If most of your net worth may sit in your startup, selling a small slice of stock before exit may lower pressure without ending your upside story.

Here’s the short version: founders often look at three main paths for pre-exit liquidity in the U.S. - secondary rounds, tender offers, and structured sales. Each path may change price, timing, taxes, approvals, and how much stock you keep.

A few patterns show up fast:

- Secondary rounds may give founders more say over buyer and timing, but pricing may come at a 10% to 30% discount to the last preferred round, and approvals may take 30 to 60 days

- Tender offers may be cleaner for many shareholders at once, with a sale window of at least 20 business days

- Structured sales may work best when a company wants repeatable liquidity windows instead of one-off deals

- Many investors may view founder sales of 10% to 20% of total holdings as normal, while sales above 20% to 30% may create questions

- QSBS may change the math in a big way: waiting for the five-year hold may affect after-tax proceeds more than a small price change

If I were reducing founder concentration, I’d likely compare cash need, sale size, board process, ROFR/co-sale limits, and tax timing before focusing on headline price alone.

Founder Liquidity Options: Secondary Rounds vs. Tender Offers vs. Structured Sales

How Founders Access Liquidity in Pre-IPO Companies

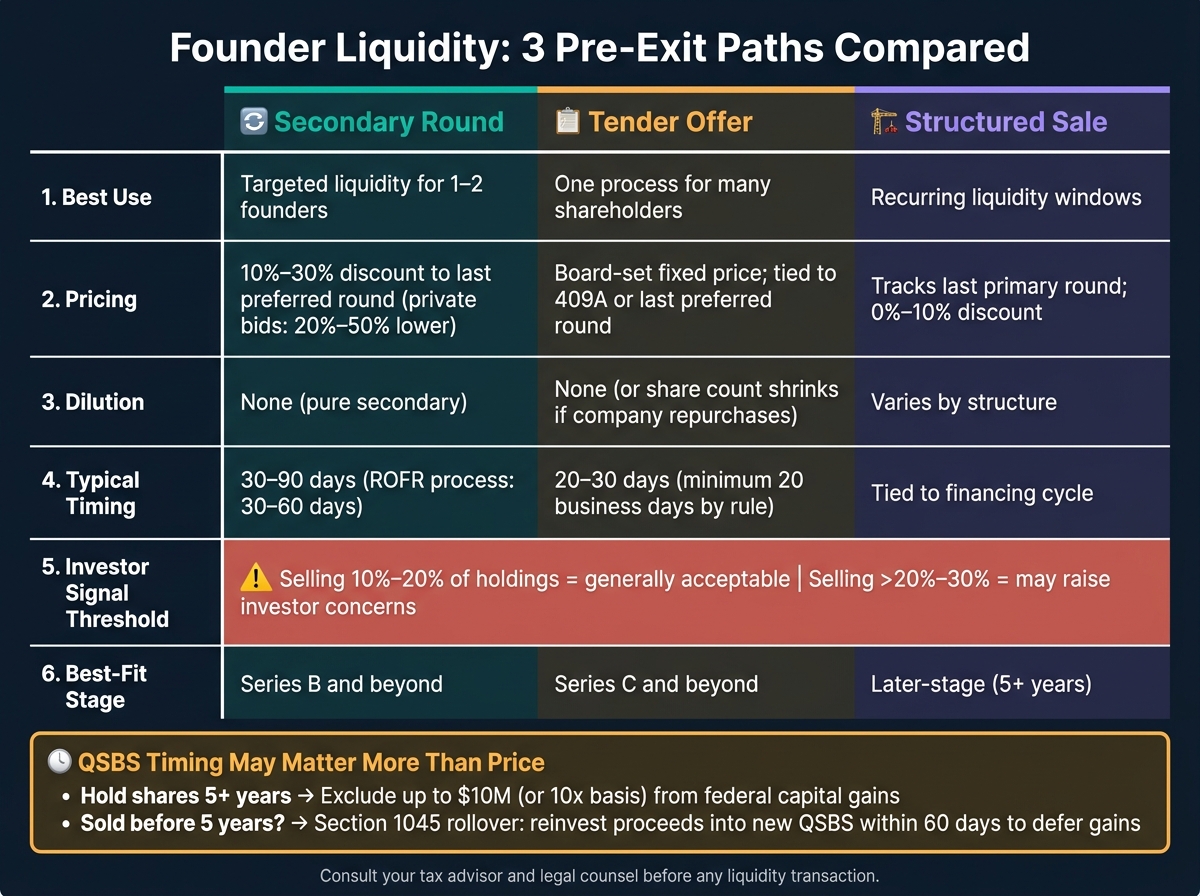

Quick Comparison

| Path | Best use | Pricing | Dilution | Typical timing | Main watchouts |

|---|---|---|---|---|---|

| Secondary Round | One founder or a small group wants targeted liquidity | Often below last preferred round | None on a pure secondary | 30–90 days | ROFR, co-sale rights, pricing discount, signaling |

| Tender Offer | Company wants one process for many holders | Board-set fixed price | Often none unless company buys shares | 20–30 days | Board control, disclosures, tax treatment may vary |

| Structured Sale | Company wants repeat liquidity windows | Often tied to last financing, sometimes with a small discount | May vary | Often tied to financing cycle | Board rules, buyer screening, less price flexibility |

This article breaks down how each option may work, where friction often shows up, and how founders may think about tradeoffs like $500,000 now versus more ownership later.

1. Secondary Rounds

A secondary round lets a founder sell part of their existing shares straight to a buyer, often a current investor or a private secondary buyer. The company doesn’t get the cash. The seller does. That’s the basic tradeoff here: some liquidity now, without issuing new shares, though often at a lower price than the last round.

Pricing & Dilution

That lower price may be the cost of getting liquidity without new dilution. Common stock often trades at a 10% to 30% discount to the latest preferred price. Private secondary bids may come in 20% to 50% lower, and fees may add 5% on each side plus $500 to $5,000 in transfer costs.

Selling common at the same price as preferred may create tax risk. The IRS may view the extra value as compensation taxed at ordinary income rates, not capital gains. It may also make sense to keep the sale price in line with the company’s 409A process so later option grants remain defensible.

Control & Approvals

Most secondary sales run into transfer limits, including ROFR and sometimes co-sale rights. Those terms may slow down a deal or stop it altogether. The ROFR process often takes 30 to 60 days, and co-sale rights may let current investors sell alongside you on the same terms.

It may help to have your own attorney review the transfer limits before lining up a buyer. Company counsel represents the company, not you.

Stage matters too. Earlier-stage sales may get more scrutiny. Later-stage, smaller sales are often read as prudent de-risking. Selling 10% to 20% of total holdings is generally viewed as acceptable, while selling more than 20% to 30% may signal weaker conviction to investors.

Once the approval terms are clear, the next issue may be the tax bill.

Tax Treatment

If the shares have been held for more than one year - or for one year after an 83(b) election - the proceeds may qualify for long-term capital gains.

QSBS under Section 1202 may offer a larger tax break: an exclusion of up to the greater of $10,000,000 or 10x your basis from federal capital gains tax, as long as the shares have been held for at least five years. Waiting until that point may improve after-tax proceeds, which may be worth it if cash needs aren’t urgent.

"If you're a few months away from hitting the five-year QSBS holding period... it may make sense to consider waiting." - Zoe Egelman, Elego

If a sale happens before the five-year mark, a Section 1045 rollover may defer gains by reinvesting the proceeds into new QSBS within 60 days.

Timing & Founder Fit

Secondary rounds may fit best when the goal is targeted liquidity for a small group of founders or executives at Series B and beyond, especially when there’s a clear cash need - like buying a home or catching up after years of below-market pay - while keeping most of the upside in place.

When more shareholders want liquidity on similar terms, tender offers may be the cleaner next step.

2. Tender Offers

A tender offer is a company-run liquidity event. The board sets a fixed price, opens a sale window that stays open for at least 20 business days, and lets eligible shareholders sell a set portion of their shares. Unlike a secondary round, the company manages the whole process from start to finish. For founders, this may be one of the cleanest ways to give many holders liquidity at the same time - possibly reducing personal financial concentration while keeping most equity in place.

Pricing & Dilution

The board sets one standardized, take-it-or-leave-it price for everyone who joins. That price is usually informed by the latest 409A valuation or the last preferred financing round. In many cases, the board sets the price below the latest preferred round to reflect the lack of liquidation preferences and to lower tax risk.

No new shares are issued, so there may be no dilution. If the company repurchases shares, the share count shrinks. If a third party buys them, ownership simply shifts from one holder to another. One tradeoff: a high tender price may push up the 409A valuation and may lead to higher future option strike prices.

Control & Approvals

The company controls the process: price, eligibility, timing, and volume caps. Founders are often expected to sell only 10% to 20% of their holdings in a single event so they may stay aligned with investors. The board must formally approve the process and waive transfer restrictions, and lead investors may need to approve it too.

ROFR is usually waived, which may remove a major friction point that often shows up in one-off secondary sales. Stripe and OpenAI used tender offers in 2024 to let employees cash out without an IPO.

After process comes the next question: how the sale may be taxed.

Tax Treatment

The tax result depends on how the deal is structured. If a third-party investor buys the shares, the sale is generally treated as a capital transaction. If the company repurchases the shares, the deal may be treated as a dividend under §301 unless it meets the "substantially disproportionate" test under §302, meaning your ownership percentage drops in a meaningful way after the sale.

QSBS may still apply, but a sale before the five-year mark may forfeit the exclusion. There's also a state tax wrinkle. States like California, Pennsylvania, and New Jersey do not conform to federal QSBS rules and may tax the full gain.

Timing & Founder Fit

Tender offers tend to fit best at Series C and later, when a company may have a broad shareholder base - founders, early employees, and former team members - who may face similar liquidity pressure. They may be a good fit for founders with long-held, concentrated equity who want liquidity for a major life event without waiting for an IPO.

When price or timing needs are less standardized, structured sales may offer more flexibility.

3. Structured Sales

When liquidity requests start showing up again and again, a structured sale program may make more sense than handling each request as a one-off. Instead of treating every sale like a special case, the company sets up a standing process.

A structured sale program is a board-approved setup for recurring founder and employee liquidity windows. It lays out the rules in advance - who may sell, how much, to whom, and when. That may replace ad hoc back-and-forth with a repeatable framework that keeps the cap table more orderly and may reduce the chance of unsanctioned share transfers.

Pricing & Dilution

Pricing usually tracks the latest primary round or comes in at a small discount, often 0%–10%. One pricing risk to watch: if common stock is sold at the same price as preferred stock without a typical discount, the IRS may recharacterize the excess value as ordinary compensatory income.

Keeping a defensible discount in place may reduce that risk. The tradeoff here may be less about squeezing out the top price and more about keeping the process under control.

Control & Approvals

Founders typically may sell 10%–20% of their total holdings per window. Selling more than 20% in a single transaction is often viewed as a red flag by investors.

One practical upside versus uncoordinated secondary trades is buyer screening. The board may review buyers before shares change hands, which may keep competitors or other problematic parties off the cap table.

Tax Treatment

Tax treatment depends on how the sale is structured. Third-party sales are usually treated as capital gains, while company repurchases may trigger §302 dividend treatment if the ownership drop is not substantial. State QSBS nonconformity remains a risk.

That means structure may matter just as much as price when a company or founder weighs whether this type of program fits a given liquidity goal.

Timing & Founder Fit

Structured programs tend to fit later-stage companies best, especially when liquidity requests are recurring and the company wants a repeatable process. They may also fit founders who have been building for five or more years and want a steadier way to manage personal financial concentration without creating negative signaling.

In that setting, structured liquidity may make it easier for founders to stay focused on long-term execution.

Pros, Cons, and Best-Fit Scenarios for Each Liquidity Path

This table may help match each path to your cash need, control tolerance, and tax position - while limiting how much future upside you give up.

The table below shows where each path may work well and where it may start to break down.

| Liquidity Path | Strengths | Drawbacks | Best-Fit Founder Profile |

|---|---|---|---|

| Secondary Round | Negotiated pricing; low operational burden on the company; may be tied cleanly to a primary raise | May require investor approval; ROFR may delay closing by 30–60 days; signaling risk if the sale is too large | Founders seeking roughly $250,000 to $2,000,000 during a strong primary financing round, with the sale kept modest relative to their total holdings |

| Tender Offer | Board-controlled process; standardized terms; clearer optics and more even treatment across holders | May be expensive and operationally demanding to execute; may require formal disclosure and coordination | Late-stage founders at Series C and beyond who need to provide liquidity for themselves and a broad employee base at the same time |

| Structured Sale | Pre-approved framework may reduce one-off negotiation; board-defined cadence; repeatable and predictable | May offer less pricing flexibility; may require an established process | Later-stage founders who want recurring liquidity windows and predictable timing |

Size may matter as much as structure. Investors may read a large sale as a signal. Selling more than 20% of your total holdings in a single transaction is often viewed as a red flag.

Before moving forward, it may make sense to review a few points with your counsel, lead investors, and tax advisor:

- [ ] Do current bylaws or investor rights agreements require board approval, and are there active lock-up periods?

- [ ] Does this sale trigger co-sale or tag-along rights?

- [ ] Is there a minimum primary capital threshold before a secondary allocation is permitted?

- [ ] Will this be treated as a capital sale taxed as capital gains or a Section 302 redemption?

- [ ] Does the sale still qualify for QSBS?

If QSBS applies, timing may matter more than price. Selling before year five may forfeit the exclusion; a Section 1045 rollover gives you a 60-day window to reinvest proceeds into a new qualified small business and defer the gain.

Conclusion

Each liquidity path may fit a different situation. Secondary rounds may suit targeted, financing-linked liquidity. Tender offers may suit board-run liquidity for many holders at once. Structured sales may suit later-stage companies that want repeatable windows.

Once the mechanics are clear, the decision may become personal. The choice often comes down to cash needs, net worth concentration, confidence in future upside, tax posture, and investor alignment.

Some shareholders may model after-tax proceeds, remaining exposure, and their QSBS timeline before agreeing to a sale.

That kind of analysis may work better when you can see the impact across your full financial picture. Mezzi is designed to help model after-tax proceeds, remaining equity concentration, and scenario tradeoffs across your full balance sheet.

The goal may not be to cash out. It may be to reduce pressure, buy focus, and preserve enough upside for the eventual exit.

FAQs

How do I choose between a secondary, tender offer, and structured sale?

Choose based on your company’s size, your liquidity goals, and how much control your board may want.

- Secondary: more personal control and timing flexibility, but it may be messier and may be subject to ROFR.

- Tender offer: a cleaner, company-run process, but pricing and timing may be set by the company.

- Structured sale: the most formal and recurring option, often used by larger companies through board-approved windows.

Also confirm transfer restrictions, tax impact, and board and investor support.

How much founder stock is usually safe to sell before it raises concerns?

There’s no hard limit here, but a common rule of thumb suggests that selling 10% to 20% of your holdings in a single transaction may be viewed as acceptable. Selling 5% to 10% is usually seen as noncontroversial.

At 15% to 20%, a sale may be viewed as acceptable from Series B onward if the company is doing well. Selling a much larger share, such as 40%, may raise serious concerns about founder alignment and long-term incentive.

Should I wait for QSBS eligibility before selling shares?

Yes - waiting may be worth strong consideration. QSBS may let some shareholders exclude up to the greater of $10 million or 10 times their basis from federal capital gains tax, but that treatment generally depends on a five-year holding period.

If you sell before that five-year mark, you may give up that tax break. It may make sense to confirm your specific QSBS holding period with tax counsel before selling any equity.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.