Switching brokerages can help organize your finances or change your cost structure, but the process involves more than just moving your account. Here’s what you need to know:

- Assets Transfer Process: Most investments, like stocks, ETFs, and mutual funds, move through ACATS (Automated Customer Account Transfer Service) in 3–6 business days. However, some assets, like proprietary mutual funds or fractional shares, may need to be sold, creating potential tax events.

- Account Freeze: During the transfer, your account is frozen, meaning you can’t trade or withdraw funds, leaving you exposed to market risks.

- Fees and Costs: Many brokerages charge outgoing transfer fees ($50–$100), though some receiving firms may reimburse these costs for large transfers.

- Tax Concerns: Lost or misreported cost basis data can lead to IRS issues. Liquidated assets may trigger taxable gains or losses. Wash sale rules can further complicate tax reporting.

- Avoid Mistakes: Ensure all forms are accurate, download your records before transferring, and disable dividend reinvestment plans to prevent issues.

Problems You May Face When Switching Brokerages

Switching brokerages isn’t always a smooth process. Even if you follow all the steps, unexpected hurdles can arise, potentially disrupting your portfolio and adding unforeseen expenses. Let’s break down some of the most common challenges and how they might impact your investments.

Account Freezes and Transfer Delays

One of the biggest headaches during a transfer is dealing with incorrect or incomplete paperwork. The Transfer Instruction Form must match your old brokerage’s records perfectly. Even small differences - like including a middle initial where it wasn’t used before - can cause the transfer to be rejected automatically[ [8]]. Once a problem is flagged, your old brokerage has one to three business days to review and validate the request.

"If the old firm takes no action on the request or a problem is not resolved within two business days, the transfer request is purged (or deleted) from ACATS." - Investor.gov

Another potential snag comes from unsettled trades. If you’ve recently bought stocks or options, the transfer will be delayed until those transactions settle - usually two business days for stocks and one for options. Additionally, features like dividend reinvestment plans, recurring deposits, or automated portfolio rebalancing can interfere with the transfer process. Any leftover cash from dividends or interest payments will often be swept into your account separately, but this can take up to 10 business days, leaving that money temporarily out of reach.

Transfer Fees and Associated Costs

Switching brokerages can also come with a financial hit. Many firms charge an outgoing transfer fee, which typically ranges from $50 to $100, depending on the brokerage[ [8]]. This fee is deducted directly from your account balance, which may reduce your overall account value. However, some receiving brokers may reimburse these fees if you transfer a large enough balance. For example, Robinhood offers reimbursements of up to $75 for transfers exceeding $7,500.

Another issue is the inability to trade during the transfer period, which usually lasts three to six business days. This leaves you exposed to market risks, as you won’t be able to react to sudden price changes or take advantage of opportunities during that time.

Tax Complications and Reporting Issues

Taxes can add another layer of complexity to the transfer process. Certain assets, such as fractional shares or proprietary mutual funds, cannot be transferred through ACATS. These assets are automatically liquidated, which could result in an unexpected taxable event.

Cost basis data - the original purchase price of your investments - can also get lost or misreported during the transfer. If your new brokerage reports a $0 cost basis to the IRS, you could be taxed on the entire sale price instead of just your actual gains.

"A misunderstanding of transfer rules could lead to billions in unnecessary, self-inflicted tax payments across the market." - TaxSharkInc

Wash sales further complicate matters. If you repurchase the same security within 61 days, the loss may not be deductible, and any adjustments from the old brokerage will carry over to the new one. Keeping detailed records is essential to avoid surprise tax bills.

How ACATS Transfers Work

ACATS Brokerage Transfer Process Timeline and Steps

ACATS is an electronic system designed to streamline most U.S. brokerage transfers. Created by the National Securities Clearing Corporation and managed by the Depository Trust & Clearing Corporation, it standardizes how investments are moved between firms. Knowing how ACATS works can help you plan a smooth, tax-efficient transfer and set realistic expectations for the process.

Here’s a closer look at how assets are securely transferred between brokerages.

The ACATS Transfer Process Step by Step

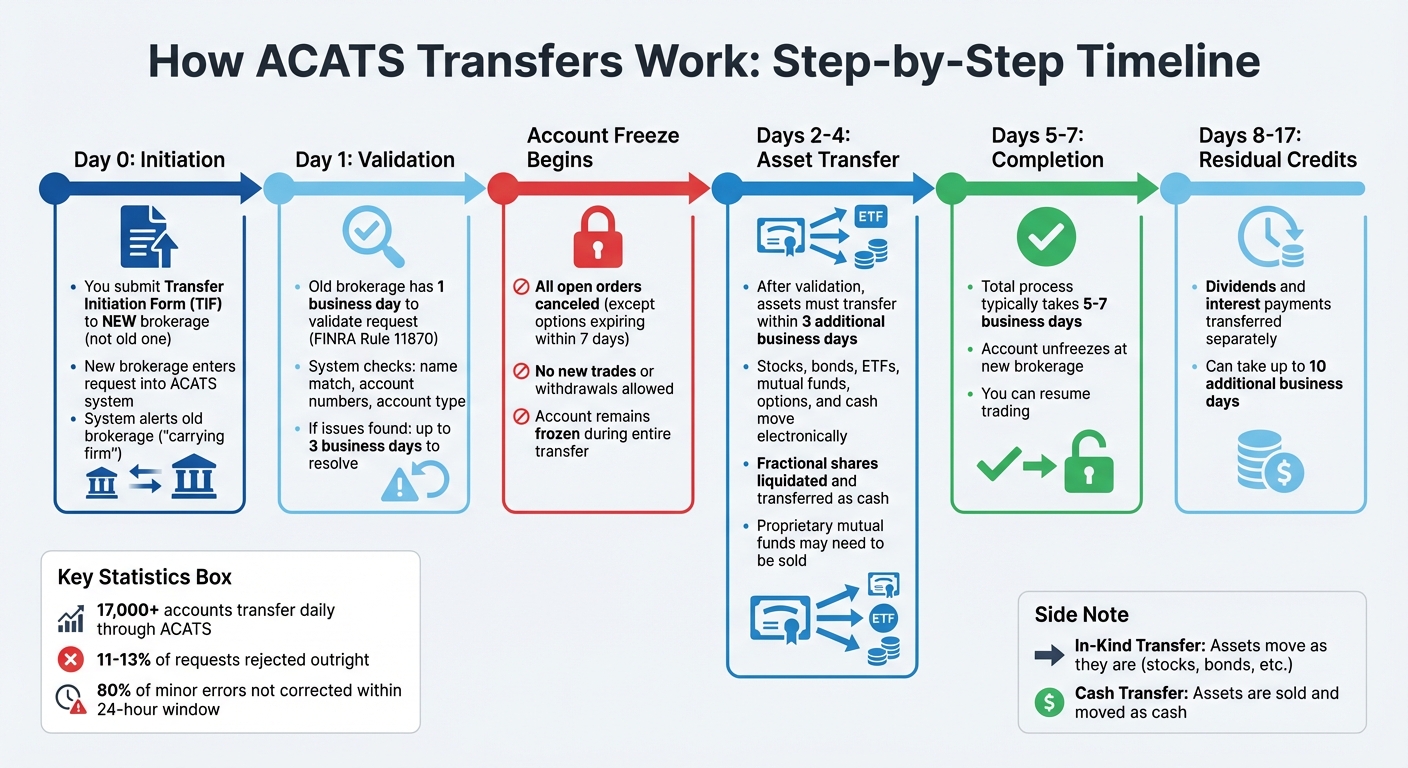

The process starts when you submit a Transfer Initiation Form (TIF) to your new brokerage - not your current one. The new firm enters the request into the ACATS system, which alerts your old brokerage (referred to as the "carrying firm"). Under FINRA Rule 11870, the old brokerage has one business day to validate the request. If there are issues, like mismatched names or incorrect account numbers, they have up to three business days to resolve them.

Once the request is validated, the old brokerage freezes your account, canceling all open orders except for options expiring within seven days. This freeze ensures no new trades or changes disrupt the transfer. After validation, the actual transfer of assets must be completed within three additional business days. Overall, the process typically takes five to seven business days.

"The fast and efficient transfer of customer accounts is of critical importance to both the industry and investors." - FINRA

Despite its efficiency, ACATS isn't flawless. Over 17,000 accounts transfer through the system daily, yet about 11% to 13% of requests are rejected outright. Additionally, nearly 80% of minor errors aren't corrected within the 24-hour window, causing the process to restart. To improve speed, the industry removed the settlement preparation stage as of October 17, 2025.

In-Kind Transfers vs. Cash Transfers

An in-kind transfer moves your investments exactly as they are - for instance, 50 shares of Apple stock will remain 50 shares of Apple stock in your new account. This method avoids selling your holdings, so you won’t trigger capital gains taxes. Plus, your cost basis (the original purchase price) transfers along with the assets, keeping your tax records intact.

A cash transfer works differently. Your old brokerage sells your holdings, transfers the cash to your new account, and you’ll need to repurchase the investments manually. This process creates taxable events on any gains, which can lead to unexpected tax bills. If you plan to repurchase similar assets immediately, be careful to avoid wash sales that could disallow your losses. Cash transfers are generally used only when ACATS isn’t available, such as when transferring funds from a bank or credit union that doesn’t participate in the system.

"An in-kind or ACAT transfer allows you to transfer your investments between brokers as is, meaning you don't have to sell investments and transfer the cash proceeds." - NerdWallet

Understanding these transfer types helps you determine the best approach for your assets.

Which Assets Can and Cannot Transfer

ACATS handles most common investments seamlessly, including stocks, bonds, ETFs, mutual funds, options, and cash. However, some assets face limitations. For example, proprietary mutual funds - those managed exclusively by your old brokerage - cannot transfer if your new firm doesn’t offer them. Similarly, fractional shares are liquidated and transferred as cash, which creates a small taxable event even during an in-kind transfer.

Certain assets, like annuities, are entirely excluded from ACATS since they are insurance products, not securities. These require separate processes, such as a 1035 exchange or a manual agent-of-record change. Other exceptions include bankrupt securities without a transfer agent and some foreign securities. Options positions expiring within seven business days are also excluded to prevent complications during the account freeze.

Any residual credits - such as dividends or interest - are transferred to the new account in a follow-up process that can take up to 10 business days.

How to Avoid Common Transfer Mistakes

While ACATS simplifies the asset transfer process, even small errors can cause frustrating delays. Fortunately, most issues can be avoided by taking the right steps before and during your transfer.

Review All Forms Carefully

Double-check that the information on your Transfer Instruction Form (TIF) matches your current brokerage records exactly. Details like your name, Social Security number, and account type must align perfectly with what's on file. Even minor discrepancies can result in a rejection.

"A missing middle initial or a slight name variation is the #1 reason for transfer rejections." - TaxSharkInc

For example, a mismatch such as "James T. Smith" versus "Jim Smith" could derail your transfer. Account types must also match: a Traditional IRA must transfer to another Traditional IRA, and an individual taxable account must move to a similar account type. Before submitting the form, download your historical statements and cost basis data from your current broker. This information will be key for accurate tax reporting.

Additionally, close any open limit orders and cancel pending trades before initiating the transfer. Once the process is complete, compare your first statement from the new brokerage with your final statement from the old one. Verify that all shares, cost basis data, and acquisition dates transferred correctly.

Finally, ensure you're aware of any tax consequences before proceeding with the transfer.

Watch Out for Wash Sales

Wash sales can complicate things during a transfer, especially if assets are liquidated rather than transferred in-kind. A wash sale happens when you sell a security at a loss and repurchase the same or a similar security within 61 days.

This rule applies across all your accounts. For instance, selling a stock at a loss in a taxable account and repurchasing it in an IRA within 30 days would trigger a wash sale. If the wash sale occurs in an IRA or Roth IRA, the disallowed loss is permanently forfeited, as the IRA's basis isn't adjusted.

To avoid this, opt for in-kind transfers whenever possible. If selling at a loss is unavoidable, wait at least 31 days before repurchasing the security at your new brokerage. Also, disable dividend reinvestment plans (DRIPs) during the transfer to prevent automatic purchases that might trigger a wash sale.

Once you've addressed these tax concerns, focus on keeping communication open during the process.

Stay in Contact with Both Brokerages

In addition to reviewing forms and managing tax concerns, staying in touch with both your current and new brokerages is key to a smooth transfer. Confirm that both firms have received your TIF and ACATS request. If any issues arise, ask for clear explanations and instructions on how to resolve them.

"If there is a problem, ask for an explanation of how to correct it." - Investor.gov

Be prepared for your old account to be frozen for about a week during the transfer process. Identify any non-transferable assets, such as proprietary mutual funds or annuities, and decide whether to liquidate them or leave them behind.

If delays occur, escalate the issue within the affected firm. Many new brokerages also offer reimbursement for transfer-out fees, which typically range from $50 to $100, so inquire about these programs when initiating your switch.

Using Mezzi to Manage Your Brokerage Switch

Switching brokerages can feel overwhelming, especially when you’re juggling multiple accounts, keeping an eye on tax outcomes, and trying to stay true to your investment strategy. Mezzi’s AI-powered platform takes the stress out of the process by consolidating everything into one dashboard and offering automated insights to help you sidestep costly mistakes.

AI-Driven Tax Optimization

Understanding the tax and fee implications of transferring brokerage accounts is one of the trickiest parts of the process, but Mezzi’s advanced AI tools make it easier to navigate. The platform automatically identifies wash sale risks across your linked accounts, keeping you in line with IRS regulations. It reviews your transaction history and calculates disallowed losses under IRS rules. For example, if you sold $10,000 worth of Tesla stock at a loss before transferring accounts and then repurchased it within 30 days at your new brokerage, Mezzi would calculate the disallowed loss - say $3,200 - and suggest alternatives like a comparable ETF.

Some users have reported capturing 15-20% more in tax savings compared to manual methods, which may help improve tax efficiency during a transfer.

Maintaining Portfolio Balance with the X-Ray Feature

When you transfer brokerages, your accounts are typically frozen for about a week, making it tough to keep tabs on your portfolio’s allocation. Mezzi’s X-Ray feature steps in by aggregating holdings from both your old and new accounts, helping you spot hidden risks. For example, it might reveal that you’re 25% overexposed to tech stocks, with combined positions in Apple (12%), Microsoft (8%), and Nvidia (5%) exceeding your target allocation of 15%.

The X-Ray tool updates daily during the 5-7 business day ACATS transfer process, flagging potential concentration risks like single-stock holdings above 10% or sector overweights. One user discovered an 18% overlap in tech exposure they hadn’t noticed when viewing accounts individually. With this insight, you can make pre-transfer adjustments - like trimming positions - before the freeze begins, keeping your strategy intact.

Viewing All Accounts in One Place

Mezzi connects seamlessly with major brokerages like Fidelity, Vanguard, Schwab, and Robinhood through secure Plaid integration, bringing all your accounts together in one dashboard. This consolidated view may help streamline management and reduce errors and delays during the transfer process.

The dashboard provides real-time updates on balances, positions, and transfer statuses, helping you track validation progress (which usually takes 1-3 days) and quickly flag issues like delayed dividends. Some users have reported 40% faster transfer verifications and 25% fewer errors in asset matching compared to manual methods. For instance, in one case involving a $500,000 portfolio transfer, Mezzi identified non-transferable assets early, which may help users avoid certain fees. The platform even supports fractional shares and crypto holdings, ensuring you have a complete view of your portfolio - even when some assets can’t be transferred through ACATS.Conclusion: Planning Your Brokerage Switch

What to Remember When Switching Brokerages

Switching brokerages requires careful preparation to ensure your investment strategy stays intact. Start by initiating the transfer with your new broker, double-checking that all details - such as names, Social Security numbers, and account types - match perfectly across your documents. Before the process begins, download all your account statements, trade confirmations, and cost basis records. It’s also wise to disable dividend reinvestments and close any pending limit orders to avoid complications during the transfer.

Opt for an in-kind transfer whenever possible. This method moves your assets without triggering taxable events, like capital gains. However, be aware that some assets, like proprietary mutual funds or fractional shares, may need to be sold and cannot transfer directly. Once the transfer is complete, carefully compare your final statement from the old brokerage with the first statement from the new one to confirm that all shares and their cost basis have been correctly transferred.

Using tools like Mezzi may help make the process more efficient. Mezzi consolidates your accounts, highlights potential wash sale risks, and provides AI-powered insights that may support portfolio balance, even when accounts are temporarily frozen. Its X-Ray feature also allows you to monitor your holdings across brokerages, which may help you identify concentration risks and make adjustments before the transfer. By following these steps, you may help your investment strategy remain consistent and tax-efficient throughout the switch.

FAQs

Should I do an in-kind transfer or a cash transfer?

When it comes to transferring assets, an in-kind transfer is often used to move securities directly to another account without selling them, which may help you avoid triggering taxable events.

In contrast, a cash transfer requires selling your assets first. While this might seem straightforward, it can lead to taxable gains, depending on how much your investments have appreciated.

Before making a decision, it’s important to think about your tax situation and your investment goals. Each option has its pros and cons, so aligning your choice with your financial strategy is key.

How can I avoid wash sales during a brokerage transfer?

To steer clear of wash sales, make sure to wait at least 31 days before buying back the same or a substantially identical security. Another smart approach is using in-kind transfers, which involve moving securities directly between accounts without selling and repurchasing them - this sidesteps potential wash sale issues.

It’s also important to coordinate your trades across all accounts, including those held by your spouse. Be cautious about repurchasing securities in IRAs or HSAs during the 61-day wash sale window, as doing so could jeopardize your tax benefits.

What should I check if my cost basis is missing after the move?

If your cost basis is missing, start by verifying whether it was transferred correctly from your previous records or brokerage. Sometimes, missing details can happen due to transfer errors or incomplete documentation. To resolve this, you might need to use recovery methods or estimate the cost basis to ensure your tax reporting stays accurate.

Reach out to your brokerage for assistance or consult a tax advisor to handle any discrepancies. Taking these steps can help you stay on top of your records and remain compliant with tax regulations.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.