A single stock may build wealth fast - and may also leave a portfolio exposed. If selling may trigger a large tax bill, three tools often come up: collars for downside limits, prepaid variable forwards for cash now with tax deferral, and exchange funds for diversification without an immediate sale.

Here’s the short version:

- Collars may put a floor under losses, but they may cap upside and do not provide cash.

- Prepaid variable forwards may provide upfront cash - often a large share of the stock’s value - while taxes may be deferred until maturity, but upside may be limited and the setup may be complex.

- Exchange funds may swap single-stock risk for a pool of stocks with tax deferral, but money may be tied up for about seven years and there may be no upfront cash.

A few facts frame the issue:

- A large share of individual stocks in long-run data fell more than 75% and did not recover in a meaningful way.

- For some high-income investors, federal long-term capital gains tax may reach 23.8% before state tax.

- In states like California, combined tax on a sale may run much higher.

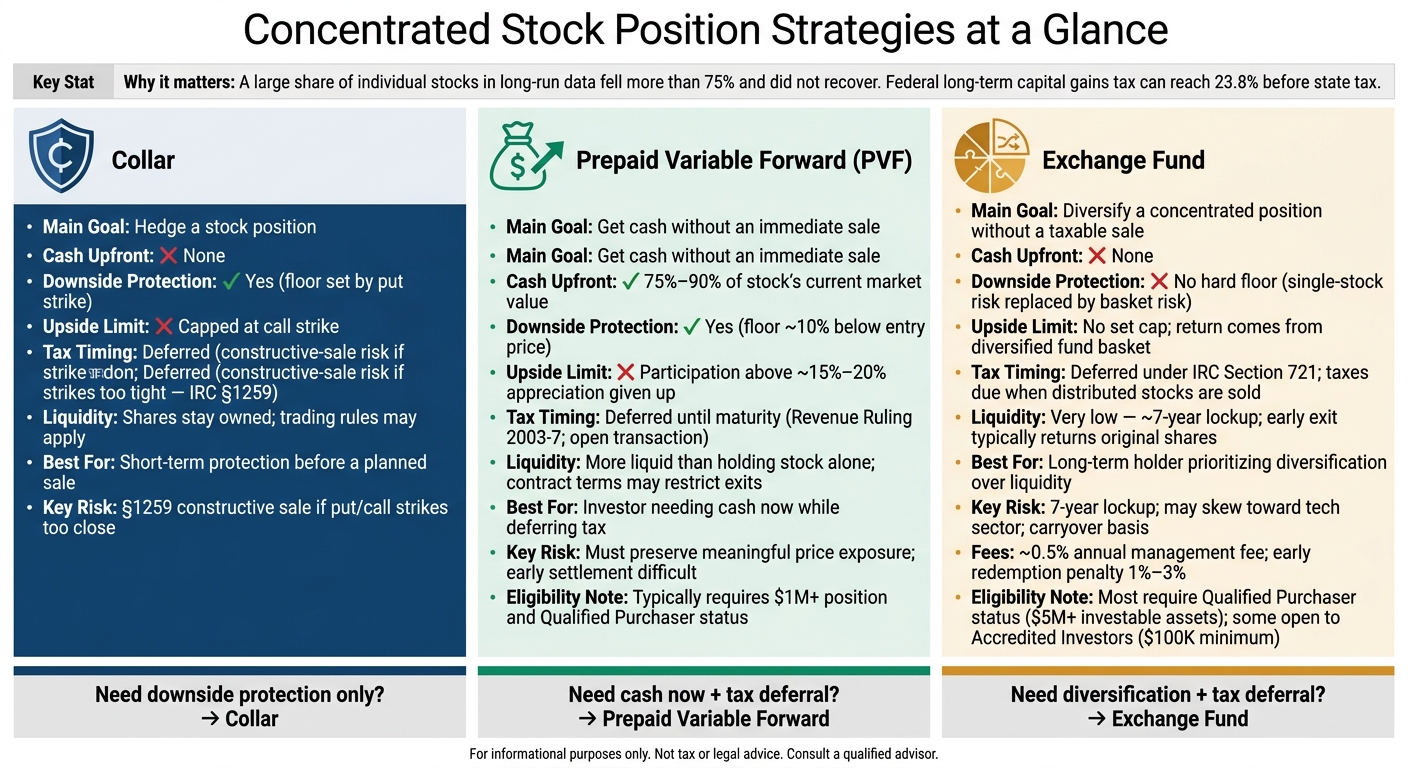

Collars vs. Prepaid Variable Forwards vs. Exchange Funds: Concentrated Stock Strategy Comparison

Managing Concentrated Stock Positions (with Ben Lake, CFA®, CFP®)

Quick Comparison

| Tool | Main goal | Cash upfront | Downside limit | Upside limit | Tax timing | Liquidity |

|---|---|---|---|---|---|---|

| Collar | Hedge a stock position | No | Yes, within the hedge terms | Yes | Tax may be deferred, but some setups may face constructive-sale issues | Shares stay owned, but trading rules may apply |

| Prepaid Variable Forward | Get cash without an immediate sale | Yes | Yes, within the contract terms | Yes | Tax may be deferred until maturity if the setup meets IRS rules | More liquid than holding stock alone, but contract terms may restrict exits |

| Exchange Fund | Diversify a concentrated position | No | No hard floor | No set cap, but return comes from the fund basket | Tax may be deferred under Section 721 | Low near-term liquidity due to lockup |

If I had to reduce this article to one line, it would be this: each tool solves a different problem, and the tradeoff usually shows up in taxes, liquidity, or lost upside.

1. Collars

For investors who may want to keep the stock but put some limit on losses, a basic hedge may be a collar.

A collar pairs a protective put with a covered call on the same stock. In a zero-cost collar, the premium from selling the call may offset the cost of buying the put, so there may be no out-of-pocket cost to put the hedge in place.

Downside Protection

The put may set a floor on losses. The stock may still move as usual within the range between the put strike and the call strike.

Liquidity & Cash Access

A collar does not create cash. The shares may still support margin borrowing, but lock-ups and Rule 144 limits may affect when the collar may be opened or how it may settle.

Tax Timing

Entering a collar usually may not trigger tax right away. The IRS may treat a tight collar as a constructive sale under IRC §1259. Tighter strikes may be associated with more constructive-sale risk. IRC §1092 may also pause the holding period, which may affect long-term gain treatment.

Upside & Flexibility

The tradeoff is capped upside above the call strike. Collars are often used before a known liquidity event or planned exit. Insiders may still need compliance review before using a collar.

When an investor may want both downside protection and upfront cash, the next tool may be a prepaid variable forward.

2. Prepaid Variable Forwards

If a collar may limit downside but doesn't put cash in your hands, a prepaid variable forward (PVF) may do both. With a PVF, an investor receives cash today in exchange for delivering a number of shares that adjusts based on the stock price at maturity, often two to five years later. In plain English: it pairs downside protection with upfront liquidity, which may appeal to someone who wants cash now without an immediate taxable sale.

Downside Protection

A PVF sets a floor that may protect against declines beyond about 10% from the stock's value when the contract begins. Unlike a standalone collar, the hedge and the cash feature sit inside the same contract.

Liquidity & Cash Access

Investors typically receive 75% to 90% of the stock's current market value upfront in cash. That cash may be used for diversification, spending, or other planning needs. A PVF may let someone monetize a concentrated position without an immediate share sale.

These contracts are generally used by high-net-worth investors with positions above $1 million and Qualified Purchaser status.

That upfront cash also changes the tax picture, which is where PVFs tend to stand apart from collars.

Tax Timing

The upfront cash payment is not a taxable event when received. Under Revenue Ruling 2003-7, the IRS treats a PVF as an open transaction, so capital gains taxes may be deferred until the contract matures. But the structure needs to keep real upside and downside exposure. If not, the IRS may view it as a constructive sale. If the spread is too tight, the IRS may recharacterize the contract as a sale.

Upside & Flexibility

The tradeoff for getting cash now is pretty simple: you may give up part of the stock's future gain. In many cases, participation above roughly 15% to 20% of the stock's appreciation is given up. For some investors, that may feel like a fair swap. For others, it may be too much of the upside to part with.

Insiders also need to coordinate PVFs with trading windows, 10b5-1 plans, and short-swing rules. At the center of the structure is a plain tradeoff: more cash now, less upside later.

For investors who may want diversification instead of cash, exchange funds are the next step.

3. Exchange Funds

Unlike collars and prepaid forwards, an exchange fund is built around diversification, not cash access or a set level of price defense. Instead of selling a concentrated position, you contribute appreciated shares to a private partnership with other investors doing the same. In return, you get a pro-rata interest in a more diversified pool of stocks without selling a single share.

The tax deferral piece generally relies on IRC Section 721, which treats the contribution as a non-taxable event. Your original cost basis carries over to the fund units, and later to the basket of stocks you receive when you exit. To keep that tax treatment, the fund usually needs to hold at least 20% of its assets in illiquid holdings, often real estate.

Downside Protection

Exchange funds do not provide a hard floor like a collar may. The idea is simpler than that: you trade single-company risk for exposure to a broader stock pool. That may help if the main concern is a collapse in one company, but it may not offer much shelter in a broad market sell-off.

There’s also a catch. Some exchange funds may end up heavily tilted toward technology, so the trade may shift risk from one stock to one sector.

Liquidity & Cash Access

To keep the tax deferral, investors usually remain in the fund for at least seven years. If someone exits early, they usually get back their original shares, so the diversification benefit may be delayed. There’s no upfront cash, no built-in income stream, and not much room to maneuver during the lockup.

"An exchange fund might be able to help diversify her concentrated holding in a tax-efficient way, but it would also severely impact her liquidity – replacing one risk (having most of her net worth in shares of a single stock) with another (having most of her net worth entirely inaccessible for a seven-year period)." - Ben Henry-Moreland, Senior Financial Planning Nerd, Kitces.com

Annual management fees may run around 0.5%, versus roughly 0.2% for a standard index fund, and early redemptions may come with penalties of 1% to 3%.

Tax Timing

The contribution is generally tax-deferred under Section 721, and taxes usually come due only when the distributed stocks are later sold. Over time, that delay may matter. One estimate puts the benefit at more than 2.3% per year versus selling and reinvesting.

Upside & Flexibility

After seven years, you receive a diversified basket instead of the original single stock. You don’t pick the stocks in that basket; the manager does, often with the aim of tracking a broad index such as the S&P 500 or Nasdaq-100. Most funds require Qualified Purchaser status, meaning $5 million or more in investable assets, though some may be open to Accredited Investors with minimum contributions as low as $100,000. A step-up in basis at death may remove the deferred gain.

So the trade-off is pretty plain: more diversification, but less liquidity and no current cash payout. For some investors, that may fit better when the main goal is reducing concentration without triggering an immediate sale.

Pros and Cons of Each Strategy

Use the table below to line up each tool with the constraint that may matter most: downside protection, cash, or diversification. It narrows the choice to the tradeoffs that may matter most in practice: cost, cash access, tax timing, and limits on upside.

| Strategy | Key Pros | Key Cons | Best For | Watchouts |

|---|---|---|---|---|

| Collar | Low upfront cost; downside floor; tax deferral | Upside capped at the call strike; possible tax on option gains | Investor needing short-term protection before a planned sale | §1259 constructive sale risk if put and call strikes are too close together |

| Prepaid Variable Forward | Upfront cash equal to 75%–90% of stock value; tax deferral until maturity; no margin calls | High complexity; counterparty risk; fees; shares must be delivered at maturity | Investor who needs cash now and wants to defer tax | Must preserve meaningful price exposure; early settlement is difficult |

| Exchange Fund | Diversification without a taxable sale; tax deferral | Seven-year lockup; carryover basis | Long-term holder who prioritizes diversification over liquidity | May skew toward tech; early exit usually returns original shares |

A few rules cut across all three strategies.

For collars and prepaid forwards, overly tight hedges may trigger constructive-sale treatment under IRC §1259 if they remove too much economic risk. In many cases, a wider spread may reduce that risk.

Exchange funds require a seven-year hold, and an early withdrawal would typically trigger gain recognition.

Corporate insiders may face extra limits under Section 16 and 10b5-1 cooling-off periods. Those rules may affect how quickly any of these strategies may be put on or unwound.

Conclusion

Taken together, these tools may address three different concentrated-position problems. Collars may cap downside. Prepaid variable forwards may provide upfront cash while deferring tax. Exchange funds may trade liquidity for diversification for a concentrated stock position.

From there, the choice may come down to personal constraints. That may include liquidity needs, time horizon, cost basis, tax rate, and available losses.

For a concentrated stock position, different tranches may call for different tools. Some investors match each tool to the right tranche of stock. Tax, legal, and fiduciary review may be part of the process before acting. In setups like these, structure may matter more than speed.

FAQs

How do I choose between a collar, a prepaid variable forward, and an exchange fund?

Choose based on your goals for liquidity, diversification, and tax deferral.

- Some investors use a collar to limit downside and cap upside, often as a way to buy time for a staged exit.

- A prepaid variable forward may offer upfront cash and tax deferral, while still leaving room for some upside.

- An exchange fund may appeal to investors looking for long-term diversification without an immediate tax bill, if they’re comfortable with a multi-year lockup.

What are the biggest tax risks with these strategies?

For collars and prepaid variable forwards, the main risk may come from the IRS constructive sale rule under IRC §1259. If the structure gets too tight, the IRS may view the position as if it were sold, which may trigger immediate capital gains tax.

That’s the line people usually watch: tax deferral may depend on keeping real market exposure. In many cases, that may mean keeping about 15% to 20% of both the upside and downside risk, rather than locking in the position too closely.

For exchange funds, the main drawback is simpler. They may defer taxes, but they do not eliminate them. And if an investor redeems before the seven-year holding period, the result is often punitive.

Can I use these strategies with employer stock or insider shares?

Yes, but employer stock and insider shares may come with major regulatory and compliance hurdles.

Executives, founders, and employees sometimes use collars, prepaid variable forwards, and exchange funds to manage risk while deferring taxes.

That said, these approaches may need to fit within Section 16 insider trading rules, company policies, and a structure that may avoid constructive sale treatment under IRC Section 1259. In many cases, professional guidance may be needed.Disclosures:

- This content is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.

- Tax treatment of investment strategies may vary based on individual circumstances and is subject to change. Consult a qualified tax or legal advisor before making any investment decisions.

- Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.