When planning for retirement, your investment approach matters. You can choose between target-date funds, which adjust automatically as you age, or building your own portfolio, which gives you more control but requires effort. Here's the quick breakdown:

- Target-Date Funds: Simple, automated, and beginner-friendly. They adjust risk levels over time but may not fully align with your unique financial situation. Average fees are around 0.29% (as of 2024).

- Custom Portfolios: Tailored to your goals, risk tolerance, and tax strategy. They require hands-on management or tools like Mezzi, which simplifies the process without high advisory fees.

Key Takeaway:

- Choose target-date funds for a hands-off approach with built-in adjustments.

- Opt for a custom portfolio if you want flexibility, tax optimization, and control over your investments. This includes automated tax loss harvesting to improve after-tax returns.

The right choice depends on your preferences, time commitment, and financial complexity. Let’s explore both options in detail.

DIY 3-Fund vs. Target Date Fund | Detailed Comparison

What Are Target-Date Funds?

A target-date fund is an investment option that combines stocks, bonds, and cash into a single portfolio. These funds are tied to a specific year - the "target date" - which aligns with when you expect to retire. For instance, if you aim to retire in 2050, you'd likely pick a fund labeled "Target 2050."

The beauty of these funds lies in their simplicity. Once you choose a fund based on your retirement year, it automatically adjusts its investments over time. This hands-off approach has made target-date funds a popular choice in workplace 401(k) plans. By 2023, 98% of retirement plans offering a Qualified Default Investment Alternative opted for a target-date fund.

These funds are often the default option in 401(k) plans, thanks to the Pension Protection Act of 2006. This legislation allows employers to invest contributions into target-date funds when employees don’t actively select another option.

How Target-Date Funds Work

Target-date funds rely on a "glide path" to manage your investments. Early in your career, the fund leans heavily on stocks to maximize growth. As you get closer to retirement, it shifts toward bonds and cash to reduce risk and protect your savings.

Glide paths come in two main types:

- "To retirement" glide paths aim for a conservative allocation by the target date.

- "Through retirement" glide paths maintain some stock exposure even after the target date, with an average equity allocation of around 44%.

Fund managers handle all the rebalancing, making these funds a true "set-it-and-forget-it" option.

Benefits of Target-Date Funds

The main draw of target-date funds is their simplicity. They handle diversification, rebalancing, and risk management for you in a single step.

"Target date funds provide an all-in-one fund option that can help individuals stay invested, disciplined, and on track to help meet their financial goals." - Angus Stewart, Director of Investment Product Management, Fidelity Investments

Another perk is diversification. These funds are usually structured as a "fund of funds", meaning they hold thousands of securities across different asset classes, industries, and regions. Plus, costs have dropped significantly. The average expense ratio for target-date funds fell to 0.29% in 2024, down from 0.55% in 2015. Providers like Vanguard offer options with expense ratios as low as 0.08%, making them a cost-effective choice compared to building your portfolio from scratch.

While target-date funds simplify investing, they do have limitations, which we’ll explore further when discussing more personalized strategies like Mezzi’s.

Drawbacks of Target-Date Funds

Despite their advantages, target-date funds have some downsides. A key issue is their one-size-fits-most approach. They don’t consider your unique financial picture, such as a pension, other retirement accounts, or your personal risk tolerance.

"If your preference is to have full transparency into each position you own, a target date fund might not be the best option." - Paige Morandi, Financial Consultant, Fidelity

Another challenge is managing investments across multiple accounts. If you hold a target-date fund in your 401(k) but also have other investments, you could end up with overlapping holdings or an asset allocation that doesn’t match your overall risk profile.

Expense ratios can also vary widely. While some funds are as low as 0.08%, others, like the Fidelity Freedom 2050 Fund (FFFHX), charge 0.75%, which is nearly ten times higher than Vanguard’s comparable option. Additionally, some funds keep up to 60% of their assets in stocks at retirement, which could expose you to sequence-of-returns risk. A market downturn early in retirement could hurt your savings, especially if the fund’s glide path doesn’t account for your withdrawal strategy or other income sources.

Next, we’ll dive into what it takes to build your own portfolio.

What Does Building Your Own Portfolio Involve?

Building your own portfolio puts you in the driver’s seat. Instead of relying on a pre-made fund, you decide which investments to choose and when to adjust them. While this requires more effort upfront, it allows you to tailor your investments to fit your financial goals and circumstances.

"Your financial goals are the 'why' of investing." - Marci McGregor, Head of Portfolio Strategy, Merrill and Bank of America Private Bank

To start, assess your risk tolerance and decide how to allocate your money among stocks, bonds, and cash in a way that matches your financial timeline. Asset allocation is a major factor in determining how your investments perform over time.

Steps to Build Your Own Portfolio

Once you’ve set your goals and determined your risk tolerance, the next step is diversification. Spread your investments across different industries, company sizes, and even regions of the world. You can choose between individual stocks and bonds or pooled options like ETFs and mutual funds. Then, decide if you want to actively manage your investments (aiming to outperform the market) or take a passive approach using index funds that track a benchmark.

Tax efficiency is another key consideration. For example, placing tax-inefficient assets like taxable bonds in accounts such as a 401(k) or IRA can help reduce your tax burden. On the other hand, tax-efficient options like index funds are better suited for taxable accounts. Over time, these strategies can save you significant money. Finally, make it a habit to review and rebalance your portfolio annually. This involves selling assets that have grown too much and buying those that have lagged to maintain your desired allocation.

Benefits of a Custom Portfolio

One of the biggest advantages of building your own portfolio is control. You can shape your investments to match your unique financial situation, personal values, and tax needs. For instance, if you’re passionate about sustainable investing, you can focus on companies that align with those principles. If managing capital gains is a priority, you have the flexibility to do so.

Custom portfolios also tend to come with lower costs, especially when using low-cost index funds. Warren Buffett famously proved this point when his choice of a Vanguard S&P 500 index fund earned an 8.5% average annual return over a decade, significantly outperforming hedge funds that managed only 2.4%.

"The S&P 500 Index Fund is the one to use... It's the one I've told the trustee for my wife to put 90% of the funds I leave her in to." - Warren Buffett, CEO, Berkshire Hathaway

Transparency is another perk. A simple portfolio using just three funds - a total U.S. stock fund, a total international stock fund, and a broad U.S. bond fund - provides a clear view of where your money is going. This clarity allows you to adjust your risk level as your financial goals evolve, rather than being locked into a predetermined path.

Challenges of Managing Your Own Portfolio

Of course, managing your own portfolio comes with its challenges. It requires time, research, and discipline. You’ll need to stay on top of market trends, monitor your portfolio’s performance, and rebalance consistently. Missing just the 10 best market days during the 2010s would have cut your returns nearly in half - 95% versus 190% for those who stayed fully invested. This underscores the importance of staying calm and avoiding impulsive decisions during market swings.

"Time itself is one of your best assets." - Marci McGregor, Head of Portfolio Strategy, Merrill and Bank of America Private Bank

Managing multiple accounts can also get complicated. If you have a 401(k), IRA, and taxable brokerage account, coordinating your asset allocation across all of them can feel overwhelming. Tools like Mezzi, which use AI to streamline portfolio management, can help reduce the manual work and make the process more manageable.

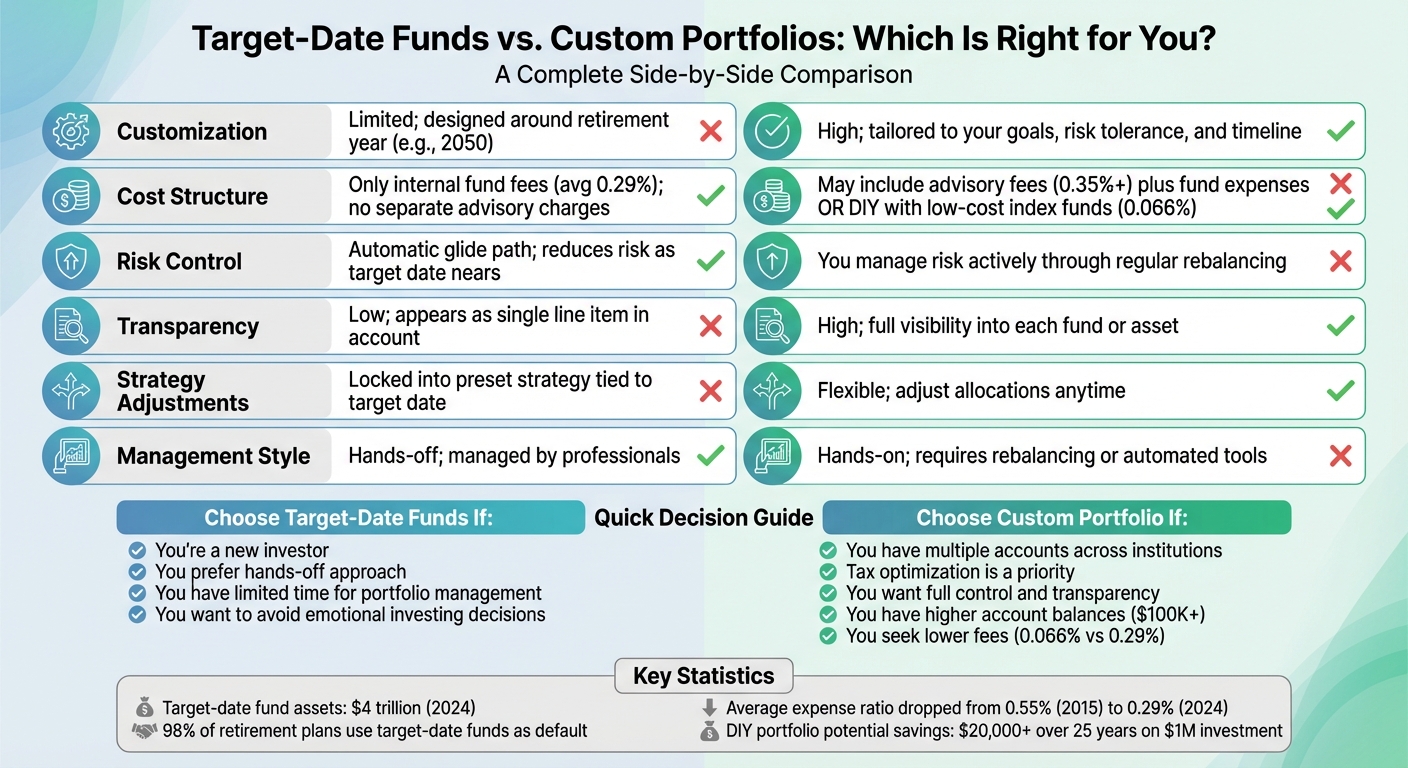

Target-Date Funds vs. Custom Portfolios: Side-by-Side Comparison

Target-Date Funds vs Custom Portfolios: Complete Comparison Guide

Here’s a closer look at how target-date funds stack up against custom portfolios. Your decision largely depends on how much control you want, your sensitivity to investment fees, and how involved you wish to be in managing your investments.

Comparison Table

| Factor | Target-Date Fund | Custom Portfolio |

|---|---|---|

| Customization | Limited; designed around a specific retirement year (e.g., 2050) | High; tailored to your unique goals, risk tolerance, and timeline |

| Cost Structure | Only internal fund fees; no separate advisory charges | May include advisory fees (e.g., 0.35% for balances over $25,000) in addition to fund expenses |

| Risk Control | Follows an automatic glide path, reducing risk as the target date nears | You manage risk actively through regular rebalancing |

| Visibility | Low; appears as a single line item in your account | High; full transparency into each fund or asset in your portfolio |

| Strategy Adjustments | Locked into the fund's preset strategy tied to the target date | Flexible; you can tweak allocations or change strategies whenever needed |

| Management Style | Hands-off; managed by professionals as a one-fund solution | Hands-on; requires manual rebalancing or automated tools to stay on track |

This table highlights the key differences between the two approaches, helping you weigh the pros and cons based on your preferences and financial objectives.

When Target-Date Funds Make Sense

Target-date funds are perfect for those who prefer simplicity and automation over active investment management. They work well for beginners, busy professionals, or anyone who might make impulsive decisions during market swings. Let’s take a closer look at who benefits most from this hands-off strategy.

The numbers speak for themselves: target-date fund assets hit an all-time high of $4 trillion in 2024. This milestone highlights their popularity as a dependable, low-effort investment choice.

Who Should Use Target-Date Funds

New investors can greatly benefit from the ease of target-date funds. If you're just starting out and still figuring out the complexities of different asset classes, these funds handle the heavy lifting for you. Plus, with the average expense ratio dropping to just 0.29% in 2024 (down from 0.55% in 2015), they offer an affordable way to access professional management without needing to become an expert investor yourself.

Busy professionals often find these funds to be a lifesaver. Whether you’re juggling a demanding career, raising a family, or simply don’t have the bandwidth to dive into investment research, target-date funds take care of everything. They follow a structured glide path, starting with a stock-heavy allocation in your early years and gradually shifting to about 44% stocks by retirement.

Investors prone to emotional decisions can also find value here. Market swings can tempt even the best of us to make rash moves, but target-date funds help keep those impulses in check. For instance, during the market turbulence of early 2024, these funds had smaller losses compared to the S&P 500. Their automated approach helps shield you from panic selling during downturns or chasing trends during rallies. As Meredith Dietz, Senior Staff Writer at Lifehacker, explains:

"These funds essentially put your retirement portfolio on autopilot, eliminating the need for constant monitoring and rebalancing."

When a Custom Portfolio Is the Better Option

Target-date funds might be a good fit for investors who prefer a hands-off approach, but they can fall short when financial situations become more intricate. If you have assets in multiple accounts, prioritize tax efficiency, or want more control over your investments, a custom portfolio could provide better outcomes. Let’s break down who benefits most from this tailored approach.

Who Should Build Their Own Portfolio

A custom-built portfolio can cater to specific needs and goals, offering flexibility that generic target-date funds often lack.

Investors managing assets across multiple institutions are prime candidates for a custom portfolio. If you’re juggling several retirement and taxable accounts, relying on a single target-date fund won’t give you a coordinated strategy. A custom approach lets you allocate assets strategically across all accounts, ensuring a more cohesive financial plan.

Tax-conscious investors have a lot to gain from building their own portfolios. With a custom strategy, you can implement asset-location techniques that target-date funds can’t match. For example, you might place tax-inefficient assets like bonds in a 401(k) or IRA to shield interest income from taxes, while keeping tax-efficient equity funds in a taxable brokerage account. Plus, the cost savings add up. A DIY three-fund Vanguard portfolio has an average expense ratio of about 0.066%, compared to 0.08% for a Vanguard Target Retirement Fund. Over 25 years, this 0.014% difference could mean over $20,000 in additional value on a $1,000,000 initial investment.

Investors with higher account balances or unique risk preferences may find target-date funds too limiting. These funds often become overly conservative as retirement nears, shifting heavily into bonds and money markets. But if you need more growth to sustain a retirement that could last 30 years or more, this approach might not work. As Dave Ramsey bluntly states:

"Target date funds... won't give you the growth you need to support you through 30-plus years of retirement".

Warren Buffett’s famous 10-year bet, which ended in 2017, highlights this point. His low-cost S&P 500 index fund delivered an average annual return of 8.5%, far outpacing actively managed hedge funds, which averaged just 2.4%. His advice?

"The S&P 500 Index Fund is the one to use... It's the one I've told the trustee for my wife to put 90% of the funds I leave her in to".

Those seeking transparency and control will appreciate the clarity a custom portfolio offers. You’ll know exactly how much you’re holding in U.S. stocks, international stocks, and bonds. This visibility allows you to adjust allocations based on your life circumstances rather than a preset timeline. Plus, you can avoid the double layer of fees that target-date funds often carry - the fund’s expense ratio and the fees of its underlying investments.

How Mezzi Makes Custom Portfolio Management Easier

Managing your own portfolio gives you the freedom to tailor your investments, but juggling multiple accounts can get tricky. Mezzi steps in to simplify the process, offering insights and guidance comparable to a financial advisor - without the hefty 1% annual fee that could cost you over $1 million over 30 years.

Mezzi connects securely to your accounts through read-only access using Plaid and Finicity. This setup lets the platform view your complete financial landscape - 401(k)s, IRAs, and taxable brokerage accounts - without requiring you to transfer assets or give up control. Unlike traditional advisors who are limited to the assets they manage, Mezzi provides a full-picture assessment of everything you own, no matter where it's held. Here’s a closer look at some of Mezzi’s standout features.

Portfolio X-Ray and Overlap Detection

Mezzi’s Portfolio X-Ray feature digs deep to uncover hidden overlaps in your investments. It highlights duplicate stock exposures across ETFs and mutual funds, giving you a clearer understanding of your portfolio’s true composition. As Shuping, Founder of Summer AI, noted:

"Mezzi's X-Ray feature allowed me to uncover exposure to stocks I didn't realize I had."

This tool doesn’t just flag stock overlaps - it also reveals overlapping fee exposures, which can quietly erode returns. Warren Buffett has long warned about the dangers of high fees, especially when comparing active management to low-cost index funds. Mezzi helps you sidestep these pitfalls.

Tax Optimization Guidance

Tax efficiency is critical for maximizing returns, and Mezzi offers tools to help you keep more of what you earn. By identifying tax-loss harvesting opportunities, the platform can potentially boost your returns by 1%–2% annually - equating to $10,000–$20,000 per year on a $1 million portfolio. It also tracks wash sale risks across all connected accounts, ensuring you don’t unintentionally forfeit tax benefits by purchasing similar securities within a 30-day period.

Additionally, Mezzi provides advice on asset location, such as holding tax-inefficient bonds in tax-advantaged accounts while placing tax-efficient equity funds in taxable accounts. This level of precision goes far beyond what a single target-date fund can offer.

Retirement Planning Based on Your Actual Accounts

Forget generic retirement calculators with hypothetical inputs - Mezzi uses real data from your connected accounts to deliver personalized retirement projections. You can ask specific questions about your timeline, contributions, or spending, and Mezzi provides tailored answers on demand.

As Mike, a product manager, shared:

"Mezzi gives me answers and ideas when I need them, no matter what time of day or how big or small the question."

This instant access eliminates the long waits often associated with traditional advisors, enabling you to make informed decisions when it matters most.

Conclusion: Choosing the Right Approach for Your Situation

The choice between target-date funds and custom portfolios boils down to your preferred balance of simplicity and control in managing your investments. Target-date funds are a hands-off option, taking care of diversification, rebalancing, and gradually adjusting risk as you age. They’re great if you want to avoid the emotional pitfalls of investing and aim for near-market returns. However, this ease of use often comes with an average fee of 0.51% and limited flexibility in strategy.

On the other hand, custom portfolios give you more control and can be more cost-effective. By using low-cost index funds with expense ratios around 0.08%, you can create a strategy tailored to your tax situation, retirement goals, and account structure. Advances in digital tools have also made managing custom portfolios much easier. This is where Mezzi steps in to enhance your experience.

Mezzi bridges the gap between the flexibility of custom portfolios and the guidance of traditional advisors. With tools like Portfolio X-Ray, tax optimization, and data-driven retirement planning, Mezzi helps you fine-tune your investments without the need to transfer assets or pay hefty advisory fees.

Ultimately, the right choice depends on your situation. If you’re a busy investor focused on simplicity, target-date funds might be the way to go. But if you have multiple accounts, prioritize tax efficiency, or want more control without the high costs of traditional advisors, Mezzi’s tailored approach to custom portfolios could be the ideal solution.

FAQs

How do I pick the right target-date year?

When picking a target-date year, think about when you want to retire or achieve your financial goal. Factor in your current age, expected retirement age, and how much risk you’re comfortable taking. Not sure? Choosing a year a bit further out can give you some wiggle room to handle market ups and downs. These funds automatically adjust their mix of investments as the target year gets closer, keeping you aligned with your plan.

When is a custom portfolio worth the extra work?

A personalized portfolio can be a smart choice if your financial goals, risk tolerance, or personal preferences demand strategies that go beyond generic solutions. Tools powered by AI, like Mezzi, make it easier to design portfolios that adjust to both market shifts and your unique requirements. This approach is especially helpful when aiming for precise tax strategies, fine-tuned asset allocation, or integrating behavioral insights into how you invest.

How can Mezzi help me rebalance and reduce taxes?

Mezzi's AI-powered platform takes the guesswork out of managing your portfolio. It identifies tax-loss harvesting opportunities to help reduce your tax burden. Plus, it uses dividends and contributions to rebalance your portfolio strategically - without triggering unnecessary taxes.

The platform also excels in managing tax-deferred accounts like IRAs and 401(k)s, enabling frequent rebalancing to keep your investments aligned with your goals. By optimizing asset locations and prioritizing tax efficiency, Mezzi helps you grow your wealth smarter and faster.

Disclosures:

- This content is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.

- Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.

- Savings and performance examples are hypothetical and for illustrative purposes only. Actual results will vary based on individual circumstances, portfolio composition, market conditions, and fees.

- Registration does not imply a certain level of skill or that the SEC has approved the company or its services.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.