Asset type | Harvesting may be easy? | Main tax issue | Main practical issue |

|---|---|---|---|

| Public REITs | More likely | Wash sale rules may apply | Need lot selection and repurchase tracking |

| Direct real estate | Less likely | Passive-loss limits and recapture may affect use | Selling may take time and cost money |

| Directly held crypto | More likely under current law | Property treatment; no current wash sale rule | Wallet-by-wallet basis tracking |

| Crypto ETFs | Less likely for same-day rebuy | Wash sale rules may apply | May look like stock harvesting |

| Private equity / VC funds | Often limited | Loss usually needs a triggering event | Timing may sit with the fund, not the investor |

A few rules sit underneath everything:

- Harvesting generally applies only in taxable accounts

- Short-term and long-term losses may offset gains by character first

- Unused capital losses may carry forward

- Specific lot ID may change the size and type of loss

- Trades in a spouse’s account or retirement account may still create wash sale issues for taxable holdings

That’s the whole article in plain English: REITs and direct crypto may offer the cleanest paths, direct property and PE may be much messier, and recordkeeping may decide whether the loss holds up on a return.

Tax-Loss Harvesting for Alternative Investments: Quick Comparison Guide

Wash Sale Rule Explained: Tax Loss Harvesting for Stocks and Crypto by Katie St Ores CFP

Real estate: REIT losses are harvestable; direct property losses are harder to use

The main split here is between publicly traded REITs and direct property. What matters for taxes isn't only whether an asset is down. It’s also whether the loss may be realized in a clean, usable way. Publicly traded REITs are generally simple to sell and report. Direct property tends to be illiquid, slower to close, and tougher to use for tax-loss harvesting.

How to harvest losses in publicly traded REITs

Publicly traded REITs are classified as securities under IRC §165(g), so standard wash sale rules may apply. If a taxable REIT position trades below your basis, some investors sell the position and use the loss to offset capital gains, subject to those wash sale rules.

Why direct real estate rarely works as a harvesting tool

Direct property usually doesn’t work as neatly for harvesting. Sales may take time, transaction costs may be high, and passive loss rules may limit how a loss gets used. If the property has been depreciated, a sale may also trigger depreciation recapture, taxed at 25% on the portion of the gain tied to prior depreciation.

There is one more practical exception. A partial disposition election may allow recognition of the remaining basis of a replaced component - like a roof or HVAC system - as a loss.

Unlike real estate, crypto usually gives you more control over timing - but that may create recordkeeping risk.

Crypto: the most flexible harvesting option, with record-keeping risk

Crypto may give investors more control over when they realize losses. But that extra room may come with more paperwork.

For tax purposes, crypto is treated as property, not a security. That means losses on directly held crypto are capital losses. Those losses may offset gains elsewhere, and the wash-sale rule does not currently apply. Under current rules, someone may sell Bitcoin at a loss and buy it back right away. That same move would not work with a stock or a publicly traded REIT.

The tax comparison with stocks and other securities mostly comes down to two things:

| Feature | Crypto (Directly Held) | Stocks & Securities / REITs |

|---|---|---|

| Wash Sale Rule (§1091) | Does not apply | Applies; 61-day disallowance window |

| Record-Keeping Burden | High; per-wallet basis required | Moderate; broker-handled via 1099-B |

How to realize crypto losses without creating tax-reporting problems

Since Jan. 1, 2025, IRS Rev. Proc. 2024-28 has required digital-asset basis tracking by wallet or account, rather than using one pooled basis. Within that setup, specific identification may produce the largest loss. Instead of falling back to FIFO, you identify the lots being sold - often the highest-basis lots - which may increase the loss realized.

To use specific identification, you need records made at the time of the transaction. That usually means keeping:

- acquisition date and time

- sale date

- quantity

- proceeds

- fees

- transaction hashes for any self-custody wallets

Starting with 2026 transactions, exchanges must report proceeds and basis on Form 1099-DA. If assets are held in self-custody, those records may still remain your job. Some investors use harvested crypto losses against short-term gains first, since short-term gains may be taxed at ordinary income rates.

That edge depends on current law, which is why rule changes matter.

What to watch as crypto wash sale rules change

S. 2207, the Digital Asset Tax Relief Act introduced in July 2025, proposes a 30-day wash-sale rule for digital assets, along with a $300 de minimis exemption. Crypto ETFs are already classified as securities, so standard wash-sale rules apply to them. Tokenized products or derivatives may also be treated as securities instead of property, which may trigger wash-sale rules even under current law.

Unlike crypto, private equity usually ties the loss to fund timing, not investor choice.

Private equity and illiquid funds: losses matter, but timing is mostly out of your hands

Private equity may be the toughest alternative when it comes to tax-loss harvesting because the timing usually isn't yours to control. Unlike crypto, where an investor may choose when to sell, private equity usually works differently. Private funds trade infrequently, and reported values may update only from time to time. Under Treas. Reg. §1.165-1(d), a loss must be tied to a sale, liquidation, abandonment, or worthlessness event. If the loss is still unrealized, it generally may not be usable for tax purposes until something concrete happens.

There’s another catch. You usually may not separate gains and losses inside one fund interest. When you invest in a PE or VC fund, you generally hold one partnership interest, so losses from the fund’s underlying holdings may show up only as one tax event. K-1s also often arrive late, sometimes as late as September, which may push investors to file extensions. So even if the marked value drops, that alone may do nothing for tax purposes until the fund exits, liquidates, or becomes worthless.

When a private investment loss becomes usable

The tax issue usually isn't whether the investment is down in value. It’s whether a clear triggering event has taken place.

A private investment loss may become deductible when a real transaction or confirmed event occurs. Common triggers may include:

- A secondary market sale

- A fund wind-down

- A worthlessness determination

PeerStreet offers a useful example. After filing for Chapter 11 in June 2023, its bankruptcy plan became effective in early May 2024, which may have given investors with confirmed claims an identifiable event for recognizing losses on their 2024 tax returns.

For partnership or LLC interests, one of the clearest signs may be a final Schedule K-1 with the "Final" box checked and a zero ending capital account. For positions that are genuinely worthless, some investors may be able to claim an abandonment loss under IRC §165, but only if the asset has no current liquidating value and no reasonable prospect of future value. If the position still exists but appears worthless, selling the stake to a third party for $1 may create a clean, documented transaction for tax purposes.

Secondary market platforms like Forge and Nasdaq Private Market have made exits possible, but thin markets may still force discounts. And if the investment qualifies as Section 1244 stock, losses may be deductible as ordinary losses up to $100,000 for joint filers. That treatment may be more useful than capital-loss treatment for some investors, given the $3,000 annual cap on capital losses against ordinary income.

Build a cross-account harvesting workflow with Mezzi

Once you know where harvesting may work, the next step may be pulling every taxable account into one view. The main issue is scattered records across taxable, crypto, and alternative accounts. When your taxable brokerage, crypto exchange, and alternative holdings each sit behind a different login, you may miss losses you might use later. You may also create wash-sale mistakes without meaning to. Mezzi links those accounts with read-only access so you may get a household-level view.

What data you need to make good harvesting decisions

This workflow may help you apply the rules above across every account. The goal isn't just finding losses. It's also avoiding disallowed repurchases across accounts.

| Step | Required Inputs | Output |

|---|---|---|

| 1. Connect Accounts | Read-only access to taxable, crypto, and alternative-investment accounts (including a spouse's) | Unified household dashboard |

| 2. Inventory Losses | Cost basis by lot, current market value | Unrealized losses ranked by size and holding period |

| 3. Review Tax Effect and Conflicts | Realized gains year to date, tax bracket, 61-day transaction history across all linked accounts | Projected tax savings; alert on substantially identical replacements before you trade |

| 4. Execute & Record | Selected lots, replacement assets, account access | Loss reported on Form 8949; updated basis records |

Retirement accounts don't produce harvestable losses, but trades inside them may create wash-sale risk for a taxable account.

Starting in 2026, centralized crypto brokers must report gross proceeds and basis on Form 1099-DA, so mismatches may draw IRS scrutiny. Mezzi is designed to help reconcile broker-reported basis with your own lot records.

After you identify a loss, the workflow may be pretty simple: trade, record, and monitor the repurchase window. Mezzi tracks unrealized losses year-round, checks wash-sale risk across linked accounts, and tracks the repurchase window after you trade. If a mid-year drawdown hits, you may see the opportunity ranked by size, with wash-sale risk already checked across connected accounts.

Conclusion: Start with liquid losses, then use the full household picture

Put simply, it may make sense to start with liquid losses and use a household view to spot the ones that may actually be usable. REITs may be the easiest liquid starting point, crypto may give you the most timing control, and direct real estate or private equity usually depend on a triggering event. The value may come from seeing every taxable account together, ranking losses by size and holding period, and acting with clean records.

This content is for informational purposes only and does not constitute tax or investment advice. Consult a qualified tax professional before making decisions based on your specific situation.

FAQs

Which alternative assets are easiest for tax-loss harvesting?

Cryptocurrency may be one of the easier alternative assets to use for tax-loss harvesting because it may be treated as property rather than a security. In practice, that may mean it is not currently subject to the IRC Section 1091 wash-sale rule. So some investors may sell at a loss and buy back right away while keeping market exposure.

Private equity and direct real estate may be much harder to use this way. Illiquidity, limited pricing, and more complex tax rules may all make the process tougher.

Can I rebuy crypto right after selling at a loss?

Yes. As of 2026, you may be able to sell cryptocurrency at a loss and buy it back right away because the IRS generally treats crypto as property, not a security. That distinction matters: the 30-day wash sale rule usually applies to stocks and crypto ETFs, but it generally may not apply to spot digital assets.

That said, there’s still some gray area. Some tax practitioners have warned that the IRS may challenge instant repurchases under the Economic Substance Doctrine. To lower that risk, some people wait a short period before buying back in, or they keep notes that explain the reason for the trade.

When is a private equity loss deductible?

A private equity loss may be deductible only when it’s realized through a closed, completed transaction tied to an identifiable event. A drop in value or insolvency by itself may not be enough.

For a fund interest, the loss may be recognized in the year you receive a final Schedule K-1 marked final with a zero ending capital account. If the investment becomes wholly worthless with no reasonable prospect of future value, an ordinary loss under Section 165 may apply.

Disclosures:

- This content is for informational purposes only and does not constitute tax or investment advice. Consult a qualified tax professional before making decisions based on your specific situation.

- Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.