Want to minimize taxes on your investment gains? When you sell investments like stocks or real estate for a profit, you'll owe capital gains taxes. These taxes can significantly impact your returns, but careful planning may help reduce your tax liability. Here's what you need to know:

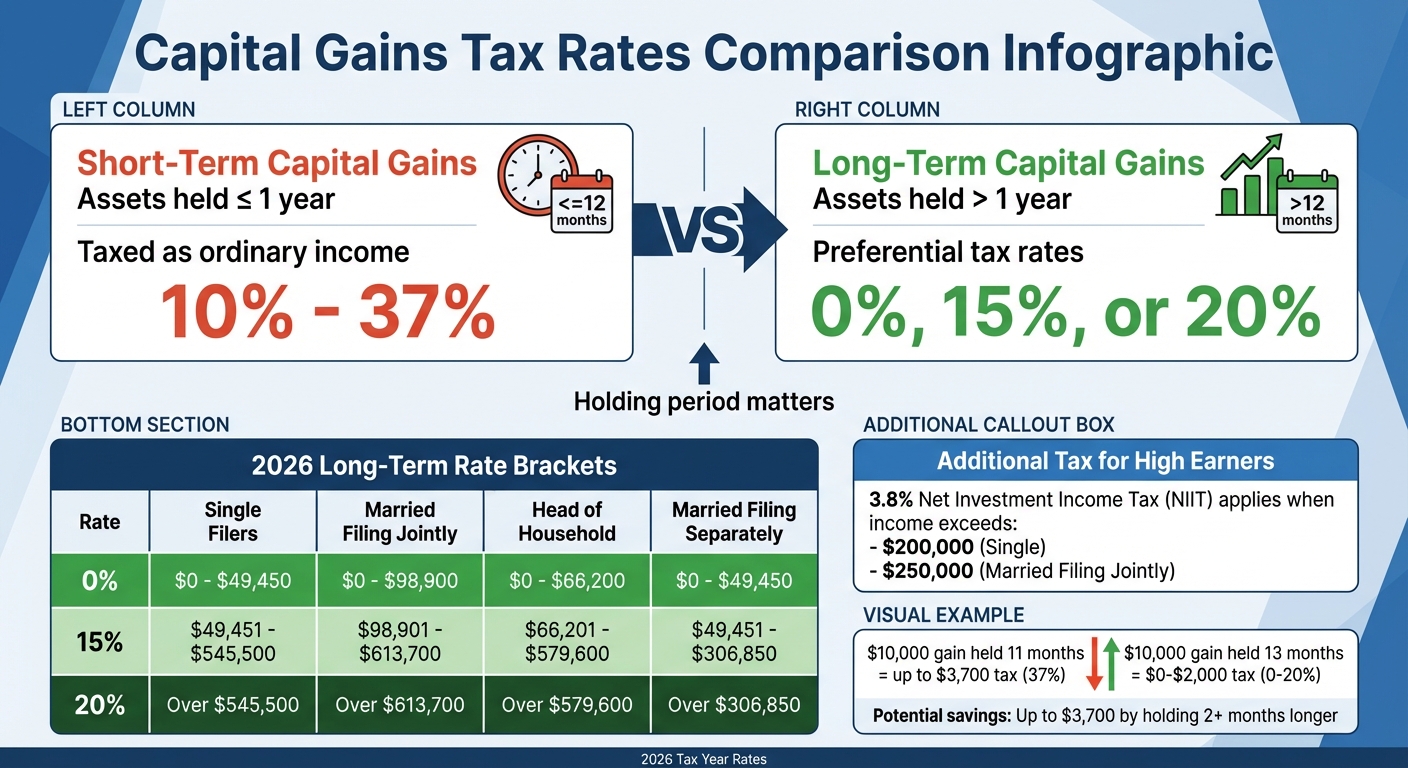

- Short-term gains (assets held for 1 year or less) are taxed as ordinary income, up to 37%.

- Long-term gains (assets held for over 1 year) are taxed at lower rates: 0%, 15%, or 20%, depending on income.

- Income over $200,000 (single) or $250,000 (married) may also face a 3.8% Net Investment Income Tax.

Why it matters: Taxes reduce the money you can reinvest, and over time, this "drag" compounds. Reinvesting tax savings may provide additional growth over time.

How to calculate manually:

- Cost Basis: Start with your purchase price plus fees.

- Net Proceeds: Subtract selling costs from the sale price.

- Gains/Losses: Subtract cost basis from net proceeds.

- Tax Rates: Apply the correct rate based on holding period and income.

Simplify the process with Mezzi: This AI-powered tool connects to your accounts, tracks holding periods, flags tax-saving opportunities like tax-loss harvesting and deferral, and calculates your capital gains liability in real time.

For $299/year and up, Mezzi helps you avoid errors, pursue tax-efficient strategies, and monitor after-tax outcomes - all without moving your assets or paying high advisor fees.

Short-Term vs Long-Term Capital Gains Tax Rates 2026

Capital Gains Tax Explained: Why You DON'T Pay 0%, 15%, or 20% (The Real Math)

How to Calculate Capital Gains Taxes Manually

Breaking down the manual steps of calculating capital gains taxes helps highlight how tools like Mezzi's AI tax-loss harvesting simplify the process. The calculation involves four key steps: figuring out your cost basis, determining your net proceeds, calculating gains or losses, and applying the correct tax rate.

Step 1: Determine Your Cost Basis

Your cost basis is essentially what you initially invested in the asset, adjusted for certain factors. This typically includes the purchase price plus transaction fees, commissions, and other adjustments [8,9,12]. For stocks and ETFs, it’s the price per share plus brokerage fees. For example, if you purchased 100 shares at $50 each and paid a $10 commission, your total cost basis would be $5,010.

If a stock split occurs (e.g., a 2-for-1 split), you’ll need to adjust the share price accordingly [8,12]. For mutual funds, many investors rely on the Average Cost Method, dividing the total investment amount by the number of shares owned [9,10,12]. For real estate, the cost basis includes the purchase price, closing costs (like title insurance and legal fees), and major improvements (such as adding a new roof). Routine repairs, like fixing a leak, don’t count [9,12,13].

"Cost basis is the original value of an asset for tax purposes, usually, the purchase price, adjusted for stock splits, dividends, and return of capital distributions." - Kieth Sipes, District Sales Analyst

Reinvested dividends should also be included in your cost basis to avoid paying taxes on them twice [8,9,12]. Keeping records of Dividend Reinvestment Plan (DRIP) purchases is crucial to avoid errors.

Once you’ve established your cost basis, the next step is calculating the net proceeds from the sale.

Step 2: Calculate Net Proceeds

Net proceeds are what you actually receive from the sale after subtracting transaction-related costs [5,16]. This means deducting commissions, fees, and closing costs from the gross sale price [16,17].

For instance, in an example from Virtue CPAs, an investor sold shares for $15,000 but paid $100 in transaction fees. The net proceeds were $14,900 ($15,000 - $100).

"Determine your net proceeds. This is the sale price minus any commissions or fees paid." - H&R Block

Step 3: Calculate Gains or Losses

Once you know your cost basis and net proceeds, you can calculate your gains or losses. Subtract the cost basis from the net proceeds. For example, if you sold shares for $14,900 and your cost basis was $5,010, your capital gain would be $9,890 ($14,900 - $5,010).

If the net proceeds are lower than the cost basis, you’ll incur a capital loss. The IRS allows up to $3,000 of net capital losses to offset ordinary income each year, with any remaining losses carried forward to future years [5,11,13].

Step 4: Apply Tax Rates

The final step is applying the appropriate tax rate, which depends on how long you held the asset and your income level. Short-term gains (assets held for one year or less) are taxed as ordinary income, with rates ranging from 10% to 37% [11,18]. Long-term gains (assets held for more than one year) benefit from lower rates of 0%, 15%, or 20% [18,19].

For 2026, single filers with taxable income up to $49,450 pay 0% on long-term gains, while those earning over $545,500 are taxed at 20% [18,19]. High-income earners may also face a 3.8% Net Investment Income Tax if their modified adjusted gross income exceeds $200,000 (single) or $250,000 (married filing jointly) [11,18].

| Rate | Single | Married Filing Jointly | Head of Household | Married Filing Separately |

|---|---|---|---|---|

| 0% | $0 to $49,450 | $0 to $98,900 | $0 to $66,200 | $0 to $49,450 |

| 15% | $49,451 to $545,500 | $98,901 to $613,700 | $66,201 to $579,600 | $49,451 to $306,850 |

| 20% | Over $545,500 | Over $613,700 | Over $579,600 | Over $306,850 |

For example, suppose an investor bought shares for $5,000 and sold them for $12,000, incurring $100 in fees. The net proceeds would be $11,900, resulting in a long-term capital gain of $6,900. If the investor’s taxable income falls in the 15% bracket, the tax liability would be $1,035 ($6,900 x 0.15).

Using Mezzi's Capital Gains Tax Calculator

Tracking cost basis, holding periods, and tax rates manually across multiple accounts can be a headache - and prone to mistakes. Mezzi simplifies the entire process by securely connecting to your investment accounts and calculating your capital gains tax liability in real time. Here’s how linking your accounts with Mezzi creates a complete tax overview.

Connecting Accounts for a Complete Tax Picture

Mezzi connects to thousands of financial institutions - including big names like Schwab and Chase - using secure, read-only access through trusted aggregators such as Plaid and Finicity (Mastercard). In just about two minutes, you can link all your accounts - whether they’re 401(k)s, traditional brokerages, Roth IRAs, or taxable accounts. This unified view is essential for tax planning because it allows Mezzi to monitor your entire portfolio. For instance, if you sell at a loss in one account but repurchase the same stock in your 401(k) within 30 days, the IRS wash sale rule kicks in, disallowing the deduction. By connecting your accounts, Mezzi identifies such scenarios and automates tax estimations across your portfolio.

Automating Tax Estimations Across Portfolios

Once your accounts are linked, Mezzi performs daily monitoring of your portfolio to calculate your total capital gains tax liability. It tracks every position to determine when holdings transition from short-term to long-term status. Timing is critical here - selling at 11 months could mean paying ordinary income tax rates of up to 37%, while waiting just one more month might qualify you for long-term capital gains rates, which can be as low as 15% or even 0%, depending on your income. This automated tracking helps you plan sales to help you pursue after-tax efficiency.

Key Insights Delivered by Mezzi

Beyond just estimations, Mezzi equips you with actionable strategies to save on taxes. For example, it sends tax-loss harvesting alerts when a position dips below your cost basis, giving you a chance to offset future gains. These opportunities can disappear quickly as markets rebound, so Mezzi’s daily tracking ensures you stay ahead. It also monitors wash sale risks across all connected accounts, letting you know when the IRS’s 30-day window has passed so you can safely repurchase securities without losing your deduction.

Another standout feature is Mezzi’s X-Ray tool, which reveals hidden stock exposures in ETFs and mutual funds. This helps you spot overlapping holdings that could lead to unintended tax hits when rebalancing.

"Mezzi's X-Ray feature allowed me to uncover exposure to stocks I didn't realize I had."

– Shuping, Founder of Summer AI

Additionally, Mezzi provides holding period alerts, notifying you when positions are nearing the 12-month mark. This gives you the option to hold on for long-term capital gains treatment or sell sooner if needed. All of these insights are tailored to your actual portfolio, thanks to Mezzi’s AI-powered interface, which goes beyond generic calculators to deliver strategies intended to support tax efficiency.

Tax Optimization Strategies with Mezzi

Mezzi provides a thorough portfolio overview to help reduce tax liabilities and support tax-efficient outcomes. By keeping an eye on your portfolio daily, Mezzi identifies year-round opportunities to save on taxes.

Identifying Tax-Loss Harvesting Opportunities

Tax-loss harvesting is a strategy where you sell underperforming assets at a loss to offset taxable gains. Here's an example: if you harvest $6,000 in losses, it can reduce $10,000 in gains to a net taxable gain of just $4,000. This method is especially useful for offsetting short-term capital gains, which can be taxed at rates as high as 37% for some individuals. For instance, if you harvest $15,000 in losses to offset $15,000 in short-term gains, someone in the highest tax bracket could see significant tax effects, depending on their individual situation.

Mezzi simplifies this process by monitoring your portfolio daily. It alerts you when assets drop below their cost basis, signaling potential harvesting opportunities. The platform goes a step further by identifying the most strategic positions to sell first - like assets where you’re overweighted or those taxed at higher rates, such as collectibles (28%) or real estate with unrecaptured depreciation (25%). For high-income earners subject to the 3.8% net investment income tax (NIIT), harvested losses can offset gains taxed at a combined rate of 23.8%, compared to 20% for others.

However, successfully implementing this strategy also means staying mindful of risks, such as inadvertently triggering wash sales.

Managing Wash Sale Risks Across Accounts

Harvesting losses is only effective if you avoid violating the IRS wash sale rule. This rule disallows a deduction if you buy back the same or a substantially identical security within 30 days before or after selling it at a loss. The rule applies across all accounts, so selling Apple stock in a taxable account and repurchasing it in a 401(k) within 30 days would invalidate the deduction.

Mezzi helps by tracking all connected accounts simultaneously, flagging potential wash sale violations before they happen. Once you harvest a loss, the platform monitors the 30-day window, letting you know when it’s safe to repurchase the security without risking your deduction. If you want to maintain market exposure during this period, you can opt for alternatives - like switching to a similar index fund from another provider or moving from an individual stock to a broader sector ETF.

Rebalancing Portfolios in a Tax-Efficient Way

Tax-efficient rebalancing allows you to adjust your portfolio while minimizing taxes. This often involves selling positions that have lost value to offset gains, and using new cash contributions to buy underweighted assets instead of selling appreciated holdings.

For example, if your portfolio is heavy on stocks but light on bonds, you could sell underperforming stocks at a loss and use new contributions to bolster your bond allocation. This approach ensures you maintain your target allocation without triggering unnecessary taxes. Mezzi’s tools make it easier to execute this strategy by providing clear visibility into overlapping holdings with its X-Ray feature and offering actionable rebalancing suggestions. Depending on factors like market conditions and portfolio activity, this approach may improve after-tax efficiency, depending on individual circumstances.

Conclusion

Mezzi's capital gains tax calculator removes the hassle of managing investment taxes. By securely connecting all your accounts - like 401(k)s, brokerages, and Roth IRAs - through read-only access, it offers a complete view of your tax situation. No more juggling spreadsheets or waiting endlessly for an advisor’s callback. The platform updates your portfolio daily, keeping track of holding periods to help you shift from short-term to long-term gains - potentially lowering your tax rate, depending on how long investments are held.

Mezzi doesn’t just monitor; it provides real-time, actionable insights. It highlights tax-loss harvesting opportunities as they arise, tracks 30-day wash sale windows across all accounts to safeguard deductions, and offers guidance on minimizing taxes during rebalancing.

What makes Mezzi stand out is its simplicity and control. You don’t need to transfer assets or give up custody - everything stays exactly where it is. For $199 per year, you gain access to advanced tax planning and portfolio analysis, avoiding the typical 1% AUM fee charged by traditional advisors. Over 30 years, that could mean saving more than $1 million. Plus, you can ask questions, get tailored answers based on your accounts, and act when you’re ready.

Whether you're planning a sale to lock in long-term rates, harvesting losses during market dips, or rebalancing with minimal tax impact, Mezzi equips you with the tools to make smarter, tax-efficient decisions. It simplifies the complexities of tax planning, so you can focus on building your wealth.

FAQs

What counts toward my cost basis?

Your cost basis is the original price you paid for your investments, but it doesn’t stop there. It’s adjusted to account for things like stock splits, dividends, or return of capital. Why does this matter? Because your cost basis is key to figuring out your capital gains or losses when you decide to sell.

How do I avoid a wash sale across accounts?

To steer clear of triggering a wash sale across accounts, make sure you don’t buy back a "substantially identical" security within 30 days before or after selling it at a loss. This is a key requirement under IRS rules. Tools like Mezzi can simplify this process by monitoring your portfolio in real-time. They provide alerts and tailored recommendations, helping you effectively manage wash sale windows while fine-tuning your tax-loss harvesting strategies.

When should I wait to qualify for long-term gains?

To benefit from long-term capital gains tax rates, you need to hold onto your investment for more than one year before selling it. These gains are taxed at a lower rate compared to short-term capital gains, which apply to investments sold within one year or less.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.