Coast FIRE may mean this: you save enough early that your portfolio may reach your retirement target later, even if you stop adding new retirement contributions now. You still work to cover current bills. You just may no longer need to keep saving for retirement if the math holds.

Here’s the short version:

- I’d treat Coast FIRE as a calculation, not a retirement date

- The core math may come down to retirement spending × withdrawal rate × years left

- A portfolio target of $1,500,000 at age 65 may require about $197,000 today at a 7% real return or about $347,000 at a 5% real return

- Small changes in returns, inflation, spending, taxes, and timeline may move the number a lot

- Missing accounts, tax differences, high fees, or single-stock exposure may give a false sense of progress

- Some people use a buffer of 10% to 20% and review the plan each year

Coast FIRE may sound simple. But the hard part may be the assumptions. If I stop contributions too early, weak market returns, higher spending, or tax blind spots may push the target out.

Here’s a quick snapshot of how Coast FIRE compares with other FIRE paths:

| Approach | Working now? | Adding retirement savings? | Portfolio use |

|---|---|---|---|

| Coast FIRE | Yes | No | May grow until retirement |

| FIRE | No | No | May fund life now and later |

| Lean FIRE | No | No | May fund a lower-spend life |

| Fat FIRE | No | No | May fund a higher-spend life |

| Barista FIRE | Part-time | No | May support partial withdrawals |

If I were checking whether Coast FIRE may fit, I’d focus on five numbers first: retirement spending, FI target, real return, Coast FIRE number, and current invested balance after tax differences. That may give a much cleaner view than relying on one account balance or a rough guess.

Coast FIRE Explained (With Real Life Examples!)

How to Calculate Your Coast FIRE Number

Coast FIRE Number by Age: How Much You Need to Save Today

Coast FIRE math has three steps: estimate retirement spending, turn that into an FI number, then discount that target back to today.

Start With Your Retirement Spending Goal and FI Number

Start by estimating what you may spend each year in retirement, in today’s dollars. That estimate may need to account for costs that may move the number in a big way, like healthcare before Medicare starts at 65, taxes, and any lifestyle drift you expect.

Once you have that annual spending estimate, divide it by your safe withdrawal rate (SWR) to get your FI number. That’s the total portfolio size you may need in order to retire. The standard 4% rule uses a multiplier of 25x annual spending, while a more conservative 3% rate pushes that to 33x.

So if you expect to spend $80,000 per year in retirement, your FI number may be $2,000,000 at 4% or $2,640,000 at 3%. That target may then serve as your Coast FIRE number once you work backward to today’s balance.

Use Real Return Assumptions, Not Nominal Returns

Use real returns, not nominal returns. Real returns are growth after inflation.

Real return = ((1 + nominal return) / (1 + inflation)) − 1

If your FI number is expressed in today’s dollars, using nominal returns may make your Coast FIRE number look far too low over long time periods. Historical U.S. equity returns have averaged about 7% after inflation, though many planners use 4% to 5% real for a more conservative estimate. Use the wrong return basis, and the number may look smaller than it may actually be.

Work Backward From Your FI Number to Today's Balance

With your FI number and real return in hand, the last step is figuring out what you may need today. The formula is:

Coast FIRE Number = FI Number ÷ (1 + Real Return)^Years to Retirement

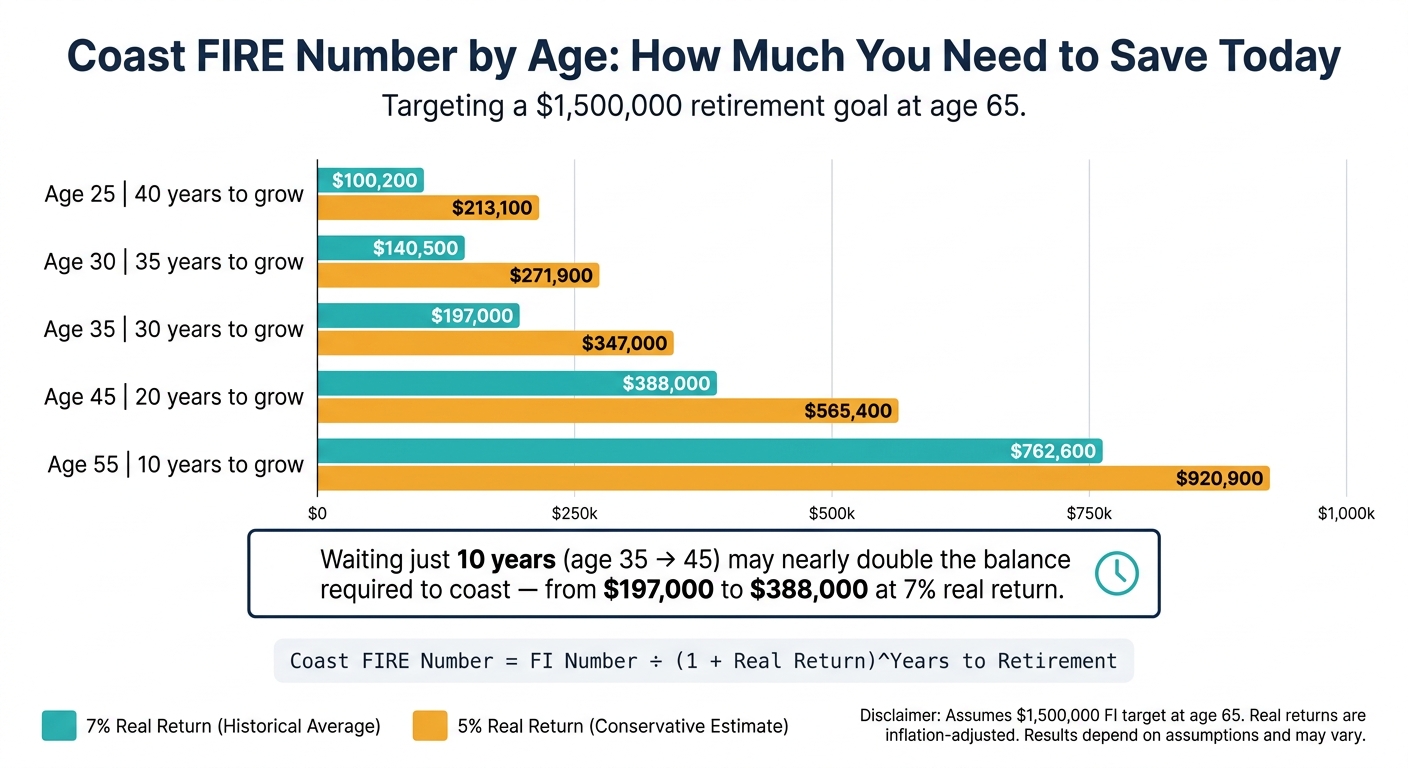

Here’s a simple example. Say you’re 35 years old, want to retire at 65, and your FI number is $1,500,000. With a 7% real return over 30 years, your Coast FIRE number may be about $197,000. Lower that return assumption to 5%, and the same target may require about $347,000 today - a 76% increase from one conservative adjustment.

The table below shows how the required balance may shift by current age, all while targeting the same $1,500,000 at age 65:

| Current Age | Years to Grow | 7% Real Return | 5% Real Return |

|---|---|---|---|

| 25 | 40 | $100,200 | $213,100 |

| 30 | 35 | $140,500 | $271,900 |

| 35 | 30 | $197,000 | $347,000 |

| 45 | 20 | $388,000 | $565,400 |

| 55 | 10 | $762,600 | $920,900 |

Every five years of delay may increase the balance you’d need today, which is why some people stress-test the math at both 5% and 7% real returns. The result still depends on assumptions, and those assumptions may not hold.

What Can Break the Plan: Assumptions, Volatility, and Data Gaps

The math may look simple. The assumptions behind it may not.

That’s why it often makes sense to treat your Coast FIRE number as a range, not a fixed target. Small shifts in return, inflation, spending, or timing may move the result a lot - before retirement contributions stop.

Start with the inputs that may change the answer the most.

The 4 Inputs That Move Your Coast FIRE Number

Every Coast FIRE calculation depends on four core variables: expected real return, safe withdrawal rate (SWR), annual retirement spending, and time horizon. Even a five-year delay may add tens of thousands to the target.

The biggest swing often comes from real return. A one-point gap - say, 5% versus 4% - may change the required Coast FIRE balance by 20% to 30% over a 25-year horizon. The SWR matters too. Moving from a 4% withdrawal rate to a more conservative 3.5% may increase the full FI number, and that higher figure flows straight into a higher Coast FIRE requirement.

Spending may be just as sensitive. If the estimate is off, the rest of the plan may be off with it. A move from $50,000 to $65,000 in annual retirement spending increases both the FI number and the Coast FIRE number in proportion.

Using nominal returns instead of real, inflation-adjusted returns is not a small miss. It may break the plan.

Why Market Volatility Hits Harder When You Stop Contributing

Even if the Coast FIRE number is right, the plan may still go sideways if returns show up in the wrong order.

Poor returns early in the no-contribution phase may delay retirement even when long-term averages recover later. A long stretch of weak returns - like the period from 1966 to 1982, when U.S. equities produced annualized real returns of about 1% to 2% - shows how rough timing may be.

Here’s how the starting balance changes for a 35-year-old with a $1.5 million FI target and a 25-year horizon:

| Scenario | Real Return | Coast FIRE Number |

|---|---|---|

| Conservative | 4% | $562,400 |

| Moderate | 5% | $443,000 |

| Optimistic | 6% | $349,700 |

| Aggressive | 7% | $276,200 |

Some people run their plan against a conservative case to leave more room for bad markets.

Missing Account Data Can Lead to Bad Decisions

The last risk may not come from the market at all. It may come from missing data.

A common mistake is building projections from an incomplete view of household assets. That may mean forgetting an old 401(k) from a past employer, leaving out a spouse’s IRA, or missing an HSA or taxable brokerage account.

Account type matters too. A $1 million pre-tax balance may be worth less than $1 million in Roth assets after taxes. Treating them as the same may overstate Coast FIRE progress on paper.

Concentrated stock positions add another hidden risk. RSUs or a large stake in one company may make a portfolio look diversified by total value, even when a big slice depends on a single stock.

Home equity and emergency cash usually are not counted as Coast FIRE assets. They do not support the compounding this formula assumes.

A proper Coast FIRE check may need every account, every tax type, and every owner in one view.

How to Reach Coast FIRE Earlier Without Flying Blind

Front-Load Savings While Your Time Horizon Is Longest

Once the math is set, the next move may be simple: save more while time may do the most work. If someone is aiming for Coast FIRE, heavier saving earlier may lower the amount they may need later. A dollar invested at 30 may grow far more by retirement than a dollar invested at 60. And each year of waiting may push the required Coast FIRE balance higher.

That delay may add up fast. The earlier someone reaches their Coast FIRE number, the more time the portfolio may have to grow without new contributions.

Some people start with the full employer match, then use Roth IRA and workplace-plan contribution room before putting money into taxable accounts. In 2026, Roth IRA contributions are capped at $7,500 ($8,600 if you're 50 or older), and 401(k)/403(b) contributions go up to $24,500 ($32,500 if you're 50 or older). If that tax-advantaged room runs out, a taxable brokerage account may add more runway.

Track Progress Across 401(k)s, IRAs, HSAs, and Taxable Accounts

Saving early may only tell part of the story if the accounts aren't tracked together. A Coast FIRE number may only be as good as the data behind it. Looking at one account at a time may create a broken picture, and that may lead to poor decisions.

The full picture may include every invested account in one place. It may leave out home equity, vehicles, and emergency cash, since those don't compound toward a retirement goal in the same way. Another common miss: tracking the gross balance instead of the amount that may be spendable after taxes. That may matter most with pre-tax accounts like a traditional 401(k), where part of the balance may later go to taxes.

Fees are another quiet issue. A 1% investment fee may compound against an investor the same way returns may compound in their favor - slowly, year after year - potentially pushing up the balance needed to coast. Seeing expense ratios across all accounts, not just one brokerage, may make progress tracking more grounded.

Use Mezzi to Check Your Coast FIRE Plan Against Real Data

A consolidated view may make it easier to test whether a Coast FIRE number still lines up with current account data. Mezzi pulls accounts into one view so users may check their Coast FIRE plan against current balances, fees, and allocation. Through read-only access via Plaid and Finicity, it connects to 401(k)s, IRAs, HSAs, and taxable accounts without requiring account transfers or login credentials. As an SEC-registered fiduciary, Mezzi has a legal duty to act in clients' best interest, which may give users another way to review a Coast FIRE plan using current balances, fees, and allocation instead of relying only on a spreadsheet.

Is Coast FIRE Right for You? Trade-Offs, Guardrails, and Next Steps

When Coast FIRE Makes Sense and When It Does Not

Once your numbers are on the page, the next step is simpler: figure out whether Coast FIRE may fit your life.

Coast FIRE may make the most sense for high earners who front-loaded their savings and now want more flexibility without fully retiring. If someone has already built a solid portfolio, coasting may give them room to take a lower-stress job, go part-time, or spend more time on work they enjoy, while compounding may do more of the heavy lifting.

It may be less suitable for anyone with unstable income or unclear spending needs. If retirement costs are still fuzzy, or lifestyle creep is already part of the pattern, the plan may drift over time.

The trade-off here is flexibility, not certainty.

| Feature | Coast FIRE | Keep Contributing |

|---|---|---|

| Immediate Flexibility | High | Low |

| Required Savings Pace | Front-loaded | Sustained |

| Reliance on Market Growth | Extreme | Moderate |

| Planning Complexity | High | Moderate |

For early retirees, healthcare is one of the first costs that may change the math. Health insurance needs to be part of the budget, and ACA premiums may run $14,400 to $28,000 per year depending on income and location.

Guardrails That Make a Coast FIRE Plan More Durable

If Coast FIRE seems like a fit, the plan may hold up better with conservative assumptions and clear restart rules.

Once contributions stop, bad markets may hurt more because there may be less room to make up the gap with new money. One common way some people stress-test the plan is by using a 4% real return instead of 7% real return. That small shift may change a Coast FIRE number by 20% to 30% over a 25-year horizon.

Another guardrail is building a 10% to 20% buffer above the calculated Coast FIRE number before stopping contributions. Some people also set clear rules for when they may restart contributions, such as if the portfolio falls well below its projected growth curve or spending moves above a preset limit.

Annual reviews matter here. Spending drift is a common weak spot. If a $60,000 budget becomes $80,000 because spending habits changed, the original Coast FIRE number may no longer be enough. Reviewing the plan each year - and adjusting for actual portfolio results, inflation, and any shifts in retirement goals - may keep the math grounded.

Conclusion: The Key Numbers to Know Before You Stop Contributing

That review should end with a short checklist, not a vague feeling.

Before contributions stop, five numbers need to be clear:

- your retirement spending goal in today's dollars

- your FI number (typically 25x annual spending)

- your real return assumption (inflation-adjusted)

- your Coast FIRE number (the FI number discounted back to today)

- your current invested balance across all accounts, adjusted for taxes

"Hitting your Coast FIRE number should feel like progress, not like a finish line... the milestone that actually changes your life is full financial independence." - Jared Lundrigan, Founder, Efficient Dollar

It may help to treat Coast FIRE as a live threshold, not a one-time calculator result. The Coast FIRE number may work better as a checkpoint, then get reviewed again as spending, returns, and taxes change.

FAQs

How do I know if I’ve really reached Coast FIRE?

You’ve reached Coast FIRE when your current retirement investment balance meets or exceeds your calculated Coast FIRE number.

When you compare balances, use only invested retirement assets. That may include accounts like a 401(k) or IRA. Don’t include non-invested assets like home equity or emergency savings.

Your Coast FIRE number is your full FI target, discounted based on your expected real annual return over the years until retirement. If your portfolio is at or above that number, it may be on track to grow to your retirement goal without added contributions.

Which accounts should count toward my Coast FIRE number?

Include all tax-advantaged retirement accounts, such as your 401(k), IRA, and Roth IRA. Depending on your plan, you may also want to include taxable investment accounts.

One catch: tax treatment may differ across accounts. Traditional 401(k)s and IRAs are generally taxed later, while Roth accounts may allow tax-free withdrawals. So when you estimate retirement purchasing power, it may make sense to factor in those differences instead of treating every dollar the same.

What should I do if market returns fall short after I stop contributing?

If market returns underperform, your portfolio may not reach its target by your retirement date. Coast FIRE relies on projections, not guarantees, so it may make sense to check your progress on a regular basis and stay flexible.

If returns fall short, some people adjust by resuming contributions, working longer, or lowering future spending expectations.

Disclosures:

• This content is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.

• Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.

• Savings and performance examples are hypothetical and for illustrative purposes only. Actual results will vary based on individual circumstances, portfolio composition, market conditions, and fees.

Related Blog Posts

- What portfolio value and withdrawal strategy would generate a specific monthly after-tax income?

- Create projections if I invest only half my planned amount until retirement - how does this change the goal timeline?

- Late Start Retirement: Catch-Up Contribution Strategies

- Retirement Planning at 50: How to Assess If You Have Enough

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.