A DST may be a passive way to complete a 1031 exchange when time is short - but it also may mean high fees, low liquidity, and no control.

If I were sizing up a Delaware Statutory Trust, I’d boil it down like this:

- A DST may let me place 1031 exchange proceeds into fractional ownership of real estate

- It may work within the 45-day identification and 180-day closing deadlines

- It may offer passive income, often with projected yields in the 4% to 6.5% range

- It may require me to accept a 5- to 10-year hold

- It may come with up-front fees of 10% to 18% of equity

- It may limit refinancing, new leases, new capital, and major property changes

- It may fit investors who want less landlord work, but not those who want control or easy access to cash

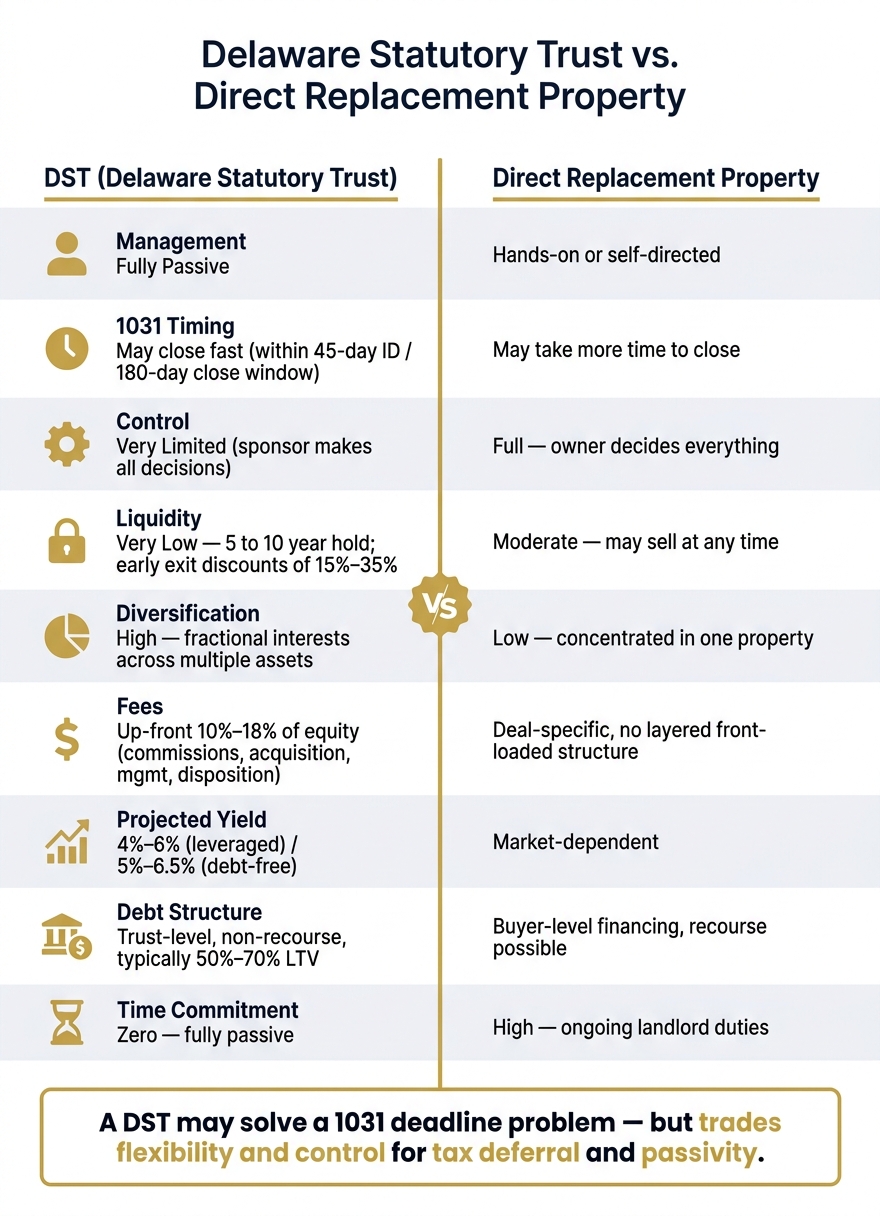

Put another way: a DST may solve a 1031 deadline problem, but it may also trade flexibility for tax deferral and passivity.

A few points stand out:

- 1031 fit: Properly structured DST interests may qualify as like-kind replacement property under IRS guidance.

- Debt matching: If DST debt is lower than the debt from the sold property, the gap may create taxable boot.

- Access to cash: Early exits may be hard, and resale discounts may run 15% to 35%.

- Investor rules: Many DSTs are private placements, so accredited investor standards may apply.

- Main tradeoff: Less work may also mean less control.

DST vs. Direct Replacement Property: Key Factors Compared

DST Basics Explained: A Smart 1031 Exchange Strategy for Investors

Quick Comparison

| Factor | DST | Direct Replacement Property |

|---|---|---|

| Management | Passive | Hands-on or self-directed |

| 1031 timing | May close fast | May take more time |

| Control | Very limited | High |

| Liquidity | Very low | Higher relative flexibility |

| Diversification | May spread money across assets | Often concentrated in one deal |

| Debt structure | Usually trust-level, often non-recourse | Buyer-level financing |

| Fees | Often layered and front-loaded | Deal-specific |

| Hold period | Often 5–10 years | Owner decides when to sell |

If I wanted one simple takeaway, it would be this: a DST may be less about return chasing and more about exchange completion, passive ownership, and giving up control.

1031 rules and DST eligibility

The 1031 timeline, like-kind standard, and debt replacement

Once the exchange clock starts, the next step may be confirming that the DST fits IRS rules. Section 1031 requires both the sold property and the replacement property to be held for investment or business use. A properly structured DST interest may qualify as like-kind real estate for Section 1031.

The timeline is tight:

- You may have 45 days to identify replacement property in writing.

- You may have 180 days to close.

Missing either deadline may make the exchange taxable.

To defer taxes in full, you generally may need to reinvest in replacement property with equal or greater value and replace the debt tied to the property you sold. With a DST, debt replacement happens at the trust level, and each investor gets a pro rata share of that debt based on their fractional interest. That debt is usually non-recourse, which means you aren't personally liable for the loan and may not need to qualify with a lender.

If the DST's debt is lower than your old mortgage, the difference may be taxable boot. Most DST financing falls in the 50% to 70% LTV range, so matching your prior debt ratio may require a close review of the specific offering with a CPA before you identify it.

The DST restrictions that keep it 1031-eligible

DSTs stay 1031-eligible only if they follow seven strict operating limits. The goal is to preserve tax status by limiting active management.

| Restriction | What It Means in Practice |

|---|---|

| No new capital | The trust can't accept more contributions after the offering closes |

| No new borrowing | The trustee can't borrow new funds or refinance existing debt, except in tenant bankruptcy or insolvency situations |

| No reinvestment | Sale proceeds must be distributed to investors instead of being reinvested by the trust |

| Limited capital expenditures | Only routine repairs, minor non-structural improvements, or legally required improvements are allowed |

| No new leases | The trustee can't enter new leases or renegotiate existing ones; a "Master Tenant" structure is usually used instead |

| Reserves only in safe instruments | Cash reserves must stay in short-term, liquid, non-speculative holdings |

| Mandatory distributions | Available cash, minus reasonable reserves, must be distributed to investors pro rata |

In plain English, that may mean you don't get a vote on property decisions, you may not trigger a refinance if rates fall, and you may not fund major renovations. It's a passive, buy-and-hold setup with little room to change course during the hold period.

Some DSTs include a Springing LLC clause that may convert the trust in an emergency, but that conversion usually ends 1031 deferral.

Investor eligibility and accredited investor standards

DST offerings are private placements, so investors usually need to meet accredited investor standards under SEC rules. That may mean either:

- Earning more than $200,000 per year individually, or $300,000 jointly with a spouse, for the past two years, with a reasonable expectation of the same going forward

- Having net worth above $1,000,000, excluding a primary residence

Trusts, LLCs, and partnerships may qualify under a separate asset-based standard. Minimum investment amounts generally range from $25,000 to $100,000, depending on the offering.

Once eligibility is clear, the next question may be how the trust actually owns and manages the property.

How DST ownership works in practice

Beneficial ownership, sponsor control, and income allocation

Once a DST qualifies for 1031 treatment, the next issue is how ownership tends to work day to day.

You own a fractional beneficial interest in a trust that holds title to the property. You do not own a deed to the property itself. Income, expenses, and debt generally pass through to you on a pro rata basis.

The sponsor sets up and manages the program. In many cases, that means the sponsor handles property management, asset strategy, and the timing of an eventual sale. A separate Delaware trustee takes care of administrative duties, such as holding title and keeping the structure in line with compliance rules.

Because DSTs face limits on active management, many of them use a sponsor-controlled master tenant for day-to-day operations and subleasing.

What investors give up compared with direct ownership

Passivity may be the main tradeoff.

Compared with direct ownership, you may give up control over leasing, renovations, refinancing, and most other operating decisions. In return, tax reporting may be simpler: at tax time, you may receive a Grantor Letter that shows your share of income, depreciation, and mortgage interest deductions.

That pass-through structure may shape cash flow, tax reporting, and liquidity limits.

Cash flow, fees, liquidity, and risk

Income potential and how distributions are taxed

When you own a fractional interest in a DST, cash flow and tax reporting generally pass through on a pro rata basis. Most DSTs pay distributions monthly or quarterly, using the net operating income the property may generate.

As of 2026, projected yields typically fall in these ranges: 4% to 6% annually for leveraged DSTs and 5% to 6.5% for debt-free DSTs. Leverage may improve appreciation potential in some cases, but it also adds debt service, which may reduce the amount of cash distributed to investors.

Headline yield only tells part of the story. A higher yield tied to short-term leases may carry a very different risk profile than a moderate yield tied to a long-term credit-tenant lease.

For tax reporting, investors typically receive a grantor letter or K-1 that shows their pro rata share of income and expenses. Depreciation may offset part of taxable income, though DSTs generally do not allow advanced strategies such as cost segregation. And if the DST owns properties in more than one state, you may need to file nonresident state returns in each of those states.

Liquidity limits and expected holding period

DSTs are not liquid investments. Most programs target a holding period of 5 to 10 years, and there’s no guaranteed way to exit before the sponsor chooses to sell the property. Secondary sales are limited, and early exits often come with discounts of 15% to 35%.

In plain English: DST capital may need to stay put for the full hold period. That limited flexibility is one reason DSTs may appeal more to people who are willing to give up control in exchange for possible tax deferral.

Fee categories and the main risks to review

Fees reduce the amount of capital that actually goes into the property. Up-front costs commonly run 10% to 18% of invested equity. Most of these charges are listed in the Private Placement Memorandum (PPM), including sponsor compensation and other expenses.

| Fee Category | Typical Range | When It's Charged |

|---|---|---|

| Selling commission (broker-dealer) | 5% – 7% of equity | Up-front |

| Acquisition fee (sponsor) | 2% – 6% of equity | Up-front |

| Asset management fee | 1% – 2% annually | Ongoing |

| Property management fee | 3% – 5% of gross income | Ongoing |

| Disposition fee | 1% – 3% of sale price | At exit |

The main underwriting questions usually center on sponsor strength, tenant quality, and loan maturity. Beyond fees, the key risks to review before committing are sponsor quality, single-sector exposure, and loan-maturity risk. IRS rules prevent a DST from renegotiating its existing loan, so a mortgage that matures during a market downturn may force a sale at an unfavorable time.

When a DST fits and how Mezzi helps you evaluate it

Once the structure makes sense, the next step is simpler: figure out whether a DST may line up with your goals and your need for cash access.

Common scenarios where DSTs are used

DSTs often come up in a few familiar situations.

The first is the "tired landlord" case. This usually involves an investor who has spent years dealing with tenants, repairs, and vacancies and now wants out of day-to-day management, while still keeping real estate exposure and deferring taxes. In that setup, a DST may offer passive monthly distributions without property management.

Another common use case involves a tight 1031 timeline. Since DSTs are typically ready to close, they may serve as a backup identification option when a direct-property deal starts to look uncertain during the 45-day window. That 45-day window may be a common point where exchanges fall apart, so having a DST lined up may reduce the chance of a failed exchange.

DSTs may also appeal to investors who want to spread proceeds across more than one property type, such as multifamily, industrial, and medical, instead of putting everything into a single replacement property. Exchange proceeds may be split across several DSTs in different sectors and geographies.

Of course, those use cases may only fit if you're comfortable with a long lockup and no control.

A simple decision framework for fit

Before moving ahead, three questions may clear up most of the complexity:

- Do you want passive income without management involvement?

- Can you leave capital locked up for a long-term hold, often 5 to 10 years?

- Are you comfortable letting a sponsor handle all operating decisions?

If the answer to any of those questions is no, a DST may not be the right fit. The table below compares DSTs with buying another directly managed property across a few of the areas people often look at first.

| Factor | DST | Direct Property |

|---|---|---|

| Control | None - sponsor makes all decisions | Full - owner decides everything |

| Liquidity | Very low - long-term hold | Moderate - may sell at any time |

| Diversification | High - fractional interests across assets | Low - concentrated in one property |

| Time commitment | Zero - fully passive | High - landlord duties continue |

| Operational complexity | Low - professionally managed | High - owner handles or oversees operations |

Key tradeoffs to review before investing

A DST may satisfy 1031 replacement rules and may defer capital gains taxes. Those features may appeal to some investors, but they also come with sponsor dependence, no operating control, upfront fees, and capital that may stay illiquid for years.

It may make sense to judge a DST against your cash needs, income needs, and estate plan, not just the offering on its own. If estate planning matters, DST interests may also be easier to divide among heirs and may receive a step-up in basis at death.

Mezzi is designed to help you test that fit against your full portfolio, not just the DST itself. With read-only access across connected accounts, Mezzi's Portfolio X-Ray shows how a DST allocation may affect concentration, liquidity, and tax planning in one view.

FAQs

Is a DST right for my 1031 exchange?

A DST may make sense for someone who wants to defer capital gains taxes through a 1031 exchange and shift into a fully passive role. That may appeal to people who don’t want to deal with tenants, maintenance, or day-to-day property work.

It may also fit situations where an investor needs to close on a short timeline, wants more diversification, or needs to replace debt without qualifying for a new loan.

A DST may be a poor fit for someone who wants control, liquidity, or the freedom to choose their own exit. In most cases, the sponsor sets the holding period, which typically runs 5 to 10 years.

How do I avoid taxable boot in a DST?

To avoid taxable boot in a 1031 exchange, some investors aim to reinvest all net equity from the sale and buy replacement property worth at least as much as the property they sold.

To avoid mortgage boot, some investors look for a DST with a leverage ratio that may match the relinquished property, so the replacement debt may be high enough to preserve full tax deferral.

What if I need my money early?

DSTs are illiquid, long-term investments, so early access to your capital may be limited.

Secondary markets for DST interests are also limited. That means there may be no guarantee you’ll be able to sell your interest before the trust’s planned 5- to 10-year life cycle ends, or that you’d get a favorable price if you do find a buyer.

For many investors, the holding period may last until the sponsor sells the property and distributes each investor’s share of the proceeds.Disclosures:

- This content is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.

- Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.

- DST investments are illiquid, may involve significant risks, and are not suitable for all investors. Investors should consult with their tax and legal advisors before making any investment or 1031 exchange decisions.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.