One stock may put too much of your money at risk long before taxes become the main issue. In many cases, a position may deserve a close look once it reaches 10% of a portfolio, and it may feel more serious around 20%+. That may matter even more with employer stock, where your pay, unvested equity, and held shares may all be tied to the same company.

Here’s the short version:

- A concentrated position may be a risk problem first and a tax problem second

- A stock that looks fine inside total net worth may still be heavy inside liquid or investable assets

- A simple stress test may help: if the stock fell 40% to 60%, what parts of your plan may change?

- Taxes may shape the exit path, but waiting only for tax reasons may leave you exposed longer

- Some people look at:

- staged selling

- specific-lot sales

- tax-loss offsets

- donating appreciated shares

- donor-advised funds

- exchange funds

- hedging, such as puts or collars

- A written target range, such as 10% to 15%, may make it easier to keep one stock from taking over again

A few numbers may put the issue in context: single stocks may show volatility around 28%, versus about 15% for the S&P 500. And a large share of public companies have had very deep losses at some point. That’s why many investors may start with one question: “If I had cash today, would I still put this much into this one stock?”

The rest of the piece walks through how people may size concentration, test downside risk, weigh taxes, and review the main ways they may diversify with less tax drag.

4 Ways to Diversify Concentrated Stock Positions (EP.118)

What counts as a concentrated stock position

Most planners may flag a stock for review once it reaches 10% of a portfolio, and many may treat 20% as a more serious concentration. Some institutional rules use 30% or more. At that point, the main issue may not be whether selling would trigger taxes. It may be whether one stock now carries enough weight to affect too much of your wealth.

That line matters because concentration risk may climb fast once a single holding has the power to change your financial plan. And single stocks may swing much more than broad indexes. On average, single stocks show volatility of 28%, versus 15% for the S&P 500.

This often happens without any grand plan. RSUs vest, ESPP shares gain value, or one winner keeps running - and before long, one ticker may take over your holdings.

Portfolio concentration vs. net-worth concentration

Your portfolio percentage and your total net worth percentage may tell two very different stories.

A $750,000 position may equal 75% of a $1 million investment portfolio, which many people may view as high risk. But that same position may be just 7.5% of a $10 million total net worth that includes real estate, a private business, and cash reserves.

So the same holding may look extreme inside a portfolio but fairly modest against total wealth. That’s why some people measure concentration against:

- total net worth

- investable assets

- liquid assets tied to near-term goals

Why employer stock is a double concentration risk

Employer stock may carry a double concentration risk because your salary, bonus, unvested equity, and current shares may all depend on the same company. If that company hits a rough patch, more than one part of your balance sheet may feel it at once.

There’s another wrinkle. Blackout windows and insider-trading limits may prevent selling at the exact moment selling feels most urgent. That timing problem may make a concentrated position harder to manage.

The history here may give some people pause. Roughly 66% of tech companies have gone through a permanent decline of 70% or more from their peak prices and never recovered. And for executives who must hold company stock equal to a multiple of salary, the concentration may not even be optional - it may be required by company policy.

Once you know your level of exposure, the next step may be deciding whether it’s high enough to warrant action. The size of the position may be only one part of that test; volatility, tax exposure, and timing may matter too.

How to tell when concentration risk is high enough to act

Concentrated Stock Risk: How One Stock Can Impact Your Entire Portfolio

A concentrated position isn't always a problem. The harder part is figuring out when it may start putting other goals at risk. The key issue isn't whether the stock has performed well. It's whether that one holding may now be big enough to disrupt the rest of your plan.

Warning signs: size, volatility, and downside scenarios

One simple way to pressure-test the position is to run a downside scenario. If the stock fell 40% to 60%, what might change? Retirement may get pushed back. College savings may need to slow down. A home purchase may need to wait. If any of that seems likely, the position may be large enough to threaten your plan.

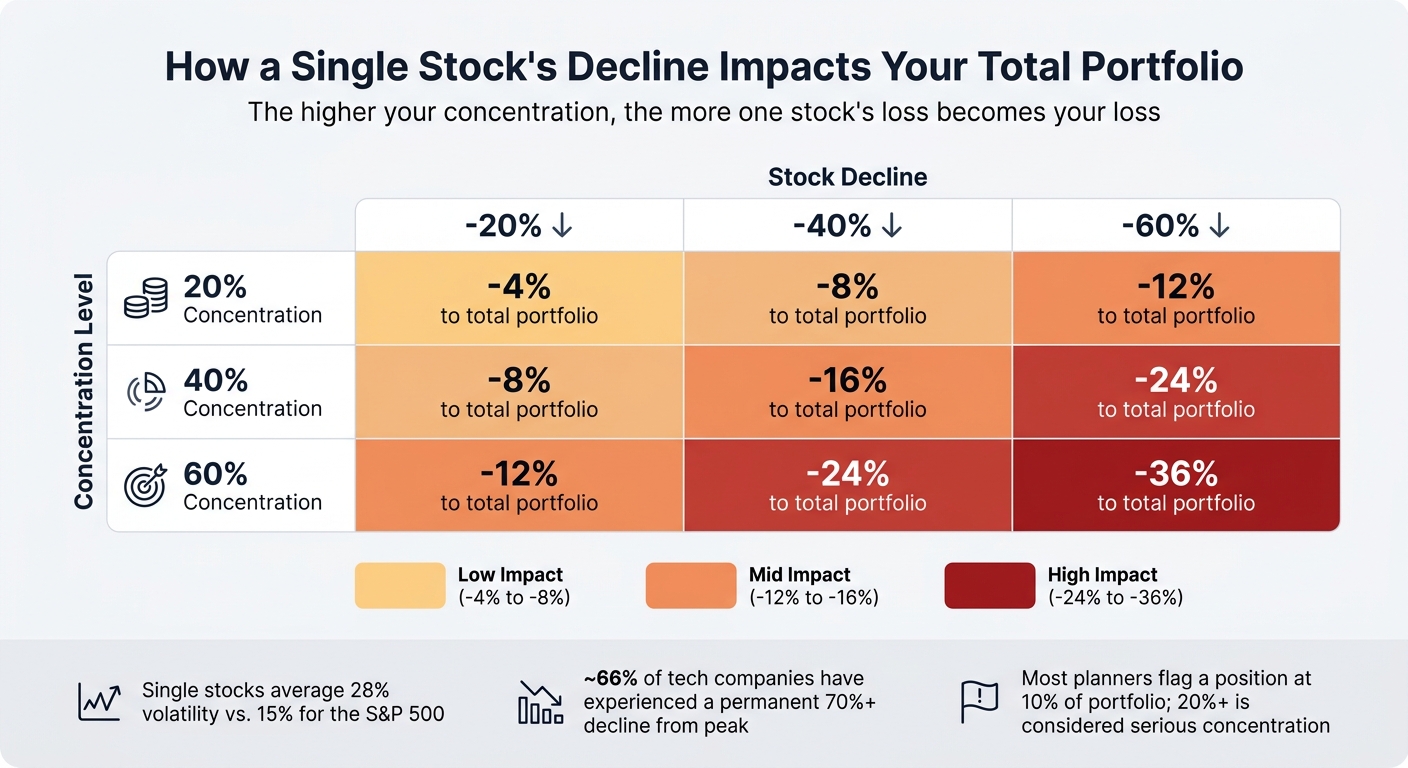

Here’s how a drop in one stock may flow through the total portfolio at different concentration levels:

| Stock Decline | 20% Concentration | 40% Concentration | 60% Concentration |

|---|---|---|---|

| -20% | -4% to total portfolio | -8% to total portfolio | -12% to total portfolio |

| -40% | -8% to total portfolio | -16% to total portfolio | -24% to total portfolio |

| -60% | -12% to total portfolio | -24% to total portfolio | -36% to total portfolio |

(Source: Fortrove Partners)

There’s also a helpful gut check: the blank-slate test. If you were sitting on cash today and taxes weren't part of the picture, would you choose to put this much into this one stock? If the honest answer may be no, the position may be sticking around more because of tax hesitation than real conviction.

If the position fails the downside test, taxes may shape how you exit, but they may not be a good reason to avoid dealing with the risk.

Tax and timing factors that affect the decision

Taxes may vary based on holding period, income, and state rules. But they're finite. Concentration risk may keep changing with the market.

Some people wait for a lower-income year, spread sales across more than one tax year, or sell a lot after it passes the one-year mark. Those moves may reduce the tax bill. Still, every month of waiting may mean another month of exposure. That holding risk may be harder to put a number on, but in some cases it may outweigh the taxes.

Use Mezzi to see your full exposure before making a move

Before making any move, it may help to get a clean picture of your total exposure. A stock held directly may also appear inside ETFs or mutual funds in a 401(k) or IRA. That may add to concentration in ways a basic account view doesn't show.

Mezzi connects taxable, retirement, and employer accounts in read-only mode, so you may see total exposure in one place. Its X-Ray feature shows overlap across funds, including holdings that may increase your true concentration. Mezzi’s tax analysis tools may also help compare the tax impact of different sale scenarios before you act.

With that exposure mapped out, it may be easier to look at diversification paths with lower tax cost.

Once the position is clearly too large to ignore, the next step may be reducing it without adding avoidable tax drag.

How to diversify a concentrated position without unnecessary tax damage

Once concentration gets high enough that action may make sense, the goal usually shifts to lowering risk without adding avoidable tax drag. The path may depend on taxes, cash needs, and how fast risk may need to come down.

Staged selling, specific-lot selection, and tax-aware rebalancing

A staged sale may reduce tax shock. Spreading sales across two to five years may keep annual gains smaller and may make bracket management easier.

Specific-lot identification may make that approach work better. Instead of selling shares in the order they were bought, you choose which lots to sell first. Selling the highest-basis shares first may mean the smallest gain gets realized on each sale.

Losses in other holdings may also offset gains.

If sales in one year may create more tax than someone wants, charitable transfers may reduce exposure without triggering the same gain.

Charitable giving, donor-advised funds, and donating appreciated shares

Donating appreciated shares may eliminate capital gains tax and may allow a deduction for fair market value.

A donor-advised fund (DAF) lets someone donate shares now, claim the deduction now, and make grants later.

Exchange funds and hedging for larger or more complex positions

For larger or more complex positions, two other tools may come into play: exchange funds and hedging strategies.

An exchange fund lets investors contribute shares into a pooled fund alongside others with concentrated positions. In return, they receive a diversified interest in the pool without triggering a taxable sale. The tradeoff is a seven-year lockup period, and access may be limited to accredited investors.

Hedging strategies like protective puts and equity collars may limit downside while someone works through a longer exit plan. A protective put sets a floor on losses while leaving upside open. A collar pairs a put with a covered call, which caps upside but may reduce or eliminate the cost of the put. One caution matters here: if a collar gets structured too tightly, the IRS may treat it as a constructive sale under IRC 1259, which may trigger taxes even if the shares haven't been sold.

The last step is turning the chosen method into a schedule you can follow.

Build a diversification plan you can stick to

Once concentration gets high enough to warrant action, it may help to put the decision in writing. Start with a full inventory of every position you hold: ticker symbols, account types, share counts, current market values, cost basis by lot, and acquisition dates. Add equity compensation details too, such as vesting schedules, grant agreements, option expiration dates, and ESPP offering periods. If you hold employer stock, include salary, bonus, and unvested RSUs, since each of those may still be tied to the same company. That full inventory often shows single-stock exposure across all accounts, not just the ones that first come to mind.

Use the same account base each time you measure concentration. That way, your target may reflect actual exposure rather than short-term market swings. Many people look at concentration against:

- total net worth

- investable assets

- liquid assets

Keeping that measurement base consistent may make the target band more useful as markets move.

From there, set a target range, not just one number. A band like 10%–15% may give you some room for normal market movement without pushing you into trades every quarter. Then pick a main path. For many people, that may mean staged selling. For others, charitable giving may fit if philanthropy is part of the picture. Exchange funds or hedging may come up for larger, more complex positions. The goal, for some investors, may be to lower risk without knocking the rest of the plan off course.

After that, put review dates on the calendar so the position may not drift back into a risky zone. A quarterly review may make sense, along with a check on how realized gains may interact with income thresholds, especially the 3.8% Net Investment Income Tax (NIIT) and any state-level tax rules. Mezzi connects all your accounts in one view and shows when sales, gains, and tax thresholds change. Regular reviews may help keep risk, taxes, and liquidity in line.

FAQs

How much of one stock is too much?

There’s no single cutoff here. It usually depends on your financial plan.

That said, many professionals treat 10% to 20% of a portfolio in one stock as a sign that the risk may be worth reviewing.

The need to respond may feel more pressing when that position is tied to your job, like employer stock. In those cases, a common diversification benchmark is keeping any one company at 4% to 5% or less of net worth.

Should I diversify even if taxes will be high?

Yes. Diversifying may still make sense even when taxes are high, because the risk tied to a concentrated position - including major losses - may outweigh the upfront tax cost.

Some people look for ways to soften the tax hit through:

- staged selling

- tax-loss harvesting

- donor-advised funds for charitable giving

- exchange funds

What’s the best way to reduce employer stock risk?

Use a disciplined, rules-based plan that balances concentration risk with tax and liquidity needs. Instead of selling everything at once, some people may prefer a staged approach.

Start by measuring your full exposure. That may include:

- vested shares

- unvested equity

- how closely your income may be tied to the stock

From there, some investors set a target allocation - often 5% to 10% - and work to reduce exposure over time through systematic selling, tax-lot selection, and reinvesting new cash or vesting proceeds into diversified assets.

Related Blog Posts

- Is it wise to add a single growth stock to a diversified portfolio, and what’s a sensible position size?

- How can I identify and reduce over-concentration risks in my 401(k) (by issuer, sector, and factor)?

- Concentrated stock position monitoring

- Stock Portfolio Analyzer: See Concentration Risk Across All Your Accounts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.