A large paper gain may turn into a large tax bill when you sell. But for some taxable assets, holding until death may reset the cost basis to market value at death, which may wipe out past capital gains for heirs under current U.S. tax rules.

Here’s the short version:

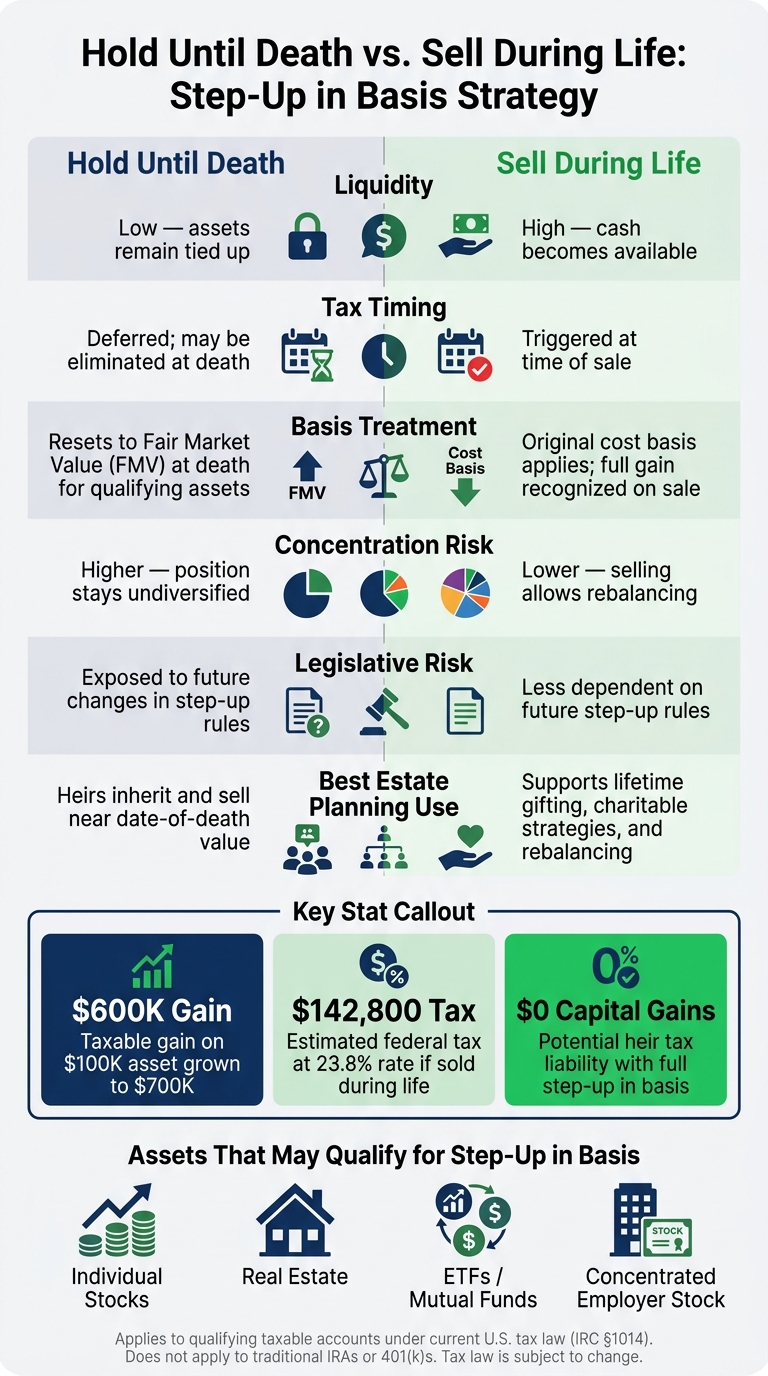

- If you bought an asset for $100,000 and it’s now worth $700,000, a sale may trigger tax on a $600,000 gain.

- At a 23.8% federal rate, that tax may be about $142,800, before state tax.

- If that same asset qualifies for a step-up in basis at death, an heir’s new basis may become $700,000.

- If the heir sells near that value, there may be little or no capital gain to report.

That sounds simple. But there are limits:

- This usually applies to taxable accounts, not IRAs or 401(k)s.

- Ownership matters. Joint accounts, community property, and trusts may get different treatment.

- Waiting for a step-up may mean taking on market risk, concentration risk, and law-change risk.

- Gifting during life often passes along the old basis instead of resetting it.

Step-Up in Basis: The Estate Planning Strategy Too Many People Miss

Quick Comparison

| Topic | Hold Until Death | Sell During Life |

|---|---|---|

| Capital gains tax timing | May be deferred until death | May apply at sale |

| Basis | May reset to FMV at death for qualifying assets | Original basis usually stays in place |

| Liquidity | May stay tied up | Cash may become available |

| Portfolio risk | May stay higher if the asset is concentrated | May fall after trimming or selling |

| Retirement accounts | Step-up usually does not apply | Withdrawal tax rules still apply |

| Law risk | Depends on future rules staying similar | Less tied to future step-up rules |

I’d look at this as a tax idea, not a stand-alone plan. It may fit people with highly appreciated taxable assets, low cash needs, and heirs likely to inherit the asset. But the tax upside may need to be weighed against the cost of waiting.

What Step-Up in Basis Means Under Current U.S. Tax Law

Under current U.S. tax law, inherited assets generally get a new cost basis equal to their fair market value (FMV) on the date of death. In many cases, that means lifetime appreciation may not be taxed to heirs. That reset may change the tax result in a big way.

How the Basis Reset Works

The rule is pretty straightforward. If a parent bought stock for $50,000 and it was worth $300,000 at death, the heir’s basis becomes $300,000. If the heir sells right away at that same value, there may be no capital gain to report. Put simply, the built-in gain is removed from the heir’s capital gains calculation.

Ownership structure then affects how much of that reset a beneficiary may actually receive.

Which Assets Commonly Qualify

Most appreciated assets may qualify, including individual stocks, ETFs, mutual funds, real estate, and concentrated employer stock. But there’s a catch: ownership may determine how much basis resets.

The same rule generally applies across several common taxable assets.

| Asset Type | Original Basis Example | Date-of-Death Basis (FMV) | Common Planning Use Case |

|---|---|---|---|

| Individual Stocks | $50,000 | $300,000 | May reduce gain for heirs |

| Real Estate | $200,000 | $850,000 | May reset years of appreciation |

| ETFs / Mutual Funds | $100,000 | $250,000 | Often used for long-term holdings |

| Concentrated Employer Stock | $20,000 | $150,000 | Often used for highly appreciated shares |

Ownership structure also matters:

- Sole ownership generally gets a full step-up on 100% of the asset value.

- With joint tenancy with right of survivorship (JTWROS), typically only the decedent’s 50% share gets stepped up.

- Community property may allow both halves of a jointly held asset to receive a full step-up.

- Assets in an irrevocable trust usually do not receive a step-up.

The next question is when holding instead of selling may make sense.

When Holding Until Death Is the Better Tax Move

Selling may not always be the best move. When an unrealized gain is large and you don't need the cash, holding may reduce the tax burden for heirs. The key question isn't whether a step-up helps. It's whether waiting may be worth the tradeoff.

High-Gain Assets Where Selling Now Is Costly

The bigger the unrealized gain, the more a basis reset at death may matter for your heirs. A few examples make that easier to see:

- ETF held long-term: Original cost $100,000, now worth $400,000. Selling today at a combined 25% long-term capital gains rate, federal plus state, would trigger $75,000 in tax and leave $325,000 to reinvest. If the asset is held until death, the heir's basis becomes $400,000, so the full $300,000 gain disappears for income tax purposes.

- Rental property: Bought for $300,000 with $60,000 of depreciation claimed, leaving an adjusted basis of $240,000. If the property is now worth $700,000, the taxable gain on sale, including depreciation recapture taxed up to 25%, may easily produce a tax bill above $120,000 to $130,000. If held until death, the heir's basis resets to $700,000, removing both the appreciation and the accumulated depreciation recapture for income tax purposes.

- Concentrated employer stock: A $2,000,000 position with a $500,000 original basis has $1,500,000 in embedded gains. Selling half may trigger about $225,000 in tax at a 30% combined rate. Holding until death and passing the shares to heirs removes capital gains tax on that full $1,500,000 of lifetime appreciation.

Estate Planning Cases Where This Strategy Fits

This approach may fit best when the goal is to preserve wealth rather than spend it: use other assets first, direct high-gain assets to heirs who may sell, and keep appreciating taxable assets in the estate.

Spending from other assets first may be one of the more practical approaches. Retirees whose living costs are covered by Social Security, pensions, or retirement account withdrawals may be able to leave high-gain taxable positions untouched. By drawing from cash, Roth IRAs, or lower-gain holdings first, they may preserve the most appreciated assets for heirs to inherit with a stepped-up basis.

Coordinating which assets go to which heirs may matter too. Highly appreciated taxable assets may be a better fit for heirs who plan to sell soon after inheriting, while tax-deferred retirement accounts or life insurance may be used for other heirs.

Which accounts hold which assets may also shape the outcome. Long-term growth assets with high gain potential in taxable accounts may be prime candidates for step-up planning, while Roth or tax-deferred accounts may be a better fit for assets where the step-up matters less.

For concentrated positions that feel too risky to hold outright, exchange funds may offer a way to diversify without an immediate taxable sale, while keeping step-up treatment on the fund interest at death.

How Mezzi Can Help You Analyze the Tradeoff

Deciding whether to hold or sell may require a full view of your finances. Mezzi connects taxable and retirement accounts in one place, which may make it easier to spot concentrated positions, overlap, and where high-gain assets sit in taxable accounts versus accounts where step-up doesn't apply.

From there, Mezzi may help you think through a few scenarios: what selling now may cost in taxes, what a gradual trimming approach over several years may look like, and what the step-up benefit may be worth to your heirs. Mezzi's analysis focuses on your goals, not product sales.

The tradeoff is that waiting may also carry real costs.

Limits, Exceptions, and the Cost of Waiting

Hold Until Death vs. Sell During Life: Step-Up in Basis Tax Strategy Comparison

This approach may reduce taxes for heirs, but only if the facts line up. The asset generally needs to be owned at death, qualify under IRC §1014, and be included in the gross estate. If one of those pieces is missing, the tax result may change and the expected tax break may not happen.

What You Give Up by Not Selling Earlier

The big tradeoff is time. Waiting for a step-up may mean taking on market risk before any tax break arrives.

If someone holds an appreciated asset for a future basis reset, that person may also be accepting the chance that the asset drops in value first. A concentrated stock position or rental property may lose value before death. And money tied up in one stock or one property may not be available for other uses, such as a more diversified mix, income-focused holdings, or options some people may view as lower risk.

Cases Where the Tax Result May Differ

The same basic idea may lead to very different tax results depending on the account type and the way the asset is owned. Not every asset gets the same treatment.

Retirement accounts - traditional IRAs and 401(k)s - do not receive a step-up. Beneficiaries may owe ordinary income tax on withdrawals from inherited IRAs, so holding those accounts until death may not remove the tax bill. Assets gifted during life usually keep the original basis, which means the recipient may still owe tax on the full built-in gain when the asset is sold.

Ownership matters too. In joint tenancy, only the decedent's share usually gets a step-up. In community property states, both halves of a jointly owned asset may step up at the first spouse's death. Assets held in some irrevocable trusts may not qualify, since the decedent may no longer be treated as the owner at death.

Future law changes could limit the benefit. Recent proposals have discussed limiting or removing step-up for large estates, or taxing unrealized gains at death above certain thresholds. None of those proposals has become law. Even so, people who hold large unrealized gains for decades may be relying on current rules staying in place when the transfer happens.

Hold Until Death vs. Sell During Life: A Side-by-Side Comparison

The choice usually turns on tax timing, access to cash, and risk.

| Factor | Hold Until Death | Sell During Life |

|---|---|---|

| Liquidity | Low | High |

| Tax Timing | At death | On sale |

| Basis Treatment | Resets to FMV at death for qualifying assets | Original cost basis applies; gain recognized on sale |

| Concentration Risk | Higher | Lower |

| Legislative Risk | Exposed to future changes in step-up rules | Less dependent on future step-up rules |

| Estate Planning Use | Best when heirs will inherit and sell | Supports lifetime gifting, charitable strategies, and rebalancing |

This path may fit best when liquidity needs are already covered and heirs are in line to inherit the asset. If those facts aren't there, selling earlier may make more sense for some people.

Conclusion: Use Step-Up in Basis as Part of a Broader Plan

The better question may not be whether step-up in basis works. It may be whether it fits your full plan.

Step-up in basis may reduce taxes for heirs on qualifying taxable assets, but that may matter only when it lines up with your risk level, cash needs, and estate plan.

The clearest cases may involve appreciated taxable assets you don’t genuinely need to sell: a long-held stock position, an investment property, or a low-cost-basis ETF portfolio. If selling now may trigger a large federal and state tax bill, and if you have other resources for living expenses, holding for a future step-up may make financial sense. But if tax savings are the only reason to hold, that tradeoff may look less attractive. Holding just for tax reasons may backfire if your portfolio ends up too concentrated or if market losses hit at the wrong time.

Some people look at step-up in basis only after weighing retirement needs, concentration risk, embedded gain, and estate goals.

That tradeoff may be easier to judge when you can see all of your accounts in one place. Mezzi can link your accounts, flag concentration risk, and model hold-versus-sell outcomes for your largest positions.

Here are the main points.

Key Points to Remember

- Step-up in basis resets qualifying inherited assets to fair market value at death, which may eliminate capital gains tax on prior appreciation. It may fit best with highly appreciated taxable assets that do not need to be sold soon.

- Holding purely for tax reasons can be risky if it leaves you overconcentrated in one stock or property, or short on cash.

- Step-up does not apply to traditional IRAs, 401(k)s, and similar retirement accounts. In those accounts, heirs may still owe ordinary income tax on withdrawals no matter when death occurs.

- Tax law can change. Step-up in basis has been a recurring target of reform proposals, so a plan that depends only on today’s rules staying in place may carry legislative risk.

- Use step-up in basis as one tool in a broader plan, alongside diversification, liquidity, estate documents, and your goals.

FAQs

Who benefits most from a step-up in basis strategy?

People who hold assets with large unrealized gains and may not need sale proceeds right away may get the most use from this approach.

It may also come up in estate planning. When heirs inherit assets, they may receive a cost basis reset to fair market value at death, which may reduce or even eliminate deferred capital gains taxes. That may be especially relevant for concentrated stock positions, real estate, or other large investments.

How does ownership affect the step-up I might get?

Ownership structure may affect whether an asset gets a step-up in basis - and how much may pass to heirs.

With sole ownership, the full asset usually gets a step-up at death. With joint ownership, such as tenancy in common, only the deceased owner’s share generally gets the step-up.

There’s also a state-law wrinkle. In community property states, married couples may receive a full step-up on both halves of community property. That’s a very different setup from a gift.

Gifted assets usually keep the original cost basis. So the person who receives the asset may later face higher capital gains taxes if they sell it.

When is selling before death a better choice?

Selling before death may make more sense if you need liquidity for your lifestyle or current financial goals, since a step-up in basis generally requires you to keep the asset.

It may also make sense if you expect to be in a lower tax bracket later, may use tax-loss harvesting to offset gains, or want to gift assets during your lifetime to reduce your taxable estate.Disclosures:

- This content is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.

- Tax laws are subject to change and individual circumstances may vary. Consult a qualified tax or financial professional before making decisions based on this information.

- Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.