A big exit may leave you with less spendable money than the headline number suggests. Taxes, lock-ups, vesting rules, and single-stock risk may all shrink what you may actually use in the first 12 to 24 months.

Here’s the short version: I’d frame the first year around four jobs - know what’s liquid, set aside tax cash, lower company-stock concentration, and put simple portfolio rules in writing. For many people, the costliest missteps may come from spending too soon, selling without knowing the tax hit, or keeping too much tied to one company.

What this piece covers:

- What you may own after an exit: cash, locked shares, unvested equity, escrow, and earnouts

- Why RSUs, NSOs, ISOs, NIIT, state tax, and AMT may change your net proceeds

- Why some investors try to keep single-stock exposure near 10% to 15% of net worth, while some advisors mention under 20%

- Why a 6- to 24-month cash runway may come before new investments

- How hidden overlap in ETFs, 401(k)s, IRAs, and brokerage accounts may add more company exposure than you think

- Why a short written plan, like an investment policy statement, may keep decisions from turning emotional

Quick comparison

| Topic | What may happen | What some people do |

|---|---|---|

| Liquidity | Wealth may be partly locked for months or years | Sort assets into liquid, locked, and vesting |

| Taxes | Withholding may fall short; AMT or NIIT may apply | Set aside a tax reserve and review estimated payments |

| Concentration | One stock may dominate net worth | Use a staged sell-down or a preset selling plan |

| Cash flow | Large proceeds may not match monthly needs | Keep 6 to 24 months of expenses in cash or cash-like holdings |

| Portfolio | Drift and overlap may build up over time | Write simple allocation and rebalancing rules |

That’s the core idea: protect the money first, then decide what to do with it.

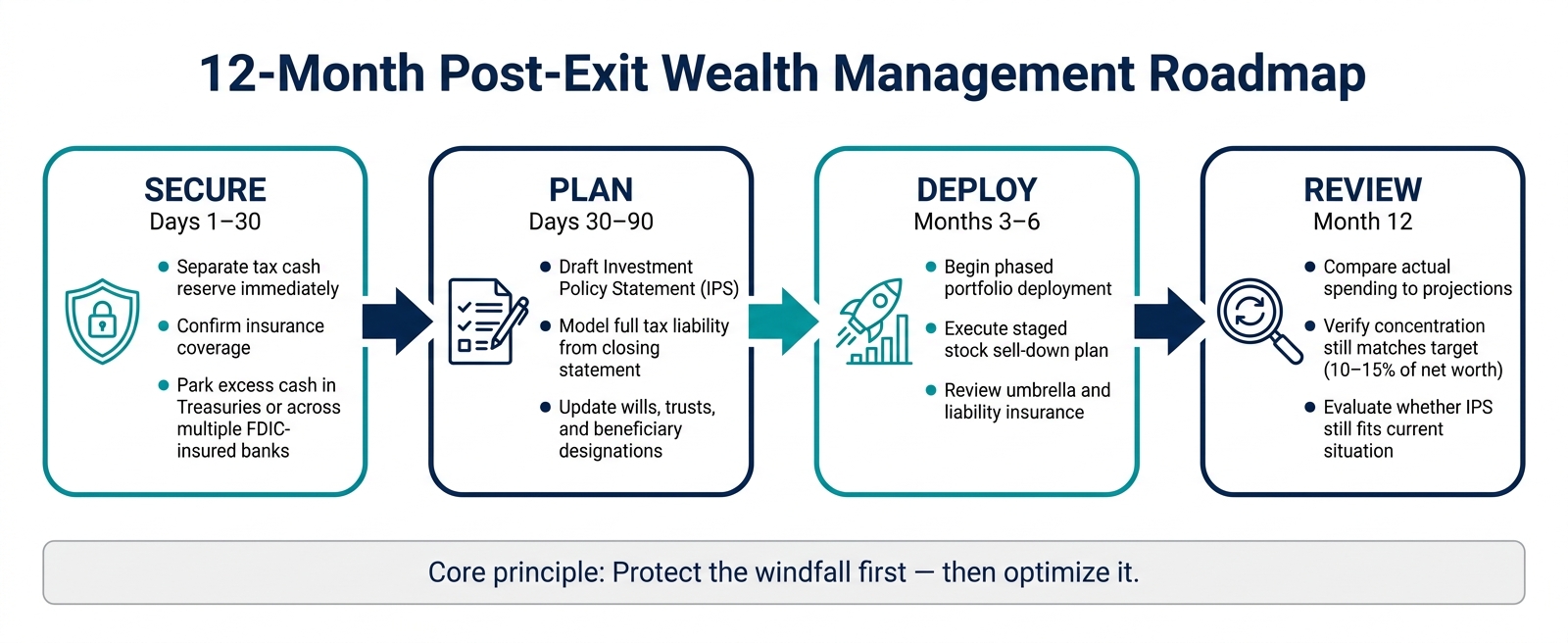

12-Month Post-Exit Wealth Management Roadmap

What to Do With Your Stock After the IPO (Step-by-Step, Lockup to Sale)

1. Get a clear picture of what you own before making big moves

Start with the inventory the introduction called for: list every asset, restriction, and vesting date before you decide what to sell or reinvest.

Before you sell or reinvest anything, you need an honest inventory of what you actually have. Post-exit wealth rarely arrives as one lump sum. It usually shows up as a mix of cash, vested shares, locked shares, unvested equity, and contingent proceeds. Pull together the inputs that shape your actual timeline: vesting dates, lock-up expiration, escrow terms, and contingent payment schedules.

Sort holdings into liquid, locked, and still vesting

A simple way to start is to sort everything into three buckets:

- Liquid: cash and vested shares with no restrictions

- Locked: shares under an IPO lock-up, rollover equity in a private equity-backed deal, and escrowed funds

- Still vesting: unvested RSUs, unexercised options, and performance grants

IPO lock-ups often last 180 days, while rollover equity may stay illiquid for years. That’s why the deal documents matter more than the headline number in the announcement. Your timeline may depend on those terms.

Set a 6- to 24-month cash runway

Once you know what’s liquid, set aside 6 to 24 months of expenses in cash or cash equivalents, such as cash, money market funds, short-term Treasuries, or FDIC-insured accounts. Map out spending across housing, taxes, healthcare, child care, tuition, and any debt you may plan to pay off.

It also helps to separate one-time big purchases, like a home down payment or a debt payoff, from monthly living costs. If your cash reserve exceeds $250,000, some people spread it across multiple banks or hold the excess in U.S. Treasuries. Keeping that reserve separate may make it easier to avoid dipping into taxable holdings too early.

Connect all accounts to see your total exposure

Read-only account aggregation may give you a better view of total exposure across taxable, retirement, and equity-compensation accounts. Connecting taxable brokerage, 401(k), IRA, Roth IRA, and equity compensation accounts into one dashboard may give you a live picture of total net worth and concentration in your former company’s stock.

Mezzi provides read-only aggregation through Plaid and Finicity. It surfaces company-stock exposure across all connected accounts at once, including overlap that may be easy to miss when looking at accounts one by one. It shows exposure without moving money.

Include liabilities too. That way, any sell-down plan may be based on net worth, not just gross proceeds. Inventory liquid cash, marketable securities, retirement accounts, equity compensation, contingent assets, and liabilities to calculate true net worth.

Once you know what’s liquid and what’s locked, you may be in a better position to estimate the tax cost of any sale.

2. Know your tax bill before you sell anything

Headline value and spendable value may be very different after federal and state taxes. Before selling, sort each grant and each sale by tax treatment.

Identify ordinary income, capital gains, and AMT risk

How proceeds are taxed may depend on the type of equity you held and how long you held it:

- RSUs: Taxed as ordinary income at vesting. Any later change in value may be treated as a capital gain or loss at sale. Taxed at vesting; no exercise step.

- NSOs: The spread at exercise is ordinary income. Any later appreciation may be a capital gain at sale. High ordinary income exposure.

- ISOs: May qualify for long-term capital gains treatment if the two-year-from-grant and one-year-from-exercise holding periods are met. An early sale converts the spread to ordinary income. ISOs may trigger AMT before you sell, which may create a tax bill on unrealized gains.

On top of federal taxes, the Net Investment Income Tax (NIIT) adds 3.8% on investment income for single filers earning above $200,000 or married couples above $250,000. In California, capital gains are taxed as ordinary income at rates up to 13.3%.

| Equity Type | Ordinary Income Trigger | Capital Gains Trigger | Key Risk |

|---|---|---|---|

| RSUs | At vesting (FMV) | Sale price minus FMV at vest | Taxed at vesting; no exercise step |

| NSOs | At exercise (spread) | Sale price minus FMV at exercise | High ordinary income exposure |

| ISOs | Only if early sale | Entire gain if qualified disposition | AMT exposure on unrealized gains |

| Founder Stock | N/A (usually) | Sale price minus basis | May qualify for QSBS exclusion if requirements are met |

Once you know what part of the proceeds may be taxable and when, set cash aside for that bill before thinking about selling tactics.

Set aside a tax reserve and plan estimated payments

Standard RSU withholding is typically 22%. If your marginal federal rate is 37%, that may leave a gap before state taxes are even counted. A lot of people get tripped up here. The brokerage deposit looks large, but part of it may already belong to the IRS and your state.

One approach some people use is to reserve the tax shortfall in cash as soon as proceeds arrive.

To avoid IRS underpayment penalties, pay at least 100% of your prior year's tax liability through estimated quarterly payments - or 110% if your prior-year adjusted gross income exceeded $150,000. Large liquidity events often push income well above normal withholding thresholds, so estimated payments may become more relevant than usual. It may make sense to treat your tax reserve as already spent before planning anything else.

Check wash-sale risk across all accounts

Tax rules also shape how rebalancing may work across accounts. Wash sales may happen across accounts, not just inside the one you sold from. That means tax-loss selling may backfire if it conflicts with your post-exit diversification plan.

Mezzi flags wash-sale risk across connected accounts before you trade. If Mezzi flags a wash-sale window, it can notify you when the 30-day period has passed so you can consider buying back the position.

3. Cut concentration risk

Once you've set money aside for taxes, the next step may be reducing company-stock concentration without pushing yourself into a poorly timed sale.

Set a concentration limit and a sell-down schedule

Before selling a single share, decide how much company stock you may be comfortable keeping. Financial advisors generally recommend cutting employer stock down to 10–15% of your total net worth. That gives you a clear target instead of a fuzzy plan to diversify "later."

After that, map out a sale schedule that may get you there. A 3- to 5-year sell-down may spread taxes across multiple years and may reduce timing risk.

If insider rules apply, a Rule 10b5-1 plan may automate a pre-set sell-down schedule.

Compare selling, borrowing, or waiting

At a high level, you may have three paths: sell shares, borrow against shares, or hold and wait. Each one comes with tradeoffs.

Tax savings may matter, but they may not justify staying heavily exposed to one stock.

| Option | Liquidity Speed | Tax Impact | Market Risk | Interest/Cost | Complexity |

|---|---|---|---|---|---|

| Direct Stock Sale | High | Immediate capital gains or ordinary income | Low (once sold) | None | Low |

| Staged Selling | Medium | Spread over multiple years | Moderate | None | Moderate |

| Securities-Based Lending | High | None until shares are sold | High (margin call risk) | Interest rates | High |

| Waiting (Holding) | Low | Deferred | High (concentration risk) | Opportunity cost | Low |

Borrowing against shares may cover a short-term cash need, but a sharp drop in the stock price may trigger a margin call.

Find hidden company exposure with overlap analysis

Your direct stock position may be only part of the risk. Index funds and ETFs may add more exposure to the same company in the background.

If you hold broad-market ETFs or mutual funds in a 401(k), IRA, or taxable account, your company stock may already be sitting there too. A position that looks manageable on one statement may turn into a much larger concentration once overlapping holdings are counted.

Mezzi's overlap analysis surfaces that hidden exposure across connected accounts, so you can see the full picture before deciding how much to sell. The combined exposure number may then be used to set the sell-down target for the portfolio you build next.

With concentration more in check, the next step may be putting the proceeds into a portfolio you may actually stick with.

4. Build a long-term portfolio and a process to manage it

With tax cash set aside and concentration brought down, the next step may be putting rules on paper so the windfall doesn't drift over time.

Write an investment policy you can follow

The habits that may help build a company don't always fit a liquid portfolio. Concentration may work in one setting and create more risk in another.

An Investment Policy Statement, or IPS, is just a written set of rules for your money. It may spell out how you think about risk, liquidity, rebalancing, and selling before emotion starts calling the shots.

Keep it short and usable. In many cases, that means defining:

- your goal

- your cash reserve

- your target allocation

- your sell and rebalance rules

A 90%–95% core portfolio of diversified, low-cost instruments and a 5%–10% active bucket for angel deals or private investments may give entrepreneurial instincts a clear lane. Some people keep speculative investing in a small sleeve so the core portfolio may stay more insulated.

It also may help to tie the IPS to the diversification plan you already set. That way, sales, rebalancing, and cash needs may follow one rule set instead of turning into separate decisions each time. A formal review at the 12-month mark, and then once a year after that, may keep the policy aligned with where things stand.

Once the rules are written, the next piece may be organizing the accounts that will hold them.

Consolidate accounts and improve asset location

Many people reach a liquidity event with accounts spread across a few custodians: an old 401(k), a taxable brokerage account, a Roth IRA, maybe a trust account. Before trying to fine-tune anything, map the full balance sheet, including cash, retirement assets, real estate, and any contingent proceeds such as earnouts or escrow.

Deciding which investments belong in taxable, IRA, Roth, or 401(k) accounts may reduce tax drag over time. One dashboard that shows taxable, retirement, and equity-compensation accounts together may make it easier to spot overlap and place assets in the accounts where taxes may be lower.

A 12-month post-exit checklist

The first year may be used to secure cash, write the plan, deploy gradually, and review once.

| Phase | Timeline | Key Actions |

|---|---|---|

| Secure | Days 1–30 | Separate tax cash, confirm coverage, and park excess cash in Treasuries or multiple banks. |

| Plan | Days 30–90 | Draft your IPS; model tax liability from the actual closing statement; update wills, trusts, and beneficiary designations |

| Deploy | Months 3–6 | Begin phased portfolio deployment; review umbrella and liability insurance coverage |

| Review | Month 12 | Compare spending to projections; verify exposure still matches your target allocation; evaluate whether your IPS still fits |

Estate documents may deserve attention soon after an exit, not someday. Updating wills, trusts, and beneficiary designations promptly may help keep the plan aligned with the new balance sheet.

Mezzi surfaces ongoing alerts as your situation evolves - concentration thresholds creeping back up, tax-loss harvesting opportunities, wash sale windows, Roth conversion timing - so you may stay ahead of what matters.

Conclusion: Protect the windfall before you optimize it

An exit may change your balance sheet right away. But many of the biggest mistakes may happen early, and the effects may last for years. That’s why the moves may still make more sense in a clear order.

The focus now may be sequencing, not reacting. Start with cash, taxes, and concentration. Some people park tax money separately before they spend or invest. Next comes concentration risk. A sell-down plan and concentration limit may bring company stock back under control. Then the IPS may turn that target into a process you can repeat instead of something you decide on the fly.

During the first few weeks, some people park proceeds in cash or short-term Treasuries while the plan takes shape.

Protect the proceeds first. Then use the plan to diversify with discipline.

FAQs

How much of my exit is actually spendable?

Your total exit proceeds may not be the same as the amount you may actually have available to spend.

A more careful way to look at it starts with taxes. Some founders estimate federal and state capital gains taxes, plus any income taxes, on the cautious side and move that amount into a separate account. That step may make the picture feel more grounded.

Then there are the known commitments. Things like:

- mortgage payoffs

- college savings

- a lifestyle reserve

Once those goals are covered with after-tax dollars, the amount left over may be a more realistic spendable base.

What taxes should I plan for before selling shares?

Plan for taxes based on your equity type and income level. That may include ordinary income tax, long-term capital gains tax, and the 3.8% Net Investment Income Tax (NIIT).

If you have ISOs, also account for the Alternative Minimum Tax (AMT). It may create a large tax bill even before any sale happens.

It may also make sense to check for QSBS exclusions. And don’t leave out state taxes, which may add a lot to the total. In California, for example, rates may go as high as 13.3%.

How do I reduce company stock risk without rushing?

Use a staged, multi-year plan instead of selling everything at once. That approach may reduce emotional decision-making, spread taxes across multiple years, and lower the chance of trying to time the market.

Start with a target allocation. Then follow a disciplined approach, such as:

- time-based selling

- goal-based selling

- a 10b5-1 plan

If you’re not ready to sell, hedging or exchange funds may also help, depending on your tax, liquidity, and long-term goals.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.