Your 401(k) could be impacted by fees without you noticing. Even a small difference in fees may reduce your account balance over time. For example, paying 2% annually instead of 0.5% could reduce your retirement savings by a significant percentage. Here's what you need to know to help manage your savings:

- Expense Ratios: These are the primary fees charged by fund managers. Low-cost index funds (0.05%-0.50%) are much cheaper than actively managed funds (0.75%+).

- Administrative Fees: Cover services like recordkeeping and legal work. Often hidden or bundled with other costs.

- Revenue-Sharing Costs: Embedded charges like 12b-1 or distribution fees can inflate your total costs.

To minimize fees:

- Review Fee Disclosures: Check your plan's 404(a) and 408(b) documents for detailed cost breakdowns.

- Choose Low-Cost Funds: Look for index funds with expense ratios below 0.50%.

- Ask for Better Options: Request institutional share classes or lower-cost alternatives from your employer.

- Consider an IRA Rollover: If fees are too high, an IRA may offer more affordable investment choices.

Small changes today may help you accumulate more over the long run. Reviewing your 401(k) fees may benefit you in the future.

401(k) Fees: What Costs Do You Pay? How to Save

How 401(k) Fees Are Structured

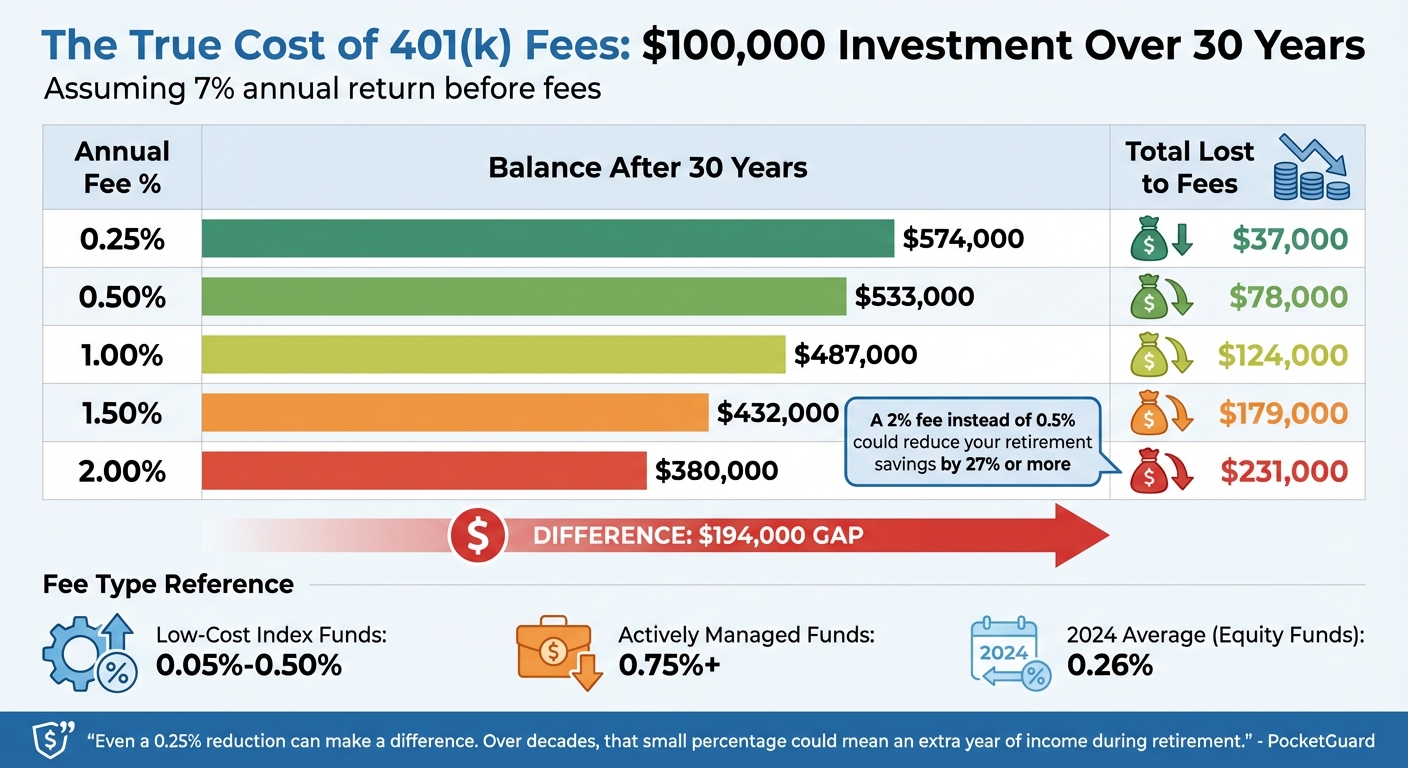

401(k) Fee Impact: How Expense Ratios Affect $100K Over 30 Years

Getting a handle on how 401(k) fees work - whether they’re investment, administrative, or individual service fees - is crucial for keeping tabs on your retirement savings. Each fee type may reduce your returns over time.

What Are Expense Ratios?

Expense ratios often make up the bulk of 401(k) costs. These are the annual percentage fees charged by fund managers to handle your investments. For example, if you have $50,000 in a fund with a 1% expense ratio, you’re paying $500 each year.

The gap between low-cost and high-cost funds becomes massive over time. Actively managed funds typically charge 0.75% or more, while passively managed index funds can cost as little as 0.05%. In 2024, the average expense ratio for equity mutual funds in 401(k) plans was 0.26%. If a fund charges over 1%, it may be considered costly relative to alternatives.

Here’s a breakdown of how different expense ratios impact a $100,000 investment over 30 years, assuming a 7% annual return:

| Annual Fee % | Balance After 30 Years | Total Lost to Fees |

|---|---|---|

| 0.25% | $574,000 | $37,000 |

| 0.50% | $533,000 | $78,000 |

| 1.00% | $487,000 | $124,000 |

| 1.50% | $432,000 | $179,000 |

| 2.00% | $380,000 | $231,000 |

"Even a 0.25% reduction can make a difference. Over decades, that small percentage could result in a higher account balance at retirement."- PocketGuard

But expense ratios aren’t the only costs to watch. Administrative and advisory fees can also reduce your savings.

Administrative and Advisory Fees

Administrative fees cover essential services like recordkeeping, accounting, and legal work. These fees might be charged as a flat rate per participant or as a percentage of your account balance.

For instance, The Cigna Group 401(k) Plan charged an annual administrative fee of 0.0130% of account balances in December 2023, with a cap of $90 per year. While this may seem small, not all plans are this upfront. Some bundle administrative fees with investment costs, making them harder to identify on your statements.

The size of your employer’s plan plays a big role in fee levels. Larger plans with 2,000 employees average a 0.78% total expense ratio, while smaller plans with just 25 employees average 1.35% - nearly twice as much. Smaller companies often lack the leverage to negotiate better rates.

Revenue-Sharing Arrangements

Revenue-sharing arrangements are deals where mutual fund companies return part of their expense ratio to the plan provider or recordkeeper to cover administrative expenses. These arrangements are often buried in 12b-1 fees, which are ongoing charges included in the expense ratio for marketing and distribution.

"The cumulative effect of the fees and expenses on your retirement savings can be substantial." - U.S. Department of Labor

A surprising number of participants - over one-third - mistakenly believe they don’t pay any fees at all. Revenue-sharing arrangements add to this confusion by embedding costs in ways that aren’t immediately obvious.

How to Find Hidden Fees in Your 401(k)

Understanding where fees hide is key to protecting your retirement savings. The good news? Your plan documents contain this information - if you know where to look. Let’s break down how to uncover these costs.

Reading Your Plan Fee Disclosures

Start by reviewing the 404(a) Participant Fee Disclosure, which provides a detailed comparison of expense ratios and shareholder-type fees for each investment option in your plan. To dig deeper, request the 408(b) Fee Disclosure, which outlines direct and indirect compensation, including revenue-sharing arrangements and other less obvious fees.

Another helpful resource is your Summary Plan Description (SPD). This document explains your plan’s rules and includes general details about administrative fees and individual service charges. For instance, before taking a loan or requesting a distribution, check your SPD for any flat-dollar fees tied to those transactions.

To see how fees impact your savings, calculate the annual cost by multiplying your balance by the total fee percentage. For example, if your account balance is $75,000 and your fees are 1.2%, you’re paying about $900 a year. Identifying these charges can help you make more informed decisions.

Next, dive into your fund prospectuses to uncover expense ratios and other hidden costs.

Finding Expense Ratios in Fund Prospectuses

Each investment option in your plan has a fund prospectus that outlines its expense ratio, management fees, and sales charges. Look for the "Fees and Expenses" section, particularly the "Total Annual Fund Operating Expenses" line. This figure often includes bundled costs like management fees, 12b-1 fees (used for marketing and distribution), and administrative expenses. These fees are deducted directly from your fund’s returns, making them easy to overlook.

Your quarterly statements will show the fees deducted over the last three months, but they usually don’t break down the individual components. That’s why reviewing fund prospectuses is essential. By identifying these costs, you can better understand how they affect your returns.

Beyond expense ratios, keep an eye out for revenue-sharing charges that might be inflating your overall costs.

Identifying Revenue-Sharing Costs

Revenue-sharing costs are often hidden within the returns of your investment options, rather than listed as separate fees on your statements. To find them, check the investment-related section of your annual fee disclosure notice.

Pay close attention to terms like 12b-1 fees, shareholder service fees, or distribution fees, which are ongoing charges for commissions and broker services. Another fee to watch for is the Sub-Transfer Agency (sub-TA) fee, which is a payment from the fund to the 401(k) provider for recordkeeping services.

Also, compare the share classes available in your plan. Retail share classes typically carry higher fees than institutional ones. Choosing lower-cost options can make a big difference in the long run.

"High 401(k) fees do not guarantee better results. They only guarantee you and your employees will keep less of your investment earnings." - David Ramirez, CFA, ForUsAll

Tools for Analyzing 401(k) Fees

Once you've reviewed your fee disclosures, it's time to dig deeper. Specialized tools can help you understand your fees and evaluate their long-term impact. While Mezzi offers a centralized approach, other tools provide additional insights and comparisons to industry benchmarks.

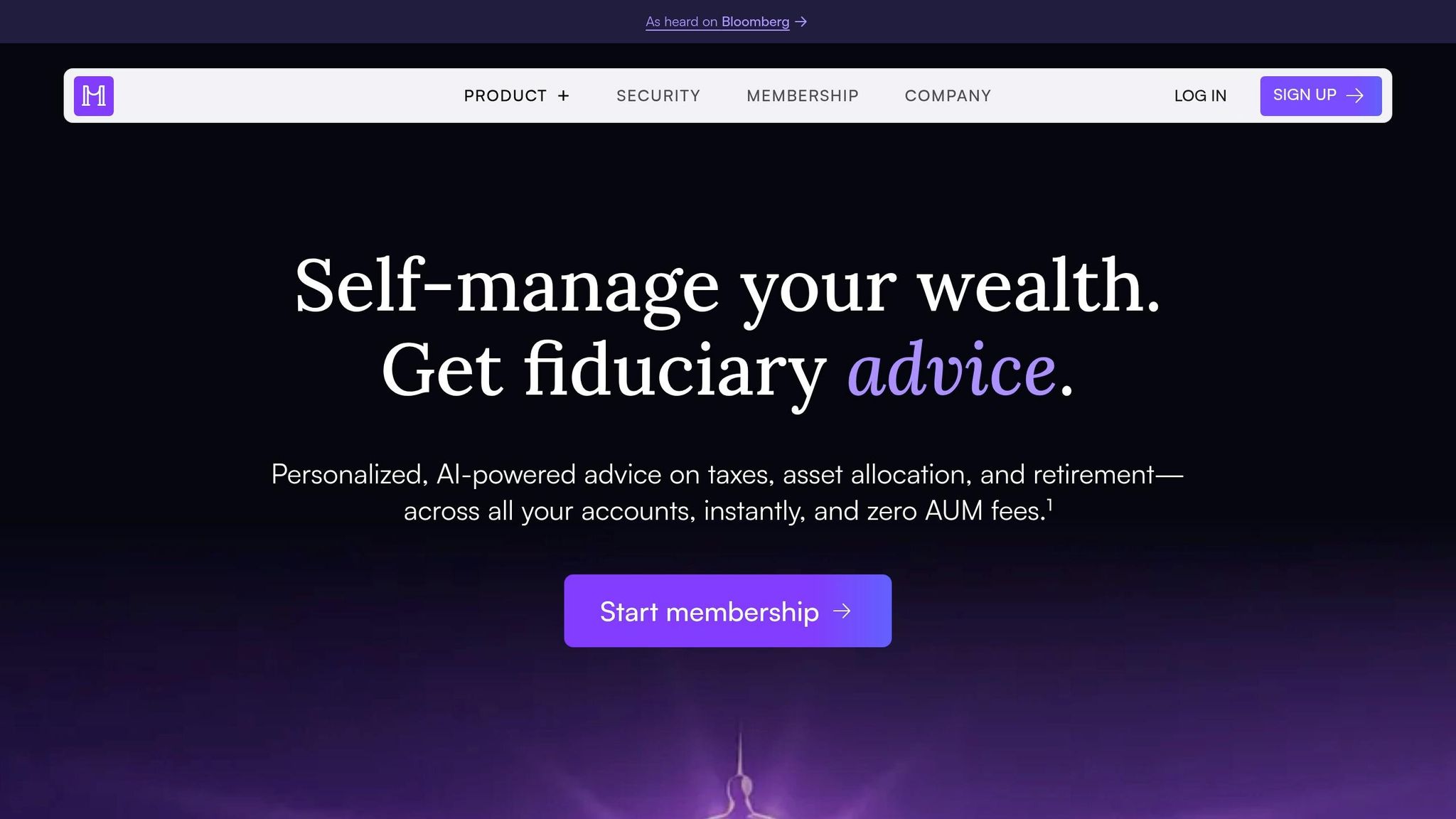

Using Mezzi to Analyze Your 401(k) Fees

Mezzi connects directly to your 401(k) account through secure, read-only access via third-party APIs. This gives you a clear, consolidated view of all your retirement accounts. The platform evaluates both percentage-based fees - like a 1% annual management fee - and flat charges, such as a $50 recordkeeping fee.

One of Mezzi's standout features is its ability to uncover hidden costs. These are expenses that might not be immediately obvious but can significantly impact your long-term savings. For example, Mezzi can compare your current fee structure to lower-cost alternatives, showing potential savings over time. By linking your accounts, it captures every fee detail, helping you see the total cost of your retirement plan.

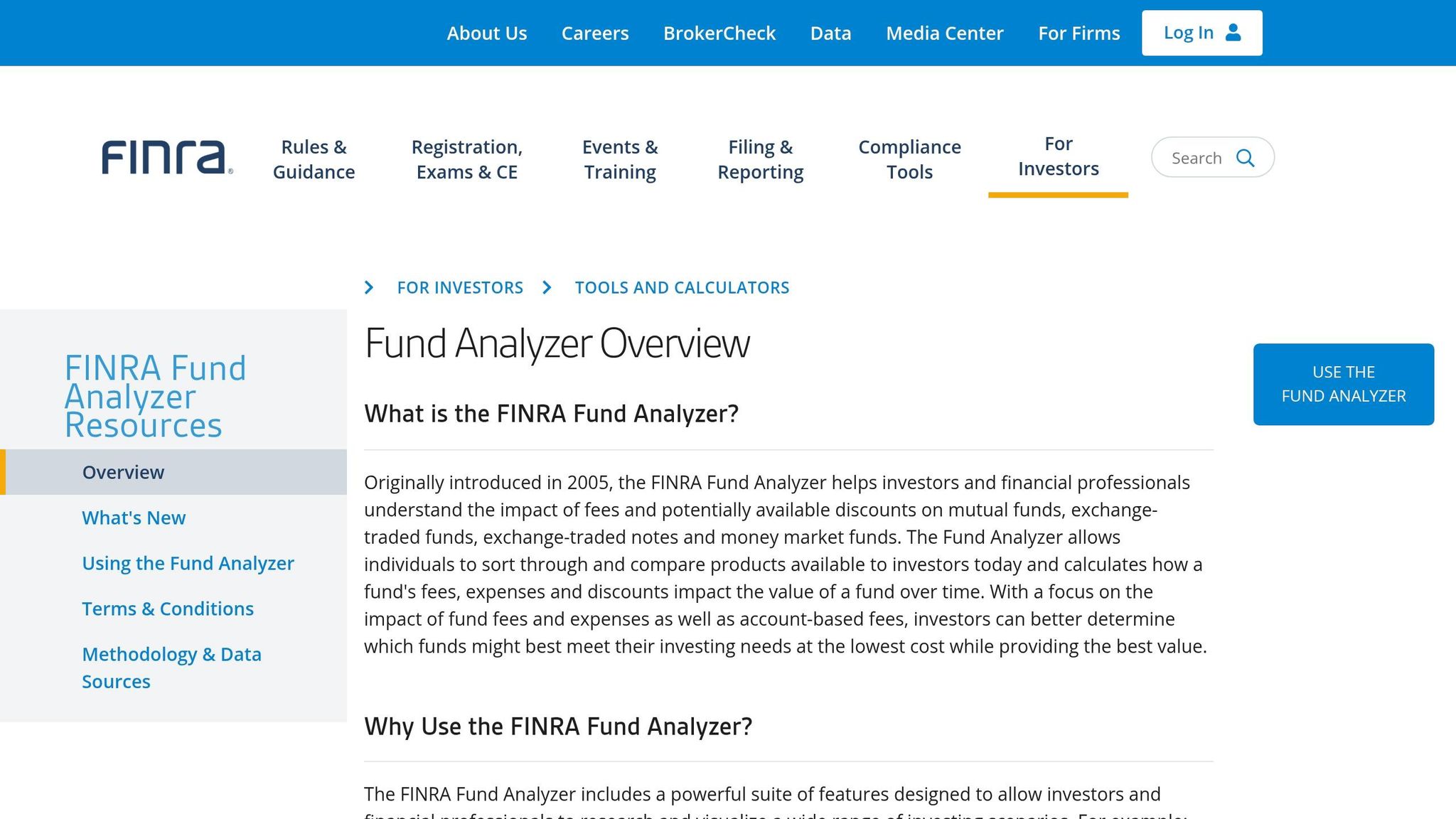

FINRA Fund Analyzer

For a second opinion, the FINRA Fund Analyzer is a great option. This free tool provides access to data on more than 30,000 mutual funds, ETFs, and ETNs. You can compare up to three funds side-by-side by entering their ticker symbols or names. The tool's default settings assume a $10,000 initial investment, a 5% annual return, and a 10-year time frame.

To fine-tune your analysis, use the Advanced Options to add advisory fees, flat fees, and contribution details. The analyzer also compares your fund's expense ratio to the average for similar funds in the same Morningstar category, helping you see if you're paying more than others.

"Even a seemingly small difference in fees can eventually add up to thousands of dollars." - FINRA

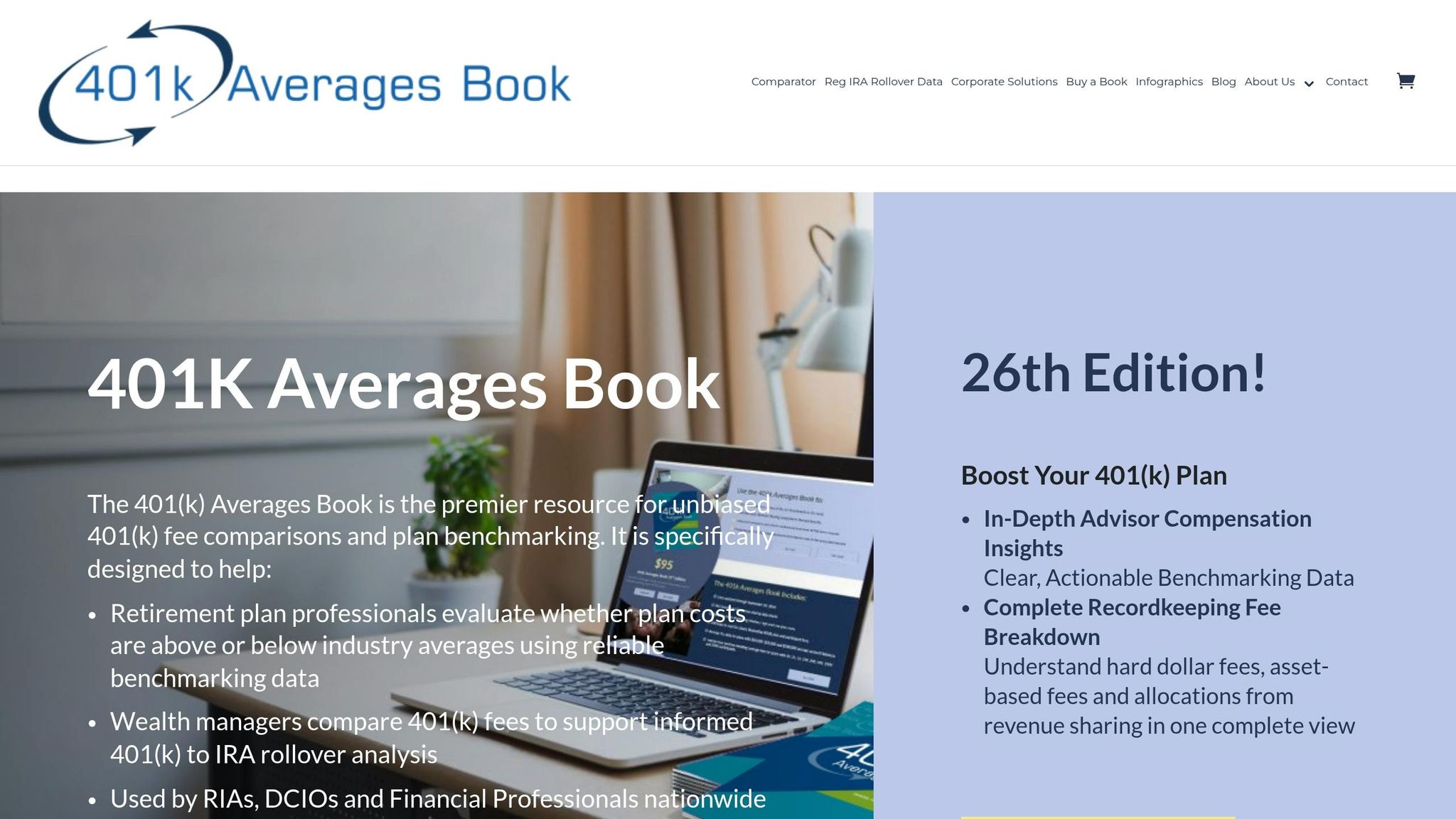

Comparing Fees with the 401(k) Averages Book

If you're looking for a broader perspective, the 401(k) Averages Book is a valuable resource. It provides benchmarking data broken down by plan size, with 288 fee charts organized into 24 sections. These charts include quartile breakdowns showing median, high, and low costs, making it easy to see how your plan stacks up against industry norms.

To use this resource effectively, match your plan to its peer group based on participant count and average account balance. This will help you determine if your fees are higher than average. The book covers a wide range of costs, including recordkeeping fees, asset-based fees, and revenue-sharing allocations. Armed with this data, you'll be better prepared to discuss potential cost-saving options with your plan administrator.

How to Reduce Your 401(k) Fees

Once you've identified hidden fees in your 401(k), it's time to take action. Even small reductions can save you tens of thousands of dollars over the course of your career. Here are three practical strategies to help you cut costs.

Choose Low-Cost Index Funds

Index funds are a great way to reduce fees. These funds don’t rely on expensive managers to pick stocks; instead, they track market benchmarks like the S&P 500. This simplicity translates into much lower expense ratios - often as low as 0.05%, compared to 0.75% or higher for actively managed funds.

To locate index funds in your plan, look for terms like "Index", "Passive", or "S&P 500" in your fund options. Focus on funds with expense ratios under 0.50%. For reference, the average expense ratio for equity mutual funds in 401(k) plans was 0.26% in 2024. If your plan offers "institutional" share classes or Collective Investment Trusts (CITs), prioritize those - they typically cost less than retail mutual funds.

Making the switch is straightforward. Log into your 401(k) portal, go to the "Investments" or "Rebalance" section, and select low-cost index funds for both future contributions and existing balances. Be sure to flag any fund with an expense ratio above 1.0% as a likely overpriced option that could be dragging down your returns.

Request Lower-Cost Fund Options

Your employer has a legal obligation under ERISA to ensure your 401(k) fees are reasonable. Many people don’t realize that mutual funds often come in multiple "share classes", and institutional versions are usually much cheaper. For instance, the R-6 shares of American Funds Growth Fund of America had a 1.27% higher annual return over five years compared to R-1 shares, as a result of lower fees.

Compare the funds in your plan to their lower-cost counterparts. Gather data on expense ratios and performance, then share this information with your HR department or plan administrator.

"Employers have a fiduciary responsibility to choose the lowest-priced share class available to their 401(k) plan – so avoidable investment fees don't reduce participant returns needlessly." - Eric Droblyen, President of Employee Fiduciary

Point out that they, too, will benefit from these changes as participants in the plan. Specifically, ask if your plan qualifies for institutional share classes. Many do, but providers don’t always make this clear. By advocating for these changes, you can help address one of the biggest sources of long-term savings erosion.

Consider an IRA Rollover

If your 401(k) options are limited to high-cost funds and your employer isn’t willing to make changes, rolling your funds into an IRA could be a smart move. IRAs offer access to a wide range of low-cost funds and ETFs, often at expense ratios much lower than those in smaller company 401(k) plans.

Before making the switch, check your Summary Plan Description (SPD) for any rollover fees, confirm whether employer-subsidized fees will carry over, and see if your 401(k) already includes institutional share classes.

If your 401(k) primarily offers high-cost actively managed funds (over 1.5%) and doesn’t include employer subsidies, an IRA rollover could reduce your fees. However, if you’re part of a large plan with institutional fund options, you may already have access to competitive pricing. A hybrid strategy might work best: contribute enough to your 401(k) to maximize the employer match, then direct any additional savings into a low-cost IRA.

"If you have a bad plan, invest enough to get the full employer match, if one is offered. Then invest outside of it." - Bob Morrison, Certified Financial Planner, Downing Street Wealth Management

Conclusion

Hidden fees in your 401(k) can quietly siphon away a significant portion of your retirement savings over time. In fact, just a 1% difference in fees over 35 years may result in a significantly lower final balance. That’s why even small, proactive steps today can make a huge difference in your financial future.

Start by checking your Annual 404(a)(5) Fee Disclosure Statement to get a clear picture of what you're paying. Pay close attention to any funds with expense ratios above 1.0%, and compare them to lower-cost alternatives, like index funds with expense ratios below 0.26% - the 2024 average for equity mutual funds in 401(k) plans. If your plan is filled with pricey actively managed funds, consider speaking with your HR department about adding institutional share classes. Alternatively, you might explore rolling over to an IRA for more affordable investment options.

"Every dollar lost to fees today is a dollar that won't compound for decades." - Eric Droblyen, President and CEO, Employee Fiduciary

The best part? You don’t need to be a financial guru to take action. Log into your 401(k) portal, switch to lower-cost funds, and set a reminder to review your fees at least once a year. During turbulent markets, even a quick quarterly review can help you stay on track.

Your retirement savings are too important to let high fees erode them. Consider reviewing your fees regularly to help manage your retirement savings.

FAQs

What’s a “good” all-in 401(k) fee percentage?

A reasonable all-in 401(k) fee is generally under 0.50%. For investments, aim for index funds with fees below 0.10% and target-date funds under 0.20%. Lower fees mean more of your money remains invested, which may help your account balance grow over time.

How can I tell if my plan is using revenue-sharing?

To find out if your plan involves revenue sharing, start by examining the plan’s fee disclosures. Key documents to review include the Participant Fee Disclosure and expense ratio details. These often highlight revenue-sharing arrangements, where mutual funds pay third parties - costs that are sometimes buried within the expense ratios.

If the information isn’t clear, reach out to your plan administrator. Request a detailed breakdown of fees and ask directly if revenue sharing is included in your investment costs.

When does an IRA rollover make sense to lower fees?

If your 401(k) comes with high costs - like hefty expense ratios, administrative fees, or management charges - an IRA rollover might be worth considering. These fees may reduce your long-term returns over time. By rolling over to an IRA with lower-cost investment options, you may be able to reduce fees and keep more of your money invested.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.