If I had to sum it up in one line: the best pick may depend on what makes your portfolio messy.

Some people may need tax and holding-level analysis. Others may need shared household tracking, private asset support, or equity-comp planning. This comparison looks at five tools - Mezzi, Empower, Monarch Money, Kubera, and Origin - across the points that may shape a net worth tracker choice most:

- Account syncing

- Holdings detail

- Private assets and debt

- Tax and fee visibility

- Price

Here’s the short version:

- Mezzi may fit investors who want a deeper view across taxable, retirement, and multi-custodian accounts.

- Empower may fit people who want a free dashboard with retirement projections and fee views.

- Monarch Money may fit couples and families who want one shared money view.

- Kubera may fit people with crypto, international accounts, and hard-to-track assets.

- Origin may fit high earners with RSUs, options, or ESPP and RSU decisions.

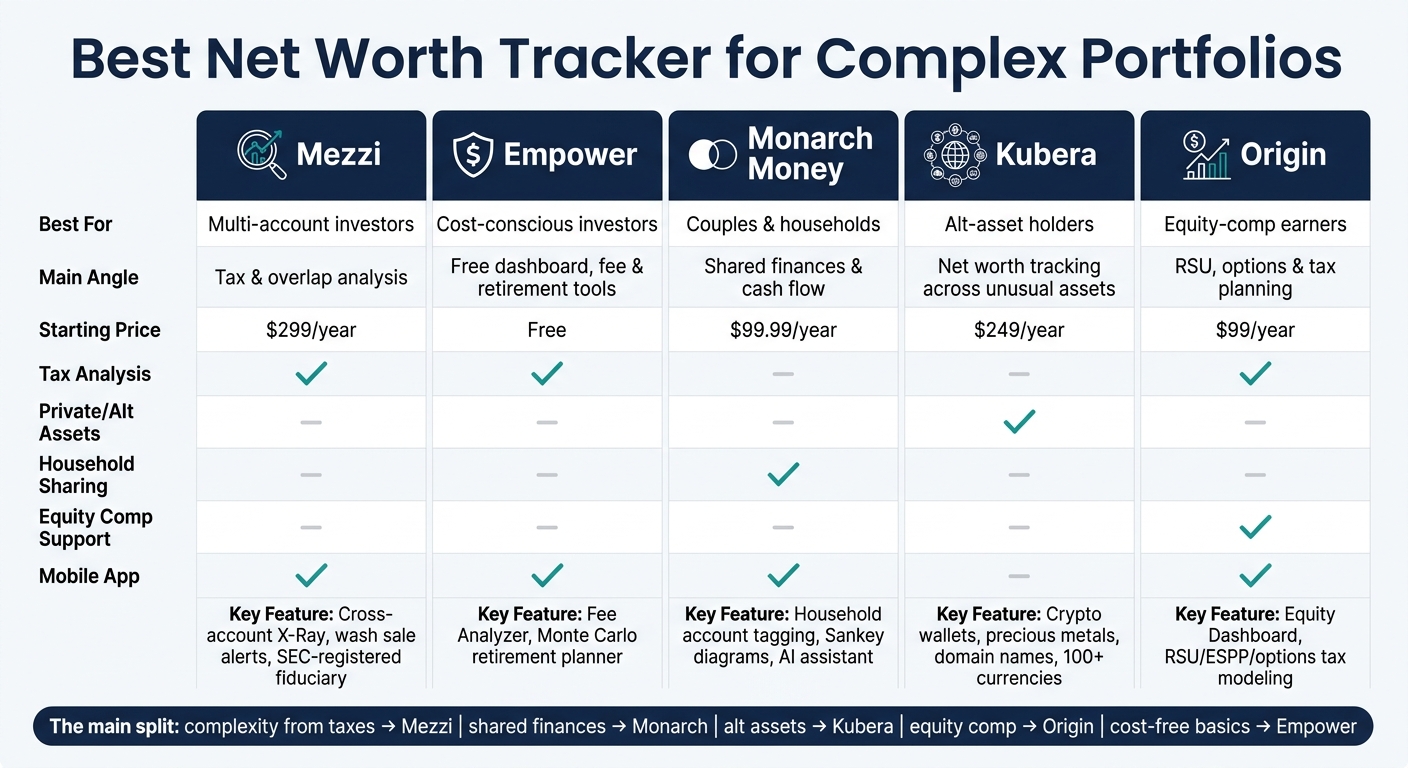

Best Net Worth Tracker for Complex Portfolios: Side-by-Side Comparison

6 Best Net Worth Tracking Apps of 2026 (Tested & Reviewed)

Quick Comparison

| Tool | May fit best for | Main angle | Starting price |

|---|---|---|---|

| Mezzi | Multi-account investors | Tax and overlap analysis | $299/year |

| Empower | Cost-conscious investors | Free dashboard, fee and retirement tools | Free |

| Monarch Money | Couples and households | Shared finances and cash flow | $99.99/year |

| Kubera | Alt-asset holders | Net worth tracking across unusual assets | $249/year |

| Origin | Equity-comp earners | RSU, options, and tax planning | $99/year |

The main split is simple: if your complexity comes from taxes, shared finances, alternative assets, or equity comp, a different tool may make more sense.

That framing may make the rest of the comparison much easier to read.

1. Mezzi

Mezzi is an SEC-registered fiduciary that connects to your accounts through Plaid and Finicity in read-only mode. That setup may give you a full portfolio view without requiring account transfers. It may pull taxable brokerage accounts, IRAs, 401(k)s, HSAs, 529s, and joint accounts into one dashboard. Once everything sits in one place, it may be easier to spot where your portfolio has concentration.

Mezzi’s Portfolio X-Ray takes account aggregation a step further by looking at exposure across your full portfolio. Say you hold VOO, VTI, and QQQ across a Fidelity taxable account and a Vanguard IRA. Mezzi may show your total Apple concentration across all of those holdings instead of viewing each account on its own.

On the tax side, Mezzi monitors positions daily and flags when positions become long-term. It also tracks wash sale risk, surfaces tax-loss harvesting opportunities, and leaves execution to your brokerage. The platform estimates these tax optimization insights may be worth $10,000–$20,000 per year on a $1 million portfolio. For some investors, that tax view may be useful when taxable accounts and retirement planning overlap.

Retirement planning in Mezzi uses your connected account data instead of generic assumptions. It factors in current balances, contributions, fees, and allocation across accounts to project timelines and suggest moves such as mega backdoor Roth contribution strategies. Pricing starts at $299/year for Core, $499/year for Plus, and $1,499/year for White Glove. Mezzi has a 9.33/10 consensus score based on 265 verified reviews.

A couple of caveats come up in reviews:

- Occasional Plaid re-authentication

- Higher pricing for portfolios under $50,000

That may make Mezzi a stronger fit for investors who want portfolio-level tax and concentration analysis, not just a simple account total.

2. Empower Personal Dashboard

Empower Personal Dashboard is free and links to major U.S. financial accounts, including checking, savings, 401(k)s, 403(b)s, IRAs, HSAs, mortgages, and loans, through Plaid, Finicity, and MX. For many investors with standard U.S. accounts, that may be enough to get a broad net worth snapshot.

Where it may feel tight is with more complex setups. Crypto tracking is manual-entry only. Private equity, business interests, and most alternative assets aren’t supported, and the platform is built for one user. For couples handling money together, the lack of shared views may feel limiting.

Empower’s Fee Analyzer may stand out the most. It turns fund expense ratios into a long-term dollar-cost estimate, which may make small fee gaps easier to see. In some cases, it may show how those differences add up over time.

The Retirement Planner uses Monte Carlo simulations to produce a "Retirement Score", which is framed as a probability estimate of whether your money may last through retirement based on your linked balances. Its allocation tool may also spot cash-like positions inside stock mutual funds, not just in money market accounts.

Empower may still work well for basic U.S. account aggregation, but the setup may start to break down once private assets or shared household finances are part of the picture. Users with more than $100,000 in linked assets may also hear from advisors, since the dashboard doubles as a path into Empower’s wealth management service, which charges 0.89% AUM on the first $1 million.

Empower has a 4.6/5 rating on the iOS App Store based on 366,000 reviews. Its limits may show up fastest in portfolios that include private assets, crypto, or shared household views.

3. Monarch Money

Monarch Money connects to more than 13,000 financial institutions. It pulls together cash, investments, debt, real estate, vehicles, crypto, and manually tracked assets. But the main draw may be its household setup, not just its account syncing. That may make it a better fit for couples and families trying to manage one shared balance sheet.

One of Monarch's strongest points may be collaboration. Couples may tag accounts as "Yours", "Mine", or "Ours" inside one shared view. That setup may make day-to-day money tracking feel a lot less messy.

Cash flow visibility may be where Monarch stands out most. Its Sankey diagrams show where money moves. It also includes a subscription manager and Flex Budgeting, which splits fixed and variable spending. On top of that, its AI assistant may answer natural-language prompts such as "How much did I spend on Amazon in Q3?" or "Project my net worth if I increase my 401(k) by 3%".

The compromise may show up on the investing side. Monarch pulls holdings, cost basis, and current values across linked accounts, and it tracks asset allocation and performance. But it does not include an automated fee analyzer. Its retirement planning is also limited to goal-setting, rather than actuarial or Monte Carlo modeling. So while its investing tools may work well for tracking, they may feel lighter than its budgeting and cash flow features.

At $99.99/year or $14.99/month, Monarch may fit households that want shared aggregation and tighter cash flow control. Investors looking for deeper fee analysis or retirement modeling may outgrow it. For readers who want deeper balance-sheet reporting, the next tracker takes a different angle.

4. Kubera

Kubera is a balance-sheet tracker built for assets and liabilities. If someone has money spread across a lot of places, it may work as a central balance-sheet hub, with syncing across more than 20,000 banks and brokerages through nine aggregators.

Where Kubera stands out may be the asset coverage. It includes items many trackers may skip, such as private equity, precious metals, domain names, and collectibles, and it places them alongside brokerage accounts as standard entries. On the crypto side, it connects directly to wallets and exchanges and tracks on-chain activity, including staking and lending.

That range matters, but so does the reporting. Kubera tracks position-level performance and calculates IRR for each asset. It also includes basic benchmarking against indexes like the S&P 500. The analytics stay fairly light by design. There are no advanced risk metrics, automated fee analysis, or tax-loss harvesting. In plain English: it tracks value, not deep performance analysis.

Kubera also uses a privacy-first model, with no ads or data monetization. Pricing starts at $249/year. Kubera Black starts at $2,499/year, and there’s a 14-day trial for $1.

For investors who want a clean view of everything in one place, Kubera may be a better fit than tools built around active tax or fee analysis. It may be strongest as a consolidation tool; the next tracker leans more toward planning.

5. Origin

Origin brings together net worth tracking, equity compensation, and tax modeling in one dashboard. It connects through Plaid, MX, and Mastercard to pull in banking, investment, retirement, and loan data automatically, so balances may update without manual entry. It also supports real estate and manual assets like crypto and vehicles.

That setup may make Origin a closer fit for high earners whose net worth may be tied to equity compensation and tax choices.

Where Origin stands apart from many trackers is equity compensation. Its dedicated Equity Dashboard tracks RSUs, stock options, and ESPP tax scenarios. It may also model the tax impact of selling concentrated stock.

Beyond equity, Origin also includes tax-aware planning. It offers tax-aware simulations for financial decisions and asset-location analysis across Roth, Traditional, and taxable accounts.

The tradeoff comes down to focus. Origin covers a lot, but its portfolio analytics may feel lighter than those of dedicated portfolio analyzer tools, especially for fee scanning. The standard membership costs $12.99 per month or $99 per year. Basic wills are included, with Full Wills and Trusts offered as add-ons for $149 and $449.

For investors looking for an all-in-one hub with equity support and tax-aware planning, Origin may be a strong match. If the main goal is the deepest possible portfolio analysis, it may feel more general-purpose than specialized. The next comparison shows where that broader scope may help and where lighter portfolio analytics may matter more.

Side-by-Side Comparison

The fastest way to narrow this down may be portfolio complexity: plain-vanilla U.S. accounts, shared household finances, alternative assets, or planning that leans tax-aware.

Account Aggregation

For standard U.S. accounts, Empower and Mezzi may cover the most ground. Kubera may reach furthest into less typical territory, including international accounts and crypto. Monarch Money appears built more around household sharing than deep portfolio aggregation. Origin seems more focused on equity compensation and tax planning than broad account coverage.

Once aggregation is in place, the next test may be holdings accuracy.

Holdings Accuracy and Portfolio Reporting

Mezzi's X-Ray tool may surface cross-account overlap that standard dashboards miss. Empower may be the strongest free option for broad portfolio analytics. Monarch Money appears stronger on household cash flow than portfolio analysis. Kubera covers international and crypto holdings, but its analytics stay light by design.

After that, the next question may be how each tool deals with private assets and liabilities.

Private Assets and Complex Liabilities

Kubera may be the clearest fit for alternative and physical assets, including precious metals, international accounts, and DeFi holdings. Mezzi explicitly supports trusts alongside standard investment accounts. Empower handles mortgages and loan syncing well. Monarch Money offers limited alternative-asset support. Origin appears aimed at high earners whose main complexity comes from equity compensation rather than physical or private assets.

The last tradeoff may come down to tax-aware planning versus a clean net worth view.

Tax-Aware Insights and Fee Analysis

Mezzi appears strongest on tax-aware portfolio analysis across taxable and retirement accounts. Empower may lead on free fee analysis. Kubera tracks complex assets well but offers little tax optimization. Monarch Money also offers little tax optimization. Origin includes equity-specific tax modeling, which may make it the strongest fit for RSU and stock option holders.

| Criterion | Mezzi | Empower | Monarch Money | Kubera | Origin |

|---|---|---|---|---|---|

| Account aggregation | Broad U.S. account coverage; strongest for taxable + retirement combos | Broad U.S. account coverage; real estate valuation | Household-first; shared account views | Widest nonstandard coverage; international and crypto | Equity compensation and tax-planning focus |

| Holdings accuracy / portfolio reporting | Cross-account overlap analysis | Strongest free option for broad portfolio analytics | Stronger on cash flow than portfolio analysis | International and crypto holdings; light analytics | Equity dashboard; lighter general portfolio reporting |

| Private assets and liabilities | Trusts; standard investment and retirement accounts | Mortgages and loan syncing | Limited alternative-asset support | Precious metals, international accounts, DeFi | Equity compensation; less focus on physical or private assets |

| Tax-aware insights | Cross-account tax-loss harvesting, wash sale tracking, asset-location guidance | Fee analysis; retirement modeling | Offers little tax optimization | Offers little tax optimization | Equity tax modeling; RSU and stock option scenarios |

| Pricing | From $299/year | Free | $99.99/year | $249/year | $99/year |

| Mobile app | Yes | Yes | Yes | Web-based | Yes |

Pros and Cons

The table below gives you the fastest way to match a tracker to the kind of portfolio you may have. The big tradeoff usually comes down to one thing: tax analysis, household coordination, alternative assets, or equity compensation.

This is a quick fit check. It shows where each tracker may stand out, and where it may fall short.

| Product | Pros | Cons | Best For |

|---|---|---|---|

| Mezzi | Cross-account tax optimization guidance, wash sale alerts across multiple accounts, X-Ray overlap tool, SEC-registered fiduciary, no data selling | Higher starting price ($299/year) | High earners managing taxable and retirement accounts who may want advisor-level guidance without the AUM fee |

| Empower Personal Dashboard | Free dashboard, strong retirement planner, fee analyzer | Paid advisory services start at 0.89% AUM for portfolios with at least $100,000; limited private asset support; lacks deeper portfolio analysis | Investment-heavy portfolios that may need solid retirement modeling at no cost |

| Monarch Money | Connects to over 13,000 financial institutions, excellent household budgeting | Basic retirement modeling; occasional sync issues with smaller institutions; limited tax optimization | Households managing shared finances alongside investment tracking |

| Kubera | Tracks alternative assets like domain names, precious metals, DeFi, and global accounts; supports 100+ currencies | Web-only with no native mobile app; no budgeting tools; expensive at $249/year | International investors or those holding major alternative and physical assets |

| Origin | All-in-one planning with equity-comp and tax modeling | Too broad for users who only want net worth tracking; no free tier | Users who may want a full planning ecosystem rather than a basic tracker |

The main divide is pretty simple: tax-aware analysis, household coordination, alternative-asset coverage, or equity-comp planning.

Final Verdict: Which Tracker Fits Your Situation

The best tracker may depend on how your portfolio is set up.

If you're a hands-on investor with taxable, retirement, and equity-comp accounts across more than one custodian, Mezzi may be the best fit for multi-custodian taxable and retirement investors. Its X-Ray view may surface overlap across accounts, while wash sale alerts and tax insights are designed to help manage concentrated positions and RSUs. At $299/year, it may be cost-effective for investors who want portfolio-level analysis instead of handling everything by hand.

If the main source of complexity comes from multiple people, not multiple account types, the better fit may change.

For couples or households, Monarch Money may fit shared budgeting and a single household view better than deep investment analysis.

If the hard part comes from unusual assets instead of shared spending, another option may make more sense.

If your portfolio includes crypto, domain names, precious metals, or other alternative assets, Kubera is built for that breadth, not for mobile-first convenience.

Across these tools, the deciding factor may not be net worth alone, but the kind of complexity behind it.

The more tax-sensitive and multi-custodian your portfolio may be, the more analytical depth may matter.

FAQs

How complex does my portfolio need to be to justify a paid tracker?

Usually, a paid tracker may make more sense when your portfolio spans multiple accounts, asset classes, and includes private or alternative investments.

That’s often the point where a paid tool may feel more useful. It may offer better accuracy, broader asset coverage, and tax-aware insights that simpler tools may not handle as well.

If your finances are straightforward, or only moderately diversified, a free or simpler tool may be enough. A paid tracker may be easier to justify as complexity grows across brokerages, retirement accounts, and private assets.

What accounts should sync correctly for accurate net worth?

For a more accurate net worth view, all of your financial accounts may need to sync correctly, including:

- bank accounts

- investment and retirement accounts, such as 401(k)s, IRAs, and Roth IRAs

- loans and credit cards

- real estate holdings via Zillow

- private or alternative assets like real estate syndications, cryptocurrencies, collectibles, and vehicles

How do I choose between tax analysis, household tracking, and private asset support?

Choose based on your portfolio’s main need.

Tax analysis may be a better fit for people who want a closer look at taxes across multiple accounts. Household tracking may suit people who want one place to view net worth, assets, liabilities, real estate, and cash flow. Private asset support may matter more if you hold real estate, private equity, or other alternative investments.

Put simply, it may make sense to put the most weight on the feature tied to what you want to monitor most closely.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.