Fine wine and whiskey may look like high-return assets, but fees, storage, slow resale, and a 28% federal collectibles tax rate may change the math. If I look past the headline returns, the main takeaway may be simple: gross gains may not match what an investor keeps after costs and taxes.

Here’s the short version:

- Returns may come only from price gains. There’s no income while I hold bottles, cases, or casks.

- Fees may be heavy. Buying, storage, insurance, and selling costs may take a large share of gains.

- Taxes may be harsher than many expect. Long-term gains on investment wine and whiskey may face a 28% federal rate, plus state tax and possibly the 3.8% NIIT.

- Liquidity may be weak. Selling may take weeks or months, not seconds.

- Proof of ownership matters. Records, warehouse documents, and chain of custody may affect resale value and tax reporting.

- Structure changes the outcome. Bottles, casks, and managed programs each come with a different mix of cost, control, and exit friction.

If I had to boil the article down even more, it would be this: these assets may fit only as a small side holding for investors who may accept illiquidity, paperwork, and fee drag.

Quick Comparison

| Asset type | Return source | Main costs | Main risks | Tax treatment |

|---|---|---|---|---|

| Wine bottles / cases | Resale price gain | Buyer's premium, storage, insurance, selling fees | Provenance issues, storage problems, slow resale | May be taxed as a collectible |

| Whiskey bottles | Resale price gain | Purchase markup, storage, insurance, selling fees | Counterfeits, condition issues, thin resale market | May be taxed as a collectible |

| Whiskey casks | Maturation and resale | Warehouse fees, insurance, regauge, transfer, bottling, brokerage | Title risk, weak oversight, low liquidity | May be taxed as a collectible |

| Managed programs / funds | Manager-driven resale gains | Annual fees, exit fees, possible performance fees | Fee drag, lockups, less control | Tax result may depend on structure |

That’s the core picture: return data may look strong on paper, but net results may depend more on fees, storage, title records, and taxes than many buyers first expect.

Fine Wine & Whiskey Investing: Net Returns After Fees, Storage & Taxes

The Pros and Cons of Whisky Investment Explained

Returns and portfolio role: what US investors can realistically expect

The main question isn't correlation. It's whether net returns may justify the risks.

And that's where things get murky. The data set for wine and whiskey is much thinner than it is for stocks or bonds. The Liv-ex Fine Wine 100 started in 2004, so long-run comparisons with equities are hard to make. The CFA Institute has also noted that wine's relative performance may depend a lot on the comparison window, and that as of October 2023, fine wine indices were no longer outperforming financial indices in the cited period. For whiskey, return expectations may be even less certain because the data is thinner still. In practice, that may make the holding structure and the timing of an exit matter more than the headline return numbers.

How returns are generated through price appreciation, not income

Wine and whiskey generate no income. Any return may come only from resale.

For wine bottles, price appreciation may be tied to a few familiar drivers:

- producer reputation

- vintage quality

- critic scores

- scarcity as bottles are consumed over time

For whiskey casks, value may build as the spirit ages and becomes more marketable at higher age statements.

Either way, the holding period may get expensive. An investor may pay for storage, insurance, and platform fees while receiving no income along the way.

Why return dispersion is wider than most investors expect

Headline index numbers may look strong at first glance, but they may hide a very wide range of outcomes. A small group of blue-chip names may drive much of the market, so selection quality may matter more than index averages suggest. Weak provenance may wipe out gains even when the broader market is moving up.

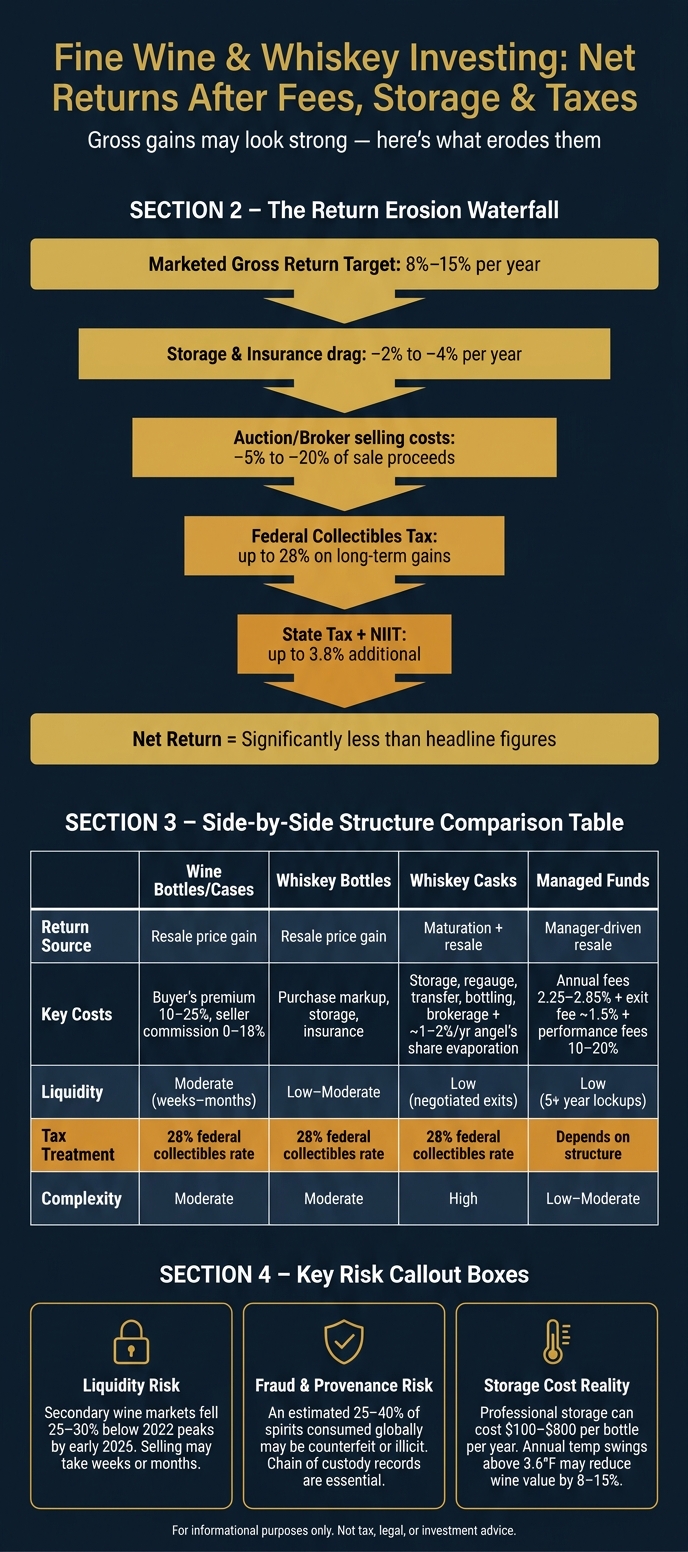

Costs add another layer. Academic research suggests storage and insurance alone may reduce gross real wine returns from about 5.3% to roughly 4.1% per year. Then come selling costs. Auction commissions, shipping, and brokerage spreads may absorb 5% to 20% of sale proceeds. So the gap between a benchmark return and what an individual investor may keep may be large.

Marketing targets often show 8% to 15% annual returns over 5 to 10 years, but those figures are targets, not guarantees.

A more cautious model may start with mid- to high-single-digit gross appreciation, then subtract 2 to 4 percentage points per year for storage, insurance, and fees, plus a haircut at sale. The ownership structure may change those numbers, which is why structure comes next.

Investment structures: bottles, casks, and funds

Once fees and exit costs are clear, the next issue may be simpler to frame: which setup may leave you with more net return after all the friction is counted? Bottles, casks, and managed funds each come with a different mix of control, cost, and day-to-day effort. So structure choice may matter almost as much as the asset itself.

Direct bottle investing in fine wine and collectible whiskey

Buying bottles or full cases may be the most direct way in. You buy investment-grade wine or collectible whiskey, ideally with original cases and clean provenance. People usually source these through specialist merchants, auction houses like Sotheby's and Christie's, or online exchanges.

This is also where costs may start showing up right away. Auction buyer's premiums commonly run 10% to 25% of the hammer price. On the sell side, seller's commissions may range from 0% to 18%, with roughly 6% often cited as a standard rate for larger consignments. In practice, a starting position may be a few thousand dollars per case, and the economics may look better for larger, higher-value lots held over several years.

Whiskey cask investing: ownership, maturation, and exit options

With casks, you're not buying a finished bottle. You're buying spirit that is still maturing. The cask stays in a bonded warehouse, where taxes are deferred until bottling or removal, and you do not take physical possession. Legal ownership may be shown through warehouse records or a delivery order. By contrast, a certificate issued only by an intermediary may offer weak protection if that intermediary fails.

Past that, the main sources of return leakage may come from title, custody, and liquidity, not just maturation. There are a lot of moving parts:

- storage fees

- insurance

- periodic regauges to measure remaining volume

- sampling costs

- transfer charges if the cask moves warehouses

- brokerage or bottling fees at exit

Then there's the angel's share, or evaporation. In Scotch regions, that runs about 1% to 2% of volume per year, and over a 10- to 20-year maturation period, that may add up in a meaningful way.

That may make casks more legally and operationally complex than bottles, even if the sales pitch sometimes sounds simpler. Exit routes may include selling the cask to another investor or trade buyer, bottling the spirit yourself, or selling it back into the trade at trade-level pricing rather than retail. Each route may bring its own costs. If you bottle it yourself, excise duties, labeling rules, and logistics costs may all come into play.

Funds and managed programs: convenience versus fee drag

Managed structures pool investor capital and hand sourcing, storage, and selling over to a manager. That may reduce the operational load. The tradeoff, for some investors, may be fee drag.

Some platform examples charge annual fees of 2.25% to 2.85%, plus an exit fee of around 1.5%. Some also add performance fees of 10% to 20% on top of management fees. Minimums often sit in the $10,000 to $50,000 range, and lockups or suggested holding periods may be five years or more.

More control usually comes with more work and more transaction costs. The table below sums up the main trade-offs across the three structures:

| Structure | Practical minimum | Custody/control | Fees and costs | Operational complexity | Typical holding period |

|---|---|---|---|---|---|

| Bottles / cases | Often a few thousand USD per case | Investor or storage provider; moderate control | Buyer's premium, storage, insurance, seller commission | Moderate | Multi-year; top labels may be more liquid |

| Whiskey casks | Low thousands for entry-level casks; older or more prestigious casks may cost much more | Bonded warehouse controls the physical asset; investor has limited day-to-day control | Storage, insurance, regauge, sampling, transfer, bottling, brokerage | High | Long-term due to maturation and exit friction |

| Funds / managed programs | $10,000–$50,000 | Manager controls sourcing and custody; investor has the least control | Management, performance, custody, storage, and insurance fees | Low to moderate | Usually 5+ years |

Before committing capital, the same three questions tend to come up in every structure: Who controls custody? Where is the asset stored? How is title evidenced? Clear answers up front may reduce the odds of expensive surprises later.

Storage, insurance, provenance, and liquidity

Once you own the asset, storage, provenance, and how you sell may have a big effect on what you actually keep. A strong paper gain on paper may look very different after storage bills, insurance, fees, and a slow sale.

Storage conditions that protect resale value

Resale value may depend a lot on stable storage. Fine wine is generally stored at about 55°F, with relative humidity around 60% to 70%, in the dark and with as little vibration as possible. Annual temperature swings above roughly 3.6°F (2°C) may reduce wine value by 8% to 15%.

Home storage may work only if it's a dedicated, climate-controlled cellar or wine fridge. For investment-grade bottles, bonded storage is often used because it may offer tighter temperature control - around ±0.9°F (0.5°C) - plus warehouse records that may support later resale. Professional storage often costs about $100 to $500 per bottle per year, and premium handling may run as high as $800 per year.

Whiskey bottles are usually tougher than wine, but collectors still care about label condition and fill level. So the same basic rule applies: keep them cool, stable, and out of the light. Whiskey casks are a different case altogether. They must remain in approved bonded warehouses, where storage conditions may affect maturation and warehouse records may support proof of ownership.

Insurance, authentication, and chain of custody

A standard homeowner's policy may not cover a serious collection in a meaningful way. Specialized valuables insurance may cover theft, accidental breakage, fire, flooding, spoilage tied to climate-control failure, and transit risks. Some insurers may also require professional-grade storage before they offer coverage. For casks, the policy may need to state the cask reference number, warehouse location, and ownership interest clearly.

Counterfeit risk tends to climb at the top end of the market. Estimates suggest that 25% to 40% of spirits consumed globally may be counterfeit or illicit. In plain English, paperwork matters. Bottles may need clean provenance. Casks may need warehouse-backed title. A Delivery Order from the warehouse itself - not a broker-issued certificate - is what proves cask ownership.

Records that may matter include:

- Original purchase invoices

- Photos of labels and packaging

- Serial numbers or cask reference numbers

- Warehouse statements

- Condition or appraisal reports

- Records of each transfer, with dates and counterparties

That chain of custody may help buyers, insurers, and tax authorities verify both the asset and its history. The same records may also support cost-basis tracking at tax time.

Liquidity, market mechanics, and the main risks to returns

Even when an asset is well stored and well documented, selling it fast may still be difficult. Auction houses often need weeks or months of lead time. Seller commissions, shipping, and listing fees may cut into proceeds. Brokers may move inventory faster, but they charge margins. Private sales may depend on having the right network and doing careful due diligence. Weak liquidity is one of the main ways gross gains may turn into much smaller realized returns.

By early 2026, many major wine regions were trading 25% to 30% below their 2022 price peaks, which may show how fast secondary-market downturns can compress realized prices. Add exit friction on top of that, and a strong headline return may end up looking far less attractive on a net basis.

The records and exit mechanics covered here feed directly into the tax treatment covered next.

| Risk category | Wine bottles | Whiskey bottles | Whiskey casks |

|---|---|---|---|

| Storage risk | High if home-stored; lower in bonded storage. | Lower than wine; label and fill level still matter. | Must stay in approved bonded warehouse. |

| Provenance / fraud risk | High for rare vintages; provenance required. | High for collectible releases; documentation required. | Title and warehouse-record risk; Delivery Order required. |

| Liquidity | Auction demand exists; fees and lead time reduce proceeds. | Depends on condition, provenance, and buyer demand. | Negotiated exits; slower and less liquid. |

US tax treatment, recordkeeping, and conclusion

Collectibles tax rules, capital gains, and cost basis tracking

Once you sell the asset, the same records that support provenance also shape the tax outcome. After storage costs, fees, and spread, taxes may play a big role in what an investor actually keeps.

Fine wine and whiskey held for investment are generally treated as collectibles for U.S. federal tax purposes. That treatment may subject long-term gains to a maximum 28% federal rate. This rate may apply to gains on assets held for more than one year. Short-term gains are taxed as ordinary income, so holding period tracking may matter quite a bit. State tax and the 3.8% net investment income tax may also apply.

Cost basis generally includes the purchase price plus documented acquisition costs, such as buyer's premiums, commissions, shipping, and import-related fees, when those costs are properly documented. For example, a $5,000 bottle with a $750 buyer's premium and $150 in shipping has a $5,900 basis. Storage and insurance usually reduce net return, but they generally do not increase basis. If buying, selling, and marketing become frequent, the IRS may view the activity as a business, which may change the tax result.

Fine wine and whiskey cannot be held in an IRA, and collectibles are prohibited in certain tax-advantaged retirement accounts. They generally are not eligible for standard IRA or 401(k) treatment.

Records to maintain so taxes and estate planning do not become a weak link

That’s why cost basis and document retention may matter just as much as resale price. Here are the core record categories for tax and estate planning:

| Record Category | Documents to Keep | Why It Matters |

|---|---|---|

| Acquisition | Purchase invoices, buyer's premiums, import/bonded documents | Establishes initial cost basis |

| Carrying Costs | Storage invoices, insurance policies, transport receipts | Supports net return calculations |

| Disposition | Sale confirmations and auction records | Calculates realized gain or loss |

| Estate/Legal | Trust documents, inheritance records, date-of-death valuations | Facilitates stepped-up basis and probate |

A tax review before any sale may be worth the effort if you have multiple acquisition lots, mixed storage locations, insurance claims, import or bonded warehouse transfers, or major appreciation. Holding period drives the tax rate, so sale timing may matter.

For these assets, tax drag may be the last big hurdle after storage and liquidity. Some investors use them only when they may absorb illiquidity and keep clean records. If liquidity needs are high or recordkeeping needs to stay simple, the friction may outweigh the upside.

Mezzi may help you think through how a small allocation like this fits into your broader portfolio by analyzing tax impact, sizing, and account placement across your connected accounts, without taking custody of your assets or executing trades on your behalf.

This section is for informational purposes only and does not constitute tax, legal, or investment advice. Tax rules for collectibles are complex and fact-specific. Consult a qualified tax professional for guidance tailored to your situation.

FAQs

How much can fees cut returns?

Fees may reduce long-term wealth by weighing on investment performance. Depending on the investment, higher fees may also be associated with less consistent returns.

It may also make sense for investors to watch for duplicate fees inside overlapping funds. Regular monitoring, along with automated AI-driven management platforms, may help spot these less visible costs and avoid high assets-under-management fees.

Is bottle or cask investing riskier?

Both come with their own risks.

Like other collectibles, bottle and cask investments may be hard to sell on short notice, and prices may move up or down over time.

Because they’re physical assets, they also tend to involve storage, insurance, and authentication. Those extra steps are meant to protect value and provenance, but they may add costs that reduce overall returns.

What records should I keep for taxes?

Keep detailed records of purchase dates, costs, transaction and exchange history, distribution classifications, and any cost basis adjustments. If you invest through a partnership, keep all K-1 forms.

It also may help to save documentation for property improvements and reconcile your records with forms like 1099-B, 1099-DIV, and 1099-INT. That kind of paper trail may support more accurate tax reporting and may lower audit risk.Disclosures:

- This content is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.

- Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.

- Savings and performance examples are hypothetical and for illustrative purposes only. Actual results will vary based on individual circumstances, portfolio composition, market conditions, and fees.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.