High-income earners face unique challenges in managing wealth, from reducing tax burdens to avoiding over-concentration risks in single assets or sectors. Here's a quick overview of strategies that may help address these issues:

- Tax Efficiency: Tools like tax-loss harvesting and backdoor Roth IRA contributions may reduce tax obligations.

- Diversification: Avoid overlapping investments (e.g., ETFs with similar holdings) and consider spreading assets across sectors and regions.

- AI Tools: Platforms like Mezzi may simplify portfolio management by identifying overlaps, rebalancing assets, and providing tax insights.

- Alternative Investments: Private equity, real estate, and Qualified Opportunity Zones may offer additional opportunities for growth and tax deferral.

- Account Optimization: Choosing the right accounts (Roth, traditional, or taxable) for specific investments may improve tax outcomes.

These strategies aim to help high-income earners maximize returns while managing risks and taxes. Keep in mind that any financial decisions should be made with the guidance of a qualified professional.

Optimal Order of Investing for High Income Earners [Wealth Lawyer Explains]

Building a Diversified Portfolio with Modern Portfolio Theory

Modern Portfolio Theory (MPT) aims to balance risk and return by focusing on reducing the correlation between asset classes. For high-income earners juggling multiple accounts - such as 401(k)s, IRAs, and taxable brokerages - achieving true diversification can be tricky. Often, the same stocks appear in different funds, leading to overlapping exposures.

Take this example: you might own both VOO (S&P 500) and VTI (Total Market), assuming they offer diversification. However, these funds share many of the same stocks, creating duplicate holdings that dilute diversification. Similarly, combining funds like VOO and QQQ could mean 30–40% of your portfolio is concentrated in mega-cap tech stocks without you realizing it.

"The hidden concentration is such a good feature. Particularly for those in tech who already hold significant amount of company stock. They often forget those same holdings make up a large % of the indexes they hold."

– Andre Nader, Author of FAANG FIRE

Achieving real diversification means digging deeper than fund names to analyze stock-level exposure. Mezzi’s AI rebalancing tools make this process easier by identifying overlaps and helping you refine your portfolio for better diversification.

Using Mezzi's X-Ray Tool to Spot Overlaps

Mezzi’s X-Ray tool offers a clear view of your holdings by aggregating data from all connected accounts. This comprehensive approach reveals duplicate stocks across different funds - something single-institution views often miss.

"I discovered individual stock exposure I didn't even know I had. Turns out my 'diversified' ETF portfolio had significant overlap, with some companies appearing across multiple funds."

– Nishant Jayant, Meta Engineer

The tool also tracks portfolio shifts in real time. For example, if a single stock like NVDA grows to represent 18% of your portfolio, Mezzi’s alerts notify you about the potential concentration risk. This feature is particularly useful for tech employees, who might already hold company stock through RSUs while unknowingly owning the same stocks in index funds, amplifying concentration risk.

If your overlap exceeds 70%, it may signal the need to consolidate or replace some funds. Overlap between 40% and 70% suggests reviewing top holdings to avoid heavy sector exposure. On the other hand, overlap below 40% generally indicates a healthier level of diversification. Beyond identifying overlaps, Mezzi also helps guide sector and geographic diversification for a more balanced portfolio.

Diversifying Across Sectors and Regions

Diversification isn’t just about reducing overlap - it’s also about spreading investments across industries and global markets. This approach helps shield your portfolio from localized economic shifts or sector-specific downturns. Mezzi provides tools to monitor exposure across global regions - like the Americas, Europe, and Asia - and sectors such as Energy, Technology, and Communication Services. This ensures your allocations align with your risk tolerance and long-term goals.

Sometimes, what seems like a globally diversified portfolio might turn out to be overly concentrated in one region, such as the U.S. If that’s the case, Mezzi can help you identify opportunities to rebalance into international or emerging markets for better global coverage.

The platform also delivers daily updates on your asset allocation - covering categories like cash, U.S. stocks, and bonds - and compares them to your chosen benchmarks. This ongoing monitoring helps ensure no single area grows disproportionately, reducing the risk of undermining your overall diversification strategy.

Tax Reduction Strategies for High-Income Earners

For those in the 32%–37% tax brackets, managing tax strategies throughout the year can help preserve wealth. Mezzi's tools are designed to complement these efforts, helping users manage portfolios while potentially improving tax outcomes.

Tax-Loss Harvesting with Mezzi

Tax-loss harvesting involves selling investments at a loss to offset capital gains, which may reduce taxable income by up to $3,000 annually. The strategy works best when implemented consistently throughout the year. Mezzi actively monitors portfolios to identify harvesting opportunities as market conditions change, aiming to help investors take advantage of these moments before they pass.

One challenge with tax-loss harvesting is avoiding a wash sale, which occurs when a "substantially identical" security is bought within 30 days before or after selling it at a loss. This can be especially tricky for investors managing multiple accounts. Mezzi simplifies this by tracking all connected accounts and flagging potential wash sale violations.

For example, selling VOO in one account while contributing to VTI in another could trigger a wash sale. Mezzi monitors such overlaps, alerts you to conflicts, and notifies you when the 30-day restriction period ends.

Backdoor Roth IRA and Mega Backdoor Contributions

High earners often exceed Roth IRA income limits, which start phasing out at $153,000 for singles and $242,000 for married couples in 2026. The backdoor Roth IRA strategy can work around these limits. It involves contributing after-tax dollars to a traditional IRA and then converting those funds to a Roth IRA shortly after.

Timing is key: converting funds within days minimizes taxable gains during the transition. To reduce risk, funds can be held in a money market or stable value fund during this period. The 2026 annual IRA contribution limit is $7,500, or $8,600 for those 50 or older.

The mega backdoor Roth strategy allows for even larger contributions. If your employer's 401(k) plan permits after-tax contributions beyond the standard deferral limit, you could contribute up to the total 401(k) plan limit of $72,000 for 2026 (or $80,000 for those 50+), then convert those funds to a Roth 401(k) or roll them into a Roth IRA.

"The mega Roth conversion bypasses those limits entirely, allowing you to funnel tens of thousands of dollars annually into a Roth environment – far more than the standard $7,000 Roth IRA contribution limit."

– David Evans, Insero Advisors

Before pursuing a mega backdoor Roth, confirm whether your 401(k) plan allows after-tax contributions and either in-service distributions or in-plan Roth conversions, as not all plans offer these options. Additionally, consider the pro-rata rule for backdoor IRAs. The IRS calculates the taxable portion of a conversion based on all traditional, SEP, and SIMPLE IRA balances. If you have existing pre-tax IRA funds, part of your conversion could be taxable. To address this, some investors roll pre-tax IRA balances into their 401(k) before executing a backdoor Roth conversion.

Choosing the Right Account Type: Roth vs. Traditional vs. Taxable

Selecting the right account for each investment is a key part of managing taxes effectively.

Where you hold your investments - Roth, traditional, or taxable accounts - depends on factors like your current tax bracket, expected retirement income, and state tax considerations. Mezzi evaluates your entire financial picture to recommend the most tax-efficient placement for your assets.

-

Traditional accounts: These accounts may reduce taxable income at higher marginal rates now, with withdrawals taxed later. If you anticipate being in a lower tax bracket during retirement, traditional accounts may provide immediate tax benefits.

"For married filing jointly couples currently and expected to remain in the top federal income tax bracket of 37%... pre-tax/traditional contributions while working likely make sense."

– Tim Kingsbury, CFP®, Veris Wealth Partners - Roth accounts: These accounts can be advantageous if you expect to remain in the same or a higher tax bracket in retirement. Roth IRAs also have no Required Minimum Distributions (RMDs) during your lifetime, and withdrawals are tax-free. Starting in 2026, individuals earning over $150,000 who are 50 or older will be required to allocate 401(k) catch-up contributions to Roth accounts.

- Taxable brokerage accounts: These accounts offer flexibility, as funds can be accessed before age 59½ without penalties. Long-term capital gains are taxed at preferential rates (0%, 15%, or 20%, depending on income). Additionally, taxable accounts allow for strategies like tax-loss harvesting, which are not available in retirement accounts.

Mezzi helps balance contributions across these account types, enabling strategic withdrawals to manage tax brackets in retirement. For example, you might use traditional IRA withdrawals to fill lower tax brackets and tap into Roth or taxable accounts for additional spending to avoid higher brackets. By aligning these strategies with your broader financial goals, Mezzi supports efficient wealth management.

Compliance Disclaimer: Mezzi is not a tax advisor. The information provided is for educational purposes only and should not be construed as tax advice. Consult a qualified tax professional regarding your specific situation.

Portfolio Management Techniques for High Earners

For individuals with higher incomes, the way you adjust your investments can play a big role in shaping your after-tax returns. This makes thoughtful portfolio management a key part of building wealth. Traditional rebalancing methods, like rebalancing on a set schedule (quarterly or annually), often fail to consider market fluctuations or the tax consequences of trades. Newer strategies, powered by AI, aim to monitor portfolios more closely, finding opportunities to adjust holdings in ways that may reduce taxes while keeping your investments aligned with your goals.

AI-Driven Portfolio Rebalancing

Mezzi offers daily monitoring of your connected accounts, keeping an eye on how your investments are allocated and how the markets are behaving. If your portfolio drifts away from its target allocation - for instance, if the stock portion of your portfolio grows from 70% to 75% - Mezzi evaluates whether rebalancing right away or waiting could help limit potential tax costs from selling assets that have gained value.

Unlike traditional methods that rely on fixed thresholds, AI-driven rebalancing takes into account various factors, such as your current tax bracket, annual income, opportunities for tax-loss harvesting, and wash sale restrictions across accounts. For instance, if rebalancing your taxable account might result in significant capital gains taxes, Mezzi could suggest offsetting those gains by harvesting losses from other positions. Alternatively, it might recommend making adjustments within a Roth IRA, where trades don't create tax obligations.

Mezzi is also designed to handle specific challenges, like managing legacy holdings, concentrated employer stock, or portfolios with ESG considerations. If it identifies a rebalancing opportunity, Mezzi provides suggestions for the most tax-efficient way to proceed, leaving the final decision in your hands. It also monitors for wash sale risks after trades and alerts you when restriction periods are over. This tailored approach aims to help high earners optimize their after-tax returns.

Direct Indexing for Customization and Tax Efficiency

Direct indexing is another strategy that can enhance both tax efficiency and personalization in portfolio management. Instead of buying an ETF or mutual fund that represents an index, direct indexing involves owning the individual stocks within that index, such as the S&P 500. This method provides two key advantages for high-income investors: the ability to harvest tax losses at the individual stock level and the flexibility to customize your portfolio.

The tax benefits can be noteworthy. For example, in 2025, over 85% of S&P 500 stocks experienced dips of at least 15% at some point during the year, creating opportunities to harvest losses throughout the year. For someone in a 41% tax bracket, harvesting a $25,000 loss could result in $10,200 in tax savings. Systematic tax management through direct indexing may add an additional 1% to 2% in after-tax returns annually, a concept often referred to as "tax alpha".

"Direct indexing replaces the one-size-fits-all nature of commingled investing with tailored, stock-level management."

– Jeremy Milleson, Director, Investment Strategy, Parametric Portfolio Associates

Direct indexing also allows for a level of customization that ETFs can't match. You can exclude specific stocks to avoid duplicating concentrated positions, apply ESG filters to reflect your values, or gradually diversify appreciated holdings while minimizing immediate tax consequences. However, it’s worth noting that direct indexing comes with added complexity. It typically requires a minimum investment of $250,000 and may involve higher management fees compared to passive ETFs. Additionally, it works best in taxable accounts, as tax-loss harvesting doesn’t apply to 401(k)s and IRAs.

Mezzi can help determine if direct indexing suits your financial situation and guide you through the process. Its X-Ray tool identifies overlapping holdings in your ETFs and individual stocks, highlighting areas where you might be paying duplicate fees. Once you transition to direct indexing, Mezzi monitors your portfolio daily to capture tax-loss harvesting opportunities and ensure compliance with wash sale rules across all your accounts.

Compliance Disclaimer: Mezzi is not a tax advisor. The information provided is for educational purposes only and should not be construed as tax advice. Consult a qualified tax professional regarding your specific situation.

Alternative Investments for Portfolio Expansion

After establishing a solid base with stocks and bonds, alternative investments could provide an additional layer of diversification and may improve after-tax returns. These assets - like private equity and real estate - often include an illiquidity premium of 1-5%, which compensates investors for locking up their capital for extended periods. For context, ultra-high-net-worth investors with portfolios exceeding $30 million typically allocate around 20% of their investments to alternatives. Below, we’ll explore how private equity, real estate, and Qualified Opportunity Zones could diversify and enhance your portfolio.

Private Equity and Venture Capital

Private equity and venture capital allow investors to gain exposure to high-growth companies before they go public. These investments often come with extended lockup periods but can deliver higher returns compared to traditional asset classes. Over the five years ending in 2024, private equity was the only alternative asset class to outperform the S&P 500, with the Cambridge Associates U.S. Private Equity Index reporting an annualized return of 15.80%, compared to 14.5% for the S&P 500. Venture capital, on the other hand, has the potential to yield returns exceeding 20%, though investors typically need to commit their funds for 8-12 years.

Accessing these opportunities generally requires accredited investor status, which involves meeting specific financial criteria: either a net worth of at least $1 million (excluding your primary residence) or an annual income of $200,000 or more. Traditional private equity funds often require a contribution of $250,000 to $1 million, but smaller-scale options, such as search funds that support entrepreneurs acquiring small businesses, may have minimums as low as $25,000 to $50,000. Additionally, venture capital investors should consider Qualified Small Business Stock (QSBS) provisions, which may exclude up to 100% of capital gains (up to $10 million) from federal taxes.

Real Estate Investment Options

Real estate offers a range of opportunities for wealth-building, from liquid Real Estate Investment Trusts (REITs) to less liquid syndications, each with distinct risk and return profiles. Public REITs, which trade on stock exchanges, are highly liquid and typically deliver returns in the range of 8-12%. Alternatively, real estate syndications and direct property ownership provide less liquidity but aim for higher internal rates of return, often between 12-18%. Syndications, which pool investor funds to purchase larger properties, usually require minimum investments between $25,000 and $250,000.

Direct real estate ownership offers notable tax advantages, particularly for high-income earners. Strategies like depreciation and 1031 exchanges may allow investors to shield a significant portion of their returns from taxation while deferring capital gains, potentially improving overall tax efficiency.

Qualified Opportunity Zones for Tax Deferral

Qualified Opportunity Zone (QOZ) funds present a compelling strategy for deferring taxes. By reinvesting capital gains into a QOZ fund, investors may defer those taxes until either the fund is sold or December 31, 2026 - whichever occurs first. Additionally, holding the investment for at least 10 years could make all appreciation within the fund completely tax-free.

The Opportunity Zone program was made permanent under the One Big Beautiful Bill Act (OBBBA) of 2025. Moreover, Qualified Rural Opportunity Funds (QROFs) now offer an additional 30% basis step-up after a five-year holding period. These provisions complement broader tax strategies and could serve as a valuable component of a diversified portfolio.

Compliance Disclaimer: Mezzi is not a tax advisor. The information provided is for educational purposes only and should not be construed as tax advice. Consult a qualified tax professional regarding your specific situation.

How Mezzi Provides Tax-Efficient Advice

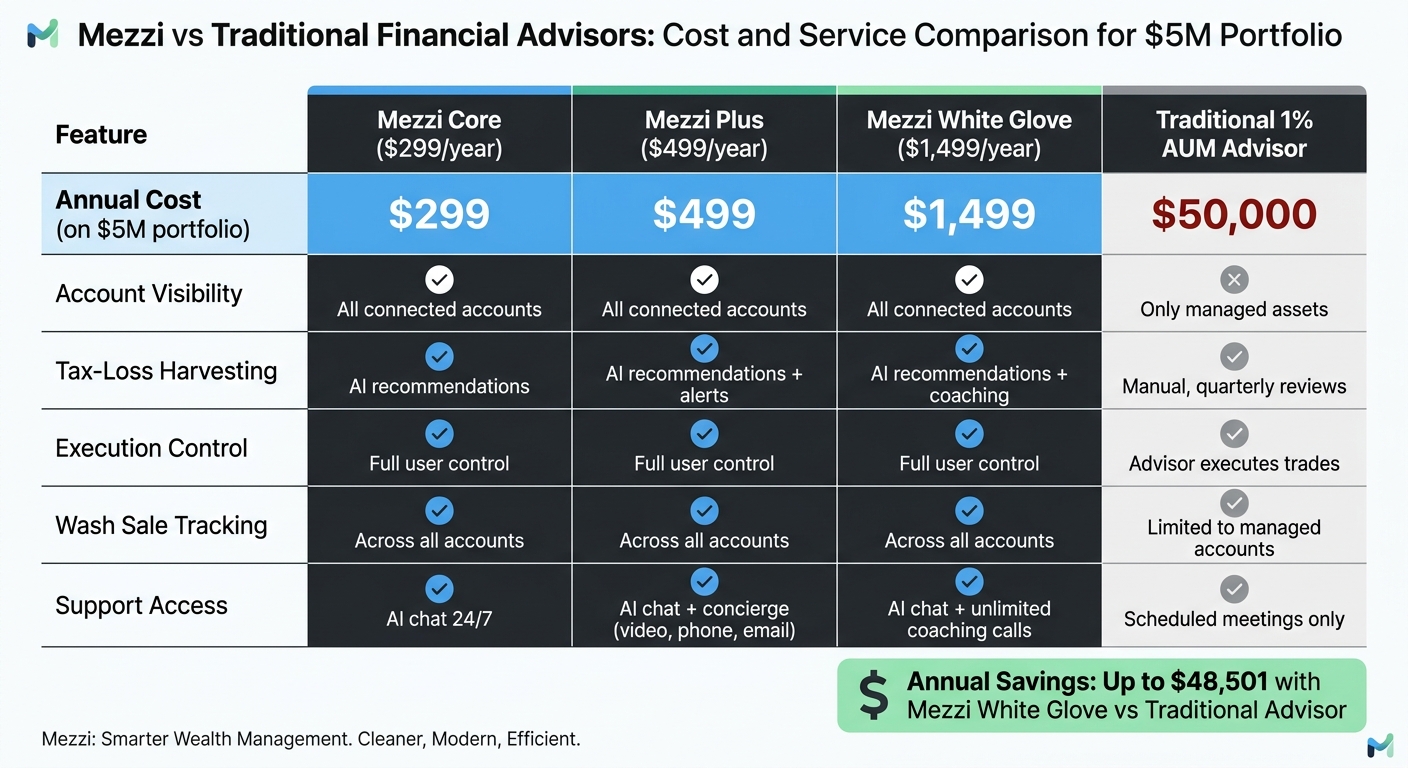

Mezzi vs Traditional Financial Advisors: Cost and Service Comparison

Mezzi combines advanced AI technology with a focus on tax efficiency, giving high-income earners tools to manage their wealth without the steep fees associated with traditional financial advisors. By using platforms like Plaid and Finicity for read-only access, Mezzi connects to over 12,000 financial institutions, offering a unified view of all your accounts. Importantly, Mezzi doesn’t move your money or execute trades, ensuring you retain full control.

Unlike traditional advisors who are limited to managing only the assets under their control, Mezzi’s comprehensive perspective allows it to identify tax-saving opportunities that might otherwise go unnoticed. Its AI continuously monitors for strategies such as tax-loss harvesting, keeping an eye on wash sale risks across accounts. It also provides guidance on advanced tactics like Roth conversions and mega backdoor 401(k) contributions. For example, if Mezzi detects a tax-loss harvesting opportunity valued at $150,000, it not only advises you on the steps to take but also notifies you when the 30-day wash sale window has passed, allowing you to repurchase the asset safely.

Mezzi also offers rebalancing recommendations and insights into optimizing account types, delivering a level of service comparable to a $10,000-per-year advisor but at a fraction of the cost. This approach not only supports tax planning but also provides considerable savings.

Mezzi vs. Traditional Advisors: Cost and Service Comparison

The financial difference between Mezzi and traditional advisors is striking. For instance, with a 1% assets under management (AUM) fee, a $5 million portfolio could cost $50,000 annually. Mezzi, on the other hand, offers a far more affordable pricing structure:

- Core: $299 per year

- Plus: $499 per year

- White Glove: $1,499 per year (includes AI coaching and unlimited support calls)

Even at its most comprehensive tier, Mezzi could save you approximately $48,000 annually compared to a 1% AUM fee on a $5 million portfolio.

| Feature | Mezzi Core ($299/year) | Mezzi Plus ($499/year) | Mezzi White Glove ($1,499/year) | Traditional 1% AUM Advisor |

|---|---|---|---|---|

| Annual Cost (on $5M portfolio) | $299 | $499 | $1,499 | $50,000 |

| Account Visibility | All connected accounts | All connected accounts | All connected accounts | Only managed assets |

| Tax-Loss Harvesting | AI recommendations | AI recommendations + alerts | AI recommendations + coaching | Manual, quarterly reviews |

| Execution Control | Full user control | Full user control | Full user control | Advisor executes trades |

| Wash Sale Tracking | Across all accounts | Across all accounts | Across all accounts | Limited to managed accounts |

| Support Access | AI chat 24/7 | AI chat + concierge (video, phone, email) | AI chat + unlimited coaching calls | Scheduled meetings only |

In addition to the cost advantage, Mezzi empowers you to act quickly on opportunities. For example, if Mezzi identifies $40,000 in unrealized losses across multiple accounts, you can immediately implement its recommendations through your brokerage platform - no need to wait for an advisor to take action.

Compliance Disclaimer: Mezzi is not a tax advisor. The information provided is for educational purposes only and should not be construed as tax advice. Consult a qualified tax professional regarding your specific situation.

Conclusion

High-income earners often face financial challenges that require more advanced and strategic approaches. The strategies outlined here - Modern Portfolio Theory diversification, tax-loss harvesting, backdoor Roth contributions, AI-powered rebalancing, direct indexing, and tax-loss harvesting across accounts, and alternative investments - are designed to help optimize returns while potentially reducing tax burdens.

Having a complete view of your finances is essential for identifying account overlaps or tax inefficiencies. Mezzi addresses this need by aggregating data across all your accounts, acting as an AI-powered financial assistant that uncovers opportunities you might otherwise overlook.

Building on these strategies, Mezzi’s real-time tools allow swift responses to changing market conditions. Its technology provides 24/7 monitoring and actionable insights, helping you manage overlaps, identify tax-loss harvesting opportunities, and maximize Roth contributions. By offering periodic rebalancing suggestions, Mezzi helps you maintain asset allocations that align with your long-term goals, even during market fluctuations.

For perspective, traditional advisory fees of 1% AUM on a $5 million portfolio amount to around $50,000 annually. Mezzi, however, provides in-depth analysis and tools for as little as $299 per year, giving you access to sophisticated financial insights without surrendering control of your assets or incurring excessive costs.

With Mezzi, self-managing your wealth becomes more efficient and informed. The platform offers fiduciary-level insights, empowering you to confidently implement complex strategies while maintaining full control. The result? A portfolio that’s more diversified, tax-efficient, and aligned with your financial goals. Mezzi serves as a reliable co-pilot, helping high-income earners execute these advanced strategies with precision.

Compliance Disclaimer: Mezzi is not a tax advisor. The information provided is for educational purposes only and should not be construed as tax advice. Consult a qualified tax professional regarding your specific situation.

FAQs

How do I know if my portfolio is too concentrated with RSUs and company stock?

If more than 20% of your wealth is tied to a single stock or company-related assets such as RSUs, your portfolio may be overly concentrated. This could leave you exposed to higher levels of risk. To help manage this, consider reviewing your portfolio regularly to assess its composition and aim for better diversification. This approach may reduce potential vulnerabilities and align your investments with your financial goals.

What’s the safest way to do a backdoor Roth IRA if I already have pre-tax IRA money?

To execute a backdoor Roth IRA strategy involving pre-tax IRA funds, it’s important to understand the pro-rata rule, which determines how conversions are taxed. To potentially reduce taxes, you might consider these steps:

- Make a non-deductible contribution to a traditional IRA.

- Convert the funds to a Roth IRA promptly to limit any taxable earnings.

- Transfer pre-tax IRA balances into an employer-sponsored plan, like a 401(k), to mitigate the impact of the pro-rata rule.

It’s always a good idea to consult a tax professional to ensure you’re following IRS requirements correctly.

When does direct indexing make sense versus sticking with ETFs in a taxable account?

Direct indexing may appeal to high-income investors with taxable accounts who prioritize tax management and personalized portfolios. Unlike ETFs, which provide simplicity and broad market exposure, direct indexing allows investors to own individual stocks directly. This approach creates opportunities for targeted tax-loss harvesting and more precise capital gains management. For those with larger portfolios, direct indexing can help systematically reduce taxes, potentially improving after-tax returns over time.

Disclosures:

- This content is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.

- Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.

- Mezzi is not a tax advisor. The information provided is for educational purposes only and should not be construed as tax advice. Consult a qualified tax professional regarding your specific situation.

- Registration does not imply a certain level of skill or that the SEC has approved the company or its services.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.