When it comes to advanced financial planning, tools like Mezzi and eMoney Advisor offer features typically reserved for professionals. But can individuals access and use these tools effectively? Here's a quick breakdown:

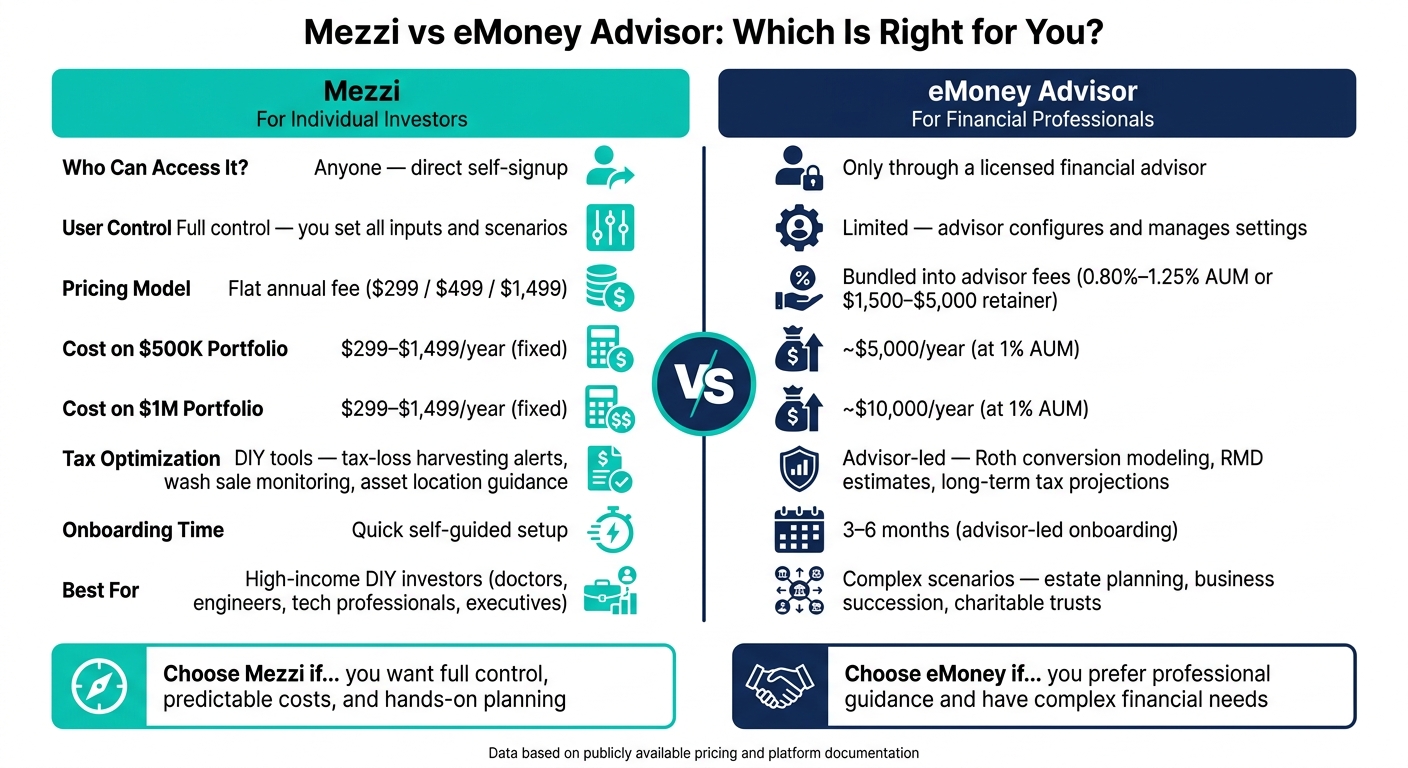

- Mezzi: Designed for individuals, Mezzi offers direct access to advanced financial planning tools without needing a financial advisor. It connects to your accounts, provides tax optimization insights, and helps model retirement scenarios. Costs range from $299 to $1,499 annually, making it a cost-effective choice for hands-on investors.

- eMoney Advisor: Built for financial professionals, eMoney is not available directly to consumers. Individuals can only access it through a financial advisor, who manages the platform and provides guidance. Costs are tied to advisor fees, often percentage-based, which can grow with your portfolio size.

Key Differences:

- Access: Mezzi is DIY-friendly; eMoney requires an advisor.

- Control: Mezzi gives users full control; eMoney limits user input.

- Cost: Mezzi charges a flat fee; eMoney is bundled into advisor fees, typically 0.80%-1.25% of assets.

| Feature | Mezzi | eMoney Advisor |

|---|---|---|

| Audience | Individual investors | Financial advisors |

| Access | Direct signup | Advisor-managed |

| Cost | $299-$1,499 annually | Advisor fees (~1% AUM) |

| Control | Full user control | Advisor-driven |

| Tax Planning | DIY tools | Advisor-led insights |

Summary:

If you prefer managing your own finances and want lower, predictable costs, Mezzi may suit your needs. For those who value professional guidance or have complex financial situations, eMoney Advisor (via an advisor) might be worth considering.

Mezzi vs eMoney Advisor: Side-by-Side Comparison for DIY Investors

Mezzi: AI-Driven Financial Planning for Individuals

How Mezzi Works

Mezzi is a financial planning platform designed for individuals, operating as a fiduciary registered with the SEC. It connects to your existing accounts - such as 401(k)s, IRAs, Roth IRAs, and taxable brokerage accounts - using read-only access through Plaid and Finicity (Mastercard). Importantly, you don’t need to transfer your accounts, share login credentials, or hand over control of your investments.

Once linked, Mezzi analyzes your financial situation to spot areas like tax opportunities, allocation imbalances, unnecessary fees, and retirement planning adjustments. The platform provides professional-level insights, valued at up to $10,000 annually, while leaving all execution decisions in your hands. Pricing is straightforward, with annual subscription options: $299 for the Core plan, $499 for the Plus plan (its most popular tier), and $1,499 for the White Glove plan, which includes personalized coaching calls. For those managing portfolios of $500,000 or more, this pricing structure may represent substantial cost savings compared to traditional advisors who often charge 1% of assets under management (AUM).

Mezzi’s features are designed to deliver actionable insights, as outlined below.

Key Features of Mezzi

Mezzi’s tools focus on providing clear and personalized financial guidance.

- ETF Overlap Detection (X-Ray Tool): This feature examines your investments across all connected accounts to identify overlapping holdings. For example, you might own a total market index fund in your 401(k) and an S&P 500 ETF in a taxable account, creating duplicate exposure to large-cap U.S. equities. The X-Ray tool highlights these redundancies, helping you avoid paying unnecessary fees for similar assets.

- Tax Optimization Guidance: Mezzi offers year-round alerts for tax-loss harvesting opportunities and monitors wash sale risks across accounts. If you sell an investment to harvest a loss, Mezzi will notify you when the 30-day wash sale window ends, so you can repurchase without triggering tax issues. It also advises on asset location, helping you decide which account types - such as Roth, Traditional, or taxable - are better suited for specific asset classes like REITs or taxable bond funds.

- Retirement Planning: Instead of relying on generic calculators, Mezzi uses data from your actual accounts to create projections. Real balances, contribution habits, and asset allocations are factored into its retirement insights, offering a more precise understanding of your financial timeline.

Every plan also includes 24/7 AI chat support, enabling users to ask detailed questions - like when to consider a Roth conversion - and receive quick, data-driven responses instead of waiting days for human feedback.

Who Mezzi Is Built For

Mezzi is tailored for high-income professionals who want to maintain control over their financial decisions. It’s especially suited for individuals like doctors, engineers, tech employees, and executives. These users often deal with stock compensation, multiple retirement accounts, concentrated holdings, and tax scenarios that go beyond what basic financial tools can handle. For these investors, optimizing tax efficiency and making informed decisions are critical.

While Mezzi doesn’t replace specialized services such as estate planning or advanced CPA guidance, it’s a strong fit for those with straightforward-to-moderately complex portfolios who prefer hands-on management. It bridges the gap for financially savvy individuals who want professional insights without relying on traditional advisors.

eMoney Advisor: A Tool Built for Financial Advisors

What Is eMoney Advisor?

Unlike Mezzi, which helps individuals access advisor-level insights on their own, eMoney Advisor is a platform specifically designed for financial professionals. Owned by Fidelity Investments, eMoney Advisor supports advisors at RIAs, banks, and broker-dealers in managing complex financial scenarios. It’s not intended for individuals to manage their personal finances. The platform is equipped to handle intricate situations like trust distributions, charitable giving strategies, concentrated stock holdings, and state-specific tax planning. According to the 2026 T3/Inside Information Advisor Software Survey, financial professionals gave eMoney Advisor an 8.14 out of 10 rating.

One of its core features, the Decision Center, allows advisors to explore "what-if" scenarios during client meetings. They can adjust variables such as retirement age, spending habits, or income assumptions in real time, providing clients with an immediate understanding of how these changes might affect their financial plans. This level of functionality is tailored for trained professionals, not individual investors.

How Individuals Access eMoney Advisor

eMoney Advisor does not offer a version for direct-to-consumer use. Instead, individuals can only access the platform through a financial advisor’s Client Portal. This exclusivity underscores its professional focus.

"Give clients a superior online Client Portal to easily view their full financial picture and securely store important documents - all in one place, available exclusively through you." - eMoney Advisor

If you’re interested in using eMoney, your best bet is to work with a CFP or a fee-only advisor who provides financial planning services through the platform.

What eMoney Advisor Can Do

For financial advisors, eMoney delivers a robust toolkit. Its features include detailed year-by-year cash flow modeling, Monte Carlo simulations, high-net-worth financial planning tools, and tax projections based on IRS 1040 calculations. The CoPlanner feature streamlines the process by automating scenario creation, reportedly reducing planning time by 48%.

For individuals, however, access is more restricted. Through the Client Portal, you can aggregate accounts, track financial goals, and securely store important documents. But the platform’s more advanced planning tools remain accessible only to advisors. Even for professionals, onboarding can take three to six months, reflecting the platform’s complexity. This steep learning curve highlights why eMoney is geared toward advisors rather than DIY investors, making it clear that its design serves a very different audience compared to platforms like Mezzi.

Mezzi vs eMoney Advisor: A Direct Comparison for DIY Users

Access and User Control

Mezzi caters directly to DIY investors, allowing them to sign up independently and manage their financial plans on their own terms. This means you control everything - inputs, assumptions, and planning parameters - without relying on an intermediary. The platform is built for users who want full autonomy in their financial planning process.

On the other hand, eMoney Advisor operates through financial professionals. Accessing the platform requires working with an advisor who sets up a client portal for you. The advisor configures critical settings, such as inflation rates, return assumptions, and active planning modules. While you can view your financial plan, making adjustments independently isn't an option.

| Aspect | Mezzi | eMoney Advisor |

|---|---|---|

| Buyer Type | Individual investors | Financial advisors and firms |

| Access | Self-signup, direct access | Advisor-provided client portal |

| User Control | Full control by user | Limited, advisor-configured |

| Onboarding | Self-guided, quick setup | Advisor-led, may take weeks |

These differences in access and control set the stage for how each platform approaches planning depth and usability.

Planning Depth and Ease of Use

Mezzi simplifies financial planning for less experienced users. It uses plain-language prompts to help you explore scenarios like Roth vs. traditional contributions, Social Security strategies, and safe withdrawal rates. Its AI-driven guidance helps navigate technical complexities, presenting results in a straightforward, visual format.

eMoney Advisor, by contrast, is designed for professionals. It offers powerful tools like cash-flow modeling, Monte Carlo simulations, and multi-goal optimization. However, the platform's interface and technical setup can feel daunting for someone without financial training, making it less suitable for DIY investors.

These distinctions also influence how the platforms handle tax strategies and multi-account insights.

Tax Optimization and Multi-Account Insights

When it comes to tax planning, Mezzi provides actionable insights tailored for DIY users. It identifies opportunities for tax-loss harvesting, flags wash sale risks, and suggests optimal asset placement - helping you decide which investments might work best in taxable accounts versus tax-advantaged ones like Roth IRAs or 401(k)s.

eMoney Advisor offers robust tax modeling, but its tools are designed for professionals to interpret. Features like long-term tax liability projections, Roth conversion modeling, and RMD estimates are geared toward advisor-led planning. As a result, DIY investors typically can't interact directly with these tools or implement changes without professional assistance.

Cost and Value for DIY Investors

Cost is a major consideration for DIY investors, especially those focused on efficient financial planning. Mezzi offers clear, fixed-price subscriptions: $299 annually for the Core plan, $499 for Plus, and $1,499 for the White Glove plan. The pricing remains consistent regardless of portfolio size, providing predictability as your investments grow.

eMoney Advisor, however, is bundled into advisor services and isn't available for individual purchase. Costs are typically tied to the advisor's fee structure, which may include annual assets-under-management (AUM) fees ranging from 0.80% to 1.25%, or flat retainers starting at $1,500 to $5,000. For example, a 1% AUM fee on a $500,000 portfolio equates to about $5,000 annually - and as your portfolio grows, so do the fees. Over time, this difference between fixed subscription costs and percentage-based fees can result in significant savings for Mezzi users.

| Mezzi | eMoney Advisor (via advisor) | |

|---|---|---|

| Pricing Model | Fixed annual fee | AUM fee, retainer, or hourly rate |

| Starting Cost | $299 per year | ~$1,500–$5,000 upfront; ongoing AUM fees |

| Scales with Portfolio Size? | No | Yes |

| Best for | DIY planners | Full-service, advisor-led clients |

Conclusion: Choosing the Right Platform for Self-Directed Planning

The breakdown above highlights the key considerations for self-directed investors weighing their options.

Key Decision Factors

For individuals focused on managing their own wealth, the choice between Mezzi and eMoney Advisor often hinges on four main factors:

- Control over the planning process

- Complexity of financial needs

- Sensitivity to costs

- Preference for hands-on involvement

If you're the type of investor who prefers logging in, running scenarios, and acting on recommendations independently, a self-serve platform might align better with your style. On the other hand, if you'd rather delegate the heavy lifting to a professional and receive periodic updates with polished plans, an advisor-led platform could be the way to go.

Consider the financial aspect as well: with $1 million in investable assets, a 1% AUM fee equals $10,000 annually, regardless of the level of planning required. In contrast, a flat subscription fee remains constant, which can be a critical factor as your portfolio grows.

When Mezzi Is the Better Fit

Mezzi shines for investors who manage complex portfolios and prefer taking action independently. As an SEC-registered fiduciary with read-only access to linked accounts, Mezzi provides a clear, comprehensive view of your finances. This enables the platform to translate theoretical advice into practical high-net-worth investing strategies for tax planning and asset allocation.

For those who value privacy, immediate access, and complete control, Mezzi delivers fiduciary-level guidance at a lower cost compared to traditional advisor models.

When eMoney Advisor Makes More Sense

eMoney Advisor is better suited for situations requiring in-depth expertise. Scenarios like multi-state estate planning, business succession strategies, charitable trust management, or coordinating the sale of a private company often demand the insights of a trained professional to interpret and implement the platform’s outputs effectively.

This platform also appeals to investors who need accountability. If you’re unlikely to act on recommendations without guidance or prefer a "done-for-you" approach, eMoney’s advisor-led model - where a professional handles monitoring, flags changes, and guides you through decisions - may justify the added expense.

Ultimately, the choice depends on your lifestyle, financial goals, and how much involvement you want in the planning process.

FAQs

Is Mezzi read-only, or can it move money in my accounts?

Mezzi operates as a read-only platform, meaning it can securely link to your financial accounts through APIs without the capability to move or manage your funds. This setup ensures that you maintain complete control over your financial assets at all times.

What accounts can I link to Mezzi (401(k), IRA, brokerage, etc.)?

You can connect accounts such as 401(k), IRA, brokerage, and joint accounts to Mezzi with read-only access via Plaid and Finicity. This setup allows you to see your entire financial picture in one place without needing to transfer any funds.

When should I use Mezzi versus accessing eMoney through an advisor?

Mezzi provides advisor-level insights, AI-powered recommendations, and allows you to maintain full control over your accounts. It delivers real-time, tailored advice on tax strategies and asset allocation, but it doesn’t handle trades automatically - keeping you in charge of every decision.

On the other hand, eMoney, when paired with an advisor, offers a guided planning experience. This includes professional support for comprehensive financial and estate planning. If you value expert assistance, eMoney might be the right fit. However, if you prefer to manage your finances independently, Mezzi could be the better option.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.