For many people, selling RSUs at vest may be the clean default. The tax on vesting may already be locked in, employer withholding may sit at 22% for many grants, and holding may leave both your paycheck and your money tied to the same stock.

Here’s the short version:

- Vesting and selling are two separate tax events.

- The vest-date value may be taxed as W-2 income.

- Selling right away may mean little or no capital gain or loss.

- Holding may only make sense if cash needs are covered, concentration stays low, and there’s a written reason to keep the shares.

- If your tax rate is above 22%, you may still owe more at filing.

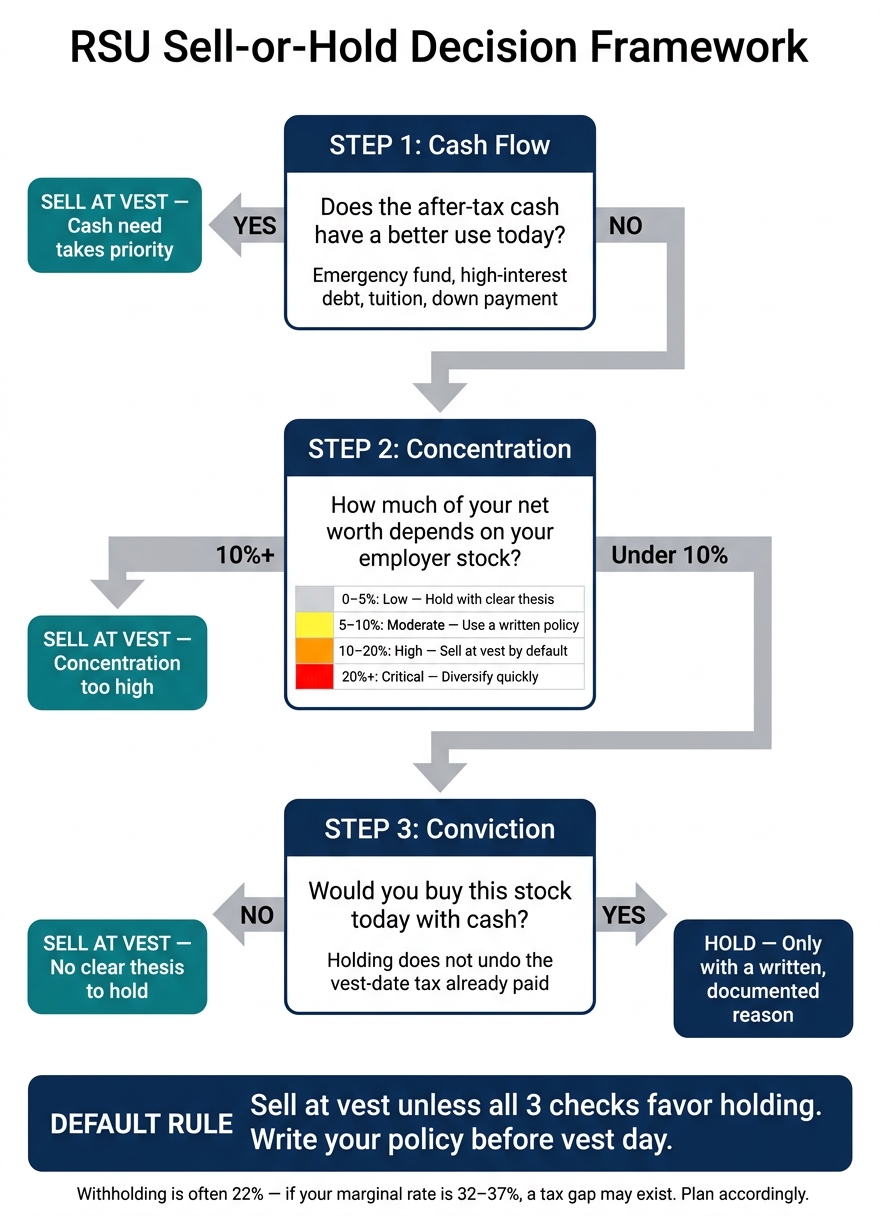

I’d frame the decision around just three checks:

- Cash flow: Would the after-tax cash do more for me today?

- Concentration: How much of my net worth may already depend on my employer?

- Conviction: If I had cash instead of stock, would I buy these shares today?

RSUs: Hold or Sell? The Right Strategy

Quick comparison

| Choice | Tax picture | Stock risk | When some people may lean this way |

|---|---|---|---|

| Sell at vest | W-2 tax may already be set; same-day sale may mean little extra tax | Lowers single-stock exposure | Tax gap, debt, cash needs, or high employer-stock exposure |

| Hold after vest | Future gains may qualify for long-term capital gains after 1 year | Keeps company-stock risk | Low concentration, no near-term cash need, and a clear reason to hold |

That’s the core idea: once RSUs vest, the question may be less about taxes alone and more about whether keeping the shares still fits your cash, tax, and risk picture.

Why vested RSUs create a real planning problem

It may help to treat vesting and selling as two separate calls. They may happen close together, but from a tax and planning angle, they’re not the same thing.

That distinction matters. If the stock drops after vesting, you may end up with a capital loss on paper, but that loss may not undo the W-2 tax that was already triggered at vest.

RSU taxes happen in two stages: vesting first, sale later

RSUs involve two tax events, and blending them together may get expensive fast.

The first tax event happens when the shares vest. At that point, the value of the shares is taxed as W-2 wages. That same vest-date price becomes your cost basis for the shares after that.

The second tax event happens when you sell. If the stock price moved up or down from the vest-date price, the difference may be treated as a capital gain or capital loss. If you hold the shares for more than one year after vesting, that gain may qualify for long-term capital gains treatment at 0%, 15%, or 20% federally, plus a possible 3.8% Net Investment Income Tax (NIIT) for higher earners. If you sell within one year, any gain may be taxed at ordinary income rates, similar to wages.

| Tax Event | When It Happens | Tax Type | What's Taxed |

|---|---|---|---|

| Vesting | Shares delivered | Ordinary income (W-2) | FMV at vest date |

| Sale (< 1 year) | Sold within a year of vest | Ordinary income rates | Gain/loss over vest FMV |

| Sale (> 1 year) | Sold more than a year after vest | Long-term capital gains | Gain/loss over vest FMV |

Employer withholding often does not match your actual tax rate

Here’s where many people get tripped up: employer withholding on RSUs may not line up with what they may actually owe.

Most employers withhold federal taxes on RSU vesting at a flat 22% for vests under $1 million, or 37% for amounts above $1 million in a calendar year. For many higher earners in the 32%, 35%, or 37% brackets, that 22% rate may create a shortfall in the range of 10% to 15%. Add state tax and a higher marginal rate, and the amount due at filing may be much larger than expected.

That gap may change how much cash you end up keeping after vesting. On paper, the vest may look rich. In practice, the after-tax amount may feel a lot smaller.

Concentration risk grows when your income and stock both come from the same employer

At that stage, this may stop being only a tax issue and start looking more like a portfolio risk issue.

A common rule of thumb is to keep any single stock below 10% to 15% of total investable assets. Academic research points to 20% as a level tied to much higher concentration risk. Once you’re above that line, continuing to hold may look less like a passive choice and more like an active bet on one company. And with each new vest, that concentration may grow.

Once you know how concentrated you are, the next call is whether continuing to hold still makes sense after the tax at vest has already been paid.

How RSU taxes work in practice after vesting

What your company typically does at vest: sell-to-cover, net settlement, or cash withholding

At vesting, taxes are usually handled through sell-to-cover, net settlement, or cash withholding. The method your company uses may affect how much cash you actually receive and how much stock exposure you still have after the shares vest.

Your cost basis is the vest price, not the original grant price

Your cost basis is the fair market value on the vest date, not the original grant price. If you sell the shares the same day, that sale may produce little or no capital gain or loss.

One catch: brokers often report RSU sales with a $0 cost basis. When that happens, the 1099-B may not match the income already included on your W-2, so reconciliation matters.

The holding period for long-term capital gains starts on the vest date, not the grant date. That detail may matter if you're weighing a sale now against holding long enough to qualify for the lower 15% or 20% federal long-term capital gains rate.

Employer withholding is only a prepayment. It isn't your final tax bill. For higher earners, the gap may be large. In some cases, people deal with that by increasing W-4 withholding or making quarterly estimated tax payments.

Once you know your basis, withholding, and timing, the sell-or-hold decision may come down to after-tax cash, concentration, and expected upside.

State taxes and income stacking can sharply reduce what you keep

State tax may add another layer, and RSU income stacks with salary and bonus in the same year, which may push more income into higher brackets.

That may make the after-tax benefit of holding look smaller than it first seems, especially once NIIT and single-stock concentration risk are added to the mix. That sets up the decision framework below.

A tax-aware framework for deciding whether to sell at vest or hold

RSU Sell-or-Hold Decision Framework: 3 Steps to a Tax-Aware Choice

When your RSUs vest, this three-step check may help you think through whether to sell or hold.

This framework is general educational information, not individualized tax or investment advice. Your situation may differ based on your income, state of residence, and overall financial picture. Consider consulting a qualified tax professional before making decisions.

Step 1: Calculate after-tax proceeds and check whether the cash has a better use today

Start with the math. Estimate your combined federal, state, and payroll tax rate on the vest, then subtract that from the gross value of the shares. What remains may be your actual take-home amount, and that number may shape the first part of the decision.

Then ask a plain question: does that cash have a better use today than the stock? An underfunded emergency fund, high-interest debt, tuition, or a home down payment may all be concrete uses that might improve your household's financial position right away. If the after-tax proceeds may clearly fill one of those gaps, selling at vest may often make sense - not because the stock is bad, but because the cash may be more useful now.

If withholding appears short, selling at vest and setting cash aside for the tax bill may be the default move.

If cash needs don't settle it, look at concentration next.

Step 2: Measure employer-stock concentration before making an upside case

Next, look at how much of your portfolio may already depend on your employer. Add up vested shares, unvested grants, and any ESPP holdings. A single-stock position above roughly 10% to 15% of liquid net worth may be viewed as a concentration issue, and 20%+ may be a clear red flag.

| Concentration level | What it means | Default action |

|---|---|---|

| 0% to 5% | Modest exposure; risk may be manageable | Hold only with a clear thesis |

| 5% to 10% | Near common diversification limits | Use a written policy |

| 10% to 20% | Meaningful concentration | Sell at vest by default |

| 20%+ | Balance sheet tied to one employer | Diversify quickly |

Holding may add stock risk to the job risk you may already carry.

If exposure still looks manageable, the next question is simple: would you buy the stock fresh today?

Step 3: Compare the case for holding against the cost of income tax already paid

If your cash needs are covered and concentration looks manageable, ask: Would you buy this stock today? If the answer is no, holding may be more behavioral than analytical.

Holding does not undo the vest-date tax.

| Factor | Sell at vest | Hold after vest |

|---|---|---|

| Taxes | Near-zero capital gain; cost basis equals vest-day FMV | Potential long-term capital gains treatment on future appreciation |

| Concentration risk | Eliminates idiosyncratic single-stock risk | High correlation with salary and career |

| Complexity | Clean audit trail; simpler tax filing | Requires tracking cost basis lots and holding periods |

| When it makes sense | Default for most; high concentration; immediate cash needs | Low concentration; known lower-bracket year; charitable intent |

Hold only with a clear, written reason. Hold only by choice, not by default.

That may give you a policy you can repeat at each vest date.

Apply the framework to common RSU situations and build a repeatable policy

Use the same three checks here: cash need, concentration, and conviction. That keeps each case tied to one framework instead of treating every vest like a brand-new puzzle.

Hypothetical pattern: high earner with large upcoming vests and a volatile stock

A $500,000 salary and $400,000 of RSUs may leave a $50,000+ tax gap, since withholding is often 22% while the marginal rate may be 32%–37%. In a setup like that, selling at vest may make sense when the tax bill and concentration risk may outweigh the stock’s upside.

When salary, bonus, and RSUs all come from the same employer, selling at vest may be the cleanest move. Some people sell most or all shares at vest, set aside enough cash to cover the withholding gap, and move the rest into a diversified portfolio.

Hypothetical pattern: moderate grants, manageable concentration, and a defined reason to hold some shares

The other case looks different: a smaller position and a clear, written reason to hold. If the position stays within your concentration limit, a partial hold may be defensible.

In that setup, some people sell enough shares to stay within their concentration limit and hold only a small tranche. The key idea is simple: hold by rule, not by default.

Conclusion: Set your RSU policy before the next vest date

Decide before vest day. Turn the framework into a rule before the next vest date.

Write down:

- Your concentration limit

- Your default sell percentage

- Your tax-withholding plan

FAQs

How do I estimate my RSU tax shortfall?

Compare your actual marginal tax rate with the flat federal supplemental withholding rate your employer used, which may be 22% in many cases. If your marginal rate may be higher, often in the 32% to 37% range for higher earners, there may be a withholding gap.

A simple way to estimate it: apply your total marginal tax rate, including federal, state, and any Medicare surcharges, to the fair market value of the vested shares. Then subtract the amount your employer already withheld. What’s left may give you a rough estimate of your remaining tax liability.

Should I sell all or only some shares at vest?

This may be more of a portfolio call than a tax one.

Why? The main tax event usually happens at vesting. So if shares are sold right away, that sale may create little extra capital gain or loss.

A simple way to think about it: use the fresh-buy test. If this same value showed up as cash today, would you buy that much of your employer’s stock?

If the answer may be no, selling may reduce over-concentration.

For some people, selling all shares at vest may serve as a disciplined default. Holding some shares may also make sense, but usually only if that choice fits a written, intentional allocation.

What if my company stock drops after vesting?

If your company stock drops after vesting, you may end up with a capital loss. That loss is usually based on the stock’s fair market value on the vesting date, because that amount becomes your cost basis.

Here’s the key distinction: the tax tied to vesting is already set by that vest-date value. So if the stock falls later, that decline does not reduce the ordinary income tax from vesting.

What the drop may do is create a capital loss that may be used in a couple of ways:

- It may offset capital gains

- If losses are higher than gains, up to $3,000 per year may be deducted against ordinary income

- Any amount above that may be carried forward to future tax years

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.