Miss Day 45 or Day 180, and a 1031 exchange may fail. If that happens, a deferred gain may become taxable in the year of sale, and for a $1,000,000 gain, the tax cost may land somewhere around $250,000 to $330,000, depending on the facts.

Here’s the short version:

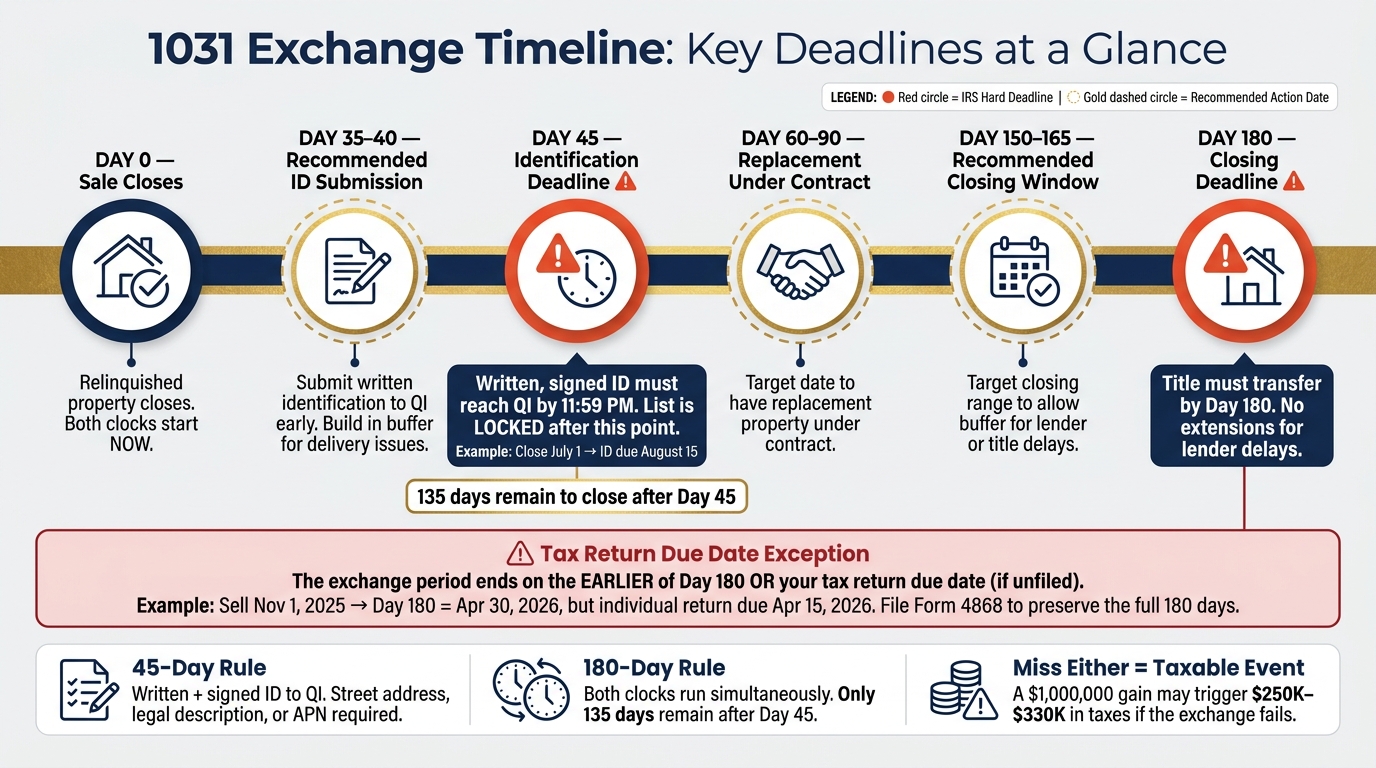

- Day 0 starts when the sold property closes and title transfers.

- Day 45 is the last day to identify replacement property in writing.

- Day 180 is the last day to close on an identified property.

- These two periods run at the same time, not one after the other.

- The exchange period may end before Day 180 if a tax return due date arrives first and no extension is in place.

- Weekends and holidays do not move the deadlines.

- A late notice, vague property description, failed financing, or wrong QI setup may cause the exchange to fall apart.

If I closed on July 1, 2026, Day 45 may fall on August 15, 2026. From there, only about 135 days may remain to finish the purchase. That’s why many investors start tracking both dates on the day the first closing happens.

| Deadline | What it covers | Basic rule |

|---|---|---|

| 45 days | Identification | Written, signed notice to the QI by midnight |

| 180 days | Closing | Title to replacement property must transfer by the deadline |

| Earlier tax filing date | Shortened exchange period | May cut off the 180-day period if no extension is filed |

This guide breaks down the timeline, the IRS identification rules, the tax return cutoff, common failure points, and a simple checklist some investors may use to stay on track.

1031 Exchange Timeline: Day 0 to Day 180 Visual Guide

The 1031 Exchange Timeline: An Easy-to-follow Guide

The 45-day identification rule

If you closed on July 1, 2026, Day 45 falls on August 15, 2026. That deadline does not move. So you have one hard date to hit: Day 45.

What counts as valid identification

Your identification has to be written, signed, and delivered to your qualified intermediary (QI) before 11:59 p.m. on Day 45.

You’ll also need to identify the property with a clear description, such as:

- A street address

- A legal description

- An assessor's parcel number (APN)

Vague descriptions don’t count.

There’s also a common timing issue here. Some exchangers send the notice late in the day and run into the QI’s delivery cutoff or time zone mismatch. To avoid that problem, some people submit early and ask for written confirmation that the QI received it.

The notice also needs to fit one of the IRS identification methods below.

The three-property, 200 percent, and 95 percent rules

Once your notice is valid, the IRS may let you use one of three identification methods:

| Rule Name | Property Limit | Value Limit | Main Compliance Risk |

|---|---|---|---|

| Three-Property Rule | Up to 3 | None | Identifying a 4th property may invalidate the entire list |

| 200% Rule | Unlimited | Total FMV ≤ 200% of relinquished property's value | Exceeding the value cap may invalidate the entire list |

| 95% Exception | Unlimited | None | Failing to acquire at least 95% of total identified value may cause the exchange to fail |

Changing your identification before day 45

You may revise your identification list as many times as needed during the 45-day window, but every change must be in writing and signed.

After midnight on Day 45, the list is locked. At that point, you may not add, swap, or revoke any property.

After identification, the clock keeps running toward the closing deadline. Next comes the 180-day closing deadline, and it runs on the same timeline.

The 180-day closing rule and how it overlaps with day 45

Why the two deadlines run at the same time

Once your Day 45 list is locked, the next deadline is the closing. The key detail: the 180-day deadline starts on the same day as the 45-day identification window. These two clocks run at the same time, not back-to-back.

So when Day 45 ends, you may have 135 days left to close on one of the properties already identified. The replacement property must come from that Day 45 list.

How the tax return due date can shorten your exchange period

A closing that looks on time may still fail if your tax filing deadline comes first. The exchange period ends on the earlier of Day 180 or your tax return due date, including extensions.

Here’s a simple example. If an individual investor sells a property on November 1, 2025, Day 180 lands on April 30, 2026. But the individual tax return is due on April 15, 2026 - 15 days sooner. If Form 4868 is not filed for an extension, April 15 may become the deadline to close.

Filing Form 4868 before filing the return may preserve the full 180 days. There’s another catch here: if you file your tax return before the exchange closes, the exchange period ends on that filing date, even if the 180 days have not passed yet.

Partial reinvestment, debt reduction, and boot

Closing on time may not be enough by itself. If you keep part of the cash proceeds or replace less debt, the gap may be treated as taxable boot. Cash kept and debt not replaced may both be taxed at capital gains rates, along with any applicable depreciation recapture.

That’s why some investors try to confirm financing before closing. Miss either deadline, and the exchange may fail.

What happens if you miss a deadline

Missing day 45: no valid replacement-property identification

If a replacement property isn’t properly identified by midnight on Day 45, the exchange fails, and the full gain may become taxable in the year of sale.

Here’s how that may play out. An investor sells a property and spends the first few weeks looking at options. They find the right replacement on Day 50 - just five days late. But because no signed written identification was delivered to the QI by midnight on Day 45, the exchange may already have failed.

Missing day 180: identified but not closed

Title must transfer by Day 180. Common delays - like lender underwriting, appraisal issues, inspection findings, title defects, or seller problems - do not extend that deadline.

So if a lender needs one more week on Day 175, the exchange may still fail if title hasn’t transferred by midnight on Day 180. In that case, the sale may become fully taxable. The only statutory relief for a missed deadline involves a federally declared disaster, which may postpone deadlines under certain IRS notices.

That’s why many investors track both dates starting on closing day.

Common mistakes that cause exchanges to fail

These are the errors that most often turn what looked like a valid exchange into a taxable sale.

One common mistake is waiting until after closing to bring in a QI. The QI assignment language needs to appear in the sale contract before closing, not after.

Two other problems show up all the time. One is assuming the deadlines use business days. They don’t. Day 45 and Day 180 are calendar days, and the IRS does not shift the deadline if it lands on a weekend or holiday. The other is using vague descriptions like “a property in Dallas” instead of a street address or legal description. If the identification is ambiguous, the IRS may treat it as no identification at all.

| Missed Requirement | Typical Cause | Result | Preventive Step |

|---|---|---|---|

| Day 45 Identification | Starting the search after closing; identifying only one property that falls through | Entire gain may become taxable in the year of sale; depreciation recapture may be triggered | Start searching before the relinquished property closes; identify multiple properties |

| Day 180 Closing | Lender delays; appraisal issues; seller backing out | Exchange may be invalidated; the sale may become fully taxable | Line up financing before the relinquished property closes |

| Tax Return Due Date | Late-year sale without filing a tax extension | The 180-day window may be shortened | File Form 4868 for individuals or Form 7004 for partnerships |

| QI Validity | Using a personal CPA or attorney as the intermediary; proceeds touching the investor’s account | Disqualification due to “disqualified person” status or constructive receipt of funds | Use an independent QI, verify the assignment language before closing, and make sure proceeds wire directly from escrow to the QI’s segregated account |

Once those risks are on the table, the next move may be pretty simple: use a checklist from Day 1 to track both deadlines.

A simple process to stay on schedule

A 1031 timeline checklist from sale closing to replacement closing

Treat both deadlines as fixed calendar dates. It may make sense to use these target dates to build some buffer into each step.

| Milestone | Recommended Timing | IRS Hard Deadline |

|---|---|---|

| Engage a Qualified Intermediary (QI) | 14–30 days before sale closing | Before Day 0 |

| Relinquished Property Closes | Day 0 | Day 0 (closing date) |

| Deliver written identification to QI | Day 35–40 | Day 45, midnight |

| Replacement Property Under Contract | Day 60–90 | - |

| Replacement Property Closes | Day 150–165 | Day 180, or earlier tax return due date if not extended |

On Day 0, calculate both deadlines right away. A date calculator or spreadsheet may help you lock in both dates on Day 0. Then set calendar reminders two weeks before each one.

Submitting identification by Day 35–40 may leave room for delivery issues. A Day 150–165 closing target may also give you some cushion if a lender or title issue slows things down.

Once the calendar is mapped out, the next piece may be tracking the tax impact across your portfolio.

Where Mezzi fits into the planning process

Mezzi gives read-only, cross-account visibility into the tax impact. If the exchange may be at risk, Mezzi may help you see the tax impact across your accounts and spot offsetting opportunities elsewhere in your portfolio. Mezzi doesn't execute transactions or provide individualized tax advice - that's the job of your QI and CPA. It gives you the visibility needed to make faster tax decisions with your QI and CPA.

With the dates set, the remaining step may be execution.

Conclusion: The 2 dates you cannot miss

The entire 1031 exchange timeline comes down to two numbers: Day 45 and Day 180. Both are measured from Day 0 and run at the same time, which may leave only 135 days to close after the identification deadline passes. Miss either deadline - or let the tax return due date go unextended on a late-year sale - and the exchange fails, even if every other step was done correctly.

FAQs

Can I identify backup properties?

Yes. Naming backup properties is allowed, and many investors use that approach to help protect a 1031 exchange.

The IRS allows three main identification methods, and you only need to close on one of the properties you identify.

The most common method is the Three-Property Rule. It lets you identify up to three properties, no matter their value. That may give you a cushion if your first-choice deal falls through before the 180-day deadline.

What if Day 45 or Day 180 falls on a weekend?

The 1031 exchange deadlines are measured in calendar days, not business days.

That detail may sound small, but it may affect timing in a big way. If Day 45 or Day 180 falls on a Saturday, Sunday, or federal holiday, the deadline does not move to the next business day.

You would still need to complete your identification or closing by midnight on the actual calendar date. There are no weekend or holiday grace periods, so planning ahead may matter.

Does filing my tax return early end the exchange?

No. Filing your tax return early does not end the exchange on its own, but it may shorten your 180-day window.

The exchange must be completed by whichever comes first:

- 180 days after the sale

- Your tax return filing deadline for that year

Filing an extension with Form 4868 before the original deadline may preserve the full 180 days.Disclosures:

- This content is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.

- Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.