Net Unrealized Appreciation (NUA) is a tax strategy that can save retirees thousands of dollars by reducing taxes on employer stock held in a 401(k). Instead of taxing the entire stock value as ordinary income during withdrawal (up to 37% or 39.6% starting 2026), NUA allows the appreciation to be taxed later at lower long-term capital gains rates (0%, 15%, or 20%). Here's how it works:

- Cost Basis: Taxed immediately as ordinary income when the stock is distributed.

- Appreciation: Taxed as long-term capital gains when sold later.

- Eligibility: You must meet IRS rules, including a lump-sum distribution and qualifying events like retirement or reaching age 59½.

This strategy is ideal for employer stock with a low cost basis and high appreciation. However, it requires careful planning to avoid mistakes, such as rolling the stock into an IRA or failing to meet lump-sum distribution rules. NUA may not be suitable for everyone, especially if the cost basis is high or if you expect a lower tax bracket in retirement. For those who qualify, it can significantly reduce taxes and preserve retirement savings.

Don’t Miss The NUA Election for Company Stock in Your 401(k)

How NUA Works and What You Need to Qualify

Navigating Net Unrealized Appreciation (NUA) requires meeting several IRS criteria. Knowing these rules is crucial if you want to make the most of your retirement tax strategy while sidestepping costly mistakes.

Events That Qualify You for NUA

To utilize NUA, you must experience one of four qualifying events: separation from service (leaving your job), reaching age 59½, total disability (if self-employed), or death. For example, if you leave your job at age 52, you may still qualify once you turn 59½. However, leaving early could result in a 10% penalty on the cost basis - unless your separation occurred during or after the year you turned 55.

The Lump-Sum Distribution Rule

A key requirement for NUA is taking a lump-sum distribution, meaning you must withdraw the entire vested balance from all similar qualified plans with your employer in the same calendar year. For instance, if you have a 401(k) and a profit-sharing plan with the same employer, both accounts need to be fully distributed by December 31 of that year.

"The IRS enforces these rules strictly. If you do not meet one of the criteria - for example, if you fail to distribute all assets within one tax year - your NUA election will be disqualified, and you would owe ordinary income taxes and any penalty on the entire amount of the company stock distribution." - Mitch Pomerance, Vice President and Financial Consultant, Fidelity Investments

To avoid complications, start the process early. Check with your plan’s service department to confirm that no late contributions, like prior-year employer matches, are added after your distribution. These could jeopardize the lump-sum status. Also, ensure that employer stock is transferred in-kind as actual shares - selling the stock for cash will forfeit any NUA benefits. Non-stock assets can be rolled into a traditional IRA to maintain tax deferral.

Which Accounts and Stocks Qualify

NUA applies only to specific employer-sponsored plans, such as 401(k)s, ESOPs, profit-sharing plans, and stock-bonus plans. IRAs and 403(b) plans are not eligible. Additionally, only employer stock qualifies - mutual funds containing company stock do not.

The stock must be shares of your employer's company. If your plan administrator tracks cost basis by individual share lots, you can apply NUA selectively to shares with the lowest cost basis while rolling higher-basis shares into an IRA. This approach can help maximize your tax savings.

| Requirement | What Qualifies | What Doesn't Qualify |

|---|---|---|

| Account Types | 401(k), ESOP, Profit-Sharing, Stock-Bonus Plans | IRAs, 403(b) plans |

| Qualifying Events | Separation from service, age 59½, disability, death | Partial distributions initiated by the account holder |

| Distribution Method | In-kind transfer of actual shares | Cash distributions after selling stock |

| Timing | All plans of the same type must be emptied in one calendar year | Distributions spread across multiple years |

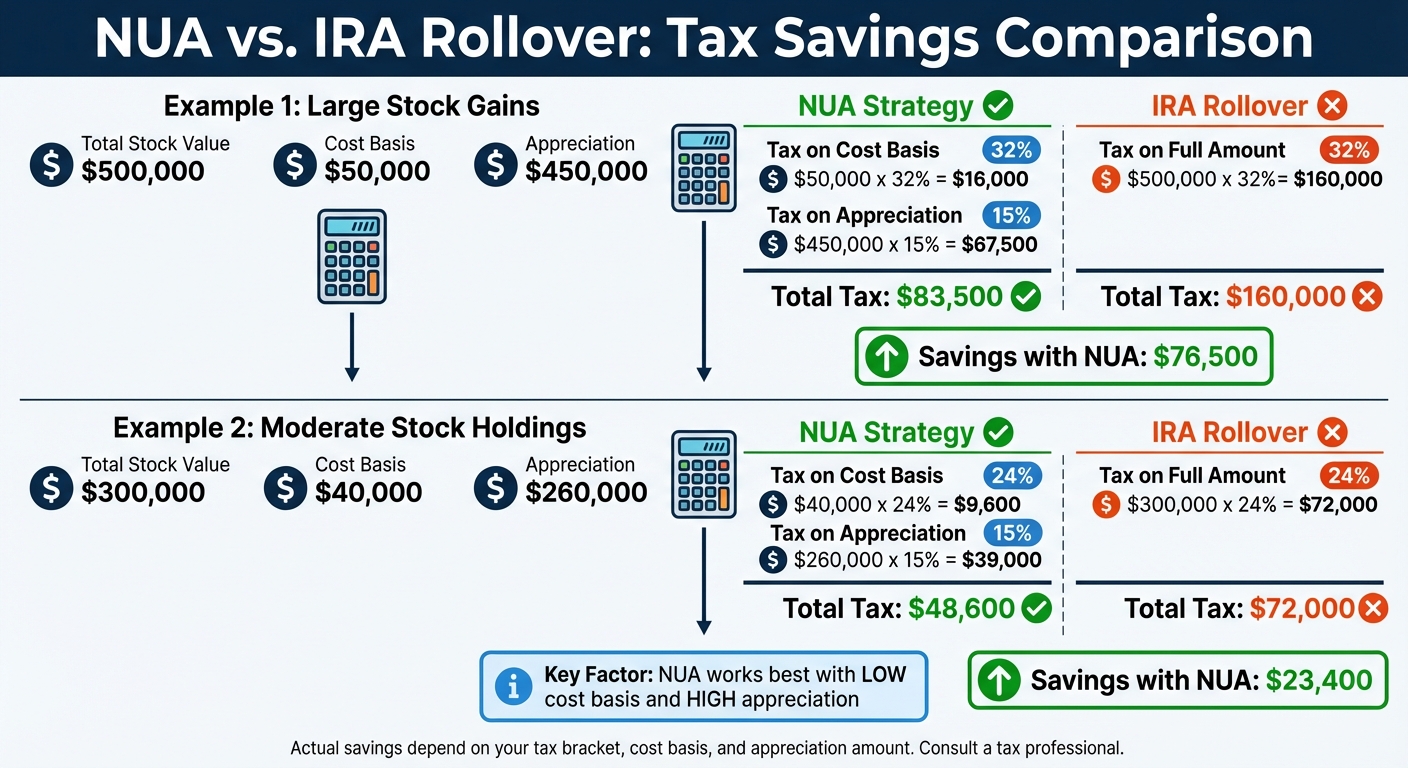

When NUA Saves You Money: Real Examples

NUA vs IRA Rollover Tax Comparison Calculator

Example: Large Stock Gains Lead to Big Tax Savings

Let's break down how NUA (Net Unrealized Appreciation) can lead to substantial tax savings. Imagine you hold $500,000 in employer stock with a $50,000 cost basis. Using the NUA strategy, you'd pay 32% on the $50,000 basis, which comes to $16,000, and then 15% on the $450,000 appreciation, totaling $67,500. That adds up to $83,500 in taxes. If you instead rolled the stock into an IRA and withdrew it later, you'd pay 32% ordinary income tax on the full $500,000, resulting in $160,000 in taxes. That's a savings of $76,500 with NUA.

Here’s another scenario: you own $300,000 in company stock with a $40,000 cost basis. With NUA, you would pay 24% on the $40,000 basis ($9,600) and 15% on the $260,000 appreciation ($39,000), bringing your total tax bill to $48,600. If you rolled it into an IRA and withdrew later at 24%, you'd pay $72,000. The NUA approach saves you $23,400.

While these examples highlight the potential benefits, NUA isn't a one-size-fits-all solution. It works best when the cost basis is low compared to the total stock value.

When NUA Might Not Work for You

The key to NUA's effectiveness is having a low cost basis relative to the stock's value. Let’s look at Irwin, a 65-year-old executive in December 2025. He had $500,000 in company stock with $250,000 in NUA. Since he was earning $500,000 annually, he was in the 35% tax bracket. If Irwin had chosen the NUA strategy, he would have faced an immediate $92,500 tax bill, bumping him into the 37% bracket. Instead, he rolled the stock into an IRA and waited until retirement, when his tax bracket dropped to 22%. By doing so, he only paid $55,000 in taxes on the same amount through Required Minimum Distributions (RMDs).

"Like Roth conversions, NUAs should be realized primarily because you want to pay a lower tax rate on assets in the future by paying some taxes in the present." - Mitch Pomerance, Vice President and Financial Consultant, Fidelity Investments

NUA is most effective when the cost basis is low, and the stock has seen significant appreciation. If the cost basis is high, the immediate tax on the basis might outweigh the long-term capital gains savings. Additionally, you’ll need enough liquid funds outside your retirement account to cover the ordinary income tax due on the cost basis in the year of distribution.

For those planning to hold investments for decades, the tax-deferred growth in an IRA might ultimately provide more benefits than the tax rate savings from NUA. The longer the time horizon, the more compounding can work in favor of leaving assets in a tax-deferred account.

Tax Comparison Tables

| Strategy | Immediate Tax on Basis | Tax on Appreciation | Total Tax Bill |

|---|---|---|---|

| IRA Rollover | $0 (Deferred) | $36,000 (24% on $130k at withdrawal) | $36,000 |

| NUA (Cash Out) | $6,000 (24% of $25k) | $15,750 (15% of $105k) | $21,750 |

Assumes $130,000 of stock with a $25,000 basis, a 24% tax bracket for ordinary income, and a 15% long-term capital gains rate.

| Factor | Favors NUA | Favors IRA Rollover |

|---|---|---|

| Cost Basis | Low (High appreciation) | High (Low appreciation) |

| Current Tax Bracket | Low or Moderate | Very High |

| Future Tax Bracket | Expected to be Higher | Expected to be Lower |

| Time Horizon | Short to Medium | Long (20+ years) |

| Liquidity | High (Can pay tax now) | Low (Need to defer tax) |

Advanced NUA Tactics and Planning Tips

These advanced strategies can help fine-tune your NUA approach, improving tax efficiency and protecting your retirement savings.

How to Lower Your Cost Basis

Reducing the cost basis of your employer stock before distribution can significantly cut down your tax liability. If your 401(k) plan allows after-tax contributions, you can use these to offset the taxable basis of your company shares. When you take a lump-sum distribution, the after-tax contributions directly lower the taxable cost basis of the stock transferred to your brokerage account, reducing the ordinary income tax owed.

For example, Tony made a $40,000 after-tax contribution to his 401(k), which lowered the taxable cost basis of his employer stock. When he distributed the stock, the $40,000 contribution reduced his taxable ordinary income from $50,000 to just $10,000. This allowed him to transfer $1 million in stock to a brokerage account while paying immediate taxes on only $10,000.

This approach works best if your 401(k) plan permits "Mega Backdoor" after-tax contributions. Review your plan details to confirm eligibility and consider making these contributions in the years leading up to retirement for maximum benefit. Once you've reduced your cost basis, the next step is deciding when to sell your stock.

When to Sell Your Stock After Distribution

After lowering your cost basis, timing your stock sale becomes critical for managing taxes. The NUA portion of your distribution is always taxed as a long-term capital gain, even if you sell the stock immediately after the distribution. However, any additional appreciation after the stock leaves your 401(k) is taxed according to standard capital gains rules. To qualify for long-term capital gains on this post-distribution growth, you must hold the stock for more than one year; otherwise, it will be taxed at ordinary income rates.

"NUA is generally treated as long-term capital gain when sold even if you sell soon after distribution (the 'long-term' characterization applies to the NUA element itself)." - Pioneer Wealth Management Group

Holding a large portion of your portfolio in employer stock can be risky. Many retirees choose to sell enough shares immediately to cover the tax on the cost basis and then gradually sell the remaining shares to manage capital gains exposure. Selling during "income gap" years - after retirement but before Social Security or RMDs begin - can help you take advantage of a lower tax bracket.

Avoiding the 3.8% Net Investment Income Tax

Once you've decided when to sell, it’s essential to consider strategies to avoid extra tax burdens. The 3.8% Net Investment Income Tax (NIIT) does not apply to the NUA portion of your distribution because it's treated as a distribution from a qualified retirement plan. However, any growth in the stock's value after it has been moved to a brokerage account is subject to the NIIT if your income exceeds $200,000 (single filers) or $250,000 (married filing jointly).

"The 3.8% Net Investment Income Tax surtax doesn't apply to NUA. However, it does apply to any increase in the company stock's value after it's taken out of your 401(k)." - Rocky Mengle, Attorney

To minimize NIIT exposure, consider selling the stock shortly after distribution to limit post-distribution growth. You can also time the distribution for years when your Modified Adjusted Gross Income (MAGI) is lower, keeping you below the NIIT thresholds. Households in the highest tax bracket (37%) are particularly affected by the NIIT on post-distribution gains, making careful timing and quick sales even more important.

Common NUA Mistakes to Avoid

To make the most of the tax advantages offered by the NUA strategy, avoiding common errors is crucial. Even a small mistake can strip away the benefits, leaving you with a hefty ordinary income tax bill on gains that could otherwise qualify for long-term capital gains rates.

Don't Roll Employer Stock into an IRA

Transferring employer stock into an IRA is a critical misstep. Doing so permanently eliminates the NUA benefit, meaning all future withdrawals will be taxed as ordinary income, no matter how much the stock appreciates. To retain the NUA tax advantage, the IRS requires an "in-kind" distribution of the stock to a taxable brokerage account. This means the actual shares, not their cash equivalent, must be transferred.

The proper method involves moving the employer stock to a taxable account while rolling over other plan assets, like mutual funds or cash, into an IRA. Confirm with your plan administrator that in-kind distributions are allowed. Keep in mind, you'll need to pay ordinary income tax on the cost basis of the stock at the time of the transfer, as there’s no automatic withholding.

Also, remember that a complete, lump-sum distribution is necessary to preserve the NUA benefit.

Taking Partial Distributions Disqualifies NUA

The IRS enforces a strict rule: to qualify for NUA, you must distribute your entire employer plan balance within a single calendar year. This means your account balance must be zero by December 31. Partial distributions or loans taken before completing a lump-sum NUA distribution will disqualify you from the tax benefit.

It’s essential to ensure that company stock is distributed as actual shares to a brokerage account, while non-stock assets are rolled into an IRA - both actions must occur within the same calendar year to meet the lump-sum requirement.

Keep Accurate Cost Basis Records

Accurate record-keeping of the cost basis is essential. The NUA amount must be reported in Box 6 of Form 1099-R. However, not all plan administrators track cost basis the same way. Some use an average cost per share, while others track the cost of individual lots. The latter method allows you to apply the NUA strategy selectively to shares with the lowest cost basis, potentially reducing your immediate tax burden.

"For record-keeping purposes, do not mix NUA stock with other company stock in the same brokerage account. Doing so could make it very difficult to get the tax break." - Investopedia

To simplify tracking, use a separate brokerage account exclusively for NUA stock. Mixing these shares with other company stock can make it nearly impossible to maintain clear cost basis records. Once the stock is in your brokerage account, you’re responsible for keeping the records up to date for tax reporting. If your plan administrator allows, consider identifying and distributing only the shares with the lowest cost basis to minimize the immediate tax hit.

Conclusion: Using NUA to Build Retirement Wealth

The Net Unrealized Appreciation (NUA) strategy offers a way to save tens of thousands of dollars in taxes during retirement. By converting what would otherwise be taxed as ordinary income - at rates as high as 37% (or 39.6% starting in 2026) - into long-term capital gains taxed at 0%, 15%, or 20%, you can hold onto a much larger portion of your retirement savings. This approach not only cuts your immediate tax bill but also creates opportunities for long-term growth in your retirement portfolio.

Retirees with highly appreciated employer stock have seen tax savings ranging from $14,250 to $50,000 when compared to a standard IRA rollover. Beyond these immediate benefits, moving employer stock out of your 401(k) also reduces future Required Minimum Distributions (RMDs), which can help lower your overall tax bracket during retirement. For instance, in a December 2025 Fidelity case study, a retiree named Tony saved an estimated $12,459 annually in taxes by leveraging the NUA strategy.

However, timing and execution are critical. Once you roll employer stock into an IRA, the NUA advantage is permanently lost. To preserve these benefits, it’s crucial to meet IRS requirements and complete a lump-sum distribution. This means ensuring your plan allows for in-kind transfers, having cash on hand to cover taxes on the cost basis, and executing the entire distribution within the same calendar year.

For those with a significant amount of employer stock and a low cost basis, NUA can play a key role in retirement planning. While it requires careful planning and precise execution, this strategy is a powerful way to reduce lifetime taxes and protect your wealth. By incorporating NUA into your retirement plan, you can better preserve your savings and reduce your tax burden over the long term.

FAQs

How do I know if my employer stock’s cost basis is low enough for NUA to help?

To figure out if NUA might work in your favor, start by comparing the current market value of your employer's stock to its cost basis (the original purchase price). NUA tends to be most advantageous when the stock has grown significantly in value. Why? Because the difference between the cost basis and the current value (the NUA) could be taxed at lower capital gains rates instead of higher ordinary income tax rates.

For instance, if you purchased a stock for $10 and it’s now worth $25, the $15 difference represents the NUA. This portion may qualify for those lower tax rates, potentially offering you substantial savings.

What steps should I follow to complete an in-kind NUA distribution without breaking the rules?

To complete an in-kind NUA distribution, here’s what you need to do:

- Confirm eligibility: Make sure your 401(k) plan qualifies and you're fully vested.

- Trigger a distribution event: This could happen if you leave your job or reach age 59½.

- Request in-kind distribution: Move your employer stock directly to a taxable brokerage account.

- Pay taxes: You'll owe ordinary income tax on the stock's cost basis and capital gains tax on any appreciation.

It's wise to consult a tax advisor to navigate this process and ensure everything is handled correctly.

What happens to NUA if I sell the shares right away versus holding them longer?

Selling the shares right away means the NUA (Net Unrealized Appreciation) amount will be taxed as long-term capital gains. On the other hand, holding onto the shares could allow them to increase in value, with any additional gains also taxed at capital gains rates. But keep in mind, this strategy comes with risks - like market volatility and possible shifts in tax laws - that could affect your overall tax benefits.Disclosures:

- This content is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.

- Tax laws and regulations are subject to change and individual circumstances may vary. Consult a qualified tax or financial professional before making any decisions regarding Net Unrealized Appreciation (NUA) or retirement plan distributions.

- Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.