A 10b5-1 plan may help an executive sell stock while reducing insider-trading risk - but only if the plan is set up before any MNPI, left on autopilot, and followed in good faith.

Here’s the short version:

- I’d treat a 10b5-1 plan as a pre-set trading script, not a shield.

- The plan may work only if the insider adopts it during an open window and while not aware of MNPI.

- For directors and Section 16 officers, the first trade usually may wait 90 days or 2 business days after the related 10-Q or 10-K filing, whichever comes later, up to 120 days.

- For other insiders, the wait usually may be 30 days.

- Changes to price, amount, or timing may end the old plan and start a new one.

- Overlapping plans, repeated one-off plans, broker input, or last-minute edits may weaken the Rule 10b5-1 defense.

- Recent cases show the risk may be large: prosecutors said Terren Peizer avoided more than $12.5 million in losses, and Ontrak stock fell 44% after the news became public.

Put another way: the plan may fail when the process fails.

A few patterns stand out from the article:

- Clean setup: open trading window, no MNPI, written certification, preset formula, no later discretion.

- Weak setup: adopting after bad news is known, editing trade terms, canceling trades, or running more than one plan for the same stock.

- Common friction points: blackout periods, Form 4 timing, Rule 144, RSU tax withholding, and pressure to change the plan later.

10b5-1 Trading Plan: Compliant vs. Noncompliant Patterns Explained

How To Design a 10b5-1 Equity Compensation Trading Plan

Quick comparison

| Topic | Lower-risk pattern | Higher-risk pattern |

|---|---|---|

| Adoption | Open window, no MNPI | MNPI may already be known |

| Cooling-off period | Full waiting period observed | Trades start too soon |

| Trade control | Broker follows preset rules | Insider gives new instructions |

| Changes | No edits to economics | Price, size, or timing changed |

| Plan count | One active plan | Overlap or repeated one-off plans |

| Good faith | Process stays fixed | Plan appears tied to new facts |

If I were summarizing the whole piece in one line, it would be this: a 10b5-1 plan may offer protection only when the insider gives up control before the trade - not after.

What a Rule 10b5-1 trading plan is

A Rule 10b5-1 plan is a written trading instruction adopted before you know any MNPI. That setup matters because it shifts a discretionary sale into a preset process. If trades later happen under the plan while you still possess MNPI, the plan may support the Rule 10b5-1(c) affirmative defense by showing the trading decision was made before that MNPI arose.

Why the plan exists: compliance, not convenience

Executives at public companies often have access to MNPI, which may make ordinary stock sales risky. The purpose here is compliance, not ease: the plan moves the trading decision to a point in time before the executive learns MNPI.

That’s why these plans are common among executives managing equity compensation. Some use them to sell stock, diversify concentrated holdings, or cover equity-related taxes.

What must be set in advance

The plan must lock in the number of shares, price, and trade dates ahead of time, or rely on a preset formula, algorithm, or other objective mechanism. After adoption, the executive should not control whether, when, or how much to trade.

What the plan may not do is leave those choices open for later. As one legal summary puts it:

"10b5-1 plans must be written to operate on autopilot by specifying the formula, algorithm, or predetermined price, quantity, and dates of future securities transactions; these cannot be subject to future discretion." - Quinn Emanuel Urquhart & Sullivan

A change to quantity, price, or timing usually ends the old plan and starts a new one, which restarts the cooling-off period. That rigidity may be what supports the defense. The defense is not automatic, though; it also depends on adopting and following the plan in good faith.

Once those terms are fixed, the next issue is timing - when the plan may start, how long the cooling-off period lasts, and who executes the trades.

How 10b5-1 plans work in practice

When and how to adopt a plan

In practice, three things tend to matter most: clean adoption, the waiting period, and broker control.

A 10b5-1 plan may be adopted only when you are not aware of MNPI, usually during an open trading window after quarterly earnings are released. Put simply, timing matters. Adoption is generally expected to happen only when you are not aware of MNPI and during an open trading window.

That usually takes coordination across a few groups: you, counsel, compliance, and the broker. In many companies, the plan may need pre-clearance from a designated compliance representative or the legal department. The company may also keep records and make any public filings that are required.

Documenting what you knew at the time of adoption may help support the plan's good-faith defense if it is challenged later.

Cooling-off periods and officer certifications

After adoption, trading may not begin right away. A mandatory cooling-off period creates space between signing the plan and the first trade. The length of that wait may depend on the insider's role.

| Role | Cooling-Off Period |

|---|---|

| Directors and Section 16 officers | Later of 90 days after adoption or 2 business days after the 10-Q/10-K filing for the quarter of adoption (capped at 120 days) |

| Other insiders (non-officers) | 30 days after adoption |

Directors and officers must also certify in writing at adoption that they are not aware of MNPI and are entering the plan in good faith.

Even with that certification, the plan may not be established or modified during a blackout period. Those windows are generally treated as higher-risk periods for MNPI.

Broker execution and loss of discretion

Once the cooling-off period ends, the broker may execute trades automatically based on the plan's preset terms, with no further input from you.

Where legal risk may show up is after the plan goes live. Direct instructions to the broker about specific trades may create problems because they may suggest you still have control over execution.

Some changes are usually treated differently. For example, updating account details or switching broker-dealers is generally viewed as an administrative change and may not terminate the plan. But changing trade terms will usually end the old plan and restart the cooling-off period.

The next compliance risk may come from any change that gives you back discretion.

Core compliance rules that can preserve or destroy the defense

Good faith, overlapping plans, and single-trade plan limits

Once a plan is in place, the main risk may shift to what happens afterward.

Adoption is only the first step. Good faith may need to continue for the full life of the plan.

Overlapping plans may weaken the defense. Insiders may not run more than one 10b5-1 plan for the same stock at the same time. If two plans are active at once, that setup may restore discretion and may defeat the defense.

A single-trade plan may be used only once in any 12-month period. A narrow exception may apply to sell-to-cover plans tied to RSU or restricted-stock tax withholding.

If overlap may weaken the defense, later changes may end it too.

Modification, suspension, and termination risks

Changing the amount, price, or timing terminates the old plan and starts a new one. Canceling a scheduled trade may trigger the same result.

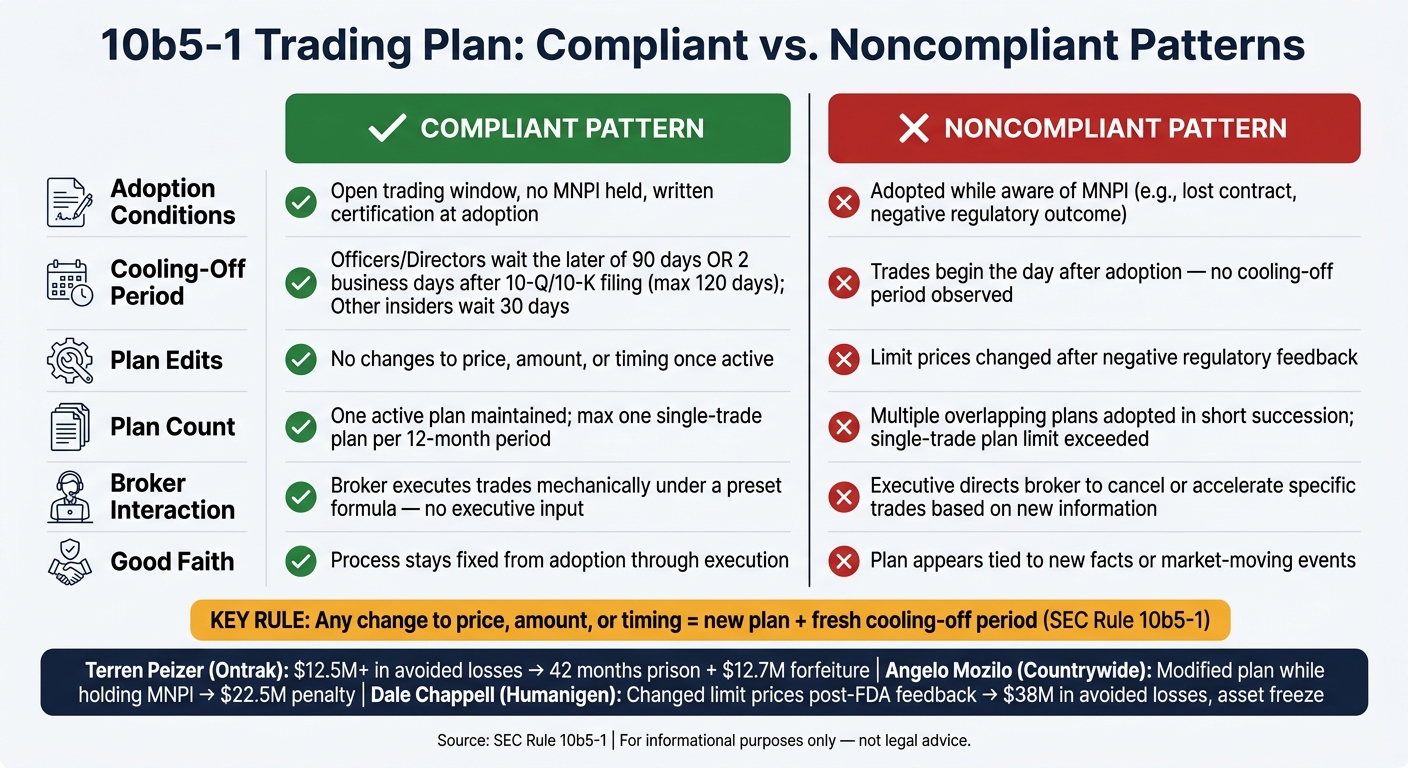

The Countrywide Financial case shows how this risk may play out. The SEC charged former CEO Angelo Mozilo with insider trading despite his use of 10b5-1 plans, alleging he established four separate plans within three months and modified one while potentially in possession of MNPI. The case resulted in a $22.5 million penalty.

Frequent cancellations may make a plan look pretextual.

Pre-action checklist: before adopting, modifying, or terminating a plan

Before any decision, some insiders may confirm a few points with legal, compliance, and tax professionals:

- Confirm whether you hold MNPI.

- Confirm the trading window is open.

- Confirm no other 10b5-1 plan is active for the same stock.

- Confirm whether earnings, M&A, or tax timing affects the plan.

- Confirm how trades will be reported on Form 4 and whether Rule 144 obligations apply.

- Confirm that planned sale volume aligns with tax withholding needs and that liquidity pressures will not force a later modification.

The real test may be whether the trades match the plan exactly. The next step is to compare clean and flawed trading patterns side by side.

Compliant vs. noncompliant executive trading scenarios

Side-by-side examples of what helps and what undermines the defense

A quick comparison makes the rule easier to follow: one clean setup versus two cases that appear to have gone off track.

Terren Peizer, then-CEO of Ontrak Inc., adopted two 10b5-1 plans while aware that Cigna - the company's largest customer - was likely to terminate a roughly $90 million contract. He began selling shares the day after each plan was adopted. When the termination was announced in August 2021, Ontrak stock fell 44%. Peizer avoided more than $12.5 million in losses. In June 2025, he was sentenced to 42 months in prison and ordered to forfeit more than $12.7 million in gains.

"The Justice Department's first insider trading prosecution based exclusively on the use of a trading plan, but it will not be our last." - DOJ Criminal Division

In a separate case, Dale Chappell, Chief Scientific Officer of Humanigen Inc., modified his 10b5-1 plan in June 2021 to change limit prices from above-market to below-market after negative FDA feedback on the company's primary drug. By selling 3.8 million shares before the public announcement of the FDA's denial, he avoided $38 million in losses. In July 2024, the Third Circuit upheld an asset freeze as the SEC pursued disgorgement.

What seems to tie both cases together? The plans no longer looked automatic. They appeared to reflect new information. That tends to weaken the defense.

The table below shows the split between a compliant pattern and a noncompliant one. Most of the difference may come down to timing, discretion, and whether the plan stayed fixed.

| Variable | Compliant Pattern | Noncompliant Pattern |

|---|---|---|

| Adoption conditions | During an open trading window after earnings, with no MNPI held; executive certifies in writing at adoption | Adopted while aware of a lost contract or negative regulatory outcome; no clean certification possible |

| Cooling-off period | Trades begin after the later of 90 days from adoption or two business days after the quarter's Form 10-Q or 10-K filing, capped at 120 days for officers and directors | Trades begin the day after adoption, with no cooling-off period observed |

| Plan edits | No changes to price, amount, or timing once active | Limit prices are changed after negative regulatory feedback |

| Plan duplication or repeated one-off trading | One active plan maintained for the full duration; no more than one single-trade plan used in any 12-month period | Multiple overlapping plans adopted within a short period; single-trade plan limit exceeded |

| Broker interaction | Broker executes trades mechanically under a preset formula | Executive directs the broker to cancel or accelerate specific trades based on new information |

The recurring weak spot is fairly plain: if a plan is adopted or changed after MNPI enters the picture, the good-faith defense may be harder to maintain.

Conclusion: A 10b5-1 plan works only if the process is as disciplined as the trades

Taken together, these rules point to a simple idea: a 10b5-1 plan may function as a compliance tool, not an automatic shield. The defense may depend on the process staying intact from adoption through execution: clean adoption, good faith, the required cooling-off period, required certifications, and no executive discretion once trading begins.

The examples above suggest the same pattern. The defense may fail before the trade, when a plan is adopted or changed after new information surfaces. Frequent edits, overlapping plans, or early terminations may also weaken the defense, even if the individual trades follow the written instructions.

Any change to price, amount, or timing is treated as a new plan under SEC rules and triggers a fresh cooling-off period. Put plainly, some companies and insiders may treat the plan as a long-term compliance commitment: document the absence of MNPI, preserve records for any change or termination, and coordinate with legal, compliance, broker, and tax professionals before acting.

FAQs

Who qualifies as an insider under Rule 10b5-1?

Under Rule 10b5-1, an insider generally includes a director, senior officer, or any person or entity that owns more than 10% of a company’s voting shares.

More broadly, it may include anyone with access to material nonpublic information about a company or its securities. Directors and officers may be the people most often linked to these plans, but the rule may also apply to other market participants seeking this affirmative defense.

What counts as MNPI when adopting a 10b5-1 plan?

MNPI means material nonpublic information: information about a company or its securities that hasn't been made public and that may matter to a reasonable investor.

If you adopt or modify a 10b5-1 plan, you may not be aware of MNPI at that time. Examples may include undisclosed quarterly results, potential mergers, litigation settlements, or clinical trial results.

To rely on the rule’s affirmative defense, you must certify in writing that you do not have MNPI when the plan is adopted.

What happens if I cancel my plan early?

Ending a 10b5-1 plan early may weaken the affirmative defense for trades that already took place if the timing raises questions about whether the plan was set up in good faith from the start. And from a legal standpoint, canceling planned transactions is generally treated the same as ending the plan.

If you later put a new plan in place, a new cooling-off period may apply. If ending the plan becomes necessary, some insiders may try to avoid doing that while aware of material nonpublic information, keep a clear record of the reason, and consult legal counsel.Disclosures:

- This content is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.

- Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.