If you’re deciding between a 457(b) and a 401(k), here’s the quick answer: focus on your 401(k) if your employer offers a match, then consider your 457(b) for additional savings or early retirement flexibility.

Here’s why:

- 401(k): Employer matches don’t count toward your personal contribution limit, allowing you to grow your savings faster. However, withdrawals before age 59½ usually incur a 10% penalty, unless exceptions apply.

- 457(b): Offers penalty-free withdrawals once you leave your job, regardless of age. It’s ideal if you plan to retire early or need flexibility. But, employer contributions (if any) count toward your total contribution limit.

If you qualify for both plans, you can contribute up to $49,000 in 2026 if under 50, or more with catch-up options. Use your 401(k) for matched contributions first, then maximize your 457(b) to boost savings or prepare for early access to funds.

1. 457(b) Plan

Eligibility and Contribution Limits

The 457(b) plan is designed for state and local government employees - such as teachers, police officers, and firefighters - as well as employees of certain tax-exempt nonprofit organizations. Interestingly, independent contractors working for eligible employers can also participate, which sets it apart from most 401(k) plans.

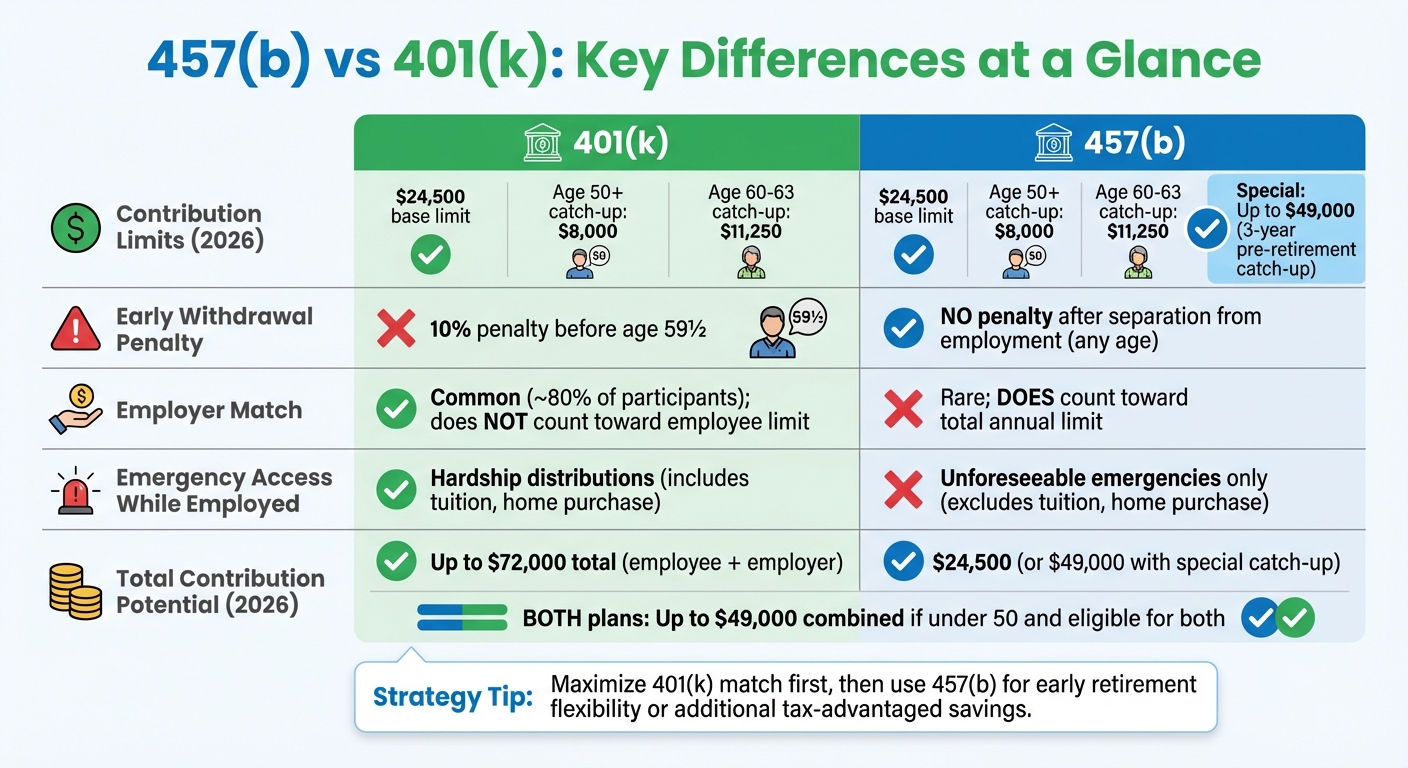

For 2026, the contribution limit is $24,500, an increase from $23,500 in 2025. Employees aged 50 and older can contribute an additional $8,000. Those between the ages of 60 and 63 have access to a "super" catch-up contribution of $11,250. Additionally, some plans allow a three-year pre-retirement catch-up provision. This means, if you're within three years of retirement, you can contribute up to double the standard limit - $49,000 in 2026. However, you must choose between the age 50+ catch-up and the three-year pre-retirement catch-up since you can't use both at the same time.

These contribution rules are essential to understanding the tax benefits and withdrawal options tied to the plan.

Tax Benefits and Implications

Contributions to a 457(b) plan reduce your taxable income, and the investments grow tax-deferred until you make withdrawals, which are taxed as ordinary income. Some plans also offer a Roth option, allowing after-tax contributions with the benefit of tax-free withdrawals later.

Withdrawal Rules and Flexibility

One standout feature of the 457(b) plan is its flexible withdrawal rules. Once you leave your job, you can withdraw funds without facing the early withdrawal penalties that applies to most 401(k) plans before age 59½. However, if you roll over funds from a 401(k), 403(b), or IRA into your 457(b) plan, those rolled-over funds will still be subject to the 10% penalty if withdrawn before age 59½.

Employer Contributions

Employer contributions to 457(b) plans are uncommon. This is a notable difference compared to 401(k) plans, where nearly 80% of participants receive employer matches. When employers do contribute to a 457(b) plan, their contributions count toward the $24,500 limit. In contrast, 401(k) plans allow employer contributions to exceed the employee contribution limit.

2. 401(k) Plan

Eligibility and Contribution Limits

The 401(k) plan is a cornerstone retirement savings option for employees in for-profit organizations and eligible nonprofit workers. However, independent contractors are typically excluded from participating in these plans, as they are designed specifically for employees.

For 2026, the individual contribution limit is $24,500, aligning with the 457(b) base limit. If you're 50 or older, you can contribute an additional $8,000 as a catch-up contribution. Employees aged 60 to 63 have the option to make a "super catch-up" contribution of $11,250 instead of the standard $8,000. There's an important caveat: if your earnings in 2025 exceed $150,000, any catch-up contributions in 2026 must go into a Roth account.

The total contribution limit, which combines employee and employer contributions, is $72,000 for 2026, or $80,000 if you're 50 or older. One major advantage of 401(k) plans is that employer contributions don't count against your personal $24,500 limit. This feature can significantly enhance your overall retirement savings. Up next, we'll look at how these limits tie into tax planning.

Tax Benefits and Implications

Traditional 401(k) contributions lower your taxable income for the year, and your investments grow tax-deferred until you retire. When you take withdrawals, the money is taxed as ordinary income. Many plans also offer a Roth 401(k) option, which allows for tax-free withdrawals in retirement. Starting in 2024, Roth 401(k) accounts are no longer subject to Required Minimum Distributions (RMDs) during your lifetime. This change gives you more flexibility and control over how and when you access your retirement funds. Next, we'll dive into the rules for withdrawing from 401(k) accounts.

Withdrawal Rules and Flexibility

If you withdraw money from your 401(k) before age 59½, you'll generally face a 10% early withdrawal penalty, unless you qualify for specific exceptions. Exceptions may include hardships like medical expenses or avoiding eviction, but even then, the penalty often applies. Once you reach age 73, you must begin taking Required Minimum Distributions (RMDs) from traditional 401(k) accounts. Failing to take an RMD results in a hefty 25% penalty on the amount you were required to withdraw.

Employer Contributions

One of the most appealing aspects of 401(k) plans is employer matching, which essentially provides you with "free money." These contributions do not count against your personal contribution limit. For example, your employer might match dollar-for-dollar up to 3% of your salary or contribute $0.50 for every $1.00 you save. About 80% of participants benefit from employer matches, though the funds are often subject to vesting schedules that can range from three to six years. With careful planning, these contributions can be a powerful tool in building your retirement savings portfolio. AI-driven tools can also help you align your strategy with changing market conditions.

401(k) vs. 457: Which One Is Better?

Eligibility, Contributions, and Tax Benefits Compared

457(b) plans cater to employees of state and local governments, certain nonprofit organizations, and even independent contractors, while 401(k) plans are designed for private-sector employees. These distinctions play a big role in determining which plan aligns with your retirement goals.

Both plans share a contribution limit of $24,500, with an additional $8,000 catch-up for those aged 50 and older. For individuals aged 60–63, the catch-up limit increases to $11,250. A unique feature of 457(b) plans is their special three-year catch-up provision, allowing contributions of up to $49,000 in the three years leading up to retirement. However, you can only use one catch-up option at a time, so you’ll need to select the one that benefits you most.

Another key advantage of 457(b) plans is the ability to "stack" contributions. Since the IRS classifies 457(b) plans as nonqualified deferred compensation, their contribution limits are treated separately from those of 401(k) plans. This means that if you’re eligible for both plans, you could contribute up to $49,000 in 2026 if you’re under 50 - or as much as $69,500 if you’re aged 60–63 and maximize contributions to both.

Tax expert William Perez explains, "The IRS allows you to save to both a 401(k) and 457(b) plan at the same time, because a 457(b) plan is a nonqualified plan".

Both plans share similar tax benefits. Traditional contributions reduce your taxable income and grow tax-deferred, while Roth options allow for tax-free withdrawals. However, starting January 1, 2026, high earners will be required to allocate catch-up contributions to a Roth account.

The main difference lies in how employer contributions are handled. In a 401(k), employer matches don’t count toward your personal contribution limit - they’re added on top. In contrast, employer contributions to a 457(b) plan count toward the total deferral limit. Since employer matches are uncommon in 457(b) plans, 401(k) plans generally provide more value when an employer match is offered. The next section will explore employer contributions in greater detail.

Withdrawal Rules and Employer Match Compared

457(b) vs 401(k) Retirement Plans Comparison Chart

One of the biggest differences between 401(k) and 457(b) plans lies in how and when you can access your funds without penalties. For 401(k) plans, withdrawing money before age 59½ comes with a 10% early withdrawal penalty. On the other hand, 457(b) plans allow you to make penalty-free withdrawals at any age after you leave your job or retire. However, it's important to note that while 457(b) withdrawals avoid the penalty, they are still taxed as ordinary income.

When you're still employed, accessing money from these plans is more restrictive. A 401(k) plan may allow hardship withdrawals for specific expenses like tuition or buying a home. In contrast, 457(b) plans typically limit withdrawals to unforeseeable emergencies, which are narrowly defined and do not include tuition or home purchases.

Employer contributions also set these plans apart. Employer matching is a common feature of 401(k) plans, and these contributions don’t count against your personal deferral limit. In contrast, employer contributions to 457(b) plans - if they’re even offered - are much less common and do count toward the total annual deferral limit.

Here’s a quick breakdown of these differences:

"The standout feature of a 457 plan is its withdrawal flexibility. You can withdraw funds penalty-free once you separate from service with your employer, regardless of your age."

– Jessica Smith, Customer Success, Gerald

"If your employer offers a match on the 401(k), it behooves you to contribute up to the match at a minimum."

– Robin Hartill, CFP, The Motley Fool

| Feature | 401(k) Plan | 457(b) Plan |

|---|---|---|

| Early Withdrawal Penalty | 10% penalty before age 59½ | No 10% penalty after separation from employment |

| Employer Match | Common; does not count toward employee limit | Rare; counts toward the total annual deferral limit |

| Emergency Access | Hardship distributions (may include tuition/home purchase) | Withdrawals for unforeseeable emergencies (excludes tuition/home purchase) |

Up next, we’ll dive into the overall advantages and drawbacks of each plan.

Pros and Cons

When comparing these retirement plans, it's clear each has its own strengths and weaknesses, making them suitable for different retirement strategies. Knowing these differences can help you decide how to allocate your retirement savings.

The 457(b) plan shines with its penalty-free withdrawals upon leaving your job, which is especially helpful if you plan to retire before turning 59½. It also offers enhanced catch-up contributions for those nearing retirement and broader eligibility criteria, which can be a plus for certain workers.

On the other hand, the 401(k) plan excels in boosting retirement savings through employer matching. These matching contributions don’t count toward your $24,500 personal contribution limit in 2026, allowing for significant savings growth. As SoFi explains, "A 401(k) has an edge when it comes to regular contributions, since employer matches don't count against your annual contribution limit". Additionally, 401(k) plans come with ERISA protection, providing federal safeguards that governmental 457(b) plans don’t offer.

However, there are trade-offs. Relying on a 457(b) plan means missing out on employer matching, as any matching contributions count toward your annual limit, reducing the amount you can personally contribute. Meanwhile, 401(k) plans are less flexible when it comes to early withdrawals from your 401(k) or IRA, as funds are generally inaccessible without penalties before age 59½. They also lack the special pre-retirement catch-up contributions that 457(b) plans provide.

For those eligible for both plans, stacking contributions can maximize savings. Since the IRS treats 457(b) and 401(k) limits separately, you could defer up to $49,000 in 2026 if you’re under 50.

Ultimately, these differences highlight how each plan caters to different retirement goals, helping you decide which route best supports your financial future.

Conclusion

Deciding between a 457(b) and a 401(k) comes down to your retirement plans, tax considerations, and whether your employer provides a matching contribution.

If your employer offers a match on 401(k) contributions, that should be your first focus. As Robin Hartill, CFP, explains:

"If your employer offers a match on the 401(k), it behooves you to contribute up to the match at a minimum. Even if you expect to retire early, paying a 10% early withdrawal penalty on a 100% free match is still a good deal".

Start by securing your 401(k) match, and then, if you anticipate retiring or changing jobs before age 59½, allocate additional savings to your 457(b). This plan allows penalty-free withdrawals upon job separation, giving you more flexibility.

For those fortunate enough to access both plans and contribute the maximum amount, a combination strategy can work wonders. In 2026, individuals under 50 can contribute up to $49,000 across both accounts. This approach provides an opportunity to maximize tax-advantaged savings.

Understanding the nuances of these plans helps you make smarter decisions about your retirement savings. Tools like Mezzi can provide tailored, AI-driven insights based on your financial accounts. With its guidance, you can optimize contributions, manage Roth conversions, and map out your retirement timeline. Whether you have questions about balancing a 457(b) and a 401(k) or other financial strategies, you can get quick, actionable advice to align with your goals.

FAQs

Can I max out both a 401(k) and a 457(b) in the same year?

Yes, if you qualify for both plans, you can contribute the maximum allowable amount to both a 401(k) and a 457(b) within the same year. This approach can be an effective way to boost your retirement savings while leveraging the distinct advantages each plan provides.

What happens if I roll a 401(k) into a 457(b) and withdraw early?

Rolling over a 401(k) into a 457(b) can help sidestep the 10% early withdrawal penalty usually tied to 401(k) withdrawals made before age 59½. That said, penalty-free withdrawals from a 457(b) are typically permitted only after you leave your job. To keep the tax benefits intact, make sure the rollover process is done properly. Keep in mind, withdrawing early while you're still employed might be limited by the specific rules of the 457(b) plan.

How do I choose the best catch-up option for a 457(b)?

If you're deciding on the best catch-up option for a 457(b) plan, start by determining if you're within three years of retirement. This is key because it could make you eligible for the special catch-up rule, which allows you to contribute more than the standard limit. Take a close look at your current contributions, compare them to the plan's limits, and reach out to your plan administrator or a financial advisor to confirm your eligibility. This approach can help you maximize your retirement savings during those crucial final years before retiring.

Disclosures:

- This content is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.

- Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.

- Savings and performance examples are hypothetical and for illustrative purposes only. Actual results will vary based on individual circumstances, portfolio composition, market conditions, and fees.

- Registration does not imply a certain level of skill or that the SEC has approved the company or its services.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.