If you receive RSUs as part of your compensation, taxes are due as soon as your shares vest. The sell to cover strategy helps you manage this by automatically selling a portion of your vested shares to cover taxes. While convenient, it doesn't always cover your full tax liability, especially if you're in a higher tax bracket. Here's what you need to know:

- RSU Taxation: RSUs are taxed as ordinary income when they vest, based on their fair market value (FMV). Employers withhold taxes at a flat rate (22% for most, 37% for income over $1M), but this may not match your actual tax rate.

- Sell to Cover: Your employer sells enough shares to cover taxes, and you keep the remaining shares. This avoids out-of-pocket tax payments but may leave a shortfall.

- Additional Tax Considerations: Federal, state, and payroll taxes (like Social Security and Medicare) also apply, and under-withholding could lead to penalties.

- Key Decisions: Decide whether to sell more shares or hold onto them, balancing tax obligations with your investment goals.

The sell to cover method simplifies tax payments but requires careful planning to avoid surprises at tax time. Tools like Mezzi can help you track your RSU vesting schedules and sales, estimate tax gaps, and manage your RSU strategy effectively.

Huge tax bill? Your sell-to-cover election on your RSUs is likely the problem

What Are Restricted Stock Units (RSUs)?

Restricted Stock Units, or RSUs, are a type of equity compensation where your employer commits to giving you company shares once specific conditions are met - typically staying employed for a certain period. Unlike stock options, which require you to pay a "strike price" to acquire shares, RSUs are awarded at no cost to you. They’re essentially a promise of future ownership.

"RSUs represent company shares, but they come with a catch: they are subject to vesting over time. You earn them gradually over time or after hitting specific performance milestones." - Jacob Dayan, CEO, Community Tax LLC

RSUs are widely used in industries like tech, finance, and healthcare as part of compensation packages. They help companies attract skilled employees and encourage them to stay for the long term. From the employee's perspective, RSUs can be a way to build wealth, especially if the company’s stock value increases. However, there’s a catch: if you leave the company before your shares vest, you lose any unvested units.

Let’s explore the basics of RSUs and how they vest over time.

RSU Basics

RSUs function as a deferred stock bonus. On your grant date, your employer assigns you a specific number of units. However, you don’t own these shares yet. They only become yours after they vest, following a set schedule. Until then, they remain a promise of future ownership.

One advantage of RSUs compared to stock options is that they retain value even if the stock price drops, as long as the company remains solvent. Stock options, on the other hand, can become worthless if the stock price falls below the strike price. Additionally, RSUs don’t trigger the Alternative Minimum Tax (AMT), which can make tax planning simpler.

Grasping these basics is essential to understanding how RSUs eventually convert into actual shares.

How RSUs Vest

Vesting refers to the process of earning ownership of your RSUs. The most common vesting arrangement is graded vesting, where shares are released incrementally over time. For example, you might receive 25% of your RSUs each year over a four-year period. Another approach is cliff vesting, where all your shares vest at once after a specific time - such as one year.

In private companies, you might encounter double-trigger vesting, which requires both time-based service and a liquidity event, like an IPO or acquisition, for the shares to vest. Knowing the details of your vesting schedule is crucial for managing your finances and preparing for tax obligations.

How RSUs Are Taxed at Vesting

RSU Tax Withholding Rates and Obligations Breakdown

When RSUs vest, they are taxed as ordinary income based on their fair market value (FMV) at the time of vesting. This event is referred to as "forced income recognition".

"RSUs are taxed as ordinary income when they vest - not when they are granted." - Jacob Dayan, CEO, Community Tax LLC

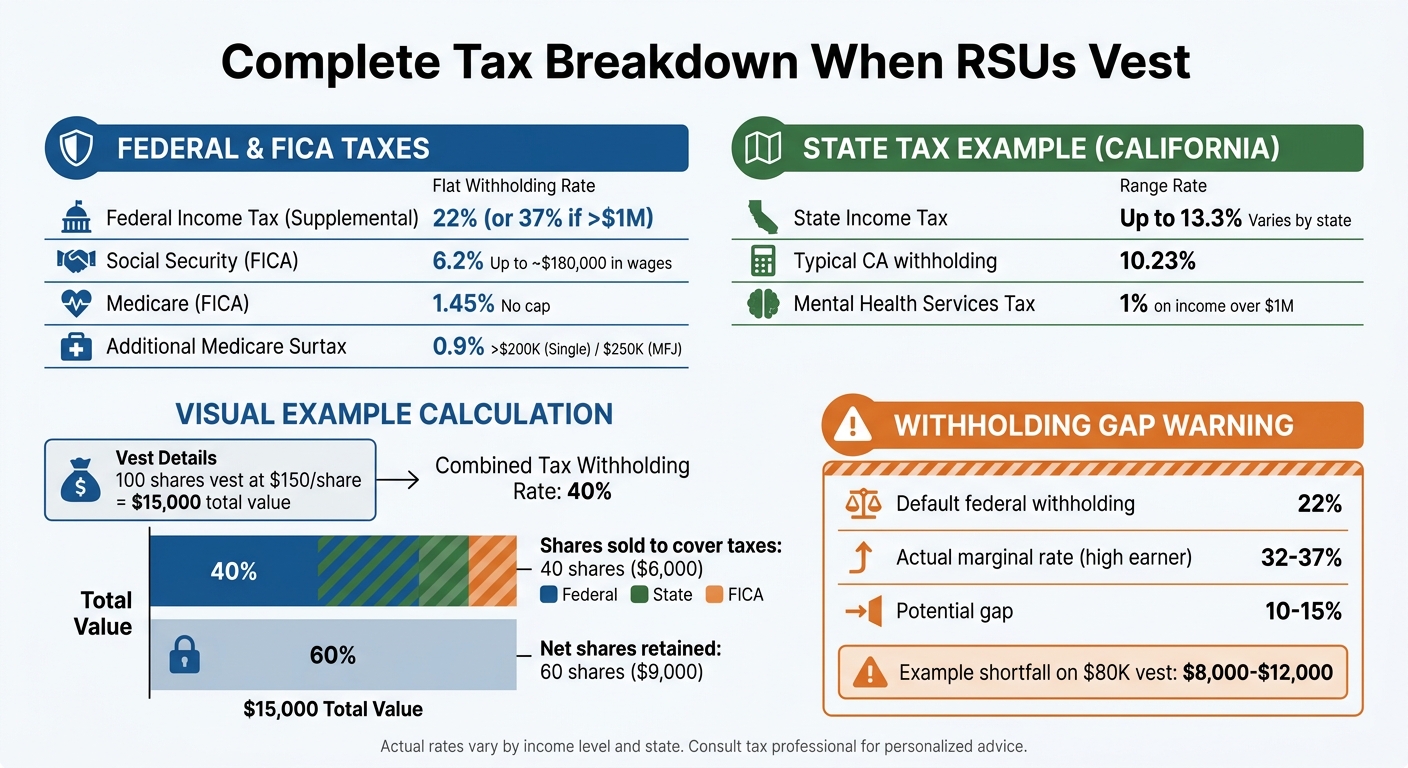

The taxable income you recognize equals the FMV of the shares at vesting. For instance, if 100 shares vest and your company's stock is trading at $150 per share, you would report $15,000 as income. This amount is included on your Form W-2 in Box 1 (Wages, tips, other compensation), Box 3 (Social Security wages), and Box 5 (Medicare wages).

Here’s a closer look at how the tax calculations and withholdings work.

Income Tax Treatment

Employers withhold income tax on RSU income at a flat rate of 22% for amounts up to $1 million and 37% for amounts exceeding that threshold. However, if you fall into a higher tax bracket, this withholding might not fully cover your tax liability. For example, if you're in the 37% tax bracket, you may owe an additional 15% when you file your taxes.

"The gap between what's withheld and what you actually owe can be thousands of dollars." - Equity Simplified

The FMV of the shares at vesting also serves as the cost basis for determining future capital gains or losses when you sell the shares.

Additional Taxes

RSU vesting triggers other taxes, including FICA taxes. Here's a breakdown:

- Social Security Tax: 6.2% applies to wages up to approximately $180,000.

- Medicare Tax: 1.45% applies to all income, with no cap.

- Additional Medicare Surtax: An extra 0.9% applies to wages exceeding $200,000 for single filers or $250,000 for those married filing jointly.

State taxes also apply, and rates vary depending on where you live. For example, in California, employers typically withhold at a 10.23% supplemental rate, but the top marginal rate can climb to 13.3%. Additionally, California imposes a 1% Mental Health Services Tax on income over $1 million.

| Tax Type | Rate | Threshold/Cap |

|---|---|---|

| Federal Income Tax (Supplemental) | 22% (or 37% if >$1M) | Flat withholding rate |

| Social Security (FICA) | 6.2% | Up to ~$180,000 in wages |

| Medicare (FICA) | 1.45% | No cap |

| Additional Medicare Surtax | 0.9% | >$200K (Single) / $250K (MFJ) |

| State Income Tax (e.g., CA) | Up to 13.3% | Varies by state |

These tax obligations - federal, state, and FICA - paint a comprehensive picture of what you might owe when your RSUs vest. To avoid underpayment penalties, it’s a good idea to estimate your marginal tax rate and set aside funds for any shortfall beyond the 22% withholding. You might also want to adjust your Form W-4 to increase withholding on your regular paycheck or consider making quarterly estimated tax payments.

What Is the Sell to Cover Strategy?

The sell to cover strategy provides a straightforward way to handle the tax burden that comes with RSU vesting. Instead of requiring you to dip into your cash reserves, this approach automatically sells a portion of your newly vested shares to cover the taxes owed. Once the taxes are paid, the remaining shares - referred to as net shares - are deposited into your brokerage account. These shares are yours to hold or sell as you see fit.

The proceeds from the sold shares typically cover federal income tax, applicable state income tax, and payroll taxes such as Social Security and Medicare. In states with higher tax rates, like California, combined withholdings can reach around 40% of the total vested value. Many public companies make sell to cover the default option, eliminating the need for manual steps or out-of-pocket payments. To understand it better, let’s break down how this process works during RSU vesting.

How the Strategy Works

When your RSUs vest, your employer calculates the fair market value (FMV) of your shares on the vesting date. They then determine the total tax withholding - including federal, state, and payroll taxes - and sell just enough shares at the market price to cover this amount. The remaining shares are transferred to your brokerage account.

For instance, imagine 100 shares vest at $150 per share, and your combined withholding rate is 40%. Your employer would sell 40 shares to cover $6,000 in taxes, leaving you with 60 shares. Unlike a same-day sale, where all shares are sold for cash, sell to cover allows you to retain a portion of your shares, maintaining your investment in the company.

Benefits of Sell to Cover

One of the key benefits of sell to cover is how it simplifies cash flow management. You don’t need to worry about finding cash to pay taxes when your RSUs vest - everything happens automatically, ensuring you remain tax compliant without added stress.

Another advantage is that it lets you keep a stake in your company’s future. Holding onto the remaining shares gives you the opportunity to benefit from potential stock price increases. Additionally, because the sale is automatic and non-discretionary, it’s generally allowed even during blackout periods for company insiders. This combination of convenience and flexibility makes sell to cover an appealing option for many employees, while also paving the way for a deeper dive into its tax implications.

Tax Implications of Sell to Cover

Understanding how sell to cover affects your taxes is essential for managing RSU-related obligations. While sell to cover simplifies paying taxes, the amounts withheld may not fully cover what you owe. This often leaves a gap that you'll need to address when filing your return. Let’s break down federal and state withholding rates and the potential risks of under-withholding.

Federal and State Tax Withholding Rates

When RSUs vest, your employer withholds taxes based on the supplemental wage rate. For federal income tax, this rate is a flat 22% on earnings up to $1 million in a calendar year. If your supplemental income exceeds $1 million, the rate jumps to 37%. Additionally, standard FICA taxes apply, along with a 0.9% Medicare surtax on wages over $200,000 for single filers or $250,000 for married couples filing jointly.

State taxes further complicate the picture. For instance, in California, combined federal, payroll, and state supplemental tax rates can total around 40%. Meanwhile, states like Idaho may withhold at a much lower rate of approximately 5.3% on supplemental wages.

Under-Withholding Risks

The federal supplemental rate of 22% often falls short of covering your actual marginal tax rate. Take, for example, a single filer earning $180,000 with $80,000 in RSU vesting. At a marginal tax rate of 32%, this individual faces an $8,000 shortfall in federal taxes alone. Add state taxes - such as California's 10.23% withholding compared to a 13.3% marginal rate - and the total underpayment for a single vesting event could reach approximately $10,456.

"If your real marginal tax rate is closer to 32%, 35%, or even 37%, but your company only withholds 22%, you are effectively borrowing money from the IRS until you repay it in April." - OnePoint BFG Wealth Partners

To avoid penalties, the IRS Safe Harbor rule requires you to pay at least 90% of the current year's tax or 100% of the prior year’s total tax (110% if your adjusted gross income exceeded $150,000). You can address under-withholding by adjusting your W-4 to increase regular paycheck withholding, making quarterly estimated tax payments, or setting aside cash from each vesting event to cover the gap. Tools like Mezzi can simplify this process by helping you calculate and track these discrepancies, ensuring you’re better prepared for tax season.

Next, we’ll explore how sell to cover compares to holding your vested shares, helping you weigh the options for your financial objectives.

Sell to Cover vs. Holding Vested Shares

When your RSUs vest, you face a choice: use a sell to cover approach or pay taxes out-of-pocket to keep all your shares. Both options trigger ordinary income tax at vesting, but they differ in how you handle the tax bill and the impact on your portfolio.

Sell to cover keeps your cash untouched. With this method, your employer sells 22% to 40% of your shares to cover taxes, leaving you with 60% to 75% of your vested shares without needing to use personal funds. On the other hand, holding all shares requires a significant cash outlay. You’ll need to pay the full tax bill yourself, which can be a hefty sum. For instance, in California, an $80,000 RSU vest could leave you needing $32,000 in cash for taxes.

The key question is: Does holding more company stock align with your financial goals? As OnePoint BFG Wealth Partners puts it, "If I had the after-tax value in cash, would I buy this stock?". If the answer is no, holding all the shares might expose you to unnecessary risk. Retaining all shares means your portfolio becomes more concentrated in a single company - the same one that also pays your salary and benefits. This concentrated stock risk can magnify if the stock underperforms.

Strategy Comparison

Here’s a breakdown of the differences between sell to cover and holding all vested shares:

| Feature | Sell to Cover | Holding All Vested Shares |

|---|---|---|

| Cash Flow | No personal outlay; taxes are paid by selling shares | Requires substantial cash to pay taxes |

| Tax Efficiency | Immediate withholding satisfied; future gains taxed as capital gains | Potential for long-term capital gains on the full grant |

| Concentration Risk | Reduced; exposure decreases by the tax percentage (about 25–40%) | High; 100% of the grant value depends on company performance |

| Volatility Exposure | Lower; some value is secured for taxes | Higher; the entire grant value fluctuates with the market |

| Upside Potential | Retained on 60–75% of shares | Retained on 100% of vested shares |

Both strategies come with a potential withholding gap. For example, if your marginal tax rate is 32% but only 22% is withheld, you’ll owe additional taxes later. The choice ultimately boils down to your cash flow preferences and your comfort level with company stock exposure. This sets the stage for understanding how to implement a sell to cover approach effectively.

How to Use Sell to Cover: Step-by-Step

Steps to Execute Sell to Cover

When your RSUs vest, the process typically involves calculating the fair market value (FMV) of the shares, selling enough to cover taxes, and transferring the remaining shares into your account. However, the default 22% federal withholding may not align with your actual tax liability. To avoid surprises, it’s a good idea to estimate your total tax liability before vesting. Use a tax calculator to compare the default 22% withholding to your actual marginal tax rate, including state taxes.

For instance, if you’re in a higher tax bracket - say 32% - the default withholding might leave you with a shortfall. On an $80,000 vest, this could mean an $8,000 gap, which could result in penalties unless addressed. To cover the difference, you might increase withholding on your regular paycheck by updating Form W-4 or make quarterly estimated tax payments using IRS Direct Pay.

After vesting, review your tax documents to ensure everything is accurate. Pay close attention to the cost basis reported on Form 1099-B. Sometimes brokerages report a $0 cost basis for shares sold to cover taxes, which could lead to overpaying taxes if not corrected. You can adjust this on Form 8949. David Snider, CEO of Harness, explains:

"If the cost basis for these shares (the original value) is the same as the price on the day they vested, you shouldn't owe any extra tax on this sale since it was done to cover taxes".

Double-check that the cost basis matches the FMV at vesting to avoid paying taxes twice on the same income.

Using Mezzi for RSU Tax Optimization

Mezzi simplifies the process of managing RSU-related taxes, offering tools that go beyond tax season. By syncing your financial accounts, Mezzi gives you a full picture of your RSU tax situation, helping you plan more effectively. It can alert you if an upcoming RSU vest might push you into a higher tax bracket or create a withholding gap. You can even ask specific questions like, "Will my April RSU vest trigger estimated tax requirements?" and get tailored answers based on your actual financial data.

Another advantage of Mezzi is its ability to monitor for potential wash sale risks. If you’re selling other company shares at a loss near the time your RSUs vest, the automatic acquisition of RSUs could trigger wash sale rules within the 30-day window. This might disallow your loss deduction. Mezzi tracks your accounts to identify and help you avoid these risks, ensuring accurate tax reporting. Unlike traditional advisors, who only see the assets they manage, Mezzi provides a broader view by connecting to all your accounts.

Common Mistakes and How to Avoid Them

Mistakes to Watch Out For

One common misconception is that a sell-to-cover transaction fully addresses tax liabilities. Employers generally withhold federal taxes at a flat supplemental rate of 22%. However, for individuals in higher marginal tax brackets - 32%, 35%, or 37% - this can leave a significant shortfall. For instance, if you have an $80,000 vest, the gap could be as much as 15%, resulting in an additional $12,000 in taxes owed.

State tax withholdings can also fall short. For example, California applies a withholding rate of 10.3%, which may not align with the state's higher effective tax rates. On top of this, high earners need to account for the 0.9% Medicare surtax, which can further increase their tax burden.

Another issue arises with the cost basis reported on Form 1099-B. If not verified, this could lead to double taxation.

Lastly, the sell-to-cover approach leaves you with retained shares, which can lead to an overly concentrated portfolio. Without careful monitoring, this concentration could increase your financial risk.

How Mezzi Helps Prevent These Errors

Mezzi’s AI-powered platform is designed to address these challenges head-on, helping you avoid costly mistakes.

The platform identifies potential withholding gaps well before tax season. By connecting all your accounts, Mezzi evaluates whether the default 22% withholding will adequately cover your actual tax liability, factoring in your overall income, including bonuses and other earnings. If an upcoming vest could push you into a higher tax bracket or require estimated tax payments, Mezzi sends proactive alerts.

Mezzi also keeps an eye on concentration risk across your portfolio. Unlike traditional advisors who only assess the assets they directly manage, Mezzi connects to all your accounts. It flags when your company stock exceeds recommended levels, helping you maintain a balanced portfolio. Additionally, it monitors for wash sale triggers, notifying you if selling other shares at a loss near a vest date might disallow your deduction. With these tools, Mezzi ensures you’re equipped to make well-informed financial decisions.

Conclusion

The sell-to-cover approach allows you to automatically sell a portion of your vested shares to handle tax obligations without needing to pay out of pocket. At the same time, it lets you retain shares to potentially benefit from future growth. As OnePoint BFG Wealth Partners explains:

"Sell-to-cover is a cash flow tool, not a tax strategy. It does not absolve you from responsibility for the withholding gap."

If you're in a higher tax bracket (32%, 35%, or 37%), you may still encounter a withholding shortfall when tax season arrives. Other factors, such as state taxes, the 0.9% Medicare surtax, and the risks associated with holding too much company stock, can further complicate your financial situation. To avoid being taxed twice on the same income, it's essential to confirm your cost basis using Form 1099-B. All of this highlights the importance of careful RSU management as part of a broader investment strategy.

Mezzi offers tools to simplify this process by consolidating all your accounts into a single, easy-to-navigate dashboard. It can identify potential withholding gaps before they become surprises at tax time. With its scenario analysis feature, you can explore different strategies - like selling shares immediately or holding them for the long term - and see the potential outcomes before making a decision.

Each RSU vesting event represents an opportunity to make a thoughtful investment decision. By incorporating proactive tax planning, you can align these decisions with your broader financial goals. Mezzi’s AI-powered tools provide insights that help you navigate these choices, offering guidance without the typical 1% AUM fee. With Mezzi, you can shift from simply reacting to tax obligations to taking a more strategic approach to managing your wealth.

FAQs

How do I estimate my RSU withholding shortfall before vesting?

To figure out your RSU withholding shortfall, start by determining the tax liability at the time your shares vest. Multiply the number of vested shares by the current stock price to get their total value. Then, apply your total tax rate - which includes federal, state, and local taxes - to this amount. Compare the result to your employer’s withholding rate, which is usually between 22% and 25%. If your total tax rate exceeds the withholding rate, you might need to set aside extra funds to cover the gap in taxes.

When should I sell more than the sell-to-cover amount?

If the automatic sell-to-cover amount doesn’t fully address your actual tax liability, you may want to sell more shares. This shortfall can occur because withholding rates are typically flat and might not reflect higher income brackets. By selling additional shares, you could reduce the risk of facing unexpected tax bills and better ensure your full tax obligations are met.

How do I avoid double taxation from an incorrect RSU cost basis?

To help prevent paying taxes twice on your RSUs, it's important that your brokerage records and tax filings correctly reflect the cost basis of your shares. The cost basis generally aligns with the fair market value (FMV) of the shares at the time they vest, which is typically reported as income on your W-2. If this information is incorrect, you may need to either amend your tax return or provide documentation to support the accurate cost basis. Tools like Mezzi are designed to assist with tracking taxes and ensuring your reporting is accurate, which may help reduce potential errors.

Disclosures:

- This content is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.

- Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.

- Savings and performance examples are hypothetical and for illustrative purposes only. Actual results will vary based on individual circumstances, portfolio composition, market conditions, and fees.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.