Paying more for primary care may buy more access, but it may not lower your total healthcare costs. In most cases, concierge medicine adds a membership fee on top of insurance, while Direct Primary Care (DPC) uses a flat monthly fee and skips insurance billing. Tax treatment may differ by model, and that may change the after-tax cost more than many people expect.

Here’s the short version:

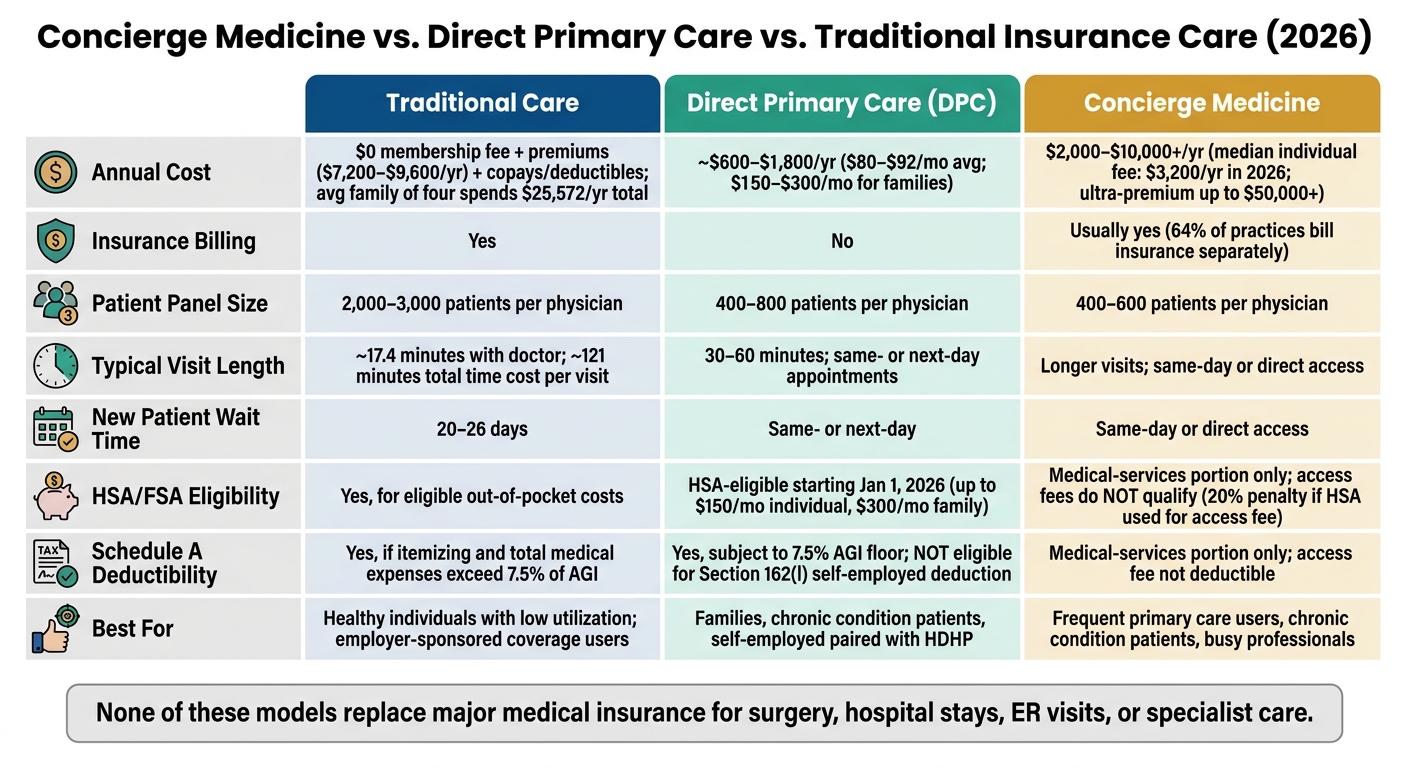

- Concierge medicine may cost about $2,000 to $10,000+ per year and often still bills insurance for visits, labs, or other care.

- DPC may cost about $80 to $92 per month on average and may cover many primary care services with no insurance billing.

- Standard primary care has no membership fee, but you may still pay through premiums, copays, deductibles, and coinsurance.

- Concierge fees may be partly tax-deductible only for the medical-services share, not the access fee.

- DPC fees may be HSA-eligible starting January 1, 2026, up to $150/month for individuals and $300/month for families.

- None of these options replace major medical insurance for surgery, hospital care, ER visits, or specialist care.

If I were comparing these models, I’d look at three things first: total yearly cost, how fast I may reach my doctor, and whether any part of the fee may qualify for HSA, FSA, or Schedule A treatment.

Concierge Medicine vs. DPC vs. Traditional Care: Cost, Access & Tax Guide 2026

Concierge Medicine vs Direct Primary Care – What’s the Difference?

Quick Comparison

| Model | Typical Cost | Insurance Billing | Access | Tax Treatment |

|---|---|---|---|---|

| Standard primary care | No membership fee, plus insurance costs | Yes | Shorter visits, longer waits may be common | Copays/deductibles may count as medical expenses if you itemize and exceed 7.5% of AGI |

| DPC | About $600–$1,800/year | No | Same- or next-day visits, longer visits may be common | May be HSA-eligible up to monthly caps in 2026; may also count on Schedule A |

| Concierge medicine | About $2,000–$10,000+ per year | Usually yes | Direct access, smaller patient panels, longer visits may be common | Only the medical-care portion may qualify; access fees usually may not |

So the core tradeoff is simple: more access usually means a higher fixed cost. The harder part may be figuring out whether that extra fee fits your care needs - and whether the tax rules may soften the cost at all.

1. Concierge Medicine

Cost Structure

Concierge medicine usually adds a membership fee on top of health insurance. In 2026, the median individual fee is $3,200 per year, and fees rose 8.4% from 2025 to 2026.

Most pricing lands in three tiers:

| Tier | Annual Cost | What's Included |

|---|---|---|

| Entry | $2,000–$4,000 | Same-day scheduling, annual physicals, business-hours direct access |

| Premium | $5,000–$10,000 | 24/7 access, house calls, advanced diagnostics |

| Ultra-Premium | $15,000–$50,000+ | Very small panels, house calls, advanced diagnostics |

What are patients paying for here? Mostly access. Smaller patient panels may give each patient more time with the doctor.

There are usually extra costs to plan for too. Onboarding fees may run from $500 to $2,000, and annual price increases may fall in the 3%–7% range. The advertised rate also usually covers one adult, not a household.

Access and Scope

The appeal of concierge medicine may go beyond faster appointments. For many patients, the bigger draw is more time with one doctor and better continuity over time.

The tradeoff is pretty simple: fewer patients per physician, but more physician time per patient. Concierge doctors usually manage 400–600 patients, compared with 2,000–3,000 in standard primary care. That smaller panel may allow longer visits and more direct follow-up.

A large share of practices also use a hybrid setup. About 64% bill insurance for clinical care, while the membership fee covers access and coordination.

Tax Treatment

The tax side may be less generous than the headline fee suggests. Only the medical-services portion of the fee, such as exams, screenings, and labs, may be deductible. The access portion usually is not.

To claim any deduction, you must itemize, and total medical expenses must exceed 7.5% of AGI. Some patients ask the practice for a written fee allocation statement, which may offer a cleaner paper trail for the deductible share.

HSA and FSA funds follow the same basic rule. They may be used only for the medical-services portion of the fee. If HSA or FSA money is used for the access fee, that may trigger taxes and a 20% penalty.

That means the tax treatment may shape the full cost of membership, not just the sticker price.

That tax treatment is only part of the tradeoff; next is how this compares with standard primary care.

Best for Patients With Frequent Primary Care Needs

Concierge medicine may make the most sense for people who use primary care often and want a doctor who knows their history well.

That may include:

- Patients managing chronic conditions such as diabetes or hypertension

- Busy professionals who value same-day or next-day access

- Families with frequent care needs

- Older adults focused on preventive care

For these groups, the model may feel more worthwhile. Still, the value may depend a lot on how often primary care is used.

That profile helps explain who gets value from the model before comparing it with traditional primary care.

2. Traditional Insurance-Based Primary Care

Compared with concierge medicine, traditional primary care shifts costs away from a membership fee and toward insurance-related charges.

Cost Structure

Traditional primary care doesn't come with a membership fee. But patients may still pay through premiums, deductibles, copays, and coinsurance. In 2026, the average insured American family of four spent $25,572 on total healthcare costs, including premiums, deductibles, and copays.

Individual PPO premiums typically range from $7,200 to $9,600 per year, with copays of $20 to $75 per office visit. For 2026, High-Deductible Health Plans (HDHPs) require a minimum annual deductible of $1,700 for individuals or $3,400 for families, with out-of-pocket maximums of $8,500 and $17,000, respectively. Urgent care averages $150 to $300, and an ER visit averages $2,873.

So while the monthly bill may look lower at first glance, the total cost may build over time. A single office visit may feel manageable. A year of premiums, deductibles, and surprise care needs may look very different.

Access and Scope

Traditional primary care usually trades lower fixed cost for bigger patient panels, shorter visits, and longer wait times. Physicians often manage panels of 2,000 to 3,000 patients. Average time with the doctor is 17.4 minutes, and new patients wait 20 to 26 days for an appointment. Once you add travel, paperwork, and waiting room time, the average visit consumes 121 minutes of a patient's day.

That's a big gap: less than 20 minutes with the doctor, but about two hours gone from the day.

After hours, patients are typically routed to a nurse line, urgent care, or the ER, not their own doctor.

Tax Treatment

Out-of-pocket costs like copays and deductibles qualify as medical expenses under IRC Section 213(d). But they may be deductible on Schedule A only if total medical expenses exceed 7.5% of AGI and only if the taxpayer itemizes. With the 2026 standard deduction at $16,100 for single filers and $32,200 for married couples filing jointly, many taxpayers may not clear that bar unless medical spending is fairly high.

Self-employed individuals may have a more favorable option: health insurance premiums may be deducted above the line under Section 162(l), which doesn't require itemizing. For many patients, the tax value may depend more on total annual spending than on the price of any one visit. Tracking out-of-pocket costs during the year may help when those expenses are combined with other qualifying medical costs and may push total spending past the 7.5% threshold.

Best for Patients With Low Healthcare Utilization

Traditional insurance-based care is often a fit for healthy individuals with minimal medical needs, budget-conscious patients for whom an extra $2,000+ per year in membership fees may not make sense, and employees with employer-sponsored coverage that already provides solid access.

If someone sees a doctor once a year for a wellness exam, a concierge membership may be hard to justify. That math may change when primary care use becomes more frequent. Direct Primary Care shifts that tradeoff again.

3. Direct Primary Care

Direct Primary Care (DPC) uses a flat monthly fee and skips insurance billing. It keeps the membership setup, but at a lower price point and with less billing friction. In 2026, the national average is $92 per month, with a median of $80. Family plans often fall in the $150 to $300 per month range, and children may sometimes be added for $20 to $49 per month.

Cost Structure

That monthly fee usually covers unlimited primary care visits, same- or next-day appointments, common labs like CBC, A1C, and lipid panels, minor procedures, and discounted medications. It does not cover specialist care, hospital care, or surgery.

Because of that gap, many patients pair DPC with a High-Deductible Health Plan (HDHP). In that setup, the membership may handle routine care, while the insurance plan may cover larger medical bills.

Access and Scope

DPC physicians typically manage panels of 400 to 800 patients, versus 2,000 to 3,000 in standard primary care. A smaller panel may mean longer visits, often 30 to 60 minutes, along with direct communication by phone, text, or secure messaging. Many practices also offer 24/7 messaging access.

Tax Treatment

Qualifying DPC fees may be paid with HSA funds on a tax-free basis, and DPC no longer blocks HSA contributions. If fees go above the monthly cap, that month may lose HSA contribution eligibility.

DPC fees may also be deducted on Schedule A as medical expenses, subject to the 7.5% AGI floor. There’s one limit worth knowing: DPC fees do not qualify for the self-employed health insurance deduction under Section 162(l) because they are not insurance premiums. So the tax treatment may shape the total cost, not just the monthly fee.

Best for Patients Who Need Frequent Primary Care

DPC may fit families with young children, patients managing chronic conditions like diabetes or hypertension, and self-employed individuals who pair it with an HDHP. For people who want more predictable costs and easier access to primary care without insurance paperwork, it may be a practical route. Those tradeoffs lead into the questions to ask before enrolling.

Pros, Cons, and Tax Questions to Ask Before You Sign Up

After you compare how each model works, the next step may be to look at the actual cost and the tax rules before you enroll. The main tradeoffs usually come down to cost, access, and tax treatment.

| Feature | Traditional Care | Direct Primary Care | Concierge Medicine |

|---|---|---|---|

| Annual Cost | $0 beyond premiums | $600–$1,800 | $1,500–$10,000+ |

| HSA/FSA Eligible | Yes, for eligible out-of-pocket costs | Yes, up to $150/mo for individuals and $300/mo for families | Medical portion only |

| Insurance Billing | Yes | No | Usually yes (hybrid) |

Tax treatment may depend on how the fee is set up. With concierge medicine, only the share tied to actual medical services - exams, labs, and screenings - may qualify as a deductible expense on Schedule A. Even then, that may apply only if your total medical expenses exceed 7.5% of AGI and you itemize. Access fees usually do not qualify as medical expenses.

That’s why it may make sense to ask the practice for a written fee breakdown. If you later claim any deduction, that paperwork may help support it.

Before enrolling, verify a few terms:

- Insurance billing: Confirm whether the practice bills your insurance or Medicare separately in addition to the membership fee - 64% of concierge practices do

- Included services: Check whether basic labs, vaccinations, and minor procedures are included, or whether the fee mainly covers access and time

- Setup fees: Some practices charge $500 to $2,000 at enrollment

- Annual increases: Price escalators typically run 3–7% per year

- Cancellation terms: See whether annual fees are prorated if you leave midyear

Those details may shape the true after-tax cost of membership. It may also help to confirm whether Medicare enrollment applies in your case - new HSA contributions are not allowed after Medicare enrollment, though existing HSA funds may still be used for qualifying services.

Conclusion

The deciding factors may be access, total cost, and tax treatment. Concierge medicine may make the most sense when frequent primary care use appears to justify the fee. Employer-paid arrangements may also improve the tax result.

The main test may not be the sticker price alone, but the after-tax cost of the full plan. Put simply, the better comparison may be the total after-tax cost.

Tax savings may depend on itemizing and getting past the 7.5% AGI floor. For many higher-income patients, the Schedule A deduction may produce little or no tax benefit. A tax professional may confirm how the tax treatment applies in a given case.

It may also make sense to compare the annual fee with retirement saving, emergency cash, and the value of faster access. From there, some people choose the model that best matches how often they use primary care and how much of the fee they may offset through tax rules.

FAQs

Is concierge medicine worth the cost for me?

It depends on how much you may value personal access, your health needs, and your budget. For some people, it may feel worth the cost if they want same-day appointments, longer visits, and direct access to their physician by phone or text.

The tradeoff is pretty simple: you may pay $2,000 to $10,000 per year and still need health insurance. The tax side may be limited too, since fees tied to access or convenience generally aren’t deductible.

Do I still need health insurance with concierge medicine or DPC?

Yes. With both concierge medicine and direct primary care (DPC), you may still need health insurance.

These memberships may improve access to primary care, but they are not health insurance. They generally do not cover major medical events such as hospital stays, surgeries, emergency room visits, or complex specialist care.

Concierge practices may still bill your insurance for visits and services. DPC membership usually covers primary care only.

Which fees can I pay with HSA or FSA funds?

Usually, concierge membership fees may not count as qualified medical expenses under IRS rules. Because of that, they generally may not be paid with HSA or FSA funds.

One possible exception may apply to Direct Primary Care (DPC) starting in 2026. Separately, some services provided inside a concierge practice - like lab work, vaccinations, EKGs, and in-office procedures - may still be HSA/FSA-eligible.

Check with your plan administrator first.

Disclosures:

• This content is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.

• Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.

• Tax treatment of medical expenses and healthcare arrangements may vary based on individual circumstances. Consult a qualified tax professional for personalized advice.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.