When it comes to managing your investments, three platforms stand out: Wealthfront, Empower, and Mezzi. Each offers unique tools to help you track your finances, optimize taxes, and plan for the future. Here's a quick breakdown:

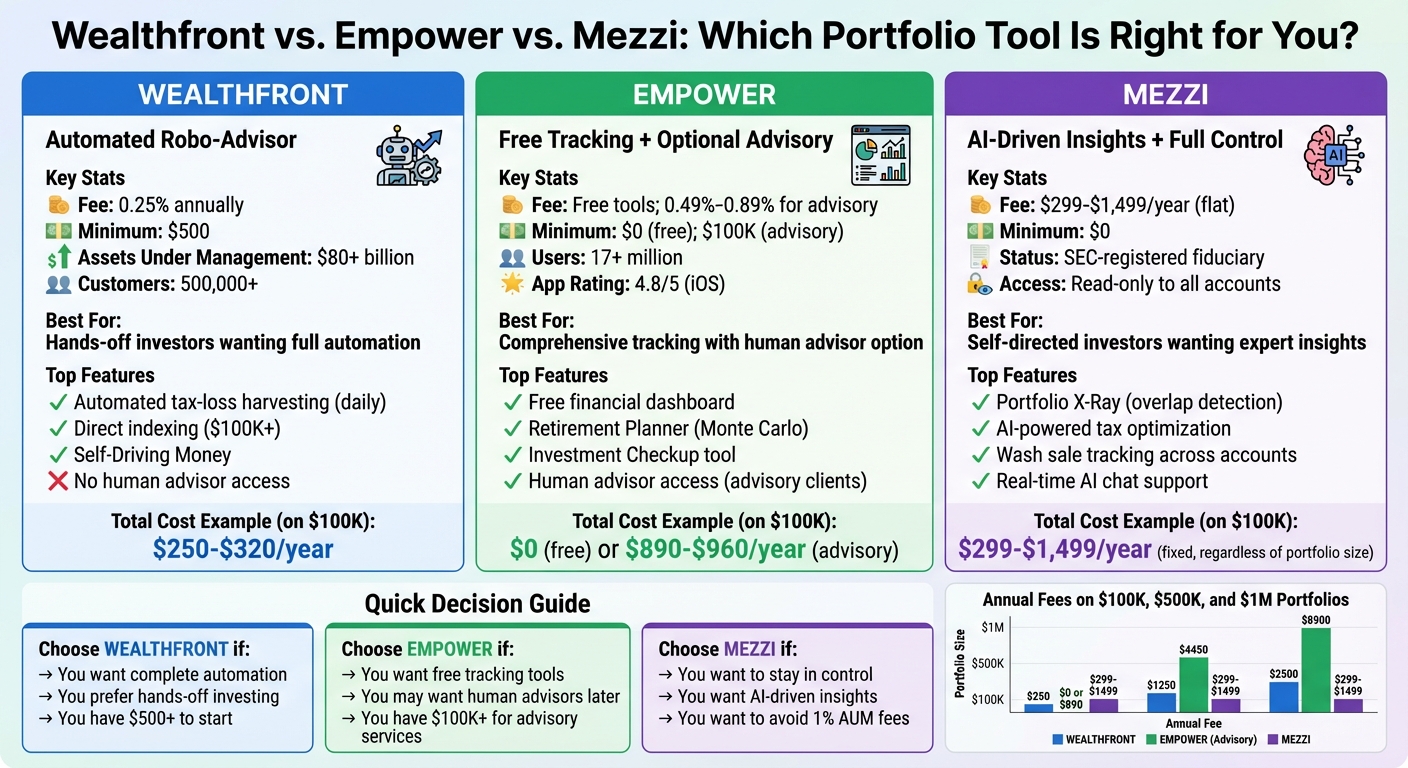

- Wealthfront: A fully automated robo-advisor with a 0.25% annual fee. It’s ideal for hands-off investors, offering tax-loss harvesting and financial planning tools.

- Empower: Known for its free financial dashboard, it aggregates all your accounts and provides tools like net worth tracking and retirement projections. Optional advisory services are available for portfolios over $100,000, with fees starting at 0.49%.

- Mezzi: An AI-driven platform offering personalized insights without managing your funds. It connects to all your accounts via read-only access and provides tools like tax optimization and portfolio overlap detection. Pricing starts at $299/year.

Quick Comparison

| Feature | Wealthfront | Empower | Mezzi |

|---|---|---|---|

| Fee Structure | 0.25% annually | Free tools; 0.49%-0.89% for advisory | $299–$1,499/year (flat fee) |

| Account Minimum | $500 | $100,000 for advisory | $0 |

| Tax Optimization | Automated tax-loss harvesting | Advisor-guided | AI-driven recommendations |

| Account Aggregation | Limited | Broad but with syncing issues | Extensive via Plaid/Finicity |

| Human Advisor Access | No | Yes (advisory clients) | White Glove plan only |

Key Takeaway

Choose Wealthfront if you want automation, Empower for free tracking with optional advisory (see our robo-advisor vs. human advisor cost comparison), or Mezzi for AI-powered insights while keeping full control of your accounts.

Wealthfront vs Empower vs Mezzi: Portfolio Tools Comparison Chart

Wealthfront Overview

Wealthfront is a fully automated robo-advisor that handles portfolio management using Modern Portfolio Theory. It charges a flat 0.25% annual fee on invested balances, with a $500 minimum investment requirement. Unlike hybrid platforms that provide access to human advisors, Wealthfront operates entirely through software, automating everything from portfolio creation to daily rebalancing. By 2026, the platform manages over $80 billion for more than 500,000 customers.

Wealthfront's approach focuses on diversification through low-cost ETFs and automatic rebalancing. This hands-off system provides professional-level management at a fraction of the cost of traditional advisors, who often charge fees exceeding 1%.

Here’s a closer look at some of Wealthfront’s standout features.

Key Features of Wealthfront

One of Wealthfront’s most notable tools is tax-loss harvesting, which automatically identifies and sells investments at a loss to offset capital gains or up to $3,000 of ordinary income annually. The platform replaces sold securities with similar alternatives to maintain the portfolio's balance while adhering to IRS wash-sale rules. In 2024 alone, this feature harvested over $145 million in losses for clients. Impressively, about 96% of users who used tax-loss harvesting for at least a year saw tax savings that outweighed the 0.25% advisory fee.

For accounts exceeding $100,000, Wealthfront offers Direct Indexing, a feature aimed at enhancing after-tax returns. This method, which goes beyond ETF-level harvesting, is estimated to generate an additional 1.50% in after-tax returns annually - about 2.7 times higher than standard ETF-level harvesting.

Wealthfront also provides tools for financial planning and cash management. The Path tool connects to external accounts to deliver real-time projections for major goals like retirement, home buying, or saving for college. It even allows users to simulate scenarios like taking a sabbatical or weathering a market downturn. Another useful feature, Self-Driving Money, monitors cash flow and shifts surplus funds from checking accounts into investments once a set threshold is reached. For instance, a software engineer earning $150,000 annually set a $5,000 buffer in their checking account, enabling the system to invest $42,000 over 12 months (roughly $3,500 per month), significantly improving their investment rate compared to their previous manual average of $2,000 per month.

Limitations of Wealthfront

While Wealthfront’s 0.25% annual fee is competitive, it’s important to factor in underlying ETF expense ratios, which range from 0.06% to 0.13%. This brings the total annual cost to about 0.31% to 0.38%.

One drawback is the lack of access to human financial advisors. While the platform is ideal for straightforward investment goals, it may fall short for individuals needing customized advice on complex topics like estate planning or advanced tax strategies. Additionally, Direct Indexing can create complications. Owning hundreds of individual stock positions can make transferring assets to another broker challenging and could lead to significant tax consequences. This "lock-in" effect makes Wealthfront better suited for investors who are comfortable with a fully automated experience.

"Wealthfront is a force among robo-advisors, offering a competitive 0.25% management fee and one of the strongest tax-optimization services available from an online advisor." – NerdWallet

Empower Overview

Empower, formerly known as Personal Capital, provides free financial tracking tools without requiring any minimum investment. With over 17 million users and partnerships with more than 69,000 organizations, it has become one of the most popular financial dashboards in the United States. Its standout feature? The ability to aggregate all your financial accounts into a single, real-time view - offered completely free of subscription fees.

Empower’s tools allow users to track changes in net worth, analyze investment portfolio allocations, and run retirement projections using Monte Carlo simulations. For those with $100,000 or more in investable assets, the platform offers optional wealth management services, charging annual fees between 0.49% and 0.89%, depending on account size. Despite these premium services, the free dashboard remains the primary attraction for most users.

As of March 2026, Empower boasts a 4.8/5 rating on the Apple App Store from 366,000 reviews. However, its Google Play rating is lower, sitting at 3.2/5 from 29,400 reviews. The platform has earned accolades such as NerdWallet’s "Best budget app for tracking wealth and spending" in January 2026 and Forbes Advisor’s "Best Budgeting App for Tracking Net Worth" in March 2025.

Let’s dive into how Empower simplifies financial tracking and planning.

Key Features of Empower

Empower consolidates data from a wide range of financial accounts, including checking, savings, retirement accounts (401(k)s, 403(b)s, IRAs, HSAs), credit cards, mortgages, personal loans, and CDs. It even tracks home values by pulling market estimates from Zillow. This unified view eliminates the need for manual spreadsheets, offering a real-time snapshot of your net worth.

The Investment Checkup tool takes a closer look at your portfolio across all linked accounts. It highlights potential issues, such as overexposure to certain sectors or high-fee funds, and compares your current asset allocation to a recommended target based on your risk profile. Meanwhile, the Retirement Fee Analyzer calculates your portfolio’s expense ratio, showing how fees can snowball over time, using a 0.50% benchmark for comparison.

One of Empower’s standout tools is the Retirement Planner, which uses Monte Carlo simulations to calculate a "Retirement Score" that estimates how sustainable your retirement plan might be. Users can tweak variables like retirement age, spending levels, and Social Security estimates to explore different scenarios. The web version even allows you to create and compare multiple "Alternative Plans" side by side. Empower suggests that a score above 90% means you’re in a solid position, with flexibility to increase spending either now or in the future.

"The best feature has been the Retirement Planner - where events, dates, and other data can be entered and combined to show where you are for retirement." – Steve G., User

Empower’s dashboards make complex financial data easy to understand. Interactive graphs let you examine daily changes or historical values, while a "Retirement Savings" meter tracks your progress toward your goal. Color-coded bar graphs break down 30-day cash flow into income and expenses by category. Additionally, a 90-day view of net worth and portfolio balance changes helps users quickly identify trends.

Limitations of Empower

While Empower offers strong tools, it does have its drawbacks. The free tools provide general insights rather than tailored recommendations. For example, the Investment Checkup might flag an imbalance in your portfolio but won’t suggest specific rebalancing actions or tax-efficient strategies. Users have reported syncing issues and occasional transaction delays, particularly on mobile apps. The desktop interface is better suited for detailed analysis, while the iOS and Android apps can feel less reliable for viewing transactions or generating comprehensive graphs.

Another common complaint involves Empower’s sales tactics. Users with linked assets exceeding $100,000 often report aggressive calls aimed at converting them into wealth management clients. This push can be frustrating for those who only want to use the free tracking tools. Additionally, free users don’t have access to human advisors, and tools like the Retirement Planner and Investment Checkup offer broad guidance rather than actionable steps.

"Empower isn't trying to be everything, and that's honestly what makes it good... Empower remains one of the best options available in 2026." – Nick Andr, Think Save Retire

Mezzi Overview

Mezzi isn’t your typical portfolio tracker. As an SEC-registered fiduciary, it’s legally obligated to act in your best interest - though it doesn’t manage funds or execute trades. Instead, Mezzi provides AI-driven financial advice, leaving you in full control of your accounts. Think of it as advisor-level insights without the hefty 1% annual fee, potentially saving you thousands each year.

The platform connects to all of your accounts - 401(k)s, IRAs, taxable brokerage accounts, and more - using read-only access through Plaid and Finicity (Mastercard). Your assets stay exactly where they are. Mezzi simply analyzes your entire financial picture and offers actionable suggestions, like identifying tax-loss harvesting opportunities or recommending portfolio rebalancing. If Mezzi spots a tax-saving move, it’s up to you to decide whether to act and execute the trade through your existing brokerage.

What sets Mezzi apart from traditional dashboards is its personalized, real-time guidance. You can ask complex, customized questions - like “Should I do a Roth conversion this year?” or “Am I on track to retire at 55?” - and get answers in minutes based on your actual portfolio data, not generic assumptions.

Mezzi offers three subscription plans: Core ($299/year), Plus ($499/year), and White Glove ($1,499/year). While there’s no free tier, Mezzi’s flat fees are far lower than the 1% annual fee many advisors charge. For example, someone with a $500,000 portfolio would pay $5,000 annually with a traditional advisor, compared to Mezzi’s fixed subscription cost.

Here’s a closer look at Mezzi’s standout features that provide AI-powered insights while keeping you in control of your accounts.

Key Features of Mezzi

Mezzi’s tools are designed to turn its AI-driven analysis into actionable insights that can improve your portfolio management.

- Portfolio X-Ray: This tool identifies hidden overlaps in your holdings. If you own multiple ETFs or mutual funds, you might unknowingly pay fees twice for exposure to the same stocks. By analyzing your positions, Mezzi highlights duplicate holdings, helping you reduce unnecessary costs and streamline your investments.

- Tax Optimization Tools: Mezzi works year-round to identify tax-saving opportunities. It flags positions trading below your cost basis for tax-loss harvesting and monitors wash sale risks across all your accounts. For instance, if you sell a stock at a loss in one account, Mezzi will alert you if buying or holding the same stock in another account could trigger a wash sale. Once the wash sale period ends, it lets you know when it’s safe to repurchase.

- Retirement Planning: Mezzi uses your connected account data to calculate retirement projections automatically. It factors in your portfolio value, contributions, withdrawals, fees, and asset allocation. You can model various scenarios - like retiring earlier or increasing contributions - and see how each decision impacts your timeline. Because it’s tied to real-time data, projections adjust as your account balances change.

- Rebalancing and Asset Location Guidance: Mezzi provides recommendations to maintain your target allocation efficiently. For example, it might suggest placing tax-inefficient investments like bonds in your Roth IRA while keeping stocks in taxable accounts. Its ability to view your entire financial picture gives it a unique edge compared to advisors who only see consolidated accounts.

These tools offer valuable insights, but they require you to take action to implement the recommendations.

Limitations of Mezzi

Mezzi’s advice-only model means you’ll need to handle all trades yourself. If it identifies a tax-loss harvesting opportunity, for example, you’ll need to log into your brokerage, place the sell order, and manage the replacement purchase. For those who prefer automation, this manual process might feel like extra work compared to robo-advisors that handle rebalancing for you.

Another drawback is the lack of a free tier. While the Core plan at $299/year is much cheaper than traditional advisor fees, platforms like Empower and Wealthfront offer basic tracking tools at no cost, which may appeal to users looking for free options.

Finally, human advisor access is only available with the White Glove plan ($1,499/year). While the AI addresses most questions, some users may prefer speaking with a person for complex decisions or reassurance during market downturns. The Core and Plus plans don’t include this feature, which could be a limitation for those who value direct human support.

Feature Comparison Table

The following table outlines the key features, fee structures, and account requirements for each platform:

| Feature | Wealthfront | Empower | Mezzi |

|---|---|---|---|

| Account Aggregation | Limited to specific account types (Taxable, IRA, 529) | Broad support but frequent connectivity issues reported | Connects with hundreds of U.S. brokerages, banks, and financial platforms |

| Tax-Loss Harvesting | Automated (Daily) | Manually monitored by advisors | AI-driven alerts (user executes) |

| Direct Indexing | Yes ($100,000+ minimum) | No | No |

| Wash Sale Protection | Automated | Manual/Advisor | AI-driven wash sale alerts (31-day tracking) |

| Portfolio Overlap Detection | No | No | Yes (X-Ray tool) |

| Retirement Planning | Basic projections | Advisor-guided | AI-powered with real account data |

| Advisory Fee | 0.25% annually | 0.89% annually (first $1M) | $299–$1,499/year (flat fee) |

| Account Minimum | $500 | $100,000 for advisory services | $0 |

| Human Advisor Access | No | Yes (included) | White Glove plan only ($1,499/year) |

This table highlights each platform's strengths, providing a foundation for comparing their approaches to tax efficiency, portfolio insights, and account integration.

Wealthfront excels in tax optimization with its automated daily tax-loss harvesting. The company claims, "Our Tax-Loss Harvesting strategy can typically cover our annual fee more than 6x over, for Automated Investing clients using the Classic portfolio". Meanwhile, Mezzi offers AI-driven tax-loss alerts, notifying users when the 30-day wash sale window ends, though users must execute trades themselves.

In terms of account aggregation, Mezzi stands out by connecting to hundreds of financial institutions through Plaid and Finicity. Unlike Wealthfront, which limits tracking to accounts within its own platform, Mezzi provides a comprehensive view of your financial landscape, including 401(k)s, IRAs, and taxable accounts. This broader integration enables features like tracking wash sale risks across multiple brokerages and its Portfolio X-Ray tool, which identifies duplicate holdings - capabilities not available with Wealthfront or Empower.

Tax Efficiency and Optimization

Tax efficiency plays a crucial role in managing investment portfolios effectively. Wealthfront, for instance, offers automated tax-loss harvesting to all its investors. This feature automatically identifies and harvests losses to offset gains and even up to $3,000 of ordinary income annually. However, this automation is exclusive to Wealthfront-managed accounts, where both rebalancing and loss harvesting occur without manual intervention.

Empower takes a different approach by combining advisor-led guidance with digital tools, rather than relying heavily on automation. Empower's advisors work closely with clients to craft personalized tax strategies tailored to individual circumstances. However, automated tax-loss harvesting isn’t a primary focus for this platform. These differing strategies provide a backdrop for Mezzi’s AI-driven tax optimization.

Mezzi stands out by using AI-powered insights to deliver tax optimization across all connected accounts. The platform identifies tax-loss harvesting opportunities, monitors wash sale risks, and offers advice on asset location - helping users strategically allocate investments between taxable and tax-advantaged accounts. When a tax optimization opportunity arises, Mezzi notifies users after the 30-day wash sale window has passed, ensuring they can safely repurchase securities. Unlike Wealthfront's fully automated execution, Mezzi provides guidance and alerts, leaving users to execute trades through their existing brokerages.

The platforms’ fee structures also highlight their distinct approaches to tax efficiency:

- Wealthfront: Charges a 0.25% annual fee plus ETF expenses ranging from 0.03%–0.07% (approximately $250–$320 annually for a $100,000 account).

- Empower: Applies a 0.89% fee on the first $1 million, alongside ETF fees of around 0.07% (totaling $890–$960 annually for a $100,000 account).

- Mezzi: Offers flat-rate fees between $299 and $1,499 annually, avoiding the percentage-based fees that can reduce returns over time.

Another key aspect of Mezzi’s service is asset location optimization - placing tax-inefficient investments in tax-advantaged accounts and tax-efficient investments in taxable ones. This strategy can significantly reduce lifetime tax liability. Mezzi’s AI aggregates data from all connected accounts to provide tailored asset location recommendations while also tracking wash sale risks. These insights not only help minimize long-term tax burdens but also enhance overall portfolio stability.

Portfolio Management and Insights

Wealthfront takes a hands-off approach to investing by using Modern Portfolio Theory to manage a curated selection of low-cost ETFs. These ETFs span six asset classes: U.S. stocks, foreign stocks, emerging markets, real estate, natural resources, and bonds. The platform handles rebalancing automatically, making it a simple option for those who prefer minimal involvement. However, its focus is limited to assets held within Wealthfront's ecosystem.

Empower, on the other hand, offers a more comprehensive financial overview. It consolidates external accounts like 401(k)s, IRAs, and taxable brokerage accounts into a unified dashboard, allowing for easier tracking. The Investment Checkup tool evaluates your overall risk and target allocation across all connected accounts. For clients with at least $100,000 who choose managed services, Empower provides access to human advisors who create custom portfolios through direct consultation. One drawback, however, is that some users experience delays in transaction updates, which can hinder real-time decision-making.

Mezzi takes a different approach by focusing on delivering real-time AI-driven insights rather than automating execution. It monitors all connected accounts and sends alerts when it identifies opportunities or risks. One standout feature is its overlap analysis, also known as Portfolio X-Ray, which highlights when the same stocks are held across multiple ETFs or mutual funds. Mezzi also provides actionable recommendations, such as identifying lower-cost funds with similar exposure to help reduce investment fees without altering your investment strategy. While Mezzi doesn’t execute trades for you, it empowers you to act on its insights through your existing brokerages, maintaining full control over your assets.

The key difference between these platforms comes down to control and scope. Empower offers a broad financial view with personalized guidance for high-balance clients. Mezzi, on the other hand, provides detailed, fiduciary-level insights across all accounts while leaving execution decisions in your hands. This makes Mezzi particularly appealing to investors who want professional-grade advice without giving up control of their portfolios.

Usability and Account Integration

Getting the most out of your portfolio often hinges on how well your accounts are integrated. Wealthfront takes a straightforward approach by focusing solely on accounts opened directly with them. To get started, you'll need at least $500. From there, the platform walks you through a simple goal-setting process based on your risk tolerance. Once funded, Wealthfront automates the entire process, leaving you to manage only the accounts held within its system.

On the other hand, Empower emphasizes account aggregation, allowing you to consolidate multiple external accounts into one unified view. Kevin Mercadante describes this as offering "the broadest possible view of your overall portfolio". Empower’s free tools, like the net worth tracker and fee analyzer, which functions similarly to an investment fee analyzer, are available to everyone, even if you don't meet the minimum requirements for their managed services. This approach pairs well with their detailed portfolio insights across various platforms.

Taking integration a step further, Mezzi combines advanced connectivity with real-time AI support. It offers read-only access to hundreds of U.S. brokerages and bank accounts via partners like Plaid and Finicity, so you don’t have to move your assets. You can also manually add illiquid assets, providing a complete financial overview. What sets Mezzi apart is its AI-powered chat interface, which replaces static dashboards. With Mezzi, you can "talk to your portfolio" and receive immediate, personalized answers to your financial questions - no need to wait days for an advisor’s response.

The distinction between these platforms comes down to control versus consolidation. Wealthfront limits its management to accounts within its ecosystem. Empower brings external accounts together for a comprehensive view. Mezzi, however, offers full visibility across all accounts while providing fiduciary-level insights, without actually managing or trading your assets.

Pricing and Free Features Breakdown

For investors who want AI-driven insights without giving up control, understanding fees and free features is key. Here's how the options stack up:

Wealthfront manages the first $5,000 in your account at no charge. After that, a 0.25% annual advisory fee kicks in - equal to about $250 per year on a $100,000 portfolio. Wealthfront also provides free planning tools, but its core investment service requires a $500 minimum deposit. Additionally, there may be an extra 0.03% fee.

Empower offers a free dashboard with tools like a net worth tracker, budgeting features, and an investment fee analyzer. If you opt for its advisory services, the fee starts at 0.89%.

Mezzi, on the other hand, uses a straightforward flat-fee subscription model, regardless of portfolio size. The Core plan costs $299 per year and includes features like unlimited AI chat, 24/7 monitoring, proactive insights, the X-Ray tool for spotting overlapping holdings, tax optimization guidance, and return analysis across all accounts. At $499 per year, the Plus plan adds advanced research tools, early access to new features, deep-thinking AI, and concierge support via video, phone, and email. For those wanting maximum personalization, the White Glove plan costs $1,499 annually and offers unlimited support calls and AI coaching via video.

With Wealthfront and Empower, fees increase as your portfolio grows. For instance, managing a $1 million portfolio would cost about $2,500 per year with Wealthfront and $8,900 with Empower. Mezzi’s flat fees, however, remain the same, making it a more cost-efficient option as assets grow. This pricing model highlights Mezzi’s ability to keep costs predictable while giving you full control over your portfolio.

The decision ultimately comes down to how much control you want. Wealthfront and Empower handle trades and portfolio management for you, while Mezzi provides fiduciary-level advice and actionable insights, leaving you in charge of implementing changes.

Limitations and Risks

Every portfolio tool has its trade-offs. Wealthfront, for instance, is a fully automated robo-advisor with no access to human financial advisors. Its automation restricts flexibility, locking users into an ETF-only portfolio. If you're looking for personalized help with complex financial matters like estate planning or advanced tax strategies, you'll need to look elsewhere. On the upside, accounts do come with standard SIPC protection.

Empower, on the other hand, balances personalized service with higher costs. It requires a US$100,000 minimum investment and charges an annual fee of 0.89%. For a portfolio of US$1 million, that’s about US$8,900 per year. While this fee grants access to human advisors, the platform lacks advanced AI-driven tools that can provide real-time tax optimization insights across all your accounts.

Mezzi takes a different approach, focusing on guidance while leaving trade execution up to you. Mezzi provides fiduciary-level advice and actionable insights, but it doesn’t handle money transfers or automatically rebalance portfolios. Instead, it tells you what steps to take, and you decide whether to follow through. This hands-on model appeals to investors who want more control. Mezzi also prioritizes security, using bank-grade encryption through Plaid and Finicity for secure, read-only account access. As an SEC-registered fiduciary, Mezzi is legally required to act in your best interest.

Who Should Choose Each Platform

Based on the comparisons above, here’s a breakdown of which platform fits different investment preferences and needs:

Wealthfront is a great match for those who want a completely hands-off approach to investing. It automatically allocates assets using Modern Portfolio Theory, making it ideal for beginners or smaller-scale investors who want professional portfolio management without active involvement. However, if you’re looking for a tool that offers a broader financial overview, you might need to explore other options.

Empower caters to investors with liquid assets between $25,000 and $2 million, offering a comprehensive way to track their financial health. Its free dashboard integrates external accounts, like 401(k)s and retirement plans, to provide a clear picture of your net worth. For those with $100,000 or more who prefer human advisors, Empower also provides personalized guidance. On the other hand, if you prioritize control over your investments without paying traditional management fees, another platform might be a better fit.

Mezzi is tailored for self-directed investors who want expert-level insights without giving up control or paying the typical 1% AUM fees. Mezzi stands out by offering real-time, AI-driven insights and consolidating all your financial accounts with read-only access. At $299 per year for the Core plan, it’s perfect for those who see unstructured investing as too risky but still want to make their own decisions. Whether you’re timing Roth conversions or fine-tuning your asset allocation, Mezzi provides on-demand, fiduciary-level guidance while letting you stay in charge.

Conclusion

When it comes to choosing a portfolio tool, the decision largely hinges on how much control and guidance you prefer. Wealthfront caters to those who prefer a more hands-off approach, while Empower appeals to individuals seeking detailed tracking paired with human advisory support.

Then there’s Mezzi, which takes a different route. Mezzi is designed for investors who want to stay in control but still benefit from expert insights - without paying the typical 1% asset management fee. Priced at $299 per year for the Core plan, Mezzi connects to all your existing accounts with read-only access. Its AI-driven recommendations cover areas like tax optimization, rebalancing, and asset allocation, offering you expert-level advice on demand.

What sets Mezzi apart is its ability to see your entire financial picture across all brokerages and account types. This allows it to spot opportunities that traditional advisors might miss - like identifying wash sale risks across accounts or overlapping ETF holdings. Importantly, Mezzi doesn’t execute trades for you. Instead, it provides actionable advice, leaving you in full control of your investments. For self-directed investors who want guidance without giving up control or incurring high fees, Mezzi offers a compelling solution.

FAQs

Is Mezzi safe to link to my accounts?

Mezzi takes your security seriously, making it safe to link your accounts. It employs strong security measures like account aggregation, AI-powered insights, and advanced tools for tax and portfolio analysis. These features work together to protect your data while helping you streamline your financial management.

Will Mezzi place trades for me?

Mezzi doesn't place trades for you. Instead, it leverages AI to sift through market data and deliver real-time insights, guiding you toward the best moments to act. This way, you stay in charge of your portfolio while making more informed investment decisions.

When is Mezzi cheaper than an AUM fee?

Mezzi offers a flat annual fee ranging from $199 to $499, which often proves to be more cost-effective compared to the typical 0.5% to 1.5% AUM fee charged by many advisors. This pricing structure is especially advantageous for portfolios under $1 million. One of the key benefits of flat fees is their predictability - your costs remain consistent, unlike percentage-based fees that grow alongside your portfolio's value.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.