Hiring full-time house staff may cost far more than the paycheck alone. In many cases, total annual cost may run 25% to 55% above base wages, once payroll taxes, overtime, insurance, benefits, and admin costs are added.

Here’s the short version:

- A quoted wage may be only 65% to 80% of total cost

- Employer payroll taxes may add about 8% to 11%

- Overtime may apply after 40 hours in a week for many household workers

- Workers’ comp, payroll service fees, and paid time off may add more

- A staffing agency fee may add 10% to 20% in year one

- Tax breaks like the Child and Dependent Care Tax Credit and a Dependent Care FSA may lower net cost for some families

- Misclassifying a worker as a contractor may lead to back taxes, penalties, and interest

If I were sizing up the budget, I’d treat the hourly rate as the starting point, not the final number. A simple rule of thumb from the piece: total cost may land around 1.25x to 1.55x base pay, with first-year hiring fees added separately.

A few numbers from the article make that gap easy to see:

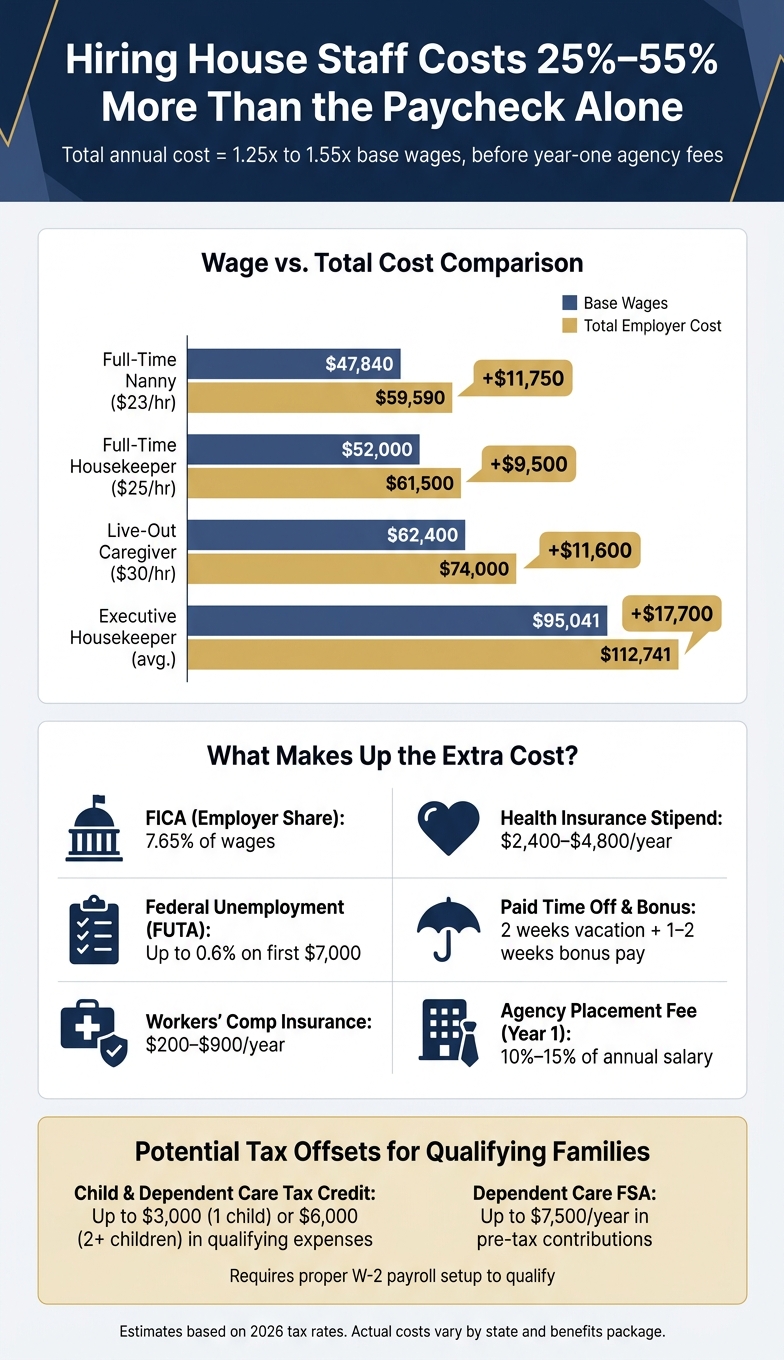

- A full-time nanny at $23/hour may cost about $59,590 per year

- A full-time housekeeper at $25/hour may cost about $61,500

- A live-out caregiver at $30/hour may cost about $74,000

- An executive housekeeper with $95,041 in wages may cost about $112,741

Most of the extra cost may come from a short list:

- FICA: 7.65% employer share

- FUTA: up to 0.6% on the first $7,000 of wages, if state rules are met

- State unemployment tax: varies by state

- Workers’ comp: about $200 to $900 per year in many cases

- Health stipend: about $2,400 to $4,800 per year

- Bonus and paid leave: often added on top of wages

There’s also a tax side. If payroll is handled the legal way, some households may qualify for:

- the Child and Dependent Care Tax Credit

- a Dependent Care FSA

- wage reporting through Form W-2 and taxes through Schedule H

If payroll is handled off the books, those tax breaks may not be available.

True Cost of Full-Time House Staff: Wages vs. Total Annual Cost

Schedule H: Household Employment Taxes | Block Advisors by H&R Block

Quick comparison

| Role | Base Wages | Est. Total Annual Cost |

|---|---|---|

| Full-Time Nanny | $47,840 | $59,590 |

| Full-Time Housekeeper | $52,000 | $61,500 |

| Live-Out Caregiver | $62,400 | $74,000 |

| Executive Housekeeper | $95,041 | $112,741 |

So the main takeaway is simple: if I only budgeted for wages, I might miss taxes, overtime, insurance, paperwork, and year-one hiring costs. This piece lays out those moving parts in plain terms, along with the tax offsets that may apply in some cases.

1. Build a realistic compensation budget

Wages, hours, and overtime rules that affect your total

Start with gross wages and overtime. Most household employees - nannies, housekeepers, caregivers - may be treated as non-exempt under the Fair Labor Standards Act. That usually means hours above 40 in a single workweek may need to be paid at 1.5 times the regular hourly rate.

Hours often shape cost just as much as the base rate. A nanny working 45 hours a week may cost 18.75% more than one working 40, because 5 of those hours are paid at time-and-a-half. Across a full year, that gap may add up fast.

Federal law generally exempts live-in domestic workers from overtime, but state law may override that rule. California, New York, New Jersey, Hawaii, and Maryland all require overtime pay for live-in staff, so a live-in setup may not reduce overtime costs in those states.

Many families also guarantee 40 hours a week, even during vacations or lighter weeks.

Benefits and extra compensation that add to the cost

Base pay is only part of the picture. Common benefits may include:

- 2 weeks of paid vacation

- 5–7 sick days

- 6–10 paid holidays

- A health insurance stipend of $200–$400 per month, or $2,400–$4,800 per year

- A year-end bonus equal to 1 to 2 weeks' pay

If your employee drives for work, mileage reimbursement may add another line item. Using the IRS rate of $0.725 per mile, that may come to about $1,200–$2,400 per year based on 10 miles per day. Some families also budget for annual raises of 3%–5% to keep pay in line with the market and potentially reduce turnover.

After compensation, it makes sense to add hiring and payroll costs to estimate the full employer budget.

Agency fees and administrative costs

Hiring costs usually fall into two buckets: one-time placement expenses and recurring annual costs.

On the one-time side, a domestic staffing agency may charge a placement fee of 10%–15% of the employee's annual salary. For a housekeeper earning $77,913 - the average for high-net-worth households - that works out to about $7,800 to $11,700 upfront. Some luxury agencies also charge a flat search initiation fee of around $750 on top of the percentage-based fee. If you handle background checks on your own, those usually run $100 to $300.

Recurring costs may look smaller, but they still stack up over time. Payroll services range from about $100 per year for budget self-service tools to $900 per year for full-service providers that handle tax filing on your behalf. Time-tracking apps for household staff cost about $10 per year.

| Cost Type | Item | Estimated Cost |

|---|---|---|

| One-time | Agency placement fee | 10%–15% of annual salary |

| One-time | Background check (DIY) | $100–$300 |

| One-time | Agency initiation fee (luxury) | ~$750 |

| Recurring | Payroll service | $100–$900/year |

| Recurring | Health insurance stipend | $2,400–$4,800/year |

| Recurring | Mileage reimbursement | $1,200–$2,400/year |

| Recurring | Contingency coverage | $25–$40/hour as needed |

These compensation costs may be only the first layer of the employer burden. Next comes payroll taxes, unemployment insurance, and workers' compensation.

2. Employer taxes, insurance, and compliance costs

Payroll taxes household employers owe

Taxes, insurance, and filings may add the next fixed layer of cost.

In 2026, if you pay one household employee $3,000 or more in cash wages, you may owe the employer share of FICA: 6.2% for Social Security and 1.45% for Medicare. You also withhold the employee share. The Social Security tax stops at $184,500 in wages.

Federal unemployment tax, or FUTA, may apply once you pay $1,000 or more to all household employees combined in any calendar quarter. The effective FUTA rate may be 0.6% on the first $7,000 of wages per employee, assuming state unemployment taxes are paid on time. State unemployment tax rates and wage bases vary a lot by state, so the total may depend on where you live.

Employer-side taxes may add about 8% to 11% to base wages, depending on location. Some households cover that tax bill by increasing withholding on a main job's W-4 instead of making separate estimated payments.

Taxes are only the first required layer. Insurance and state filings may add more.

Workers' compensation and state requirements

Workers' compensation may be required for household employers in about half of states, including California, New York, Illinois, Maryland, Massachusetts, and Washington. If an employee gets hurt on the job in one of those states and you don't have coverage, you may be personally responsible for medical bills, lost wages, and state penalties.

Annual premiums may run $200 to $900, depending on the state, wage level, and job duties. In states where coverage isn't required, some households still add a rider to a homeowner's insurance policy, which may cost less than a standalone policy.

After taxes and insurance, paperwork may become the last recurring burden.

Records and forms a household employer needs to manage

Missing forms and deadlines may turn household payroll into a penalty issue. Household employers may need an EIN, Form I-9, payroll records, and annual tax filings. On or before an employee's first day, complete Form I-9 to verify work eligibility and keep it on file for at least three years. Errors on Form I-9 may lead to fines ranging from $288 to $2,861 per form.

You issue Form W-2 to your employee and file Copy A with the Social Security Administration by January 31. Household employment taxes - FICA, FUTA, and any withheld income taxes - are reported by attaching Schedule H to your personal Form 1040, due April 15. Missing that filing may get expensive: the penalty may be 5% of unpaid taxes per month, up to 25%, with a minimum penalty of $525 or 100% of the unpaid tax, whichever is less, for returns more than 60 days late.

Keep all pay records, tax forms, and proof of payments for at least four years. Most states also require state unemployment registration and new-hire reporting within 20 days.

3. Tax breaks that can lower your net cost

After wages, taxes, and insurance, two tax tools may lower your net cost: the Child and Dependent Care Tax Credit and a Dependent Care FSA.

Child and Dependent Care Tax Credit

If you hire a nanny or caregiver so you can work or look for work, those wages may qualify for the Child and Dependent Care Tax Credit (CDCTC). The care must be for a child under 13, or for a spouse or dependent who cannot care for themself and lives with you for more than half the year.

In 2026, the credit may cover 20% to 50% of qualifying expenses, depending on your adjusted gross income. The expense cap is $3,000 for one qualifying dependent or $6,000 for two or more. That means the maximum credit may be $1,500 for one qualifying dependent or $3,000 for two or more at the top rate, and as low as $600 at the minimum rate. Employer payroll taxes may also count toward those expenses.

The CDCTC is non-refundable, so it may reduce your tax bill to $0, but it won't create a refund if the credit is larger than the amount you owe.

How a dependent care FSA can reduce out-of-pocket costs

A Dependent Care FSA (DCFSA) lets you pay for nanny or caregiver wages with pre-tax dollars through your employer's benefits plan. For 2026, the federal limit is $7,500 per household for couples filing jointly, though your employer's plan may still cap contributions at $5,000.

If you're in the 24% federal tax bracket, maxing out a $7,500 DCFSA may save roughly $1,800 in federal income tax alone. But there's a catch: FSA dollars and CDCTC dollars can't be used on the same expenses. Every dollar run through the FSA reduces the expense base available for the credit, dollar for dollar.

That means some households may use the FSA first, then apply the credit to any remaining eligible expenses up to the limit. For a family with one child, a $7,500 FSA contribution uses up the CDCTC's $3,000 expense cap. For families with two or more children, a $5,000 FSA still leaves $1,000 of expenses that may qualify for the credit.

Why proper payroll setup protects your tax benefits

Neither the FSA nor the CDCTC is available if you pay your household employee outside payroll. To claim either benefit, the worker must be treated as a household employee, not an independent contractor, and you need to report wages on a W-2.

The IRS uses Form 2441 with your annual return to verify the care provider's name, address, and Social Security Number against those wage records. FSA reimbursements also require pay records showing wages and withholdings. Cash apps and informal transfers do not qualify.

Legal payroll isn't just paperwork. It may determine whether your household can claim these benefits at all, and it may make the net cost of household employment look lower than it first appears. Mezzi helps you weigh these tax breaks against your broader plan, but a tax professional should handle situation-specific filing questions. Next, compare those tax offsets with real annual cost scenarios.

4. Cost scenarios and a planning framework for Mezzi readers

Hypothetical annual cost examples for common household roles

Once taxes, insurance, and benefits are added, the quoted wage may no longer reflect the full annual cost. Quoted pay may be only part of the picture.

The same pattern may apply to other full-time household roles. A full-time housekeeper at $25/hour may cost about $61,500 all-in. A live-out caregiver at $30/hour may cost about $74,000. And an executive housekeeper averaging $95,041 in gross wages may cost about $112,741 per year.

Quoted pay versus fully loaded cost: a comparison table

The examples below may help translate hourly pay into a full-year employer cost. These are hypothetical estimates based on 2026 tax rates and typical market benefits. Actual costs may vary by state, hours worked, and the benefits package offered.

| Role | Annual Gross Wages | Est. Employer Taxes (FICA/FUTA/SUTA) | Insurance & Admin | Benefits (PTO/Health) | Total Annual Cost |

|---|---|---|---|---|---|

| Full-Time Nanny | $47,840 ($23/hr) | $4,210 | $1,180 | $6,360 | $59,590 |

| Full-Time Housekeeper | $52,000 ($25/hr) | $4,500 | $1,000 | $4,000 | $61,500 |

| Live-Out Caregiver | $62,400 ($30/hr) | $5,400 | $1,200 | $5,000 | $74,000 |

| Executive Housekeeper | $95,041 (avg.) | $8,200 | $1,500 | $8,000 | $112,741 |

Note: Year 1 costs may rise further if you pay a placement fee.

Using Mezzi to check if household staff costs fit your financial plan

A recurring annual expense of $60,000 to $113,000 may affect more than one line in a budget. It may also be associated with cash flow, investment contributions, and retirement timing.

Conclusion: Budget for the full cost, not just the paycheck

The examples above point to a simple reality: hiring full-time household staff may involve a large recurring cost. And the paycheck may be only part of it.

Once employer payroll taxes, workers' compensation, benefits, overtime, and admin costs are added in, the fully loaded annual cost may run 25% to 55% above the base wage.

That may matter for two reasons.

- Correct payroll may be required if a household wants to claim tax breaks like the Dependent Care FSA and the Child and Dependent Care Tax Credit.

- It may also reduce the chance of retroactive liabilities, which may run above $15,000 to $20,000 in back taxes, penalties, and interest.

So when you map out the cost, it may make sense to start with the full picture, not just the quoted wage. A common starting point may be a 1.25x to 1.55x multiplier on quoted wages, with overtime and any first-year agency fees added on top.

Mezzi may show how that expense fits into your broader financial plan.

FAQs

What costs are easiest to overlook when hiring full-time house staff?

The easiest costs to miss may be payroll taxes, insurance premiums, and admin expenses. Together, those items may push a base salary budget up by 25% to 55%.

Families also often miss a few other line items, such as:

- Overtime pay

- Payroll service costs

- Time spent managing household logistics

- Placement agency fees, if those apply

On paper, a salary may look straightforward. In practice, the total cost may end up higher once those extra pieces are added in.

How do I know if a household worker is an employee or a contractor?

For IRS purposes, household workers are almost always employees, not independent contractors. The main test comes down to control: if you direct what work is done, and when, where, and how it gets done, the worker may be treated as your employee.

Job titles and written agreements usually don't change that. Independent contractors often bring their own tools, set their own methods, and work for more than one client. If a worker is misclassified, that may lead to tax penalties and legal exposure.

Which tax breaks can lower the cost of legal household payroll?

Legal household employment may be more affordable than it first appears because two federal tax breaks may help: the Dependent Care FSA and the Child and Dependent Care Tax Credit.

A Dependent Care FSA lets you set aside up to $7,500 in pre-tax pay for care costs. The Child and Dependent Care Tax Credit lets you claim a percentage of eligible expenses, up to $3,000 for one child or $6,000 for two or more.

There’s one catch: you may not use both for the same expense.

Disclosures:

• This content is for informational purposes only and does not constitute investment, tax, or legal advice. Readers should consult a qualified professional regarding their specific situation.

• Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.

• Savings and cost examples are hypothetical and for illustrative purposes only. Actual results will vary based on individual circumstances, state law, and service providers.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.