Should you open a Trump account?

In this week's The Boost, we cover "Trump accounts", a new type of savings account for children.

The IRS says 4 million children have been signed up for the new "Trump accounts" — but only 1 million families actually claimed the $1,000 government contribution. Three million left it on the table, potentially because they missed a single checkbox on the form.

If you have kids, grandkids, nieces, or nephews, this is worth 5 minutes of your time.

You can also read The Boost on X and LinkedIn.

What are Trump accounts?

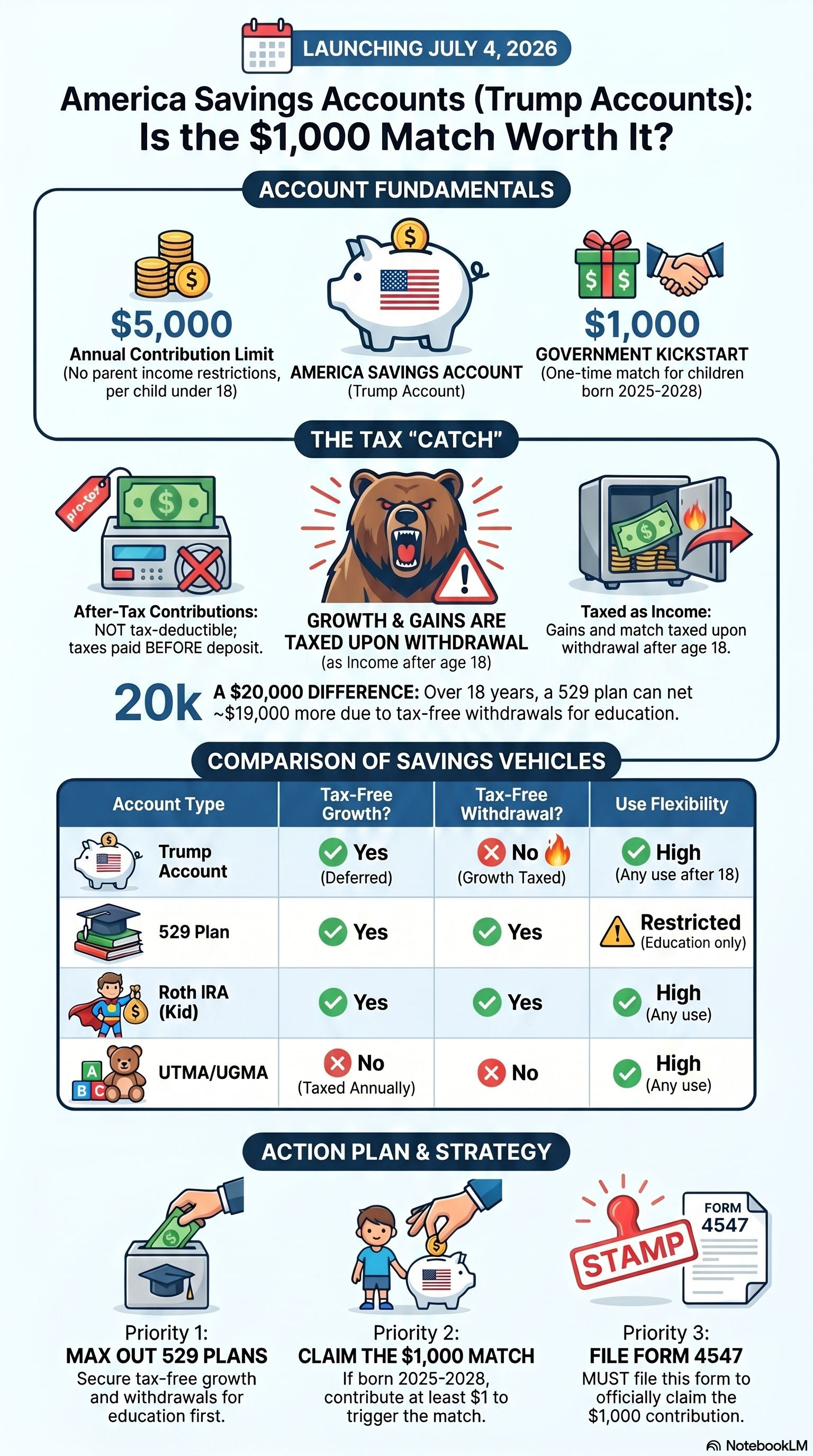

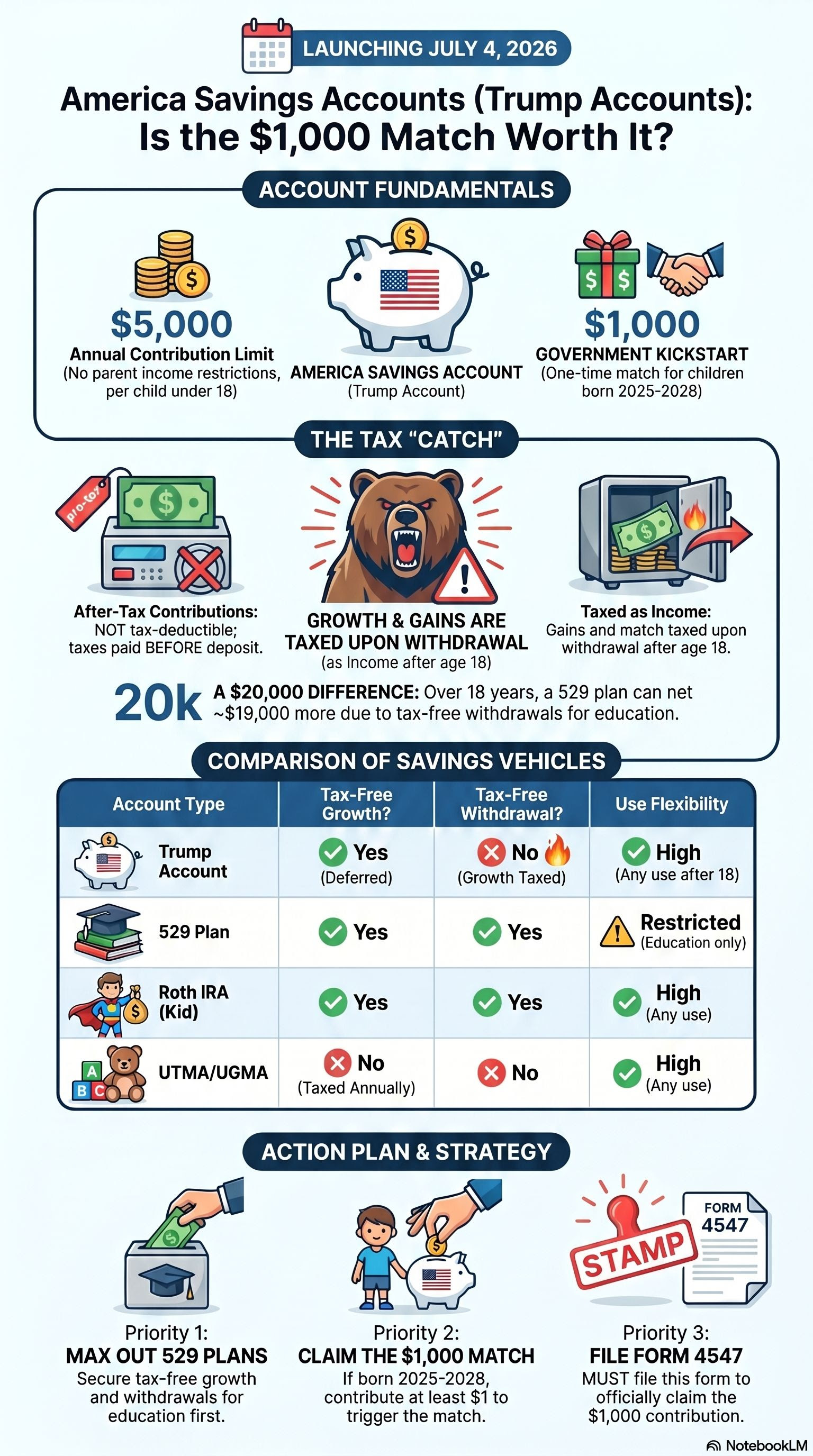

Trump accounts are new tax-advantaged savings accounts for children, named after Section 530A of the tax code (similar to how 529 plans get their name). They were created by the One Big Beautiful Bill Act and you can begin depositing in the accounts on July 4, 2026.

Any child under 18 can have one. You can contribute up to $5,000/year per child. Family members and employers can contribute too, but everything counts toward that $5,000 cap.

Kids born 2025–2028 get a bonus: a one-time $1,000 government contribution — but only if you file Form 4547 and check the box in Part III, Line 7. You can file it with your tax return or at trumpaccounts.gov.

Funds must be invested in low-cost U.S. equity index funds. The money grows tax-deferred and can't be touched until age 18.

The catch: growth is taxed as ordinary income at withdrawal. And if your child withdraws before age 59½, there's an additional 10% early withdrawal penalty on the taxable portion unless the funds are used for certain eligible expenses like education. That means a child accessing the money at 18 pays income taxes plus a 10% penalty on all growth.

Trump accounts vs. 529s: the tax math

Say you contribute $5,000/year from birth to age 18, plus the $1,000 government contribution. At 7% annual growth, that's ~$181,000 at age 18.

Trump account used for college: $90,000 in contributions comes out tax-free. The remaining ~$91,000 (growth + government $1,000) is taxed as ordinary income — but the 10% early withdrawal penalty is waived for qualified higher education. At a 22% bracket: ~$20,000 in taxes. Net: ~$161,000.

Trump account used for anything else at 18: Same income tax plus the 10% penalty (~$9,100). Net: ~$152,000.

529 plan, same contributions: $180,000 at age 18 — and if used for education, all withdrawals are completely tax-free. Net: $180,000.

Even for education, the 529 wins by ~$19,000 — and that's before state tax deductions on 529 contributions widen the gap further. For non-education use, the gap jumps to ~$28,000. 529s also cover K-12 expenses in most states (up to $20,000/year under the new law) — Trump accounts can't be touched until 18.

The general framework is clear: 529s beat Trump accounts for education. But whether that's the right move for your family depends on variables a newsletter can't cover — your tax bracket, your state's 529 rules, what accounts you already have, and how much you're contributing elsewhere.

Evaluate a 529 vs. Trump account

When Trump accounts make sense

Grab the free $1,000 — and check if your employer will double it. If your child was born 2025–2028, file Form 4547 (details above). Even if you never contribute a dollar of your own, the government's $1,000 grows to ~$3,400 by age 18. The growth gets taxed (plus the 10% penalty before 59½), but it's meaningful money for zero effort. Worth noting: companies like Schwab, BlackRock, Robinhood, SoFi, and others are matching the government's $1,000 for employees' children — check with your HR team.

The Roth conversion play. If your child has earned income at 18, they could withdraw the Trump account balance, pay taxes at a low bracket, and funnel the after-tax proceeds into a Roth IRA — where it grows tax-free forever. For the government's $1,000: ~$3,400 at 18, minus ~$750 in taxes and penalties, leaves ~$2,650 going into a Roth. At 7% for another 40 years, that's roughly $40,000 in tax-free retirement savings from a single government contribution.

Overflow savings. If you've already maxed out 529 plans ($300K–$500K lifetime caps in most states) and want additional tax-deferred savings, Trump accounts are an option. But even for flexible, non-education use, a taxable brokerage may be more efficient — capital gains rates are typically lower than the ordinary income rates Trump accounts charge.

Priority order: 529 plans first → Roth IRAs (if your child has earned income) → Trump accounts for the government match or overflow.

What Mezzi Members are doing

A Mezzi user asked this week: "Should I open a Trump account?" Mezzi pulled their actual portfolio — custodial UTMA, two 529s, $6K in annual education savings — and ran a side-by-side comparison for $5,000/year over 18 years:

- 529 (for education): $181,895 after taxes

- Taxable brokerage: $168,111 after taxes

- Trump account (for education): $163,042 after taxes (penalty waived for college — but add ~$9K more in penalties for non-education use)

- 529 (non-qualified use): $161,678 after taxes

The answer was specific to their situation, their accounts, their goals. Yours might be different — especially if you're weighing a Trump account against a UTMA you already have, or wondering if the Roth conversion play makes sense given your child's projected income.

Not sure which accounts to prioritize for your kids? Mezzi can run this analysis for you →

How should you use a Trump account?

The bottom line

If your child was born 2025–2028, don't leave the free $1,000 on the table — file Form 4547 and check the Part III, Line 7 box (details above).

For any child: Trump accounts are a decent overflow vehicle, but 529 plans and Roth IRAs should come first. The tax-free growth from a 529 is worth far more than the tax-deferred growth from a Trump account.

And if you want to know exactly how much more — for your specific situation — that's what Mezzi does.

IMPORTANT DISCLOSURES

This content is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.Savings and performance examples are hypothetical and for illustrative purposes only. Actual results will vary based on individual circumstances, portfolio composition, market conditions, and fees.

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.