How do you balance risk and return when investing? Modern Portfolio Theory (MPT), introduced by Harry Markowitz in 1952, focuses on creating portfolios that optimize returns for a given level of risk. Instead of picking individual stocks, MPT emphasizes how investments work together within a portfolio. Its key ideas include:

- Risk vs. Return: Higher returns often come with higher risk, measured by volatility.

- Diversification: Mixing assets with low or negative correlations may reduce overall risk.

- Efficient Frontier: A graph showing the best return possible for each level of risk.

While MPT has limitations - like assuming rational investors and stable correlations - it remains a widely used framework. Tools like Mezzi's AI platform aim to simplify applying MPT by analyzing portfolios, identifying overlaps, and customizing diversification strategies. Keep reading to learn how MPT works and how it might help you manage your investments.

Modern Portfolio Theory | a Step-by-Step Guide

What Modern Portfolio Theory Is Built On

Asset Correlation Impact on Portfolio Risk Reduction

Modern Portfolio Theory (MPT) is grounded in three core principles that guide the construction of portfolios aimed at balancing risk and reward. By understanding these principles, you can shift from focusing solely on individual investments to building a portfolio that works as a cohesive whole.

Risk and Return: The Fundamental Trade-Off

At its heart, MPT suggests that higher potential returns come with greater risk. Risk is measured as volatility, represented by variance or standard deviation, while expected return is calculated as the weighted average of an asset's returns. Instead of looking at investments one by one, MPT evaluates how each asset impacts the overall risk and return of the portfolio.

The theory assumes that investors generally prefer to avoid risk. They are willing to accept higher volatility only if it comes with the promise of higher expected returns. Based on this, MPT allows you to either aim for the highest possible return for a given level of risk or minimize risk while targeting a specific return. Diversification plays a crucial role in achieving this balance. Modern investors often leverage AI tools for smarter portfolio diversification to identify these non-obvious asset relationships.

Diversification and Asset Correlations

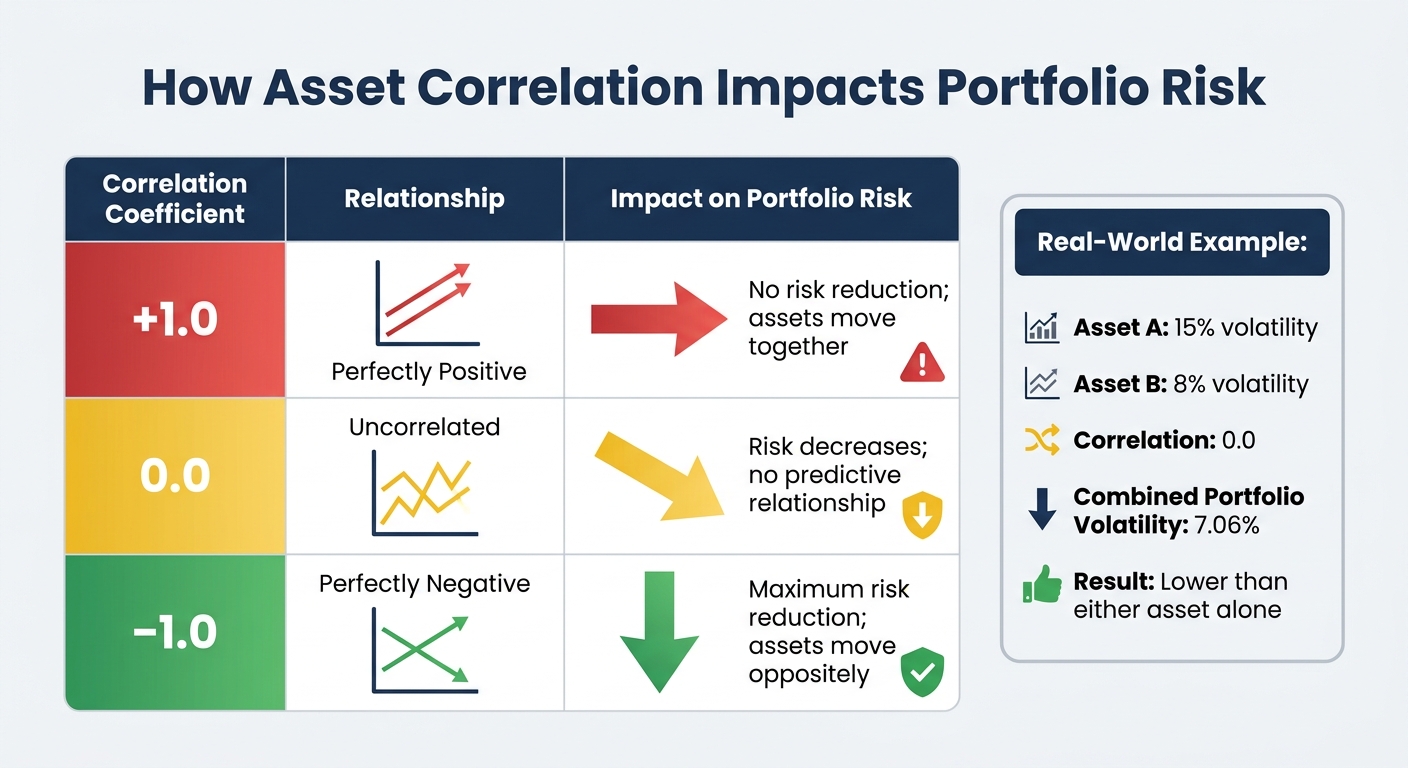

Diversification is a key tool for reducing risk without necessarily lowering expected returns. By combining assets that are not perfectly correlated, you can reduce the overall risk of your portfolio to a level below the weighted average of the individual risks. The degree to which assets move together - or their correlation - is central to this idea. Correlation values range from –1.0 (completely opposite movements) to +1.0 (moving in perfect sync).

| Correlation Coefficient | Relationship | Impact on Portfolio Risk |

|---|---|---|

| +1.0 | Perfectly Positive | No risk reduction; assets move together. |

| 0.0 | Uncorrelated | Risk decreases; no predictive relationship. |

| –1.0 | Perfectly Negative | Maximum risk reduction; assets move oppositely. |

For instance, a December 2025 study showed that combining an asset with 15% volatility and another with 8% volatility at zero correlation could produce a portfolio with just 7.06% volatility - lower than either asset alone. To apply this, consider pairing assets with low or negative correlations, such as U.S. Treasuries and small-cap value stocks. This principle directly ties into the concept of the Efficient Frontier.

The Efficient Frontier

The efficient frontier is a visual representation of MPT’s goal: optimizing a portfolio to achieve the best possible return for a given level of risk. On this graph, risk (measured by standard deviation) is plotted on the x-axis, while expected return is shown on the y-axis. Portfolios that sit on the curve are considered optimal, offering the best return for their level of risk. Anything below the curve reflects a portfolio that may carry unnecessary risk without adequate compensation.

The Global Minimum Variance portfolio, located at the far left of the frontier, represents the point of lowest possible risk. Risk-averse investors might aim for this area, while those willing to take on more volatility may choose portfolios further to the right. The efficient frontier also serves as a benchmark - if your portfolio falls below the curve, it may indicate that you’re not maximizing your potential returns for the level of risk you’re taking on. AI portfolio optimization tools can help determine the specific asset allocations needed to achieve an efficient mix, but it’s important to regularly rebalance your portfolio as asset values and correlations change over time.

How to Build a Portfolio Using MPT

Modern Portfolio Theory (MPT) offers a structured way to build a portfolio that aligns with your financial objectives and comfort with risk. By following a few key steps, you can create a strategy that adapts to your evolving financial needs.

Step 1: Assess Your Risk Tolerance and Define Goals

Start by evaluating how much risk you’re comfortable taking, both from a financial and emotional perspective. Factors like your age, income, and investment timeline will influence this, as will your personal reaction to market downturns. For example, consider how you might feel if your portfolio lost 20% of its value in a single month. If that thought feels overwhelming, you may want to lean toward a more cautious approach.

Next, outline your financial goals. Are you saving for a short-term expense, like a home down payment in three years? Or are you focused on a long-term goal, such as retirement in 30 years? These objectives will help determine the level of return you need and the time horizon for your investments. In MPT, risk is typically measured using standard deviation, which reflects how much an asset’s price tends to fluctuate. This gives you a clear, data-driven way to understand and plan for risk.

Step 2: Select and Allocate Assets

Once you’ve determined your risk tolerance and goals, the next step is choosing your investments and deciding how to allocate them. Begin by identifying the types of assets you’re willing to include, such as stocks, bonds, real estate, or commodities. Then, consider how these assets interact with one another. MPT emphasizes diversification, which involves combining assets with low or negative correlations to reduce overall portfolio volatility without necessarily sacrificing returns. For instance, pairing U.S. government bonds with growth stocks may help balance out market swings. However, it’s important to verify these correlations with actual data.

Use tools like the Sharpe ratio to evaluate your portfolio’s efficiency. A Sharpe ratio of 1.0 or higher generally indicates a good balance between risk and return, while a ratio above 2.0 is considered exceptional. This metric helps ensure that the level of risk you’re taking aligns with the returns you’re aiming for.

Step 3: Monitor and Rebalance Your Portfolio

After building your portfolio, it’s essential to keep it aligned with your goals over time. As markets fluctuate, the proportions of your investments may drift away from your original plan. For example, a portfolio initially split 60% into stocks and 40% into bonds might shift to 70% stocks and 30% bonds after a period of strong stock performance. This change could increase your exposure to risk.

To address this, rebalance your portfolio periodically by selling assets that have grown beyond their target allocation and buying those that have lagged. This process helps maintain the risk-return balance you originally set, ensuring your portfolio stays on track to meet your objectives.

Where MPT Falls Short

Modern Portfolio Theory (MPT) offers a useful framework for managing investments, but it rests on assumptions that don’t always align with how markets actually behave. Recognizing these shortcomings may help you make more informed decisions about your portfolio.

Assumptions That Don’t Match Reality

MPT assumes that investors are rational and naturally prefer lower risk for a given level of return. However, behavioral finance research suggests otherwise. Emotional decision-making, cognitive biases, and herd behavior often influence investment choices. For example, you might feel compelled to sell during a market downturn or chase stocks that are trending, even when the data advises caution.

Another key assumption is that asset returns follow a normal, bell-curve distribution. In reality, markets experience "fat tails", meaning extreme gains or losses occur far more frequently than a bell curve would predict. The 2008 financial crisis highlighted this flaw when correlations between assets surged, causing them to move in tandem. This undermined MPT’s assumption of stable correlations and reduced the benefits of diversification - right when they were needed most.

MPT also treats all volatility as equal, but most investors are more concerned with downside risk. Two portfolios with identical variance may feel very different: one with frequent small losses and another with rare but severe declines. Most people would prefer the former, yet MPT doesn’t account for this distinction. These gaps underscore the importance of strategies that can handle market volatility effectively.

Preparing for Market Swings and Surprises

To address MPT’s limitations, you might consider practical steps to better prepare your portfolio for unpredictable events. For instance, stress testing can simulate how your investments would perform under extreme conditions, like a 20% market drop. This approach gives a more realistic view than relying solely on historical averages.

Another option is exploring Post-Modern Portfolio Theory (PMPT), which prioritizes minimizing downside risk rather than total variance. This method aligns more closely with how most investors view risk.

Additionally, regular rebalancing is essential, as market movements can quickly throw your original allocation off course. Some investors also turn to strategies like Risk Parity vs 60/40, which aims to equalize the risk contribution of each asset, or Factor Investing, which focuses on specific drivers of returns, such as value or momentum. These approaches may provide alternative ways to navigate the complexities of modern markets.

Using Mezzi to Apply MPT Principles

Modern Portfolio Theory (MPT) provides a framework for constructing an optimized portfolio, and Mezzi's AI platform brings that framework to life by analyzing your entire financial picture. Without the fees associated with traditional advisors, Mezzi offers tools to provide a comprehensive view, identify hidden risks, and improve tax efficiency.

See All Your Accounts in One Place

For MPT to work effectively, you need to evaluate your portfolio as a whole. However, many investors have assets scattered across multiple accounts, such as brokerages, 401(k)s, and IRAs. Mezzi uses account aggregators like Plaid and Finicity to securely connect with over 12,000 financial institutions - including Vanguard, Fidelity, and Schwab. This integration creates a unified dashboard where you can see your total net worth and real-time asset allocation.

This consolidated view is crucial for MPT analysis. For instance, an investor with $500,000 spread across three brokers might discover a 40% overlap in tech stocks after aggregating their accounts. Unlike traditional advisors who typically work only with assets under their management, Mezzi provides a comprehensive, read-only view of all your accounts. This allows for a true portfolio-wide analysis without requiring you to transfer assets.

Find Hidden Overlaps and Improve Diversification

One of Mezzi's standout tools, Portfolio X-Ray, breaks down ETFs and mutual funds into their individual securities, helping uncover overlaps that may hinder diversification. Studies indicate that 68% of retail investors unknowingly hold duplicate assets across funds, potentially increasing portfolio volatility by 12–18% compared to MPT-optimized benchmarks.

The X-Ray tool assigns a diversification score on a 0–100 scale, using covariance analysis to measure overlap. In one example, a $1 million portfolio with three seemingly "diversified" funds revealed a 35% overlap in FAANG stocks. By replacing one fund with VXUS (an international fund), the investor reduced portfolio volatility by 12%, lowering the standard deviation from 15% to 13.2%, while maintaining an 8% expected return. This adjustment moved the portfolio closer to the efficient frontier. Dr. Alex Chen, an MPT researcher at NYU Stern, explains:

"Overlaps inflate risk without return - X-Ray quantifies this instantly."

Get Tax Guidance and Risk Alerts

Mezzi goes beyond diversification by addressing tax strategies and dynamic risk management.

While MPT emphasizes maximizing returns for a given level of risk, taxes can eat into those returns. Mezzi's AI continuously scans for tax-loss harvesting opportunities. For example, in a $300,000 taxable account, the platform might identify $12,000 in losses from ARKK to offset MSFT gains, potentially saving $2,800 in taxes for someone in a 24% tax bracket. This adjustment could increase the net return from 7.2% to 8.1%. Research from Vanguard suggests that automated tax-loss harvesting through AI tools may improve after-tax returns by 0.5–1.2% annually, which could add up to a 10–20% boost over five years.

Additionally, Mezzi monitors over 50 risk factors daily, such as Value at Risk (VaR), beta drift, and shifts in asset correlations. For instance, during a market dip in Q4 2025, the platform alerted a user to a rising correlation between equities and bonds (from 0.4 to 0.7). Acting on this insight, the user shifted 10% of their portfolio to TIPS, helping to avoid a 5% drawdown. These real-time alerts align with MPT's dynamic rebalancing principles, ensuring your portfolio remains calibrated to your target risk-return goals.

Key Takeaways

Here’s a recap of the discussion on Modern Portfolio Theory (MPT) and how Mezzi applies its principles to portfolio management.

MPT focuses on optimizing portfolios by analyzing how assets interact with one another. Its main idea is that diversification may help reduce risk without necessarily lowering returns. This groundbreaking concept, introduced by Harry Markowitz in 1952, earned him the Nobel Prize in Economic Sciences in 1990.

The theory introduces the efficient frontier, which illustrates the best possible trade-off between risk and return. Investors aim to determine their position on this curve based on their risk tolerance and adjust their portfolios through periodic rebalancing. MPT also differentiates between two types of risk: systematic risk, which impacts the entire market and cannot be eliminated, and unsystematic risk, which may be reduced through diversification.

Mezzi builds on these principles to simplify portfolio management. Its tools align with MPT by offering an integrated view of your accounts, allowing for a complete understanding of your portfolio. The Portfolio X-Ray tool highlights overlapping exposures in ETFs and mutual funds, helping identify where you might be paying duplicate fees. It also provides real-time alerts for changes in correlations and allocation drift. Additionally, Mezzi scans for tax-loss harvesting and capital gains deferral opportunities and monitors wash sale risks across accounts - insights that traditional advisors, who typically manage only specific assets, might overlook. With features like stress testing and scenario analysis, Mezzi addresses some of MPT's practical challenges while maintaining its focus on maximizing returns for a given level of risk through smarter diversification.

FAQs

How do I pick my spot on the efficient frontier?

To find your ideal position on the efficient frontier, start by evaluating your risk tolerance and investment objectives. If maintaining stability is your priority, you may lean toward a portfolio with lower risk. On the other hand, if you're open to taking on more risk in pursuit of potentially higher returns, you might aim for a portfolio further along the curve.

Tools like Excel or dedicated investment software can help you visualize different portfolio options. These tools are designed to assist in pinpointing the portfolio that may offer the best potential returns for the level of risk you're comfortable taking.

What happens to diversification when correlations jump in a crash?

When correlations increase significantly during a market crash, the ability of diversification to manage risk may weaken. In such times, many assets often move in the same direction, which can limit the protective benefits of spreading investments across various asset classes. This alignment of movement reduces the usual risk-reducing impact that a diversified portfolio might provide.

How often should I rebalance to stay near my target risk?

To keep your portfolio close to your intended risk level, consider rebalancing on a regular schedule - like once a year - or whenever your allocations shift significantly, often by about 5%. This process helps bring your investments back in line and maintain the risk profile you’re aiming for. The ideal approach depends on factors like your personal risk tolerance and current market conditions, but sticking to a consistent routine can help ensure your portfolio remains aligned with your financial objectives, even during periods of market volatility.

Disclosures:

- This content is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.

- Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.

- Savings and performance examples are hypothetical and for illustrative purposes only. Actual results will vary based on individual circumstances, portfolio composition, market conditions, and fees.

- Users should not rely solely on AI-driven tools for financial decision-making.

- Registration does not imply a certain level of skill or that the SEC has approved the company or its services.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.