Private equity funds don’t ask for your full investment upfront. Instead, they use a system called capital calls, where fund managers request portions of your committed capital as needed. This staggered approach allows investors to keep uncalled funds in other investments until required.

Here’s how it works:

- Capital Calls: Fund managers request a portion of your pledged amount when they identify investments or need to cover expenses. You typically have 10–14 days to fulfill these requests.

- Capital Call Lines: Funds may use short-term credit facilities to bridge gaps before receiving investor contributions, improving cash flow and operational flexibility.

- Key Uses of Capital: Funds are primarily used for new investments (80%+), management fees, and operating expenses.

Why it matters: These mechanisms help minimize idle cash, optimize fund performance metrics, and give investors more control over uncalled capital. However, failing to meet a capital call can lead to penalties, including interest charges or loss of fund interest.

For investors, understanding the terms in the Limited Partnership Agreement (LPA) - like notice periods, payment deadlines, and default consequences - is crucial. Reviewing how funds use subscription lines and their impact on returns can also help you make informed investment decisions.

Private Equity Capital Calls Explained | Commitments, Drawdowns & Fund Flow | Module 6

How Capital Calls Work

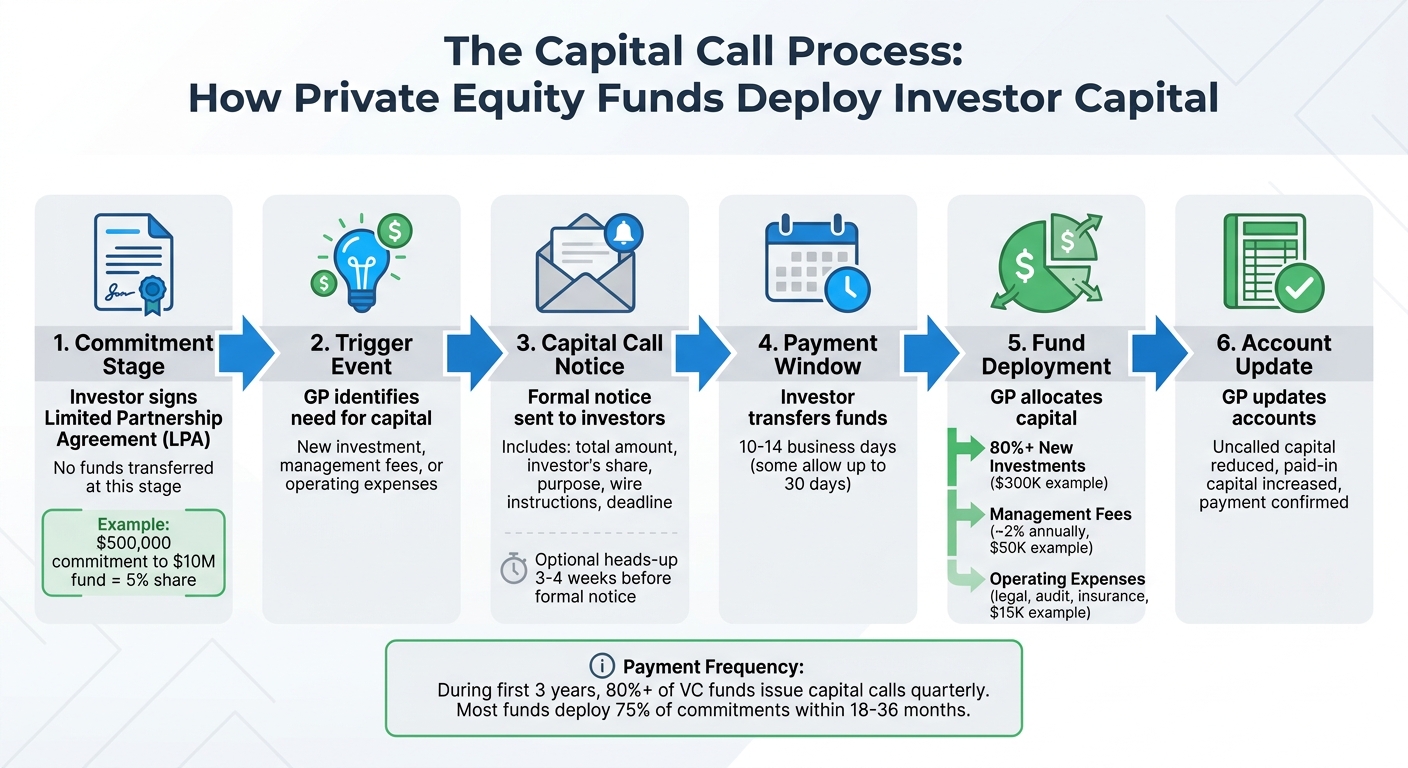

Capital Call Process: From Commitment to Fund Deployment in Private Equity

The Capital Call Process

When you sign the Limited Partnership Agreement (LPA), you agree to contribute a specific amount to the fund. However, no funds are transferred upfront at this stage.

Capital calls are triggered when the General Partner (GP) determines the need for funds. These needs could include financing a new investment, covering management fees, or handling operating expenses. The GP or fund administrator calculates each investor's share based on their commitment percentage. For example, if you’ve committed $500,000 to a $10 million fund, your share would be 5% of every capital call.

Once a capital call is initiated, you’ll receive a formal notice. This document typically includes details like the total amount being called, your specific share, the purpose of the funds, wire transfer instructions, and the payment deadline. Payment windows usually range from 10 to 14 business days, though some agreements may allow up to 30 days.

After the funds are collected, the GP updates the accounts, reducing uncalled capital and increasing paid-in capital. They also confirm your payment. The money is then allocated toward portfolio investments or used to cover fees and operating expenses.

To help investors prepare, many GPs send a heads-up email about 3–4 weeks before issuing the formal notice. As Archstone advises:

Your LPs are not ATMs. Give them time to plan, and they'll fund every call without complaint.

With this process in place, the next step is understanding how the collected funds are used.

What Capital Calls Pay For

Once the funds are collected, they are primarily used for three purposes:

- New Investments: The majority of the funds - often over 80% - are allocated to investments in portfolio companies.

- Management Fees: These fees, typically around 2% of total commitments annually, are called quarterly or semi-annually to compensate the GP.

- Fund Operating Expenses: This includes costs like legal fees, audits, insurance, and administration, which generally make up the smallest portion of any capital call.

Here’s an example of how a $365,000 capital call might be distributed:

| Use Case | Description | Example Amount |

|---|---|---|

| New Investment | Acquiring equity in a portfolio company | $300,000 |

| Management Fees | Periodic fees for fund operations | $50,000 |

| Fund Expenses | Legal, audit, insurance, and administrative costs | $15,000 |

During the first three years of a fund's lifecycle, over 80% of venture capital funds issue capital calls in any given quarter. The pace of calls generally slows once about 75% of the commitments have been deployed. Most funds complete the majority of their capital deployment within 18 to 36 months, even though the official investment period might extend to five years.

Capital Call Lines Explained

What Is a Capital Call Line?

Capital call lines, often referred to as subscription credit facilities or "sub-lines", are revolving credit arrangements that give fund managers quick access to cash. These lines are backed by the uncalled commitments of Limited Partners (LPs), allowing managers to borrow against these commitments without delay.

Essentially, these facilities serve as a type of bridge financing. A fund might use the borrowed money to close a deal or cover expenses, repaying the loan within 30 to 90 days after formally calling capital from investors. The creditworthiness of the LPs, rather than the performance of the fund's investments, is a key factor for lenders when evaluating these facilities.

The size of these credit lines typically ranges from 10% to 30% of the total fund commitments, though many funds impose a cap of 15% of the fund's size. By 2024, established fund sponsors were securing these lines at rates of roughly 200 to 325 basis points over SOFR, with undrawn commitment fees between 30 and 60 basis points and upfront fees ranging from 25 to 100 basis points.

How Capital Call Lines Operate

The security for these credit facilities includes several critical elements: the right to call capital from investors, the right to receive those contributions, control over designated bank accounts where funds are deposited, and power of attorney to enforce payments from investors if necessary.

In the U.S., the right to call capital is categorized as a "general intangible" under the Uniform Commercial Code (UCC). To secure their interest, lenders file a UCC-1 financing statement in the jurisdiction where the fund is formed.

Lenders use a borrowing base model to determine the credit available. Advance rates are applied to eligible investors, with institutional investors like pension funds typically receiving higher rates compared to high-net-worth individuals or family offices. Fund managers must maintain an updated borrowing base file, which tracks factors such as LP credit downgrades, side letter restrictions, and concentration limits, to prevent unexpected borrowing issues.

The Limited Partnership Agreement (LPA) must specifically authorize the use of credit facilities and assign the capital call rights to the lender. It should also permit capital calls to repay loan principal and interest, even after the fund’s active investment period concludes. With the proper structures in place, these facilities offer distinct advantages and potential drawbacks for both fund managers and investors.

Benefits and Risks for Investors and Fund Managers

Capital call lines influence cash flow timing and overall fund performance for both fund managers and investors. For managers, these facilities allow them to close deals quickly without waiting for capital call settlements. They also streamline operations by consolidating multiple small investments into a single capital call, reducing administrative effort. Additionally, they can improve the fund's Internal Rate of Return (IRR) by delaying the "investment clock", effectively shortening the J-curve.

The Institutional Limited Partners Association highlights the following:

The ability to delay calling capital enhances the manager's flexibility to execute deals and shortens the J-curve, enhancing the fund's IRR, particularly early in a fund's life, and therefore its competitiveness on a quartile basis.

For investors, capital call lines smooth cash flow by reducing the frequency of funding requests. This can make the process less burdensome and allow LPs to keep their committed capital invested elsewhere until it's needed.

However, these facilities also come with risks. Fund-level leverage introduces exposure to potential losses if the fund's assets underperform. Interest expenses and fees can reduce returns if the credit line isn't used efficiently. For LPs, borrowing may trigger Unrelated Business Taxable Income (UBTI) for tax-exempt entities or create other tax challenges depending on the jurisdiction. If a fund defaults on the line, lenders may even have the right to issue capital calls directly to LPs.

| Feature | Benefit for Fund Managers (GPs) | Benefit for Investors (LPs) |

|---|---|---|

| Speed of Execution | Enables quick deal closures | Reduces the frequency of small capital calls |

| IRR Optimization | Delays the investment clock, shortening the J-curve | Keeps capital invested elsewhere longer, improving IRR |

| Cash Management | Covers funding gaps efficiently | Provides smoother and more predictable cash flows |

| Risk Exposure | Involves fund-level leverage and costs | Potential overcall risk if other LPs default |

Limited Partnership Agreement Terms

The Limited Partnership Agreement (LPA) establishes the legal framework for managing capital calls and credit facilities. It outlines the timelines investors must follow and the penalties for failing to comply.

Notice Requirements and Payment Deadlines

Fund managers typically provide advance notice of 7 to 20 days before a capital call payment is due. Investors are usually given 10–15 business days to transfer funds, allowing time to liquidate assets if necessary. This system demonstrates the importance of capital call lines in addressing short-term funding needs.

In some cases, fund managers offer an informal 30-day notice of intent to help investors with liquidity planning. This additional heads-up can make it easier for investors to manage their resources and reduce the likelihood of late payments.

These structured notice and payment timelines help clarify how LPAs regulate capital deployment and address potential defaults.

Usage Limits and Default Consequences

Beyond timing, LPAs also regulate how capital can be used. During the agreed investment period, typically the first 5–7 years, fund managers may call capital for new investments. After that, capital calls are generally restricted to follow-on investments, management fees, and operational costs. Many LPAs also include concentration limits, which restrict the amount of capital that can be allocated to a single deal based on factors like industry, geography, or fund size.

Investors who fail to meet capital calls face strict penalties outlined in the LPA. As Kiel A. Bowen, Partner at Mayer Brown, explains:

The default remedies in a fund's limited partnership agreement ('LPA') significantly impact the health and stability of the subscription credit facility because they incentivize investors to fund their capital contributions and help to provide adequate security for the facility.

Penalties for defaulting investors may include 5–10% penalty interest, withheld distributions, forced sale of interests, dilution through "cram-downs", and loss of voting rights. In extreme cases, investors could forfeit 25% to 50% of their existing fund interest. To address shortfalls caused by defaults, funds may issue an "overcall", requiring non-defaulting investors to contribute additional capital.

The 2022 Ashkenazy v Gindi case in Manhattan's Commercial Division highlights how LPA terms can influence enforcement. In one Delaware LLC venture reviewed by the court, the LPA specified that the "exclusive remedy" for a failed capital call was for the contributing member to provide a loan. If unpaid after 180 days, that loan would convert into additional equity, diluting the defaulting member's stake.

Conclusion

Capital calls are binding agreements that allow private equity fund managers to request portions of the committed capital as investment opportunities arise. This drawdown structure helps reduce cash drag, letting investors keep their capital deployed elsewhere until the fund specifically needs it. The usual 10- to 20-day notice period provides investors with time to arrange liquidity, emphasizing the importance of maintaining sufficient liquidity to avoid default penalties.

Capital call lines are commonly used by funds managing over $20 million in assets. These facilities provide immediate funding for deals, allowing fund managers to consolidate investor calls on a quarterly basis. While capital call lines can enhance operational efficiency and may improve IRR by reducing the length of the capital holding period, they come with added interest costs. Gonzalo Fernández-Turégano, Global Sector Head of Financial Sponsors at BBVA CIB, explains:

"The flexibility provided by capital calls allows for more dynamic fund management and greater agility in executing investments."

These points highlight the critical factors investors should evaluate before committing to a fund.

What Investors Should Know

Before committing capital, carefully review the Limited Partnership Agreement (LPA) for details about notice periods, limits on call frequency, and default penalties. Check whether the General Partner (GP) retains the ability to call capital for expenses or follow-on investments after the formal investment period ends, as this can affect your long-term liquidity strategy.

As noted earlier, the timing of capital calls and the use of subscription lines are key elements of fund management. To fully understand how these impact returns, consider requesting dual IRR reporting - one with and one without the effects of credit facilities. This approach can help you distinguish between returns driven by investment performance and those influenced by leverage timing. Additionally, review the LPA for any restrictions on borrowing against uncalled capital to assess your exposure to fund-level leverage.

It's crucial to maintain enough liquidity to meet the standard 10-day call window. Missing a capital call can lead to escalating penalties, such as late interest charges (often as high as 18% annually) or even the forfeiture of your investment. Keep in mind that your creditworthiness also plays a role in the fund's borrowing capacity, so understanding how your financial profile contributes to the fund's credit base is essential.

Grasping the mechanics of capital calls is an important step toward making informed and strategic investment decisions.

FAQs

How can I plan liquidity so I’m never late on a capital call?

To prevent delays with capital calls, it's important to approach liquidity planning with care and foresight:

- Clear communication: Notify investors well in advance, typically 30–90 days, to ensure they’re prepared for the capital call.

- Liquidity buffer: Maintain accessible liquid assets or credit lines to manage unforeseen shortfalls or timing mismatches.

- Capital call lines: These financing tools can help bridge timing gaps, ensuring commitments are met without delay.

- Automated tracking: Leverage technology to track commitments, notices, and payments, making it easier to follow up promptly and avoid missed deadlines.

Planning ahead and using these strategies may help ensure smoother capital call processes.

Do capital call lines inflate a fund’s IRR compared to true performance?

Capital call lines are not designed to artificially increase a fund’s internal rate of return (IRR); instead, they help manage liquidity and influence the timing of returns. When used at the beginning of a fund’s lifecycle, they may temporarily enhance IRR by speeding up the process of making investments and realizing exits. However, this effect is short-lived and does not represent the fund’s long-term performance. While these lines can shift the timing of cash flows and impact how IRR is calculated, they do not change the actual returns generated by the fund’s underlying investments.

What happens to me if other investors default and the fund makes an overcall?

If other investors default and the fund issues an overcall, your responsibilities will depend on the terms outlined in the limited partnership agreement (LPA). Failing to comply with an overcall could lead to consequences such as penalties, dilution of ownership, or even a loss of certain investor rights.

Defaults can also have broader implications for the fund, potentially impacting its liquidity and key performance metrics like internal rate of return (IRR). To address these risks, fund managers may include specific provisions in the LPA or turn to alternative financing options, such as capital call lines, to cover any shortfalls caused by defaults.

Disclosures:

- This content is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.

- Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.

- Savings and performance examples are hypothetical and for illustrative purposes only. Actual results will vary based on individual circumstances, portfolio composition, market conditions, and fees.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.