Want to save on taxes while keeping your portfolio on track? Here's how:

Tax-optimized rebalancing is a smart way to adjust your investments while minimizing taxes. With tighter tax rules in 2025, these strategies can help you grow your wealth more efficiently:

- Use Tax-Deferred Accounts: Rebalance frequently without triggering taxes in accounts like IRAs or 401(k)s.

- Plan Asset Locations: Place high-tax investments (like bonds) in tax-advantaged accounts and growth assets in taxable ones.

- Leverage Cash Flow: Use dividends and new contributions to rebalance without selling.

- Harvest Tax Losses: Sell underperforming investments to offset gains and reduce your tax bill.

- Combine Rebalancing Methods: Mix time-based and threshold-based strategies to align with tax planning.

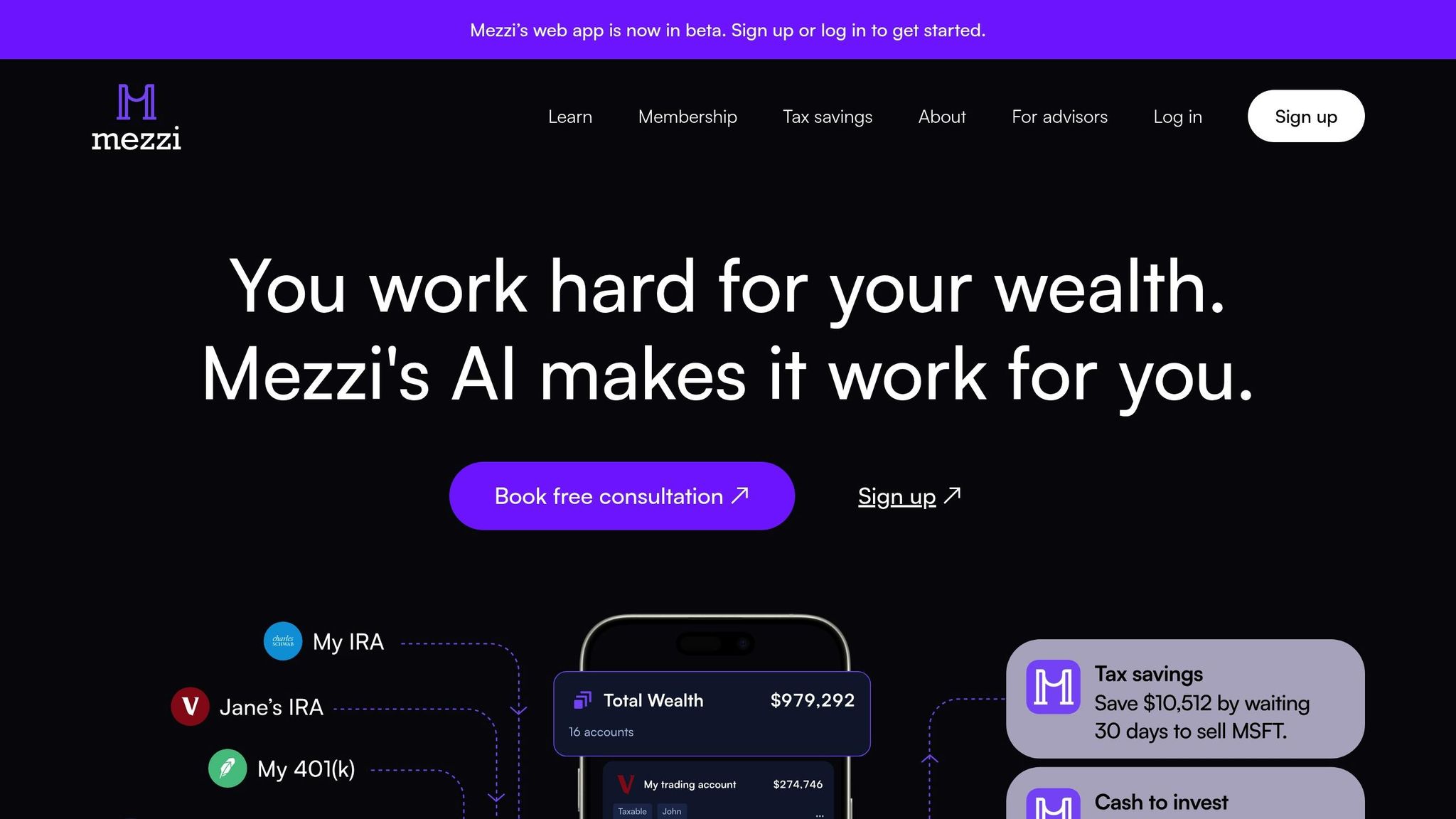

Quick Tip: Saving just 1% on taxes could add $186,877 to your retirement fund over time. Tools like Mezzi’s AI platform can simplify this process by identifying tax-saving opportunities and avoiding costly mistakes.

Ready to optimize your portfolio? Let’s dive into the details.

How to Rebalance Your Portfolio Before 2025

When preparing for the new year, it is essential to understand how to minimize taxes when realizing gains to protect your long-term returns.

Main Tax-Optimized Rebalancing Methods

Building on the earlier discussion of tax impacts, these methods help fine-tune your rebalancing strategy for 2025. The goal? Align your portfolio effectively while keeping taxes in check.

Time vs Threshold Rebalancing

Time-based rebalancing works on a set schedule, like annual or semi-annual reviews. This predictable approach reduces frequent trading and limits potential tax events. For example, scheduling rebalancing in December can align with year-end tax-loss harvesting opportunities.

Threshold rebalancing, on the other hand, kicks in when asset allocations stray beyond specific percentages - often a 5% deviation from target levels. This method reacts to major market shifts, helping manage portfolio risk and creating chances for tax savings.

| Rebalancing Method | Key Advantage | Tax Consideration |

|---|---|---|

| Time-Based | Predictable scheduling | Easier to plan within tax years |

| Threshold | Risk control | Takes advantage of market changes |

| Combined | Balanced approach | Blends scheduled and flexible tax strategies |

Combined Rebalancing Methods

This approach blends the strengths of both time-based and threshold methods, addressing the 2025 tax considerations in a practical way.

How to implement it:

- Set annual rebalancing dates that align with your tax planning schedule.

- Define a 5% deviation threshold for individual asset classes.

- Use tax-loss harvesting when threshold breaches occur.

- Factor in holding periods to qualify for long-term capital gains rates.

For example, if a stock exceeds your threshold mid-year, weigh the tax impact of rebalancing without selling immediately versus waiting for the scheduled date. This approach balances flexibility with structure, helping you reduce tax-inefficient trades while keeping your portfolio aligned with your investment goals. It also ensures you’re prepared to act on tax-saving opportunities without increasing your risk.

Tax-Deferred Account Strategies

Tax-deferred accounts allow you to adjust your portfolio without triggering taxes until withdrawal, making it easier to rebalance effectively in 2025. Many investors are now turning to AI-driven rebalancing to automate these adjustments for better long-term growth.

Benefits of Tax-Free Trading

Accounts like traditional IRAs and 401(k)s create a tax-neutral space for portfolio adjustments. Here's what that means:

- No capital gains taxes on trades

- Greater flexibility to rebalance during market swings

- Taxes are postponed until funds are withdrawn

| Account Type | Rebalancing Flexibility | Tax Considerations |

|---|---|---|

| Traditional IRA | Broad trading opportunities | Taxes deferred until withdrawal |

| 401(k) | Varies by plan rules | Growth is tax-deferred |

This flexibility allows for strategic placement of assets, an essential step in improving overall tax outcomes.

Asset Location Planning

Placing assets strategically across different account types can help align investment characteristics with the best tax treatment.

Best Fit for Tax-Deferred Accounts:

- High-yield bonds that generate regular income

- REITs with frequent dividend payouts

- Actively managed funds with high turnover

- Investments requiring frequent trades

For instance, holding a high-yield bond fund in a tax-deferred account instead of a taxable one can reduce the tax burden on income while providing room for easier rebalancing.

Steps for Smarter Asset Placement:

-

Focus on Tax-Deferred Accounts

Use tax-deferred accounts for investments that produce steady taxable income or require frequent trading. This maximizes the benefits of deferring taxes. -

Assign Growth Assets to Taxable Accounts

Reserve your taxable accounts for long-term growth investments that generate minimal income. When sold, they can take advantage of lower long-term capital gains rates. -

Rebalance Strategically

Take advantage of tax-free trading within tax-deferred accounts to maintain your target allocation, especially during market volatility.

Mezzi's platform offers real-time tools to help you avoid wash sales and enhance tax efficiency, supporting your asset placement strategy.

Taxable Account Rebalancing Tips

Rebalancing taxable accounts requires careful planning to minimize taxes. Here are some strategies to help you rebalance efficiently while keeping tax liabilities in check.

Managing Cash Flow

One effective way to rebalance without triggering taxes is to use cash flow from your portfolio. By directing new contributions and reinvested dividends toward underweighted assets, you can adjust allocations without selling existing holdings.

Common cash flow sources include:

- Regular investment contributions

- Dividend payments

- Interest income

For instance, if your target allocation for U.S. stocks is 60% but your current holding is at 55%, you can direct new contributions into U.S. stock funds until the target is reached.

Additionally, tax-loss selling vs. capital gains deferral can help lower your tax burden further.

Steps for Tax-Loss Selling

- Spot Loss Positions

Look for investments trading below their purchase price that could offset realized gains. - Estimate Tax Savings

Match these losses against short-term and long-term gains to calculate potential tax benefits. - Plan Your Sales

Sell strategically to maximize tax savings while working toward your portfolio’s target allocation. - Reinvest Wisely

Be mindful of wash sale rules when reinvesting in similar securities.

Mezzi’s platform can provide real-time insights to help you identify tax-loss opportunities and avoid wash sales across multiple accounts.

Prioritizing Long-Term Holdings

Long-term holdings often come with tax advantages, thanks to lower capital gains rates. To make the most of these benefits, aim to hold investments for over a year whenever possible. If selling becomes unavoidable:

- Start by using new contributions to adjust allocations.

- Harvest tax losses to offset gains.

- When selling, prioritize positions held for less than one year, as they incur higher tax rates compared to long-term holdings.

"Actionable insights to reduce investment tax" - Mezzi

Each trade in a taxable account can create a taxable event, so it’s crucial to plan your rebalancing moves carefully to avoid unnecessary tax consequences.

Mezzi's Rebalancing Tools

Mezzi takes tax-efficient rebalancing to the next level by using advanced AI tools to simplify the process and improve after-tax returns.

Mezzi's Tax Savings Features

Mezzi's AI engine keeps a close eye on your portfolio, constantly looking for tax-saving opportunities during rebalancing. It evaluates holdings across multiple accounts to identify smart rebalancing strategies while helping you avoid costly tax errors.

Here are some standout features of Mezzi's tax optimization:

- Multi-Account Wash Sale Prevention: Automatically detects and flags potential wash sale issues across all your investment accounts.

- Tax-Impact Analysis: Analyzes the tax consequences of various rebalancing scenarios before trades are executed.

- Long-Term Growth Focus: Strategic rebalancing that compounds tax savings over time, boosting your portfolio's overall growth potential.

Key Rebalancing Functions

In addition to tax-saving features, Mezzi provides powerful tools to make portfolio management easier:

| Function | Benefit |

|---|---|

| Real-Time AI Prompts | Delivers actionable suggestions for tax-efficient trading decisions. |

| Portfolio Analytics | Offers a comprehensive view of your accounts and tracks allocation drift. |

| Trade Evaluation | Reviews the tax impact of rebalancing moves before execution. |

| Performance Tracking | Monitors tax savings and measures overall portfolio efficiency. |

"Actionable insights to reduce investment tax" - Mezzi

These tools allow you to maintain your target allocations effectively while optimizing your tax strategy at the same time.

Summary

Tax-optimized rebalancing offers major financial advantages in 2025. By strategically managing taxes, investors can grow their wealth more effectively. For instance, saving just 1% on taxes could add $186,877 to your retirement fund, while reinvesting a $10,221 tax saving could grow to $76,123 over 30 years.

This approach hinges on three key principles:

- Strategic Account Usage: Use tax-deferred accounts for frequent rebalancing to avoid immediate tax consequences.

- Smart Asset Location: Place tax-inefficient investments in tax-advantaged accounts to minimize tax exposure.

- Automated Monitoring: Rely on technology to track allocation drift and identify opportunities to save on taxes.

Modern tools, like Mezzi's AI-powered platform, simplify portfolio management by providing real-time monitoring and actionable insights. Users have found it helpful in avoiding wash sales across multiple accounts while streamlining complex rebalancing tasks.

"Actionable insights to reduce investment tax" - Mezzi

The success of tax-optimized rebalancing depends on consistent execution and careful tax planning. By combining these strategies with automated tools that offer ongoing analysis and recommendations, investors can lower their tax burden, maintain their asset allocation, and significantly enhance portfolio growth potential.

FAQs

What are the benefits of tax-optimized rebalancing for reducing my tax burden in 2025?

Tax-optimized rebalancing can help you minimize your tax burden in 2025 by strategically adjusting your investment portfolio to reduce taxable gains. By focusing on tax-deferred accounts like IRAs or 401(k)s, you can defer taxes on growth, while tax-loss harvesting in taxable accounts can offset gains.

These strategies not only help you keep more of your investment returns but also ensure your portfolio stays aligned with your long-term financial goals.

What are the benefits of using tax-deferred accounts for rebalancing, and how do they work?

Tax-deferred accounts, such as 401(k)s or IRAs, provide significant advantages for rebalancing your portfolio. One major benefit is that you can adjust your investments without triggering immediate taxes on any gains. This allows your portfolio to grow more efficiently over time, as taxes are deferred until you make withdrawals, typically in retirement.

By using these accounts for rebalancing, you can maintain your desired asset allocation while minimizing the impact of taxes. This strategy helps maximize the long-term growth potential of your investments, ensuring your financial goals stay on track.

What are the best ways to use tax-deferred accounts for rebalancing and optimizing portfolio performance in 2025?

To optimize your portfolio's performance while minimizing tax liabilities, focus on rebalancing within tax-deferred accounts, such as 401(k)s or IRAs. These accounts allow you to adjust your investments without triggering immediate tax consequences, making them ideal for maintaining your desired asset allocation.

By strategically managing gains and losses, you can further enhance tax efficiency. For example, prioritize selling assets in tax-deferred accounts to avoid capital gains taxes while using taxable accounts for tax-loss harvesting. This combined approach can help you grow your investments more effectively over time.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.