Managing wealth when you have over $1 million in liquid assets requires more than traditional investment methods. Here's a quick breakdown of what high-net-worth investors (HNWIs) need to know in 2025:

-

Who Are HNWIs?

- High-Net-Worth: $1M–$5M

- Very High-Net-Worth: $5M–$30M

- Ultra-High-Net-Worth: Over $30M

-

Why Standard Strategies Fail:

- Complex taxes and estate planning (estate tax exemption drops in 2026).

- Unique risk management needs.

- Access to exclusive investment opportunities.

-

Optimal Asset Mix in 2025:

- 47% Public Equities (optimized via tax-efficient asset allocation)

- 17% Real Estate

- 15% Private Companies

- 8% Alternatives

- 8% Cash/Bonds

- 5% Other Investments

-

Trends by Age and Wealth:

- Younger investors (30–39): Focus on crypto and private equity.

- Older investors (60+): Income-generating assets like real estate.

- Ultra-wealthy portfolios: 38% in private businesses.

-

Alternative Investments to Consider:

- Private equity: Higher returns but less liquidity.

- Real estate: Prices down 22%, creating opportunities.

- Other: Hedge funds, commodities, and art.

-

Tax and Wealth Protection:

- Use tax-advantaged accounts and strategies like trusts.

- Prepare for estate tax changes in 2026.

-

Digital Tools for Wealth Management:

- AI platforms like Mezzi for portfolio analysis, AI tax optimization, and fee reduction.

In 2025, managing wealth means balancing growth and risk while planning for tax changes. Tailored strategies and digital tools can help HNWIs protect and grow their assets.

Sophisticated Investing: Strategies for High-Net-Worth Portfolios

Beyond asset allocation, implementing specific wealth management tax strategies is essential for long-term capital preservation.

Building an Optimal Asset Mix

Combining public equities with alternatives like private companies and real estate can help boost returns while managing risk in 2025.

Mixing Standard and Alternative Assets

High-net-worth portfolios in 2025 often feature a well-rounded mix of asset classes. Here's an example of an average allocation:

| Asset Class | Allocation | Key Benefits |

|---|---|---|

| Public Equities | 47% | Growth potential, liquidity |

| Real Estate | 17% | Income generation, inflation protection |

| Private Companies | 15% | Higher returns, direct investment access |

| Alternatives | 8% | Diversification, unique opportunities |

| Cash and Bonds | 8% | Capital preservation, liquidity |

| Other Investments | 5% | Strategic opportunities |

Investors are moving away from traditional bonds, favoring private credit for better yields. Real estate remains essential, with 81% of investors owning a primary residence and 30% holding rental properties. These allocations shift with market trends, reflecting changing priorities.

Asset Allocation Changes in 2025

Shifts in market dynamics and investor demographics are shaping how portfolios are built this year.

Age-Based Trends:

- Investors aged 30–39 dedicate 9% to crypto and lead in private equity investments.

- Those aged 40–59 focus on balancing public and private markets while increasing real estate holdings.

- Investors over 60 lean toward income-generating assets and fixed-income investments.

Net Worth Impact:

- Portfolios exceeding $25 million allocate 38% to private business investments.

- Portfolios under $5 million invest 62% in public equities.

Alternative investments are gaining traction, with nearly 60% of financial professionals planning to allocate at least 10% to private market investments in 2025. High-net-worth investors are also actively adjusting portfolios in response to market conditions, interest rates, and sector opportunities. Notably, nearly 30% of these investors now save more than half of their post-tax income, highlighting their focus on both preserving and growing their wealth.

Alternative Investment Options

Expanding on the previously discussed asset mix, alternative investments offer distinct opportunities for returns and risk management compared to traditional assets.

Private Company Investments

Private equity has consistently outperformed public markets. Between 2007 and 2017, top-quartile private equity vintages delivered returns exceeding other asset classes by more than 7%. While private equity involves higher risk and less liquidity, it appeals to investors willing to commit for the long term. Typical investments require at least $250,000 and a holding period of 4 to 7 years.

"Private equity investments can be an attractive option for investors looking to diversify their portfolios and potentially earn higher returns."

– Granite Harbor Advisors

A 2015 study by Pantheon revealed that adding private equity to a public equity portfolio could boost annualized returns by approximately 3.16%. On the other hand, real estate offers a different set of opportunities and benefits.

Real Estate Investment Benefits

Real estate remains a strong choice for high-net-worth investors, especially as U.S. commercial property prices have dropped 22% from their peak. This market correction creates opportunities for well-timed investments. Additionally, the sector is embracing innovation, with tokenization - a market valued at $3.5 billion in 2024 - expected to grow to $19.4 billion by 2033.

"Both our quantitative research and our experience suggests that investors who take concentrated risk in a specific market, theme, or even invest too heavily during a particular period of time may not be maximizing their long-term risk-adjusted return potential."

– KKR

Other Investment Types

In addition to private equity and real estate, options like hedge funds, commodities, and art offer further ways to diversify portfolios. Here's a quick overview:

| Investment Type | Key Benefits | Risk Considerations |

|---|---|---|

| Hedge Funds | Broad investment strategies | Higher fees, inconsistent returns |

| Commodities | Protection against inflation | Price volatility |

| Art/Collectibles | Low correlation with markets | Limited liquidity |

"Alternative investments provide high-net-worth individuals with exclusive opportunities to enhance portfolio performance, hedge against inflation, and diversify risk."

– Arete Wealth

To succeed with alternatives, it's crucial to maintain a diversified approach that aligns with your overall strategy. Regularly reviewing and rebalancing your portfolio ensures these investments achieve their intended role.

Tax and Wealth Protection

Preserving wealth goes beyond building a strong portfolio. Minimizing tax liabilities and safeguarding against unexpected risks are just as essential.

Reducing Tax Impact

High-net-worth investors often face complex tax challenges, making strategic planning crucial. While accounts like 401(k)s and IRAs are common tools, many investors require more advanced strategies to manage tax exposure effectively.

One key approach is strategic asset location, which involves placing investments in accounts that maximize tax benefits. Here's a quick breakdown:

| Account Type | Best Investments | Tax Advantage |

|---|---|---|

| Tax-Advantaged Accounts | Income-generating assets | Delays taxes on ordinary income |

| Taxable Accounts | Long-term stock holdings | Benefits from lower capital gains rates |

| ETFs | Growth investments | Reduces capital gains distributions |

"Effective tax optimization requires a tailored approach based on your unique situation."

Additional strategies, like Qualified Opportunity Funds and Health Savings Accounts, can further reduce tax burdens.

Wealth Transfer Planning

With the federal estate tax exemption set at $13.99 million per individual (or $27.98 million for married couples) until the end of 2025, planning wealth transfers is more important than ever.

Here are two key tools for transferring wealth efficiently:

- Annual Gifting Strategy: In 2025, you can give up to $19,000 per recipient without triggering gift taxes.

- Trust Structures: Trusts are versatile tools for achieving specific goals. Popular options include:

- Intentionally Defective Grantor Trusts (IDGTs)

- Grantor Retained Annuity Trusts (GRATs)

- Irrevocable Life Insurance Trusts (ILITs)

"Due to the high estate tax exemption levels, the vast majority of families do not have taxable estates, but this isn't the case with many ultra high net worth families. If these families don't create a comprehensive estate plan, they could be exposed to estate taxes of up to 40% on the value of the estate that's above the exemption." - Elliott Stapleton, senior vice president and managing director of wealth strategy, Ascent Private Capital Management of U.S. Bank

Pairing these tools with insurance strategies ensures even greater protection.

Insurance Protection

For high-net-worth individuals, standard insurance policies often fall short of covering substantial assets or complex financial portfolios. Tailored coverage is essential to protect wealth effectively. Key types of coverage include:

- High-value home insurance

- Personal umbrella insurance

- Fine art and jewelry insurance

- Cybersecurity insurance

- Life insurance structured through ILITs

"Life insurance can be an important asset for covering expenses after death... Affluent individuals may leverage life insurance to help protect and potentially grow their wealth, minimize taxes, and create a lasting financial legacy." - Derek Gregoire

Regularly reviewing policies ensures they keep pace with changes in your financial situation. Specialized advisors can help identify gaps and suggest strategies like bundling policies or using self-insurance to optimize protection.

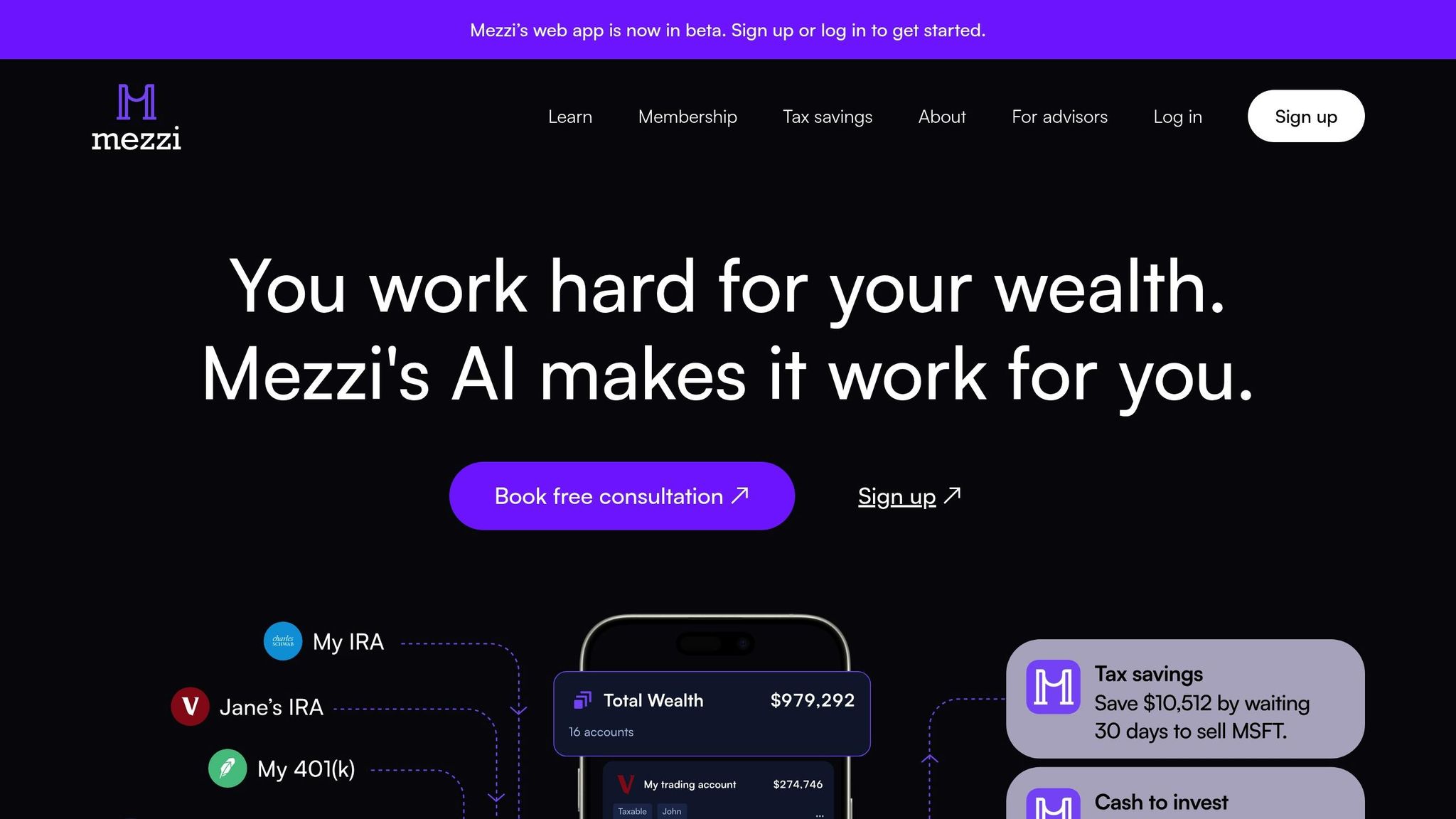

Digital Tools for Wealth Management

Today's digital tools give high-net-worth investors the ability to manage, analyze, and improve complex portfolios with ease. These technologies are designed to meet the sophisticated needs of modern investing.

Mezzi's AI Investment Analysis

AI technology now delivers deep insights into investment opportunities and portfolio management. Mezzi's platform uses AI to analyze financial data across accounts, offering personalized recommendations that can make a real difference in returns.

Here’s a breakdown of some key features:

| Feature | Impact |

|---|---|

| Real-time Portfolio Monitoring | Provides instant alerts on opportunities and risks |

| AI Tax-Loss Harvesting | Identifies ways to save on taxes across accounts |

| Fee Analysis | Highlights areas to reduce fees |

| Risk Assessment | Exposes hidden risks in your portfolio |

"Mezzi's X-Ray feature allowed me to uncover exposure to stocks I didn't realize I had." - Shuping, Founder of Summer AI

These AI-driven insights integrate seamlessly with tools for account management and tax strategies, creating a comprehensive approach to wealth management.

Account Management Systems

Digital dashboards bring all your accounts together in one place, making it easier to make informed financial decisions.

"I love the AI insights and the simplicity of UX. There is just enough info. Mezzi has helped me make changes to my portfolio. I haven't found another finance app that is doing what they are." - Tim, Former CMO of Fitbit

Security is a top priority when connecting financial accounts. Trusted providers like Plaid and Finicity offer secure, read-only account integration. This ensures that investors can view their entire financial picture without risking sensitive information.

Tax and Fee Reduction Tools

With strong account oversight in place, automated tax tools take portfolio efficiency to the next level. These systems identify ways to reduce fees and taxes, helping to grow long-term wealth.

For example:

- A 1% reduction in fund fees could add $186,877 to your retirement savings.

- Saving $10,221 in capital gains taxes and reinvesting it could grow to $76,123 over 30 years.

Mezzi’s AI continuously scans for tax-saving opportunities, avoiding wash sale issues and maximizing tax-loss harvesting. This automated process ensures no savings are overlooked.

Key Steps for Long-term Success

By 2025, high-net-worth portfolios often feature a mix of equities, private companies, real estate, alternatives, cash, and other financial products. This diversified approach balances growth potential with risk management, paving the way for strategies that consider tax implications.

Tax-Aware Investing

With tax changes expected in 2026, planning ahead is essential. Strategic wealth transfer methods can help reduce future tax burdens while ensuring assets are preserved for future generations.

| Feature | Impact on Long-term Success |

|---|---|

| Real-time Monitoring | Enables quick responses to market shifts |

| Tax Optimization | Automates AI-driven tax-loss harvesting |

| Risk Assessment | Provides timely alerts for adjustments |

| Performance Analysis | Supports data-driven decisions |

Age-Based Adjustments

Investment strategies should shift as investors age. For example, 52% of investors under 35 include crypto assets in their portfolios, with an average allocation of 9%. In contrast, older investors often focus on preserving wealth through real estate and fixed-income investments. Tailoring strategies to life stages helps align risk tolerance with individual circumstances.

Private Market Access

A significant 84% of ultra-high-net-worth investors turn to private market investments to enhance returns and reduce portfolio volatility.

Regular reviews ensure that strategies stay in sync with market trends and personal objectives. Using AI-powered tools - like those offered by Mezzi - can help maintain a disciplined focus on identifying opportunities for growth and safeguarding wealth. This includes leveraging automated tax-loss harvesting to minimize liabilities while maintaining full portfolio control.

FAQs

What should high-net-worth investors focus on when adjusting their asset allocation in 2025?

In 2025, high-net-worth investors should prioritize strategies that address changes in tax laws, economic conditions, and market trends. The reduction in the federal estate tax exemption may expose more estates to taxes, making it crucial to explore early wealth transfer options and trust structures.

Economic uncertainty, driven by inflation and global events, underscores the importance of maintaining a diversified portfolio. Consider balancing investments across public equities, private companies, real estate, alternative assets, and cash or bonds to manage risk and capitalize on growth opportunities.

On average, high-net-worth portfolios allocate approximately 47% to public equities, 15% to private companies, 17% to real estate, 8% to alternatives, 8% to cash and bonds, and 5% to other financial products. Adjusting your allocation to align with personal goals and risk tolerance is key to preserving and growing wealth.

What steps can high-net-worth individuals take to prepare for the changes in estate tax exemptions coming in 2026?

To prepare for the 2026 reduction in estate tax exemptions, high-net-worth individuals should consider taking proactive steps to maximize their wealth transfer opportunities while minimizing tax liabilities. Key strategies include:

- Making lifetime gifts now to take advantage of the current, higher exemptions before they are reduced.

- Establishing trusts, such as Spousal Lifetime Access Trusts (SLATs), Dynasty Trusts, or Irrevocable Life Insurance Trusts (ILITs), to protect and transfer wealth efficiently.

- Reviewing and updating your estate plan to ensure it aligns with the upcoming changes, including revisiting asset valuations, trust documents, and gifting strategies.

- Incorporating charitable giving tools, such as donor-advised funds (DAFs) or charitable remainder trusts (CRTs), to achieve both philanthropic and tax-saving goals.

Consulting with an experienced estate planning professional is crucial to tailoring these strategies to your unique financial goals and ensuring compliance with evolving tax laws.

How do digital tools and AI platforms enhance wealth management for high-net-worth individuals?

Digital tools and AI platforms play a significant role in transforming wealth management for high-net-worth individuals. By automating routine tasks and offering data-driven insights, they help streamline financial decision-making and improve precision.

AI can optimize investment strategies, deliver personalized financial recommendations, and enhance risk management by analyzing vast amounts of data quickly. These technologies enable affluent investors to make smarter, more informed decisions, ultimately preserving and growing their wealth efficiently.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.