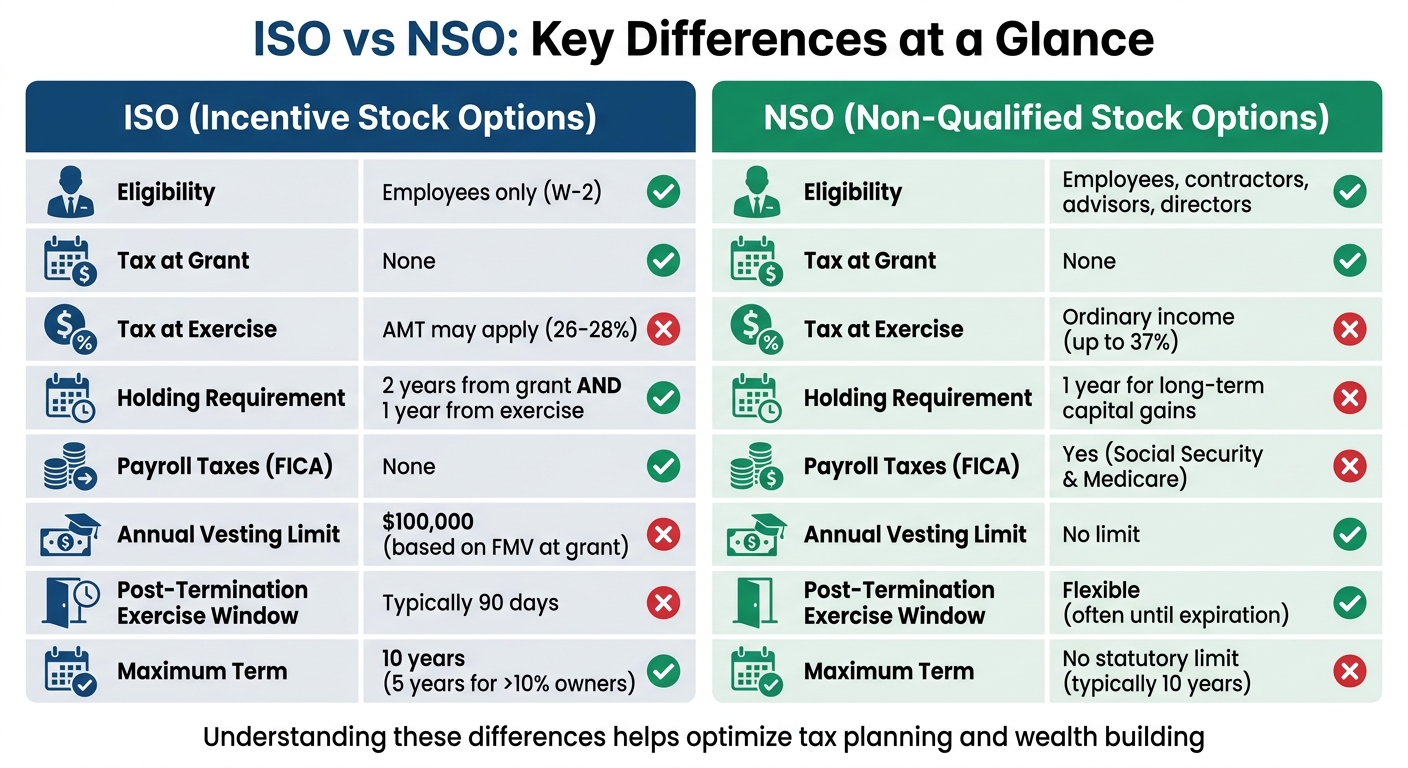

ISO (Incentive Stock Options) and NSO (Non-Qualified Stock Options) are two common types of equity compensation, but they differ in eligibility, tax treatment, and flexibility. Here's what you need to know:

- Eligibility: ISOs are only for employees, while NSOs can be granted to employees, contractors, and advisors.

- Tax at Exercise: ISOs may trigger Alternative Minimum Tax (AMT), but NSOs are taxed as ordinary income immediately.

- Holding Periods: ISOs require meeting specific timelines for favorable tax rates, whereas NSOs have simpler rules.

- Limits: ISOs have annual vesting caps and stricter post-termination exercise windows, while NSOs are more flexible.

Quick Comparison

| Feature | ISO | NSO |

|---|---|---|

| Eligibility | Employees only | Employees, contractors, advisors |

| Tax at Grant | None | None |

| Tax at Exercise | AMT may apply | Ordinary income |

| Holding Requirement | 2 years from grant, 1 year from exercise | 1 year for long-term gains |

| Payroll Taxes | None | Social Security & Medicare |

| Post-Termination | Typically 90 days | Flexible |

Understanding these differences may help you plan exercises and manage taxes more effectively.

ISO vs NSO Stock Options Comparison Chart

Who Can Receive Each Type

ISO Eligibility

ISOs come with specific and strict requirements about who can receive them. They are exclusively available to W-2 employees - those directly employed by the company or its subsidiaries. If you’re an independent contractor, consultant, advisor, or a non-employee board member, you won’t qualify for ISOs.

"ISOs can only be granted to employees - contractors, advisors, and board members are excluded." - Harness

The restrictions tighten further for employees who hold significant ownership in the company. If an employee owns more than 10% of the company’s total voting power, the exercise price must be set at a minimum of 110% of the fair market value at the time of the grant. Additionally, these shareholders are limited to a five-year option term instead of the standard 10 years.

Another limitation to keep in mind is the annual vesting cap. Only $100,000 worth of ISOs (measured by their fair market value at the time of the grant) can become exercisable for the first time in a single calendar year. Any amount exceeding this limit automatically converts to NSO status.

NSO Eligibility

NSOs are much more flexible in terms of eligibility. Companies can grant NSOs to a wide range of individuals, including employees, independent contractors, consultants, directors, advisors, and even vendors. This broad eligibility makes NSOs the go-to option for compensating anyone who doesn’t fit the traditional employee role.

"Non-qualified stock options can be granted to a company's employees as well as other service providers such as independent contractors and consultants." - Michael Callahan, Partner and Director of Wealth Management, Sachetta Callahan

NSOs don’t come with the same restrictions as ISOs. There’s no $100,000 annual vesting limit, no special rules for 10% shareholders, and no rigid post-termination exercise deadlines. If your company needs to extend stock options to individuals outside the standard employee framework, NSOs are often the only practical choice.

Tax Treatment at Grant and Exercise

ISO Tax Treatment

If the strike price matches the fair market value of the stock, no tax is due at grant or exercise. However, there’s a catch: the difference (or "spread") between your exercise price and the stock's fair market value at the time of exercise is included in Alternative Minimum Tax (AMT) calculations. If this spread is large, it could lead to a hefty AMT liability, which makes careful planning essential to balance the potential for long-term capital gains with AMT exposure.

"The core ISO planning problem: you want to hold shares long enough to qualify for LTCG treatment, but you don't want to over-exercise and trigger a large AMT bill you can't cover without selling shares you intended to hold." - Equity Simplified

For 2026, AMT rates stand at 26% for income up to $244,500 and 28% for amounts above that. Exemptions are $90,100 for single filers and $140,200 for joint filers, with phaseouts starting at $500,000 and $1 million, respectively. While your employer will provide Form 3921 to document the exercise, there’s no tax withholding at that time.

NSO Tax Treatment

NSOs don’t trigger a tax event at the time of grant. However, at exercise, the spread between the exercise price and the stock's fair market value is treated as ordinary income. This income is reported on your W-2 and is subject to federal income tax as well as Social Security and Medicare taxes.

"The moment of exercise creates a clear taxable event. The spread is taxable as ordinary income and your company will usually withhold taxes." - Shelby Whitefield, CPA, Carta

Because taxes are withheld at exercise, you’ll need sufficient cash to cover both the exercise price and the tax liability. Alternatively, you could consider a cashless exercise, where some shares are sold to cover these costs. Unlike ISOs, NSOs don’t involve AMT considerations.

Tax Events Comparison

The table below highlights the key tax differences between ISOs and NSOs:

| Feature | ISO | NSO |

|---|---|---|

| Tax at Grant | None | None (if strike price = FMV) |

| Tax at Exercise | No regular tax; AMT may apply on the spread | Ordinary income tax on the spread |

| Tax Rate at Exercise | 26–28% (AMT only) | Up to 37% (ordinary income) |

| Withholding Required | No | Yes (federal income and payroll taxes) |

| Payroll Taxes (FICA) | None | Social Security & Medicare |

| Reporting Form | Form 3921 | W-2 (Box 12, Code V) |

Holding Periods and Sale Tax Implications

ISO Holding Periods

To take full advantage of the tax benefits associated with Incentive Stock Options (ISOs), you need to follow the "2 and 1" rule. This means holding your shares for at least two years from the grant date and at least one year from the exercise date. If you meet these conditions, the entire gain - from the strike price to the sale price - is taxed at long-term capital gains rates, which are currently 0%, 15%, or 20%, depending on your income level. However, selling the shares before meeting these holding periods triggers a disqualifying disposition. In this case, the "bargain element" (the difference between the strike price and the fair market value at exercise) is treated as ordinary income, while any additional gain is taxed as a capital gain (either short-term or long-term based on how long you held the shares after exercising).

Even in the event of a disqualifying disposition, ISOs are not subject to Social Security and Medicare taxes. Timing your ISO exercise early in the year can provide flexibility. For example, if the stock price drops significantly by the end of the year, selling before the one-year mark might help you avoid an Alternative Minimum Tax (AMT) adjustment for that year.

NSO Holding Periods

For Non-Qualified Stock Options (NSOs), the holding period primarily affects how any post-exercise appreciation is taxed. If you hold the shares for more than one year after exercising, any additional gain qualifies for long-term capital gains treatment.

However, if you sell the shares within one year of exercising, any post-exercise gains are treated as ordinary income.

Holding Rules and Tax Implications Comparison

The table below highlights the key differences in holding requirements and tax implications for ISOs and NSOs:

| Feature | ISO (Qualifying) | ISO (Disqualifying) | NSO |

|---|---|---|---|

| Holding Requirement | 2 years from grant AND 1 year from exercise | Sold before meeting the "2 and 1" rule | 1 year from exercise (for long-term capital gains) |

| Tax on Spread | Long-term capital gain | Ordinary income | Ordinary income (at exercise) |

| Tax on Post-Exercise Gain | Long-term capital gain | Capital gain (short-term or long-term) | Capital gain (short-term or long-term) |

| Payroll Taxes (FICA) | None | None | Yes (at exercise) |

| AMT Exposure | Yes (at exercise) | No (if sold within the same year) | No |

| Cost Basis for Sale | Strike price | FMV at exercise | FMV at exercise |

Grasping these holding rules can help when deciding the best time to exercise or sell your options. By understanding the tax implications, you may be able to make more informed decisions that align with your financial goals.

Limits and Restrictions

ISO Limits and Restrictions

The IRS enforces specific rules and limits for Incentive Stock Options (ISOs) that shape how they function and their tax advantages. These restrictions play a major role in how you plan to exercise your options and manage potential tax events.

ISOs come with a maximum term of 10 years from the grant date. For employees who own more than 10% of the company, the term is reduced to 5 years, and the exercise price must be at least 110% of the fair market value at the time of the grant. If you leave your job, you typically have 90 days to exercise your ISOs to maintain their tax-advantaged status. After this period, they convert to Non-Qualified Stock Options (NSOs). However, in cases of disability or death, the exercise window may extend to 12 months.

"This relatively short post-employment exercise window creates effective 'golden handcuffs' that encourage continued employment - a strategic consideration for both employers and employees." – Harness

NSO Limits and Flexibility

Non-Qualified Stock Options (NSOs) offer more flexibility compared to ISOs. Unlike ISOs, NSOs are not subject to an annual vesting limit, meaning there’s no cap on how much value can vest in a single year. While NSOs typically expire after 10 years, there is no statutory maximum term, allowing for more variation based on company policies.

One of the standout features of NSOs is their flexible post-termination exercise window. In many cases, you can exercise your options at any point before they expire. Some companies even allow extended exercise periods, giving you additional time to consider factors like liquidity events or your financial readiness.

Limits and Terms Comparison

| Feature | ISO | NSO |

|---|---|---|

| Annual Vesting Limit | $100,000 (based on FMV at grant) | No limit |

| Maximum Term | 10 years (5 years for >10% owners) | No statutory limit (typically 10 years) |

| Post-Termination Window | Typically 90 days | Flexible (often until expiration) |

| Eligible Recipients | Employees only | Employees, contractors, directors |

| Transferability | Generally non-transferable | More flexible; can be gifted or transferred |

These rules are more than just compliance guidelines - they can directly impact your long-term financial strategies. For example, if you hold multiple equity grants, reviewing their vesting schedules across calendar years can help you determine which options qualify as ISOs versus NSOs. If you're planning to leave your company, it’s crucial to ensure you have the resources to exercise ISOs within the 90-day window to retain their tax benefits. By understanding these limits, you can better plan when to exercise options and how to approach tax considerations.

Impact on Wealth Building

ISO Benefits and Risks

Incentive Stock Options (ISOs) can play a key role in building wealth when managed carefully within the holding rules. By meeting these requirements, any gains are taxed at long-term capital gains rates rather than ordinary income rates. This difference in tax treatment may result in substantial savings - potentially amounting to hundreds of thousands of dollars for large equity positions.

However, ISOs come with a potential downside: the Alternative Minimum Tax (AMT). This tax applies to theoretical gains, even if you haven’t sold your shares. For 2025, AMT rates are 26% on the first $239,100 of alternative minimum taxable income and 28% for amounts above that. If the stock value drops after exercising your options but before selling, you could face taxes on gains that no longer exist.

"The complexity [of ISOs] increases the risk of paying AMT on paper gains that might disappear if the stock price declines - creating a significant downside potential." – Harness

To mitigate AMT risk, consider spreading your ISO exercises across multiple years to stay under the AMT exemption threshold, which is $88,100 for single filers and $137,000 for married couples filing jointly in 2025. Additionally, filing an 83(b) election within 30 days of early exercise can lock in a low spread and start the clock on the capital gains holding period.

NSO Simplicity and Drawbacks

Non-Qualified Stock Options (NSOs) offer a more straightforward approach but come with an immediate tax burden. When you exercise NSOs, the spread is taxed as ordinary income, along with payroll taxes like Social Security and Medicare. This means rates can go as high as 37%. Unlike ISOs, NSOs don’t involve AMT or complex holding periods, and your employer typically handles tax withholding.

For example, if you exercise NSOs with a $200,000 spread, you might owe $74,000 or more in taxes before selling any shares. While this makes NSOs less efficient for long-term wealth building, their predictability and simplicity can make planning easier.

"NSOs are inherently simple. There's no choice apart from the choice of when to exercise. With ISOs, there's so much more strategy involved." – James Bashall, Financial Advisor, NerdWallet Wealth Partners

Exercise Timing and Tax Planning

Timing your stock option exercises is just as important as deciding between ISOs and NSOs. For ISOs, exercising when the spread is small - such as during market downturns or early in your company’s growth stage - may help reduce AMT exposure. If you’re already in a high-income year due to bonuses or RSU vesting, the difference between ordinary income and AMT rates narrows, making it a relatively better time to exercise ISOs.

For NSOs, align your exercises with your financial situation and cash flow. If liquidity is an issue, many companies allow "sell-to-cover" exercises, where you sell enough shares to cover the strike price and taxes. If you plan to leave your company, keep in mind that ISOs must typically be exercised within 90 days to retain their tax advantages - otherwise, they convert to NSOs.

Exercising ISOs early in the year gives you until December 31 to decide whether to hold for long-term capital gains or make a disqualifying disposition if the stock price drops. Selling in the same year eliminates AMT liability, though you’ll owe ordinary income tax on the spread. These strategies can help you align your stock options with your broader financial goals.

"Stock options don't have to feel like a gamble with the IRS. With the right planning, they can turn into one of the smartest wealth-builders in your career." – Natalie Cohen, CPA, Dark Horse CPAs

ISOs vs. NSOs Explained: Understanding Your Stock Options

Wrapping Up

Choosing between Incentive Stock Options (ISOs) and Non-Qualified Stock Options (NSOs) often comes down to your financial goals, employment situation, and tolerance for risk. ISOs are typically available only to W-2 employees and may qualify for favorable long-term capital gains tax treatment. However, they come with potential Alternative Minimum Tax (AMT) exposure and strict holding period requirements. On the other hand, NSOs are more flexible - they can be granted to employees, contractors, and advisors - but they are taxed as ordinary income when exercised, avoiding the AMT complexities tied to ISOs.

If you're a long-term employee at a growing company and can meet the necessary holding periods, ISOs may reduce your tax bill significantly. That said, it’s worth remembering that ISOs can trigger AMT on paper gains, even if you don’t sell the shares.

For those who prioritize simplicity or flexibility, NSOs might be a better fit. While they may lead to higher taxes at exercise, they don’t require specific holding periods or carry the risk of unexpected AMT liabilities.

Timing your exercises strategically is key to managing taxes. For ISOs, exercising when the spread between the strike price and fair market value is small may help reduce AMT exposure. Spreading exercises across multiple years could also keep you under the AMT exemption threshold - set at $88,100 for single filers and $137,000 for married couples filing jointly in 2025. With NSOs, it’s wise to align your exercise timing with your cash flow and broader financial plans.

When approached thoughtfully, stock options can be a powerful tool for building wealth. By understanding how ISOs and NSOs align with your goals, you can make informed decisions that help optimize your equity compensation while minimizing tax surprises. With the right strategy, stock options can play a meaningful role in your overall financial success.

FAQs

How do I know if my options are ISOs or NSOs?

To determine whether your stock options are Incentive Stock Options (ISOs) or Non-Qualified Stock Options (NSOs), start by reviewing your grant agreement or the stock option plan provided by your employer.

ISOs are generally offered to employees and come with potential tax advantages, but these benefits depend on meeting specific holding period requirements. In contrast, NSOs can be granted not only to employees but also to contractors or other service providers. However, exercising NSOs typically leads to taxation as ordinary income.

If you're uncertain about your stock options, consider reaching out to your HR department or consulting a financial advisor for clarification.

When does it make sense to do a same-year ISO sale to avoid AMT?

When exercising incentive stock options (ISOs), a same-year sale might be worth considering if the stock's value is high at the time of exercise and you're looking to manage potential Alternative Minimum Tax (AMT) liability. Selling the shares promptly can help you sidestep a larger tax burden tied to the AMT preference item. This approach may also be useful if there's a chance the stock's value could decline after the exercise.

What should I plan for before leaving a job with ISOs or NSOs?

Before moving on from a job with Incentive Stock Options (ISOs) or Non-Qualified Stock Options (NSOs), it’s important to think through the tax implications and the timing of exercising your options. If you have ISOs, exercising them might trigger the Alternative Minimum Tax (AMT), so it’s worth evaluating how this could affect your tax situation. For both ISOs and NSOs, take a close look at the vesting schedule, the ideal timing for exercising your options, and the holding period requirements that may help you qualify for potential tax advantages. Working with a financial or tax advisor can be a smart way to reduce liabilities and ensure your decisions align with your financial goals.

Disclosures:

- This content is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.

- Tax treatment of stock options depends on individual circumstances and may change based on IRS rules and personal tax situations. Consult a qualified tax advisor for personalized guidance.

- Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.