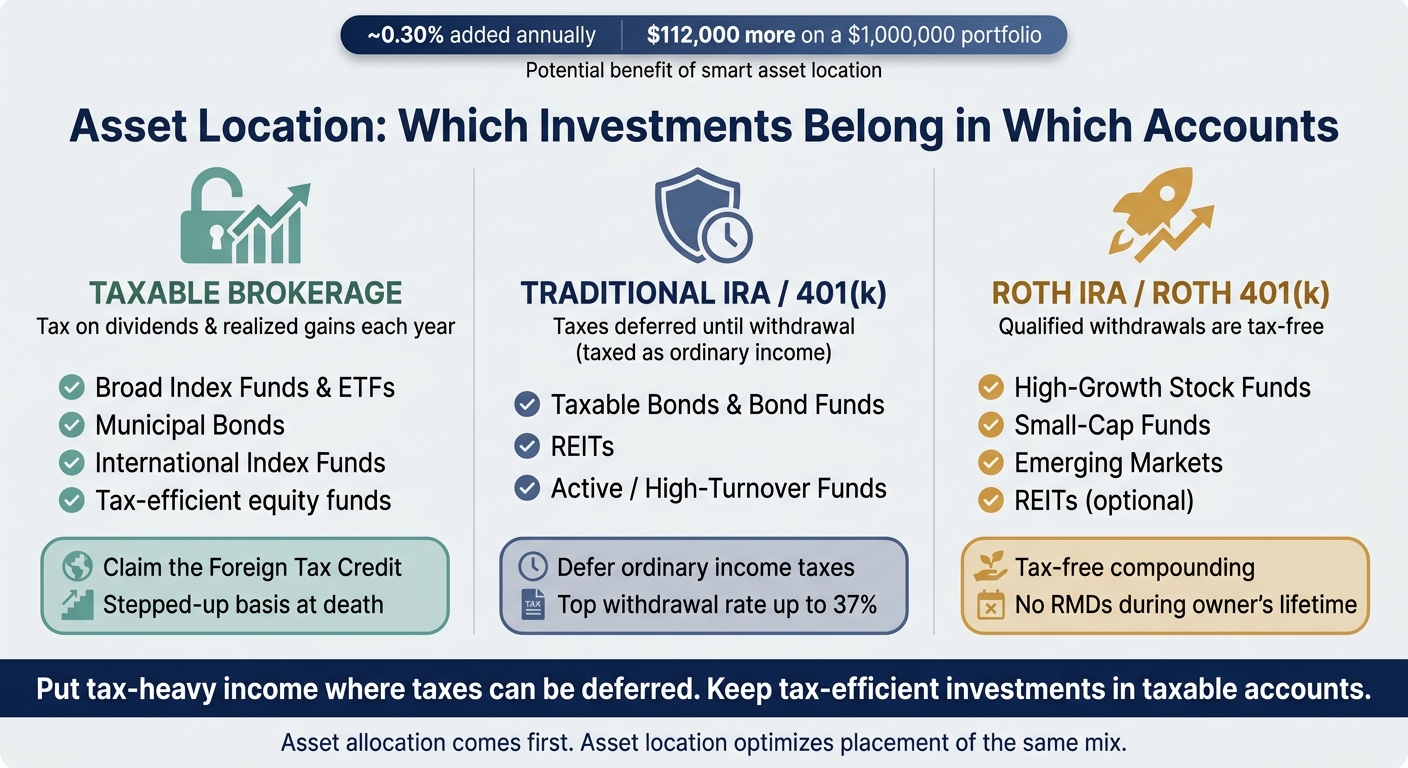

Where you hold an investment may matter almost as much as what you own. Some research suggests asset location may add about 0.30% a year and, in one example, may mean as much as $112,000 more on a $1,000,000 portfolio over time.

Here’s the short version:

- Taxable accounts may fit broad index funds, ETFs, international stock funds, and municipal bonds

- Pre-tax accounts like a 401(k) or IRA may fit taxable bonds, REITs, and high-turnover funds

- Roth accounts may fit higher-growth assets since future gains may come out tax-free if withdrawals are qualified

- Asset allocation comes first. Asset location is about placing the same mix in the right account types

- Moving too fast may trigger taxes, so some households shift with new contributions instead of selling right away

If I had to boil the whole topic down to one line, it would be this: put tax-heavy income where yearly taxes may be delayed, and leave more tax-friendly investments in taxable accounts.

Quick comparison

| Account type | Often used for | Main tax angle |

|---|---|---|

| Taxable brokerage | Index funds, ETFs, muni bonds, some international funds | Dividends and realized gains may be taxed each year or when sold |

| 401(k) / IRA | Bonds, REITs, active funds | Taxes may be delayed until withdrawal |

| Roth IRA / Roth 401(k) | Higher-growth stock funds | Qualified withdrawals may be tax-free |

This article breaks down that logic in plain English and shows how some investors may apply it across all household accounts.

Asset Location Guide: Which Investments Belong in Which Accounts

The Data Behind Asset Location (And Why It Matters) | Data Brief

How taxable, traditional, and Roth accounts are taxed in the U.S.

Before you place investments, it helps to map out how each account type may be taxed. A taxable brokerage account, a traditional IRA or 401(k), and a Roth IRA or 401(k) each treat income, gains, and withdrawals in different ways.

That difference is a big part of asset location. In plain English: the same investment may land very differently after taxes depending on where you hold it.

| Feature | Taxable Brokerage | Tax-Deferred (Traditional IRA/401(k)) | Tax-Free for Qualified Withdrawals (Roth IRA/401(k)) |

|---|---|---|---|

| Contribution tax treatment | After-tax dollars | Typically pre-tax (deductible) | After-tax dollars |

| Annual tax on income | Taxed annually (interest/dividends) | Deferred until withdrawal | None |

| Tax on gains | Taxed when realized (0%–20% long-term, or 23.8% including the 3.8% Medicare surtax) | Deferred; taxed as ordinary income at withdrawal | None |

| Withdrawal treatment | Principal tax-free; gains taxed at capital gains rates | Entire withdrawal taxed as ordinary income | Tax-free (qualified withdrawals) |

| Typical asset-location role | Tax-efficient equities, municipal bonds | Bonds, REITs, high-turnover funds | Highest-growth equities |

Taxable brokerage accounts: annual taxes and control over gains

Taxable accounts may give you more control over timing. You decide when to realize gains, which may affect when taxes come due. You may also harvest losses to offset gains, plus up to $3,000 of ordinary income per year.

There’s another piece people often pay attention to: appreciated assets may receive a stepped-up basis at death, which may wipe out embedded capital gains tax entirely.

Traditional IRA and 401(k): defer taxes now, pay ordinary income rates later

Traditional IRAs and 401(k)s usually take pre-tax dollars, then defer taxes on income and gains inside the account. Later, withdrawals may be taxed as ordinary income, with current top rates reaching 37%.

There’s also an RMD angle. Traditional accounts are subject to Required Minimum Distributions starting at age 73. That may push taxable income into your bracket whether or not you need the cash.

Roth IRA and Roth 401(k): pay taxes now, withdraw gains tax-free later

Roth accounts use after-tax contributions. If withdrawals are qualified, the money you take out in retirement - including growth - may be tax-free. Roth IRAs also have no RMDs during the original owner's lifetime.

Because of that setup, some investors use Roth space for assets with the highest expected growth. The idea is pretty simple: if more of the upside happens inside a Roth, those qualified withdrawals may come out tax-free.

Once you have that tax map, the next step gets a lot easier: place each investment in the account where its tax cost may be lower.

Which investments belong in which accounts

The basic idea is pretty simple: put tax-heavy income in accounts where taxes may be deferred, and put tax-efficient growth in places where it may compound with less tax drag. The account choices below follow from the tax treatment covered earlier. Think of this as a starting map for a household portfolio, then line it up with the accounts you actually have.

| Investment Type | Best in Taxable | Best in Tax-Deferred | Best in Roth | Why |

|---|---|---|---|---|

| Broad index funds / ETFs | ✓ | Low turnover; many dividends are qualified, and gains are usually taxed at lower long-term capital gains rates. | ||

| Municipal bonds | ✓ | Their interest is already federal tax-exempt, so tax-advantaged space may waste that benefit. | ||

| Taxable bonds / bond funds | ✓ | Interest is taxed as ordinary income, so deferral may reduce annual tax drag. | ||

| REITs | ✓ | ✓ | Payouts are generally taxed as ordinary income; Roth may be attractive if you want tax-free growth. | |

| Active / high-turnover funds | ✓ | Frequent capital gains distributions may create annual tax bills. | ||

| International index funds | ✓ | Taxable accounts may let you claim the foreign tax credit. | ||

| High-growth stocks / funds | ✓ | Tax-free withdrawals may matter most when the biggest gains compound inside the Roth. |

Tax-efficient equity funds: generally good fits for taxable accounts

Broad index funds and ETFs often fit well in taxable accounts because they tend to trade less and may produce fewer taxable surprises. Many also pay qualified dividends, and gains are often taxed at long-term capital gains rates if held long enough. That setup may make taxable accounts a decent home for plain-vanilla equity exposure.

International index funds often belong in taxable accounts for a more specific reason: the foreign tax credit. When you hold international stock funds in a taxable account, you can usually claim a credit for foreign taxes paid on your U.S. return. You usually lose the foreign tax credit in tax-advantaged accounts.

Bonds, REITs, and high-turnover funds: generally better in tax-deferred accounts

Assets that throw off ordinary income usually fit better where that income may be deferred. Bond interest is taxed as ordinary income, so bond funds often make more sense in tax-deferred accounts when that option is available.

REITs work in a similar way. Most REIT distributions do not qualify for the lower qualified dividend rate and are taxed as ordinary income. Active funds may create another issue: annual capital-gains distributions, even when you didn’t sell anything. For that reason, both often line up better with tax-deferred space.

Municipal bonds are the main exception. Their interest is already federal tax-exempt, so they generally fit better in taxable accounts.

High-growth assets: where Roth space tends to matter most

When the main tax cost comes later through appreciation, Roth space may become more useful. Roth space may matter most for assets with the highest expected growth, because future gains may compound tax-free. That’s why some investors give Roth space to small-cap funds, emerging markets, or other aggressive growth strategies.

Qualified-dividend funds may fit taxable accounts. Higher-yield or less tax-efficient dividend strategies may fit better in tax-advantaged accounts.

How to build an asset location plan across all your accounts

Start by mapping all accounts as one household portfolio

The first step is to treat all accounts as one household portfolio, not a stack of separate buckets.

List every account you and your spouse own:

- 401(k)s

- traditional IRAs

- Roth IRAs

- taxable brokerage accounts

Next to each account, write down each holding and its current balance. Then mark the holdings that may create more tax drag. That may include investments that throw off ordinary income or other less tax-friendly distributions.

This matters because asset location may work at the household level, not the individual account level. A bond fund in a taxable account may create the same drag whether the account belongs to you or your spouse.

Fill each account type in a practical order

Once you have the full map, a simple sequence may work for many households:

- Fill tax-deferred accounts first with your most tax-costly holdings.

- Reserve Roth space for your highest expected-growth assets.

- Use taxable accounts for broad index funds, ETFs, and municipal bonds for remaining fixed income needs.

A simple household example makes the rule easier to see:

| Account | Balance | What Goes Here |

|---|---|---|

| Traditional 401(k) / IRA | $600,000 | Entire bond allocation + REITs |

| Roth IRA / Roth 401(k) | $200,000 | Small-cap growth, emerging markets |

| Taxable brokerage | $400,000 | Total stock market index funds, municipal bonds |

That setup may shelter ordinary income, keep Roth space open for assets with more upside, and leave taxable accounts for holdings that may be more tax-efficient.

Improve asset location over time without triggering unnecessary taxes

Most households don’t start from scratch. You may already have a bond fund in a taxable account with years of embedded gains. Selling it just to move it may trigger a large capital gains bill, which may offset years of tax savings.

So instead of doing everything at once, some households phase in asset location over time. New contributions and reinvested dividends may be directed to the accounts that fit them best, rather than selling everything in one shot.

Here’s the basic idea:

- Redirect new contributions and reinvested dividends to the right accounts.

- If your taxable account may be overweight in bonds, stop adding bonds there.

- Direct new 401(k) contributions toward bonds.

- Direct new taxable contributions toward equity index funds until the mix moves back in line.

- Rebalance inside tax-advantaged accounts when possible to avoid realized gains.

Use these rules as the checklist for the summary below.

Conclusion: the key rules to remember, and how Mezzi helps

A short checklist of asset location rules to keep in mind

Asset location may not need constant attention, but a few core rules may be worth keeping in mind. Think of this as a last review of your household portfolio before adding new money or rebalancing.

- Allocation first. Start with your target mix of stocks, bonds, and other assets. Then think about where each holding may fit.

- Taxable accounts may work best for tax-aware holdings like broad index funds, ETFs, and municipal bonds.

- Traditional IRA and 401(k) accounts may be a better home for assets tied to ordinary income, such as taxable bonds, REITs, and high-turnover active funds.

- Roth accounts may be a place for higher-growth assets, like small-cap stocks and emerging markets.

- Move gradually if immediate changes may trigger a large tax bill. Some investors redirect new contributions first and rebalance inside tax-advantaged accounts when possible.

How Mezzi helps you spot asset location opportunities across all accounts

Once these rules are clear, the next step may be seeing every account together so you can apply them the same way across the household. That’s often the hard part. Mezzi brings those accounts into one view.

Mezzi connects your taxable, traditional, and Roth accounts with read-only access and shows them in one household view. From there, it surfaces asset location opportunities, wash sale risks, and portfolio overlap across your accounts.

As an SEC-registered fiduciary, Mezzi is legally obligated to act in your best interest. It surfaces opportunities; you stay in control of trades and rebalancing.

FAQs

How is asset location different from asset allocation?

Asset allocation is about what you own across your portfolio - like stocks, bonds, REITs, and cash - with the goal of balancing risk and return.

Asset location is about where you hold those investments, such as a taxable brokerage account, traditional IRA, or Roth IRA, with the goal of improving tax efficiency. Put simply: allocation is what you own; location is where you hold it.

Should I move holdings now or change future contributions first?

Generally, it may make sense to start with your current holdings. Adjusting asset location across the accounts you already have may improve tax efficiency right away, especially if you already hold a mix of investments.

After that, some people adjust future contributions so new money goes into the most tax-efficient accounts from the start. That step-by-step approach may improve after-tax growth while limiting extra tax costs.

What if I do not have enough Roth or pre-tax space for ideal placement?

Use your tax-advantaged account space as efficiently as you can. Some people start by maxing out Roth accounts or pre-tax accounts, then place more tax-efficient holdings, like index funds or ETFs, in taxable accounts. Less tax-efficient assets, like bonds or REITs, may fit better in tax-deferred accounts.

If that space still feels tight, many investors prioritize the holdings that may get the most from favorable tax treatment and accept that some assets may land in less-than-ideal accounts. The aim may be to make the best use of each account type, not to chase perfect placement.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.