For many investors, the short answer may be no. If you hold a simple taxable account or 1–2 properties, direct ownership plus umbrella insurance may cover most of the issue at a much lower cost than an LLC. Once investable assets reach around $500,000+, rental risk grows, or estate transfer becomes part of the picture, an LLC - and later a trust - may start to look more reasonable.

Here’s the simple version:

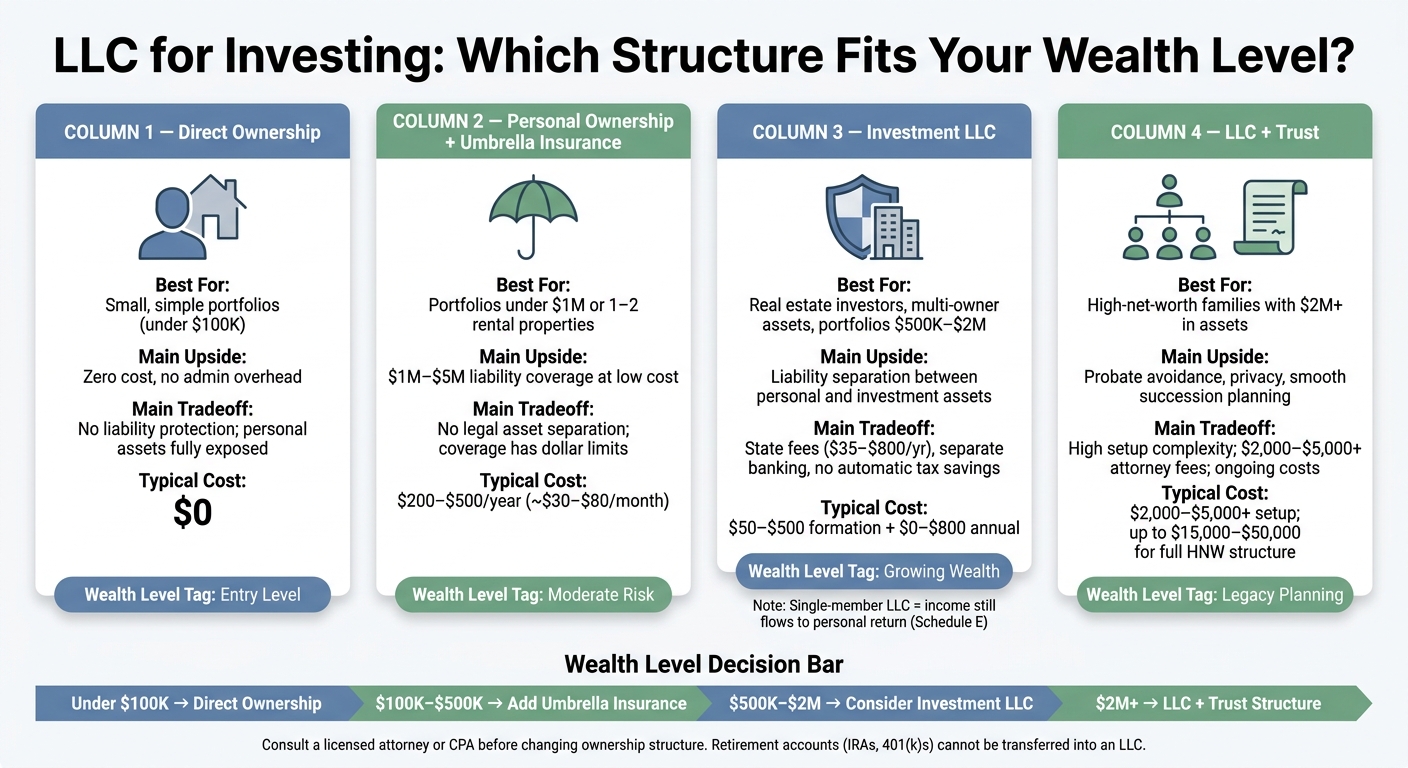

- Direct ownership may fit small, simple portfolios with low admin needs.

- Umbrella insurance may add $1 million to $5 million of liability coverage for about $200 to $500 per year.

- An LLC may add a legal layer between your personal assets and certain investment risks, but it may also bring filing fees, annual costs, separate banking, and recordkeeping.

- An LLC with a trust may make more sense when probate avoidance, privacy, and succession planning start to matter more than low cost.

- Retirement accounts like IRAs and 401(k)s generally need to stay in your name.

- Mortgaged real estate moved into an LLC may run into lender limits, including due-on-sale language.

- A single-member LLC usually does not create a new tax shelter. Income may still show up on your personal return.

What changes with wealth level? Mostly the tradeoff. At lower asset levels, the extra cost and paperwork may outweigh the legal layer. At higher levels - especially above $2 million - the mix may shift toward liability separation, probate planning, and privacy.

LLC for Investing: Which Structure Fits Your Wealth Level?

Do you really NEED an LLC for your Business or Real Estate Investment?

Quick Comparison

| Option | May fit best for | Main upside | Main tradeoff | Typical cost |

|---|---|---|---|---|

| Direct ownership | Small taxable portfolios | Lowest friction | No asset separation | $0 plus normal account costs |

| Direct ownership + umbrella | Under $1 million or 1–2 properties | Low-cost liability coverage | No legal wall between assets | About $200–$500/year |

| Investment LLC | Rentals, private deals, multi-owner assets | Liability separation | State fees, admin, banking rules | Formation and annual fees may range from $35 to $800+ depending on state |

| LLC + trust | Higher-net-worth households | Probate avoidance, succession, privacy | Higher setup cost and more moving parts | Trust setup may run about $2,000–$5,000+ |

So if you’re asking, “Do I need an LLC for investing?” the better question may be: What risk am I trying to separate, and is that risk large enough to justify the cost?

1. Direct personal ownership

When you hold stocks, bonds, ETFs, or rental property in your own name, the account ties back to your Social Security number for tax reporting. Any income and gains may flow onto your personal tax return. There’s no separate entity to set up, no extra filing for the entity itself, and no annual state paperwork tied to that structure.

For smaller accounts, this may be the default setup because it’s cheap and simple. The tradeoff: it may offer the least protection.

There’s no legal wall between the investment and your personal assets. So if a claim comes up, it may reach your home, savings, or other personal property. With smaller taxable portfolios, insurance may matter more than setting up an entity. But that may change when a certain asset type or a lender’s rules make ownership more involved.

Some assets also need to stay in your name. Retirement accounts must remain in your name, and moving a mortgaged property into an LLC may trigger lender restrictions, including due-on-sale language.

Direct ownership may also do less for estate planning. Assets held personally may pass through probate, which is public and may move slowly. For many investors, the next step may be more insurance, not an LLC.

2. Personal ownership plus umbrella insurance

For many investors, the first step up from direct ownership may be a personal umbrella policy. It may add $1 million to $5 million in liability coverage on top of auto and homeowners policies for about $200 to $500 a year. And the appeal is pretty plain: no separate entity tax return, no state registration, no annual reports, and no registered agent fees.

That said, this type of protection is financial, not legal. It may pay covered claims above your primary policy limits, but it does not cover business debts or contract disputes. If you own rental property, that gap may matter.

There’s also the limit issue. If a judgment goes past your policy cap, your home equity, brokerage accounts, and savings may still be exposed. And unlike an LLC, which may separate one asset from another, personal ownership means a lawsuit tied to one investment may reach the rest of what you own if insurance runs out.

For investors with 1–2 properties or under $1 million in combined assets, this setup is often the most practical choice. At that size, the low cost and easy upkeep may outweigh the tradeoffs.

Even if someone later adds an LLC, umbrella coverage may still matter for personal liability. Privacy also stays low here. Your name appears on public title and ownership records, which some investors may not mind early on. But once liability, privacy concerns, or rental exposure grow past what umbrella coverage may handle, the next step may be an LLC.

3. Investment LLC

An LLC separates your personal assets from your investment activity. But the main point is liability protection, not tax savings. In many cases, a single-member LLC is taxed as a disregarded entity, which means the income may still flow through to your personal tax return.

If the LLC faces a claim, only the LLC's assets are typically at risk, not your home or personal savings. That setup may matter more once your assets grow, or when your liability exposure may go beyond what personal ownership or umbrella insurance may reasonably cover.

By default, a single-member LLC is a disregarded entity. So for tax purposes, the income may still show up on your personal return. With rental real estate, that often means Schedule E.

That protection only works if you keep a clean line between you and the LLC. In practice, that usually means:

- A separate bank account

- No commingling of personal and LLC funds

- An operating agreement

If that separation isn't maintained, courts may pierce the corporate veil and hold you personally liable. In plain English: if you treat the LLC like your personal wallet, a court may do the same.

The cost side is hard to ignore. State filing fees range from $35 in Montana to $500 in Massachusetts. Annual fees range from $0 in Delaware to $800 in California. Registered agent services also tend to cost about $50 to $150 per year.

There are financing issues too. Moving mortgaged property into an LLC may trigger a due-on-sale clause. And financing through an LLC often requires 20% to 30% down.

An investment LLC may fit best when liability risk rises and the portfolio is large enough to absorb the added cost. The article ties that more closely to investors with $500,000 or more in investable assets, multiple rental properties, or private deals. For a plain taxable brokerage account, the extra fees and paperwork often add more friction than value.

At higher wealth levels, estate-transfer planning may matter as much as liability protection. That’s usually where a trust may start to become part of the setup.

4. LLC plus trust

At higher wealth levels, liability protection may be only one part of the picture. Once that piece is covered, the next issue may be transfer and continuity. An LLC by itself may not handle those two jobs.

A common setup places the LLC interests inside a revocable living trust. In that structure, the trust owns the LLC, and the LLC holds the assets. When the LLC interest is titled to the trust, the membership interest may avoid probate, and a successor trustee may step in to manage it. That may matter most if someone else may need to take over the account without delay.

Without the trust layer, your LLC interest may still become a probate asset. That means a court-supervised process that may take 12 to 18 months. In California, probate fees may reach 4% to 6% of gross estate value.

On taxes, a revocable trust is usually tax-neutral. The IRS generally treats it as a grantor trust, and it may not add meaningful protection from personal creditors. An irrevocable trust may offer stronger separation, but its tax brackets compress fast. Because of that, it may fit mainly very large estates or narrow asset-protection goals.

Privacy may also improve with this setup. The trust, not your personal name, appears on the LLC's ownership records and filings.

The cost reflects the extra moving parts. An attorney-drafted trust typically runs $2,000 to $5,000. A full high-net-worth structure may reach $15,000 to $50,000 upfront, with $5,000 to $15,000 per year for tax returns and trustee fees.

One mistake shows up again and again: people create the structure, then forget to retitle the LLC interests into the trust. For smaller accounts, that overhead may outweigh the upside. The cost-benefit split may be easier to see when the structures sit next to each other.

5. Using Mezzi to review your situation before changing ownership structure

Before paying an attorney to draft an LLC operating agreement, it may make sense to map your accounts first. Mezzi connects brokerage, retirement, real estate, and crypto accounts through read-only connections, so you may see your holdings in one place without moving anything.

That matters because the right structure may depend on what you own, where the risk may sit, and whether an account may legally be retitled. For example, some of your net worth may sit in taxable accounts with more liability exposure. At the same time, not every asset may be moved into an LLC. Retirement accounts like 401(k)s and IRAs cannot be transferred into one.

Mezzi may also make it easier to test simpler options first. If the numbers suggest an umbrella policy may cover most of the risk, an LLC may add cost without much upside. In California, the $800 annual minimum franchise tax applies even if the LLC earns nothing. When you stack that cost next to the protection the structure may add, the tradeoff may be easier to see.

The same account view may also show whether your records are clean enough for LLC protection in the first place. If transactions mix personal and investment expenses, the LLC may not protect you in the way you expect. That pattern weakens LLC protection. Seeing that before forming the entity may be more useful than finding out later.

Pros and cons by structure and scenario

Each structure may address a different type of risk. The table below shows where each one may fit, based on wealth level and portfolio setup.

Direct ownership may be the starting point for simple portfolios. Umbrella insurance may be the lowest-friction next step for liability coverage. It may pay claims, but it does not separate assets. Because of that, it may be the usual first move some people make before setting up an LLC.

An investment LLC may fit real estate or co-owned investments. In most cases, an LLC may serve mainly as a liability shield, not a tax break. By default, a single-member LLC is taxed like a sole proprietorship. The tradeoff may look better as liability exposure and asset complexity increase.

An LLC plus trust may fit estate transfer planning. A trust may add probate avoidance, privacy, and smoother succession. That may be why this setup often shows up in higher-wealth planning instead of early-stage investing.

| Structure | Best Fit | Main Benefits | Main Drawbacks | Typical Cost |

|---|---|---|---|---|

| Direct Ownership | Small, simple portfolios | Simplicity; no extra fees; direct tax reporting | No liability protection; personal assets exposed | $0; minimal admin |

| Ownership + Umbrella Insurance | Moderate risk, mid-wealth | Cost-effective coverage without entity overhead | No legal asset separation; coverage has limits | $30–$80/month; low friction |

| Investment LLC | Real estate, multi-owner groups | Asset protection; governance framework | Annual fees; separate banking required; no automatic tax savings | $50–$500 formation; $0–$800 annual maintenance |

| LLC + Trust | High-net-worth, legacy planning | Probate avoidance; privacy; smooth succession | High setup complexity; reduced control if irrevocable | $1,000–$5,000+ setup; high friction |

Use your actual account mix and risk exposure before changing title on anything.

How to decide based on your actual numbers

Put the tradeoffs above into your own math before you retitle anything.

- Define the goal first. Start with the main goal: liability, taxes, estate transfer, or privacy. Each one may point to a different setup.

- Match your asset level to a structure. Under $250,000, direct ownership plus umbrella insurance may often come out ahead on cost. From $500,000 to $2 million, an LLC may start to make more sense for liability protection. Above $2 million, trust planning may start to enter the picture. Once you know the asset level, compare the yearly carrying cost of each option.

- Compare state filing and annual costs. Put the yearly LLC cost in your state next to the umbrella premium you might otherwise pay. In California, for example, the $800 annual franchise tax applies even if the LLC earns nothing.

- Test umbrella coverage first. For smaller portfolios and side businesses, it may address the liability issue at a lower cost.

The chart below turns those thresholds into a simple profile-based rule.

| Investor Profile | Personal + Umbrella Insurance | Investment LLC | LLC + Trust |

|---|---|---|---|

| Small taxable investor (<$100k) | Often sufficient | Usually unnecessary | Usually too much structure |

| Real estate investor (1–2 units) | Usually not enough | Often sufficient | May fit |

| High-income household ($500k–$2M) | May fit | Often sufficient | May fit |

| High-net-worth family (>$2M) | Usually not enough | May fit | Often sufficient |

FAQs

How do I know if an LLC is worth the cost for my portfolio?

It depends on your goals and risk tolerance. An LLC does not automatically lower taxes. Its main role may be liability protection and a more formal way to manage things on the admin side.

It may make sense if you have major assets to protect, put money into higher-risk areas like real estate, or want a clear structure for tracking ownership, contributions, and distributions with partners. If your portfolio is small or your liability risk may be low, annual fees of $50 to $800 or more may outweigh the upside.

Should each rental property have its own LLC?

It depends on your risk tolerance and the size of your portfolio.

Putting each property in its own LLC may add a layer of legal separation. So if one property faces a lawsuit, the equity in your other properties - and even your personal accounts - may be better insulated from that claim.

But there’s a tradeoff. Separate LLCs may mean more cost and more admin work.

For smaller portfolios, some investors use one umbrella LLC for several properties. Others rely more on strong umbrella insurance instead.

When does it make sense to add a trust to an LLC?

It may make sense if you want an LLC’s day-to-day flexibility along with longer-term estate and succession planning.

The LLC may handle operations and liability. The trust may control how ownership interests are held and transferred.

That setup may support:

- smoother inheritance

- more private ownership

- continued control of assets across generations

In many cases, the trust owns the LLC membership interests.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.